June 21, 2026

Global energy infrastructure faces an unprecedented stress test as geopolitical tensions expose the fragility of interconnected supply networks spanning continents. Modern economies depend on energy flows that traverse narrow maritime corridors, creating systemic vulnerabilities that can trigger cascading disruptions across multiple sectors when threatened. The concentration of critical energy transit through strategic chokepoints represents one of the most significant structural risks facing the global economy today.

Understanding Critical Energy Transportation Vulnerabilities

Maritime energy transportation systems demonstrate remarkable efficiency under normal operating conditions but reveal dangerous concentration risks during periods of geopolitical instability. These vulnerabilities stem from geographic constraints that force massive volumes of energy commodities through narrow waterways, creating single points of failure for global supply chains.

Strategic Importance of Persian Gulf Energy Corridors

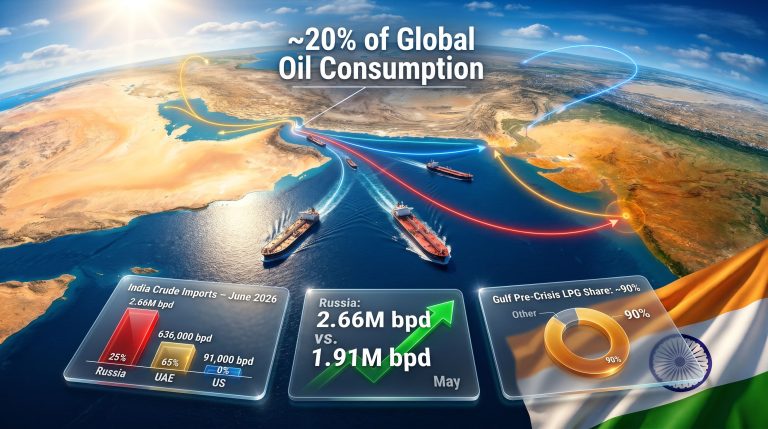

The Strait of Hormuz shipping halt demonstrates how quickly energy security can deteriorate when critical transportation arteries face disruption. Current data indicates this strategic waterway normally facilitates the transit of approximately 21% of worldwide petroleum liquids and nearly 25% of global liquefied natural gas flows. Under typical operating conditions, more than 20 million barrels of crude oil pass through this corridor daily, representing an energy volume that alternative transportation networks cannot readily replace.

Alternative route limitations become apparent during crisis periods, with overland pipelines handling less than 15% of regional capacity compared to maritime transportation. This infrastructure imbalance creates immediate supply constraints when shipping routes face security threats, forcing energy markets to operate under severe scarcity conditions. Furthermore, oil price stagnation analysis reveals how structural vulnerabilities compound existing market pressures.

Economic Multiplier Effects Beyond Energy Markets

Supply chain disruptions extend far beyond petroleum markets, affecting manufacturing costs, transportation expenses, and consumer goods pricing across diverse economic sectors. Energy price volatility transmits through interconnected systems via multiple channels:

- Direct fuel cost increases affecting transportation and logistics networks

- Manufacturing input cost escalation impacting energy-intensive production processes

- Insurance premium surges affecting commercial shipping and cargo financing

- Currency market volatility as energy-importing nations face balance of payments pressures

- Inflation acceleration through energy-dependent goods and services pricing

The current crisis demonstrates these transmission mechanisms in practice, with energy buyers worldwide scrambling to diversify supplies as key export terminals go offline and maritime risk reaches elevated levels. Additionally, understanding trade war oil impact becomes crucial when assessing broader market dynamics during geopolitical tensions.

When big ASX news breaks, our subscribers know first

How Maritime Security Threats Transform Energy Market Dynamics

Financial markets exhibit extreme sensitivity to geopolitical events affecting critical infrastructure, with energy commodities experiencing rapid price movements that often exceed fundamental supply-demand calculations. The Strait of Hormuz shipping halt exemplifies this phenomenon, where market psychology amplifies physical disruptions through speculative trading and risk-averse positioning.

Immediate Market Response Patterns During Transportation Disruptions:

| Market Segment | Typical Price Response | Duration of Impact | Current Crisis Example |

|---|---|---|---|

| Brent Crude Oil | 8-15% spike within 24 hours | 2-4 weeks | Multi-month highs reached |

| Natural Gas (Europe) | 12-25% increase | 1-3 months | Sharp price surges reported |

| Shipping Rates | 50-100% premium | 4-8 weeks | Dozens of tankers halted |

| Energy Equity Indices | 3-8% volatility increase | 2-6 weeks | Extended volatility expected |

War Risk Insurance Market Mechanics

Insurance markets respond immediately to maritime security threats, with war risk premiums escalating dramatically during active conflict periods. War risk insurers halt Strait of Hormuz cover entirely for affected regions, creating cascading effects on shipping economics and cargo financing. Premium rates can increase 10-50 times normal levels during active hostilities, while coverage exclusion zones eliminate insurance availability for specific geographic areas entirely.

Fleet immobilization effects create artificial capacity constraints as commercial vessels avoid designated risk zones, extending transit times and reducing available tonnage for global energy transportation. Charter rates for tankers typically increase 200-400% during major disruption periods, reflecting both physical constraints and risk premiums demanded by vessel operators.

Market Assessment Suspension Protocols

Price discovery mechanisms face severe challenges during extreme volatility periods, leading major assessment firms to suspend trading activities rather than publish potentially misleading valuations. S&P Global Platts suspended price assessments for Middle East crude, refined products, and liquefied natural gas shipping through affected waterways, indicating market uncertainty exceeded traditional pricing frameworks.

This suspension represents a critical safeguard preventing artificial price formation during periods when normal supply-demand relationships become distorted by security concerns rather than fundamental market forces. However, the interconnected nature of global markets means that OPEC production boost decisions elsewhere can help offset regional disruptions.

Alternative Energy Transportation Routes During Persian Gulf Disruptions

Existing overland energy transportation networks offer limited substitution capacity compared to maritime volumes, creating structural bottlenecks when sea routes face extended disruptions. Pipeline infrastructure capacity analysis reveals significant gaps between alternative route availability and actual transportation requirements during crisis periods.

Alternative Route Capacity Assessment:

- Saudi East-West Pipeline: 5 million barrels per day capacity to Red Sea terminals

- UAE-Oman Pipeline: 1.5 million barrels per day alternative export route

- Iraqi Pipeline Networks: Multiple routes through Turkey and Jordan totalling 2.8 million barrels per day

- Combined Regional Capacity: Approximately 3.2 million barrels per day, representing less than 16% of typical maritime transit volumes

LNG Export Terminal Diversification Challenges

Liquefied natural gas transportation faces even greater constraints during maritime disruptions, as LNG requires specialised terminals and vessels that cannot easily redirect to alternative routes. Qatar's North Field expansion projects aim to reduce dependency on single-route exports, though implementation timelines extend through 2027-2030, providing little immediate relief during current disruptions.

"Critical Infrastructure Reality: Combined pipeline capacity from the Persian Gulf region represents less than one-sixth of normal maritime transportation volumes, demonstrating the structural limitations of alternative routes during extended shipping disruptions."

Transshipment Hub Vulnerabilities

Alternative routes face additional bottlenecks at terminal facilities, where Red Sea terminals, Oman ports, and Turkish pipeline endpoints may lack sufficient throughput capacity to handle redirected volumes. These secondary constraints often prove more limiting than primary pipeline capacity, creating multiple chokepoints within supposedly redundant transportation networks.

Political constraints affecting some alternative routes, including sanctions considerations and regional diplomatic relationships, further reduce practical capacity during crisis periods when energy buyers seek maximum supply diversification. Moreover, as Iran-US tensions strain shipping, alternative solutions become increasingly critical for global energy security.

Regional Production Shutdown Amplification Effects

Coordinated infrastructure vulnerabilities demonstrate how security threats to individual facilities can trigger precautionary shutdowns across multiple operations within the same geographic region. The current crisis illustrates this multiplier effect through simultaneous production halts affecting multiple major energy producers.

Qatar's LNG Market Concentration Risk

Qatar's position as a dominant LNG supplier creates systemic vulnerabilities when production faces disruption. Current market data indicates:

- Global LNG market share: Nearly 20% of worldwide LNG exports originate from Qatari facilities

- Facility concentration: Ras Laffan Industrial City represents the world's largest LNG export complex

- Asian market dependency: Significant portions of Qatar's LNG exports supply Asian energy consumers

- European supply significance: Substantial volumes of EU gas imports derive from Qatari sources

The cessation of LNG production demonstrates concentration risk in practice, where attacks on operating facilities in Ras Laffan Industrial City and Mesaieed Industrial City effectively eliminate a major portion of global LNG supply capacity. Industry sources indicate that authorities continue assessing damage extent while exports remain paused due to deteriorating security conditions across the Gulf region.

Saudi Refining Infrastructure Impact

The temporary shutdown of Ras Tanura refinery, which processes approximately 550,000 barrels per day, illustrates how individual facility disruptions affect regional product supply chains. While emergency teams brought fires under control following drone attacks, operational suspension reflects growing concerns about Gulf energy infrastructure vulnerability during widening conflicts.

Ras Tanura represents one of the world's most important oil export hubs, and its precautionary closure adds to mounting fears of significant supply constraints affecting both crude oil and refined petroleum products markets globally.

Multi-Regional Production Coordination Effects

The current crisis demonstrates cascading shutdown patterns across multiple geographic areas:

- Iraqi Kurdistan: Production halted affecting approximately 200,000 barrels per day of crude exports

- Northern Iraq Gas Sector: Dana Gas stopped natural gas exports from Khor Mor complex due to security conditions

- Multiple Facility Coordination: Simultaneous disruptions across Qatar, Saudi Arabia, and Iraq amplify individual facility impacts

This coordination pattern, whether intentional or coincidental, multiplies supply constraints beyond simple addition of individual facility capacities, creating systemic stress that exceeds the sum of component disruptions. Consequently, the importance of critical minerals & energy security becomes evident when considering long-term resilience strategies.

Macroeconomic Transmission Mechanisms During Extended Supply Disruptions

Energy price shocks propagate through economic systems via multiple transmission channels, affecting transportation costs, manufacturing inputs, and consumer purchasing power across diverse sectors. Current analyst warnings suggest prolonged disruption could lift crude prices toward or beyond $100 per barrel, with significant effects on inflation and global growth prospects.

Economic Impact Modelling by Disruption Duration:

| Disruption Duration | Global GDP Impact | Inflation Effect | Recovery Timeline |

|---|---|---|---|

| 1-2 weeks | 0.1-0.2% reduction | 0.3-0.5% increase | 3-6 months |

| 1-2 months | 0.4-0.8% reduction | 1.2-2.1% increase | 9-15 months |

| 3-6 months | 1.2-2.5% reduction | 2.8-4.5% increase | 18-30 months |

Central Bank Policy Response Frameworks

Monetary authorities face complex trade-offs between supporting economic growth and controlling inflation during energy supply shocks. Historical patterns suggest coordinated international policy responses often emerge during extended disruptions, though effectiveness depends on shock duration and severity.

The current crisis, entering its third consecutive day of intense conflict, suggests potential movement beyond initial 24-48 hour market adjustments into more serious economic impact scenarios requiring policy intervention consideration.

Strategic Industry Vulnerability Assessment

Manufacturing sectors with high energy intensity experience disproportionate cost pressures during extended supply disruptions:

- Aluminium Smelting: Extremely energy-intensive processes facing immediate margin pressure

- Steel Production: Coal and natural gas dependencies creating dual vulnerability

- Chemical Processing: Feedstock and energy cost escalation affecting production viability

- Cement Manufacturing: High-temperature processes requiring continuous energy supply

- Transportation Logistics: Direct fuel cost increases affecting delivery networks

These sectors often implement production curtailments during extended energy price spikes, creating secondary economic impacts through reduced industrial output and employment effects. Furthermore, implementing renewable energy transformations becomes increasingly attractive during such volatile periods.

Shipping Industry Response Dynamics to Maritime Security Threats

Commercial shipping operators implement dynamic risk management strategies during maritime security crises, fundamentally altering global transportation patterns and capacity utilisation. The current Strait of Hormuz shipping halt demonstrates these adaptive responses, with dozens of tankers halting transit and waiting offshore rather than attempting passage through threatened waterways.

Fleet Deployment and Route Optimisation

Shipping companies activate emergency protocols that prioritise crew safety and vessel security over delivery schedules, creating immediate capacity constraints across global energy transportation networks. Current patterns show major oil and shipping firms suspending crude, fuel, and LNG movements through affected waterways, citing safety concerns that override commercial considerations.

War Risk Insurance Market Response Patterns:

- Premium escalation: Rates increase 10-50 times normal levels during active conflict periods

- Coverage exclusion zones: Insurers designate specific geographic areas as uninsurable

- Fleet immobilisation: Vessels avoid risk zones, creating artificial capacity constraints

- Charter rate implications: Day rates increase 200-400% during disruption periods

Container Shipping Collateral Impact

Non-energy cargo faces significant delays and cost increases as shipping lines reroute vessels around affected regions, extending transit times by 10-14 days for major Asia-Europe trade lanes. This secondary impact affects global commerce beyond energy sectors, creating inflationary pressures across consumer goods and manufactured products markets.

The cascading nature of shipping disruptions demonstrates how energy security threats create broader economic vulnerabilities through interconnected transportation networks serving multiple commodity categories.

The next major ASX story will hit our subscribers first

Long-Term Strategic Infrastructure Resilience Implications

Extended energy chokepoint vulnerabilities drive fundamental reassessments of strategic petroleum reserve policies, pipeline infrastructure investments, and renewable energy transition timelines. Supply disruption events often catalyse increased domestic renewable energy investment as nations seek reduced dependency on volatile import sources.

Energy Security Policy Evolution

Current disruptions highlight critical infrastructure gaps that require long-term investment solutions:

- Pipeline Network Expansion: Overland alternatives to maritime transport routes requiring multi-year development

- Storage Capacity Enhancement: Strategic reserve expansion programmes targeting 90+ day import replacement

- Supply Source Diversification: Long-term contracting with geographically distributed producer regions

- Technology Deployment: Advanced monitoring and early warning systems for critical infrastructure protection

Renewable Energy Acceleration Incentives

Energy security concerns often accelerate domestic renewable energy deployment as governments recognise the strategic vulnerabilities associated with fossil fuel import dependencies. Current crisis conditions may catalyse policy support for accelerated renewable capacity installation, though deployment timelines typically require 3-7 years for meaningful impact on energy security metrics.

Infrastructure Investment Priority Frameworks

Long-term energy security planning increasingly emphasises redundancy and diversification across multiple dimensions:

- Geographic diversification of supply sources to reduce single-region dependency

- Transportation route redundancy through multiple pipeline and shipping alternatives

- Storage capacity expansion to buffer short-term supply interruptions

- Domestic production enhancement to reduce import vulnerability ratios

- Technology resilience through cybersecurity and physical protection upgrades

Strategic Petroleum Reserve Activation and Market Stabilisation

Emergency petroleum stockpiles represent critical buffers during supply disruptions, though actual effectiveness depends on reserve sizes, release coordination, and consumption patterns during crisis periods. Major consuming nations maintain reserves equivalent to 60-90 days of net imports under normal operating conditions, though actual duration varies based on demand management and alternative supply activation.

Current market conditions may trigger coordinated strategic reserve releases among major consuming nations, following established protocols for international energy emergency response. However, reserve effectiveness diminishes during extended disruptions exceeding 90-day stockpile capacity, requiring longer-term supply diversification strategies.

Market Psychology and Speculation Effects

Financial market responses often exceed physical supply-demand imbalances during energy crises, as speculative positioning and risk-averse behaviour amplify price movements beyond fundamental justification. Current market psychology reflects heightened uncertainty about conflict duration and geographical expansion, creating volatility premiums that persist beyond immediate supply constraints.

Professional energy traders implement position management strategies during extreme volatility periods, often reducing exposure and increasing cash reserves rather than attempting to capture directional price movements. This defensive positioning contributes to reduced market liquidity and increased price sensitivity to new information flows.

Frequently Asked Questions About Strategic Energy Chokepoint Disruptions

How quickly do global energy markets respond to major shipping route threats?

Commodity futures markets typically react within hours of confirmed threats to critical transportation infrastructure, with price movements often preceding actual physical supply impacts by days or weeks. Electronic trading systems enable immediate global price discovery, causing rapid volatility spikes when major chokepoints face security threats.

What percentage of global energy trade depends on vulnerable maritime corridors?

The Strait of Hormuz shipping halt affects approximately 21% of global petroleum liquids and 25% of worldwide LNG exports under normal operating conditions. Additional chokepoints including the Suez Canal and Strait of Malacca create multiple vulnerability points affecting global energy security.

How effective are strategic petroleum reserves during extended supply disruptions?

Strategic reserves provide 60-90 days of import replacement under normal consumption patterns, though actual duration depends on demand management measures and alternative supply activation. Reserve effectiveness requires coordinated international releases and cannot address disruptions exceeding several months without additional supply diversification.

Which economic sectors face the greatest vulnerability to energy supply constraints?

Energy-intensive manufacturing including aluminium smelting, steel production, chemical processing, and cement manufacturing experience immediate cost pressures during supply disruptions. Transportation and logistics sectors face direct fuel cost increases, while broader economic impacts emerge through inflation transmission mechanisms affecting consumer goods pricing.

Investment Considerations: Energy supply chain disruptions create complex investment implications across multiple asset classes, requiring careful analysis of duration expectations, geographic exposure, and sector-specific vulnerabilities when evaluating portfolio positioning during crisis periods.

This analysis is based on publicly available information and market data. Investors should conduct independent research and consider consulting qualified financial advisors before making investment decisions during periods of elevated market volatility and geopolitical uncertainty.

Could Energy Supply Disruptions Create Major Investment Opportunities?

Discovery Alert instantly identifies ASX-listed companies positioned to benefit from global energy transitions and supply chain disruptions using its proprietary Discovery IQ model. Understand why major mineral discoveries in critical commodities can generate substantial returns by exploring Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of market-moving developments.