May 15, 2026

Understanding Energy Chokepoint Vulnerabilities Through Strategic Risk Assessment

Global energy markets operate within an intricate web of dependencies where physical geography, technological limitations, and geopolitical tensions converge to create systemic vulnerabilities. These chokepoints represent more than shipping lanes or pipeline routes—they function as pressure points where disruption can cascade through interconnected systems, affecting everything from manufacturing supply chains to strategic military capabilities.

The concentration of critical energy transit through narrow geographic corridors creates asymmetric leverage opportunities for regional powers while exposing consuming nations to supply shock scenarios that traditional economic models struggle to predict or mitigate. Furthermore, this concentration risk extends beyond immediate price volatility, influencing long-term investment patterns, technological development priorities, and geopolitical alliance structures.

When examining recent supply disruption events, particularly those involving major transit chokepoints, several patterns emerge that challenge conventional assumptions about market resilience and alternative route capacity. The psychological premiums embedded in energy pricing reflect not just current supply-demand fundamentals, but expectations about future vulnerability scenarios and the adequacy of existing backup systems.

When big ASX news breaks, our subscribers know first

Economic Cascade Effects During Critical Transit Disruptions

Energy supply interruptions through major transit chokepoints generate economic impacts that extend far beyond immediate commodity price increases. The Strait of Hormuz blockade scenario demonstrated how approximately 20% of daily global trade flowing through a single waterway creates systemic dependencies that amplify throughout interconnected markets.

During the recent three-week closure period, oil futures outlook showed prices exceeded $100 per barrel while natural gas prices in Europe doubled from pre-crisis levels. Asian spot LNG prices reached multi-year highs as supply competition intensified across regions.

These price movements reflected not just physical supply constraints, but market psychology responding to uncertainty about resolution timelines and alternative supply activation. Consequently, the ripple effects extended into refined products and industrial inputs, with Asian refiners paying unprecedented premiums for non-Middle Eastern crude while simultaneously reducing processing rates to manage supply uncertainties.

Several countries implemented fuel-preserving measures, including four-day work weeks and fuel export bans, indicating how energy disruptions quickly translate into broader economic restrictions. The economic impact analysis reveals how these measures become necessary when critical supply routes face extended disruptions.

Manufacturing and Industrial Supply Chain Impacts

Chokepoint disruptions affect petrochemical feedstocks, fertilizer production, and manufacturing supply chains dependent on Gulf-region hydrocarbons. These impacts create secondary shortages across agricultural, chemical, and manufacturing sectors that often persist longer than the original energy supply disruption.

In addition, tariff impact on supply chains becomes more pronounced during energy crises. In the United States, despite domestic energy production capabilities, gasoline prices approached $4 per gallon, representing more than $1 per gallon increase compared to one month prior to the crisis.

This demonstrates how global energy markets create price transmission effects even in supposedly energy-independent regions. For instance, manufacturers dependent on chemical feedstocks face compounding pressures from both energy price increases and supply chain disruptions.

Regional Vulnerability Variations

Europe faced particular challenges as the gas refilling season became severely constrained, with Asia outbidding European buyers for spot LNG supply. Moreover, Qatar's LNG facility disruptions potentially eliminated full capacity for up to five years, fundamentally altering global LNG market dynamics and forcing European utilities to compete for limited alternative supplies.

The crisis revealed fundamental infrastructure gaps where producers began slashing output due to lack of storage capacity, creating additional delays in supply recovery even after transit route restoration. However, natural gas forecasts suggest that this storage constraint factor often receives insufficient attention in scenario planning but proves critical during extended disruptions.

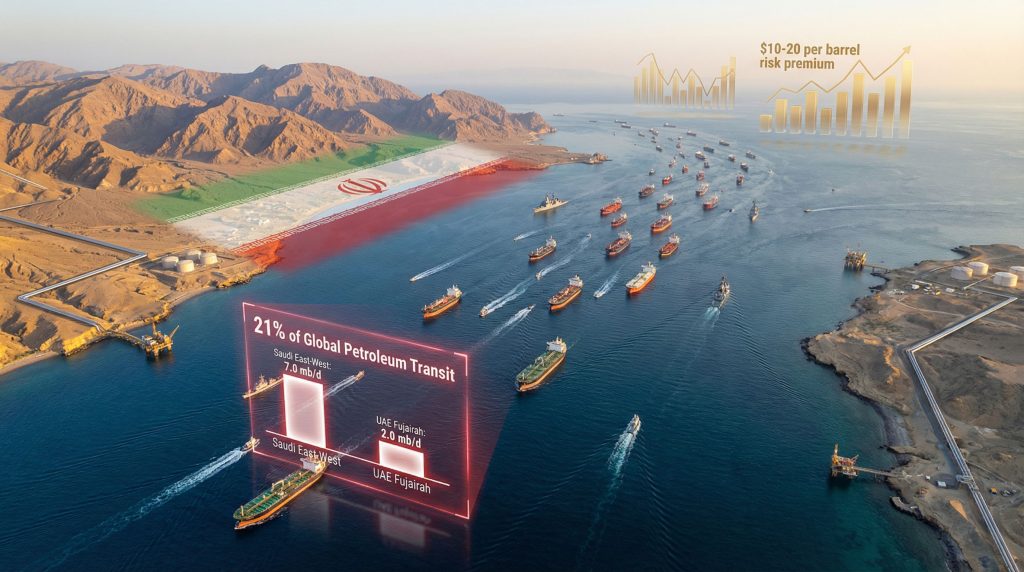

Alternative Route Capacity Analysis and Infrastructure Limitations

Current bypass infrastructure demonstrates significant inadequacy when measured against normal transit volumes through primary chokepoints. Furthermore, the combined capacity of major pipeline systems reveals substantial gaps between available alternatives and typical flow requirements.

Bypass Infrastructure Capacity Overview:

• Saudi Arabia's East-West Pipeline: 7.0 million barrels per day maximum capacity, currently operating at approximately 65% utilization

• UAE's Fujairah Route: 2.0 million barrels per day capacity with 75% current utilization

• Iraq-Turkey Pipeline: 0.6 million barrels per day capacity operating at 40% utilization due to political instability

• Total Available Bypass Capacity: 9.6 million barrels per day representing less than half of typical chokepoint flows

Geographic and Political Constraints

Alternative routes face their own vulnerability profiles, with the East-West pipeline exposed to Red Sea security risks and the Fujairah route constrained by limited storage capacity. In addition, the Iraq-Turkey route demonstrates how political instability can reduce effective capacity below technical maximums.

Expanding bypass infrastructure to handle full chokepoint traffic would require decades of investment and international coordination, with costs potentially exceeding $200 billion globally. Consequently, these timelines far exceed typical geopolitical crisis durations, creating persistent vulnerability windows.

Regional Refining Strategy Limitations

Middle Eastern nations have increasingly focused on domestic refining capacity to reduce crude export dependency. However, Saudi exploration dynamics show this strategy creates new vulnerabilities as refined products often require the same transit routes and face similar chokepoint risks while reducing flexibility in global supply chain management.

The concentration of refining capacity in specific regions can exacerbate supply disruptions when those facilities become inaccessible or when their products cannot reach destination markets through disrupted transit routes.

Market Psychology and Price Discovery Mechanisms

Oil futures markets demonstrate extreme sensitivity to chokepoint-related disruptions, with price volatility often exceeding fundamental supply-demand imbalances. Furthermore, the psychological premium associated with chokepoint risks can add significant per-barrel costs even during minor incidents or threat escalations.

Recent market behavior showed that oil prices reflect fundamentals but have been driven by hectic trading activity on geopolitics, indicating how speculative trading and risk assessment mechanisms amplify price movements beyond what supply-demand fundamentals alone would justify.

Strategic Reserve Deployment Challenges

Government-controlled strategic reserves serve as primary shock absorbers during supply disruptions, yet their effectiveness faces coordination challenges and political constraints that limit deployment during extended crises. The lack of available resources to plug Middle Eastern supply gaps demonstrates how even substantial strategic reserves prove insufficient during major chokepoint closures.

Reserve release mechanisms require international cooperation and face political considerations that can delay or reduce effectiveness when rapid market response is most critical. Consequently, these delays often allow speculative trading to drive prices beyond levels that physical supply shortages would justify.

Algorithmic Trading and Risk Premium Calculations

Financial markets price chokepoint risks through complex algorithms factoring geopolitical tensions, military capabilities, and historical precedents. These calculations create feedback loops where political rhetoric and military positioning can trigger significant price movements independent of actual supply disruption.

The characterisation of recent events as the worst disruption in oil market history reflects how market participants assess both physical supply impacts and precedent-setting effects for future crisis scenarios. For instance, the OPEC meeting impact on pricing becomes more pronounced during periods of heightened geopolitical tensions.

Geopolitical Leverage Through Resource Control

Regional powers increasingly utilise energy chokepoint control as strategic leverage, with recent events demonstrating how whoever controls major transit routes has enormous leverage on inflicting global economic pain. This dynamic has transformed energy infrastructure from economic assets into tools of geopolitical influence.

Iran's Strategic Positioning and Naval Capabilities

Iran's military doctrine emphasises asymmetric naval warfare designed specifically for chokepoint scenarios, including swarm boat tactics, coastal missile systems, and mining capabilities that leverage geographic advantages over conventional naval forces. Moreover, these capabilities create persistent threat scenarios that influence market psychology even during peaceful periods.

The military options analysis highlights how geographic advantages can offset technological disparities in chokepoint control scenarios. The effectiveness of asymmetric strategies against conventional naval responses demonstrates the complexity of reopening blocked waterways.

Resource Concentration Beyond Energy

China's dominance in critical minerals demonstrates parallel chokepoint dynamics beyond traditional energy markets. China holds a 59% share of rare earths mining, 91% of refining, and 94% of magnet manufacturing, creating supply concentration risks across defence and automotive industries.

China's restrictions on rare earth exports early in 2025 exemplified how resource control creates strategic leverage across multiple sectors. This approach transforms raw material access into geopolitical bargaining power comparable to traditional military capabilities.

Western Response Strategies

The United States has responded through Project Vault, a Strategic Critical Minerals Reserve initiative, while taking stakes in minerals mining companies and leading efforts to break Chinese stronghold on pricing mechanisms for defence-critical materials.

However, rising neodymium-praseodymium supply from countries like the United States and Australia is projected to reduce China's market share to 69% by 2030 from 90% in 2024, indicating gradual supply chain diversification despite significant timeline constraints.

Long-term Energy Architecture Transformation

Persistent chokepoint vulnerabilities accelerate structural changes in global energy architecture, driving investment patterns toward route diversification and alternative energy systems. However, meaningful transition timelines extend decades beyond typical geopolitical crisis durations, creating sustained periods of vulnerability during infrastructure development phases.

Technological Solutions and Implementation Challenges

Advanced surveillance systems, autonomous shipping, and alternative energy vectors represent potential technological solutions to chokepoint vulnerabilities. Nevertheless, implementation costs and international coordination requirements create substantial barriers to rapid deployment across global shipping networks.

Maritime security technology development gains additional strategic value during supply disruption scenarios, but the integration of new technologies into existing shipping infrastructure requires extensive validation and regulatory approval processes.

Trade Pattern Reshaping

Persistent chokepoint risks encourage trade route diversification and regional energy market development, potentially accelerating the emergence of separate energy trading blocs that reduce global market integration. This fragmentation could create efficiency losses while providing regional security benefits.

The development of alternative payment systems and trading mechanisms for energy transactions reflects how chokepoint vulnerabilities influence financial infrastructure beyond physical supply chain considerations.

Investment Timeline Considerations

Energy infrastructure projects offering chokepoint bypass capabilities often require lead times as long as 10 years to get new material out of the ground, creating significant gaps between investment decisions and operational capacity delivery.

These extended development timelines mean that current Strait of Hormuz blockade vulnerability scenarios will persist well into the future, regardless of immediate investment commitments. This supply shortfall due to trade uncertainties gives pricing power to the few producers currently able to supply critical materials outside of traditional chokepoint-dependent routes.

The next major ASX story will hit our subscribers first

Strategic Investment Frameworks for Energy Security

Investment opportunities exist across bypass infrastructure, strategic storage facilities, and alternative energy systems that offer long-term returns while contributing to global energy security. These projects gain additional strategic premiums during periods of heightened chokepoint vulnerability.

Infrastructure Development Priorities

Pipeline and storage facility development represents primary investment categories, though returns often depend on sustained political support and international coordination that can span multiple electoral cycles. Cost-benefit analyses must factor both commercial returns and strategic security premiums.

Regional energy independence projects gain additional value during supply disruption scenarios, creating investment premiums for renewable energy technologies and domestic resource development that reduce import dependency through vulnerable transit routes.

Technology Sector Opportunities

Companies developing maritime surveillance, autonomous systems, and naval defence technologies benefit from increased security spending driven by chokepoint concerns. However, these markets face concentrated customer bases and regulatory constraints that influence commercial viability.

The fracturing of globalised markets creates opportunities for technology providers offering supply chain diversification solutions, though these often require substantial capital commitments with extended payback periods.

Investment Disclaimer: The analysis presented examines strategic energy security considerations and should not be construed as specific investment advice. Geopolitical scenarios involve substantial uncertainties, and investment decisions should consider individual risk tolerance and professional financial guidance. Energy infrastructure investments typically involve extended development timelines and regulatory risks that may affect returns substantially.

Looking to Capitalise on Energy Infrastructure Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across critical materials sectors, helping investors identify opportunities in companies developing alternatives to traditional energy supply chains. With strategic minerals becoming increasingly vital for energy security, subscribers gain actionable insights into exploration breakthroughs that could reshape global resource dependencies and begin their 14-day free trial today to position themselves ahead of these transformative market shifts.