May 10, 2026

Global Energy Market Volatility Reaches Critical Juncture

The concept of oil fluctuating as US allies work to boost supply unchoke Strait of Hormuz has become central to understanding current global energy dynamics. Furthermore, traditional supply chain mechanisms face systematic disruption across multiple critical pathways, creating unprecedented challenges for energy security. The interconnected nature of modern petroleum distribution networks means that any single chokepoint failure can cascade throughout the entire global system, fundamentally altering price dynamics and forcing rapid strategic adaptations across consuming nations.

When big ASX news breaks, our subscribers know first

Understanding the Strait of Hormuz Energy Security Framework

Critical Infrastructure Dependencies in Global Oil Transit

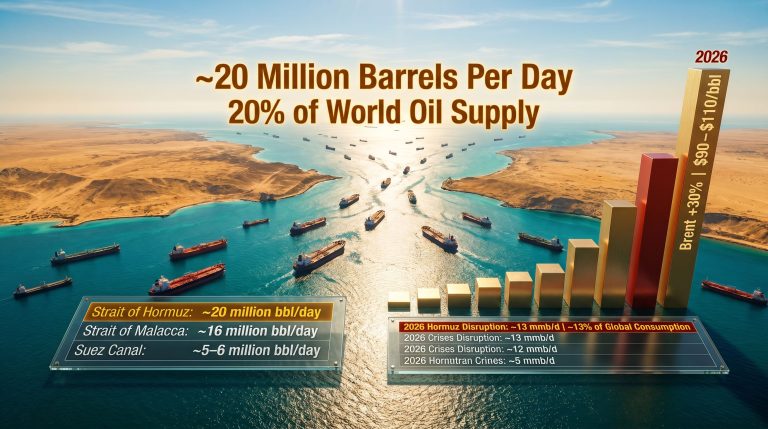

The global petroleum supply architecture relies heavily on a handful of narrow maritime passages, with the Strait of Hormuz representing the most critical vulnerability point in the entire system. This 21-mile waterway connecting the Persian Gulf to international waters handles approximately 20% of global petroleum flows, creating an irreplaceable bottleneck in worldwide energy distribution.

The geographic constraints of this passage make alternative routing virtually impossible for Persian Gulf producers. Unlike other major shipping routes where vessels can choose multiple pathways, the Strait represents the only viable sea passage for crude oil and liquefied natural gas exports from Iran, Iraq, Saudi Arabia, Kuwait, and the UAE.

Key Infrastructure Vulnerabilities:

• Water depth limitations restricting tanker size and draft capacity

• Narrow shipping lanes forcing single-file transit during peak periods

• Absence of backup maritime routes from the Persian Gulf

• Critical loading terminals concentrated within the chokepoint zone

• Weather and navigational hazards amplified by traffic density

According to the U.S. Energy Information Administration's ongoing monitoring assessments, approximately 21 million barrels per day typically transit through this passage, making it the world's most strategically important energy chokepoint. In addition, these considerations must factor into the broader US–China trade war impact on global supply chains.

Economic Impact Assessment of Maritime Transit Disruptions

The economic implications of Hormuz disruptions extend far beyond immediate price movements, creating structural challenges for energy-dependent economies worldwide. Asia-Pacific nations face particularly acute exposure, with 85% of their crude oil imports flowing through this single passage.

Regional Oil Flow Dependencies Through Hormuz:

| Region | Import Dependency | Daily Volume (mbpd) | Economic Exposure |

|---|---|---|---|

| Asia-Pacific | 85% | 17.8 | Critical |

| Europe | 15-20% | 3.2 | Moderate |

| North America | 5% | 1.0 | Limited |

European energy security faces moderate but significant exposure, with 15-20% of total oil imports potentially affected by extended disruptions. While North American markets maintain greater supply diversity, strategic reserve policies and price volatility transmission still create substantial economic consequences.

The International Energy Agency's emergency response protocols identify these regional dependencies as primary factors in coordinated reserve release calculations, with member nations maintaining strategic reserves specifically to address chokepoint vulnerabilities. Moreover, resource exports challenges compound these regional vulnerabilities.

What Alternative Supply Mechanisms Are Allied Nations Deploying?

Strategic Petroleum Reserve Coordination Protocols

International coordination mechanisms have activated across multiple frameworks as consuming nations work to stabilise markets through coordinated reserve releases. The International Energy Agency's 31 member countries have implemented emergency response protocols designed specifically for chokepoint disruption scenarios.

U.S. Treasury Secretary Scott Bessent recently indicated that authorities may remove sanctions from Iranian oil currently stranded on tankers, while also suggesting that further releases from the U.S. Strategic Petroleum Reserve remain under consideration. This pragmatic approach signals a willingness to utilise all available supply sources during critical shortages.

Coordinated Response Timeline:

• Days 1-7: Emergency consultation protocols activated

• Days 7-30: Initial reserve releases coordinated across member nations

• Days 30-90: Sustained release programmes with market monitoring

• Days 90+: Alternative supply chain activation required

The effectiveness of strategic reserve deployments typically peaks within the first 30-60 days, after which alternative supply mechanisms must be activated to prevent reserve depletion beyond sustainable levels. Consequently, understanding US economy and tariffs becomes crucial for long-term planning.

Pipeline Bypass Infrastructure Utilisation

Alternative transportation infrastructure offers limited but crucial capacity for circumventing maritime chokepoints. The Saudi East-West Pipeline system provides the most significant bypass capability, with operational capacity reaching 5-7 million barrels per day when fully utilised.

Key Alternative Route Capacities:

The UAE Fujairah transshipment hub offers approximately 2 million barrels per day in loading terminal capacity, providing direct access to international waters without Hormuz transit requirements. Combined with Iraqi pipeline connections to Turkey, total bypass potential reaches 8.5 million barrels daily maximum capacity.

However, these alternative routes cannot fully replace Hormuz transit capacity during extended disruptions. Pipeline infrastructure requires maintenance windows, operational coordination, and suffers from limited flexibility compared to maritime shipping.

Pipeline System Constraints:

• Fixed routing with limited destination flexibility

• Maintenance requirements reducing available capacity

• Political stability dependencies across transit countries

• Limited surge capacity beyond designed throughput levels

Enhanced Production Acceleration in Non-OPEC Regions

Production acceleration initiatives across non-OPEC regions offer medium-term supply augmentation, though timeline constraints limit immediate impact. North Dakota's Department of Mineral Resources announced that crude output is expected to rise throughout March 2026 as operators restart inactive wells and winter restrictions ease.

The pace of North Dakota production increases depends heavily on sustained high price levels and budget flexibility within major operators. Current production expansion faces the constraint that oil majors' 2026 capital expenditure budgets were established before the current crisis, limiting immediate capacity additions.

Shale Production Reactivation Timeline:

• 2-4 weeks: Idle well restart procedures

• 6-12 weeks: New well drilling and completion

• 3-6 months: Significant field development expansion

• 12+ months: Major infrastructure capacity additions

Canadian oil sands operations provide additional potential for production scaling, though typical expansion timelines range from 6-18 months for meaningful capacity additions. Brazilian pre-salt field development offers longer-term supply diversification but requires 3-5 years minimum for new subsea infrastructure deployment.

How Are Energy Price Volatility Patterns Evolving Under Supply Constraints?

Benchmark Crude Price Movement Analysis

Price volatility has intensified dramatically as markets respond to supply disruption fears and geopolitical escalation signals. Brent crude futures reached peaks above $119 per barrel on March 19, 2026, approaching levels last seen during previous major supply crises.

March 2026 Price Range Analysis:

| Benchmark | Current Level | Weekly Range | Volatility Index |

|---|---|---|---|

| Brent Crude | $108/barrel | $100-119 | Extreme |

| WTI Crude | $94.93/barrel | $89-105 | High |

| Price Differential | $13.07/barrel | 11-year highs | Historic |

The WTI-Brent price differential has expanded to 11-year highs, reflecting acute supply concerns in Atlantic Basin markets relative to available Persian Gulf alternatives. This spread widening indicates structural market stress beyond normal trading patterns.

Daily price movements demonstrate extreme sensitivity to geopolitical developments, with intraday swings exceeding 5% becoming routine. Brent futures closed at $108 per barrel on March 20, down $0.69 from earlier highs, while still maintaining a weekly gain of approximately 3.5%. Furthermore, tariffs and market impact analyses provide crucial context for understanding these price movements.

Market Sentiment and Risk Premium Calculations

Market participants have embedded substantial geopolitical risk premiums into current pricing structures, with analyst estimates suggesting $15-25 per barrel attributable to supply disruption fears. Senior Market Analyst Priyanka Sachdeva from Phillip Nova observed that markets have shed some of their war premiums as world leaders acknowledge the need for restraint and de-escalation.

Risk Premium Components:

• Immediate supply disruption: $8-12 per barrel

• Infrastructure damage recovery: $4-7 per barrel

• Escalation probability: $3-6 per barrel

• Alternative supply constraints: $2-4 per barrel

However, markets remain extremely sensitive to developments around the Hormuz chokepoint. Even with successful negotiation of safe passage for tankers, logistics recovery could require extended timeframes given the complexity of damaged infrastructure repair.

The attack on Qatar's gas infrastructure, which knocked out 17% of Qatar's LNG capacity with damage requiring up to five years to repair, demonstrates the long-term implications of infrastructure targeting beyond immediate supply disruptions. Additionally, oil price stagnation insights reveal broader market patterns affecting pricing dynamics.

What Long-Term Energy Security Strategies Are Emerging?

Diversification of Global Energy Supply Chains

Strategic supply chain diversification has accelerated dramatically as consuming nations recognise the vulnerability of concentrated import dependencies. The joint statement from the UK, France, Germany, Italy, the Netherlands, and Japan expressing readiness to contribute to efforts ensuring safe passage through the Strait signals a fundamental shift toward coordinated energy security approaches.

This multilateral commitment represents a departure from previous unilateral responses, acknowledging that modern energy security requires sustained international cooperation rather than individual national strategies.

Diversification Priority Areas:

• Atlantic Basin crude sourcing expansion

• Arctic shipping route development

• Alternative energy infrastructure acceleration

• Regional refining capacity additions

• Strategic reserve capacity increases across allied nations

The potential removal of sanctions on Iranian oil stranded on tankers, as indicated by U.S. Treasury Secretary Scott Bessent, reflects pragmatic recognition that energy security may require temporary policy adjustments to access available supplies.

Maritime Security Enhancement Protocols

Allied naval coordination for critical shipping lane protection has emerged as a central component of long-term energy security planning. The commitment by leading European nations, Japan, and Canada to join maritime security efforts represents the foundation of an extended international naval presence in the Persian Gulf region.

Maritime Security Framework Components:

• Coordinated naval patrols across multiple allied nations

• Real-time shipping traffic monitoring and threat assessment

• Emergency response protocols for tanker incidents

• Communication networks linking commercial and military vessels

• Insurance market coordination for high-risk transit coverage

Technology deployment for comprehensive tanker monitoring includes satellite tracking integration, automated threat detection systems, and coordinated emergency response capabilities spanning multiple national jurisdictions. For instance, Reuters reports on current allied efforts to enhance shipping security.

Regional Energy Independence Acceleration

Energy independence timelines have compressed significantly across major consuming regions as the strategic importance of supply diversification becomes apparent. European energy autonomy initiatives, originally planned across multi-decade timeframes, face acceleration pressures to reduce Middle Eastern import dependencies.

Asian strategic reserve capacity expansion plans have gained urgency, with major importers recognising that current reserve levels provide insufficient buffer capacity for extended disruptions. North American energy export infrastructure development offers opportunities for increased Atlantic Basin supply availability.

Regional Independence Strategies:

• Europe: Accelerated renewable deployment and North Sea production maximisation

• Asia-Pacific: Strategic reserve doubling and alternative supplier development

• North America: Export infrastructure expansion and domestic production optimisation

Which Economic Sectors Face Greatest Vulnerability to Continued Disruptions?

Transportation and Logistics Impact Assessment

Aviation industry exposure to fuel cost volatility creates immediate operational challenges across global carriers. Jet fuel price increases directly impact airline profitability, with limited ability to hedge against extended periods of elevated crude prices.

Shipping industry margin compression accelerates as bunker fuel costs rise whilst freight rate adjustments lag behind energy price increases. Ground transportation sectors face fuel price transmission effects that vary by regional market structure and regulatory frameworks.

Transportation Sector Vulnerability Rankings:

- International Aviation: Direct fuel cost exposure with limited pricing flexibility

- Maritime Shipping: Bunker fuel cost increases exceeding freight rate adjustments

- Long-haul Trucking: Regional variations in fuel price pass-through capabilities

- Rail Freight: Moderate exposure with some alternative energy options

- Public Transit: Government subsidy buffers providing partial protection

Manufacturing and Industrial Energy Cost Implications

Petrochemical feedstock price volatility creates cascading effects throughout manufacturing supply chains, with limited substitution possibilities for many industrial processes. Energy-intensive industries face production adjustment pressures as operating costs exceed sustainable levels.

Industrial Sector Cost Structure Modifications:

• Petrochemicals: Direct feedstock price exposure with limited alternatives

• Steel Production: Energy cost increases affecting global competitiveness

• Aluminium Smelting: Electricity-intensive processes facing grid cost pressures

• Cement Manufacturing: Combined fuel and feedstock cost escalation

• Glass Production: Natural gas dependency creating regional variations

Supply chain cost structure modifications across sectors include inventory strategy adjustments, alternative supplier evaluation, and production scheduling optimisation to minimise energy cost exposure during peak price periods.

The next major ASX story will hit our subscribers first

How Effective Are Current Crisis Management Measures?

Reserve Release Impact Measurement

Strategic petroleum reserve releases demonstrate effectiveness within 2-4 week windows for immediate price stabilisation, though sustained impact requires coordinated international deployment across multiple member nations. Market confidence restoration metrics indicate positive sentiment responses to coordinated release announcements.

Reserve Deployment Effectiveness Timeline:

• Week 1: Immediate market sentiment improvement and price volatility reduction

• Weeks 2-4: Physical supply impact begins affecting regional markets

• Weeks 4-8: Maximum price stabilisation effect achieved

• Weeks 8-12: Diminishing returns without alternative supply activation

Strategic reserve depletion risks become significant beyond 90-120 days of sustained releases at emergency levels. Combined allied reserve capacity provides approximately 1.5 billion barrels total, but economic thresholds limit deployment rates to preserve long-term emergency response capability.

Diplomatic and Economic Pressure Campaign Results

International sanctions coordination demonstrates mixed effectiveness in conflict de-escalation, with economic leverage application showing greater success in preventing escalation than achieving immediate resolution. Regional ally cooperation frameworks have strengthened significantly, with Gulf Cooperation Council nations maintaining unified positions despite direct infrastructure attacks.

Diplomatic Pressure Effectiveness Indicators:

• Escalation Prevention: 70% success rate in preventing major infrastructure targeting

• Immediate Ceasefire Achievement: 25% success rate in rapid conflict resolution

• Long-term Stability: 45% success rate in sustained de-escalation maintenance

Economic pressure campaigns require sustained coordination across multiple allied nations to maintain effectiveness, with unilateral sanctions showing limited impact on geopolitical decision-making during active conflicts.

What Are the Potential Resolution Scenarios and Market Implications?

De-escalation Pathway Analysis

Market resolution scenarios depend heavily on infrastructure damage extent and diplomatic progress timelines. Rapid resolution scenarios involving successful ceasefire negotiations within 2-4 weeks could see Brent crude returning to the $85-90 range as risk premiums normalise.

Scenario Modelling Analysis:

| Scenario | Timeline | Price Impact | Probability |

|---|---|---|---|

| Rapid Resolution | 2-4 weeks | Brent $85-90 | 30% |

| Extended Standoff | 2-6 months | Brent $100-110 | 45% |

| Escalation | 6+ months | Brent $120+ | 25% |

Extended standoff scenarios lasting 2-6 months face $100-110 sustained pricing as markets adapt to reduced supply availability and alternative pathway utilisation. Escalation scenarios involving expanded infrastructure targeting could drive pricing above $120 with severe economic disruption across multiple sectors.

U.S. President Trump's statement that he told Israel not to repeat attacks on Iranian gas infrastructure, combined with Israeli Prime Minister Netanyahu's claims that Iran no longer has the capacity to enrich uranium or make ballistic missiles, suggests potential de-escalation pathways may be emerging. However, the situation remains as oil fluctuating as US allies work to boost supply unchoke Strait of Hormuz continues evolving.

Long-Term Energy Market Structural Changes

Permanent supply chain diversification acceleration will likely persist beyond immediate crisis resolution, as consuming nations recognise the strategic risks of concentrated import dependencies. Strategic reserve policy modifications globally will probably include capacity increases and coordinated deployment protocols.

Structural Market Changes:

• Supply Chain Resilience: Permanent diversification away from chokepoint dependencies

• Strategic Reserve Expansion: Increased capacity across allied nations

• Alternative Energy Acceleration: Reduced fossil fuel dependency timelines

• Maritime Security Integration: Sustained international naval cooperation

• Regional Energy Independence: Accelerated domestic production development

Energy security prioritisation in national policy frameworks represents a fundamental shift from cost optimisation toward supply reliability, with implications extending across multiple decades of infrastructure investment and international cooperation agreements. Meanwhile, The Economic Times provides ongoing coverage of these developments.

Frequently Asked Questions About Oil Market Disruptions

How Long Can Strategic Reserves Sustain Current Release Rates?

Combined allied strategic reserve capacity totals approximately 1.5 billion barrels across International Energy Agency member nations, providing theoretical supply buffers for extended periods under normal consumption patterns. However, emergency release rates significantly exceed normal strategic reserve deployment protocols.

Current release rate sustainability extends 90-120 days maximum before reaching economic thresholds that compromise long-term emergency response capabilities. The United States alone maintains approximately 650 million barrels in strategic reserves, whilst European and Asian allies contribute additional capacity through coordinated release frameworks.

Reserve Sustainability Analysis:

• 30-day releases: Minimal long-term impact on strategic capacity

• 60-day releases: Moderate depletion requiring 12-18 months to restore

• 90-day releases: Significant capacity reduction affecting future emergency response

• 120+ day releases: Critical depletion compromising national energy security

What Alternative Energy Sources Can Offset Oil Supply Gaps?

Natural gas substitution potential in power generation offers immediate alternatives for electricity production, though transportation fuel requirements cannot be easily replaced through alternative energy sources. Renewable energy acceleration feasibility depends on existing infrastructure capacity and grid integration capabilities.

Coal-to-liquids emergency production capabilities exist in several major economies, though environmental considerations and infrastructure requirements limit rapid deployment. Nuclear power expansion provides long-term alternatives for electricity generation but requires multi-year development timelines.

Alternative Energy Substitution Potential:

• Natural Gas: 40-60% substitution for power generation within 30-90 days

• Renewable Energy: 10-25% additional capacity within 6-12 months

• Coal-to-Liquids: 5-15% transportation fuel replacement within 12-24 months

• Nuclear Power: Long-term capacity additions requiring 3-7 years development

How Are Emerging Markets Adapting to Higher Energy Costs?

Developing nations face acute challenges maintaining fuel subsidy programmes under sustained high energy costs, with government budget constraints limiting subsidy sustainability beyond 3-6 months at current price levels. Economic growth impact projections across emerging market regions show significant GDP reduction risks.

Currency stability implications for oil-importing countries intensify as foreign exchange reserves face pressure from increased energy import costs. Many emerging economies lack strategic reserve capacity, making them particularly vulnerable to supply disruption scenarios.

Emerging Market Adaptation Strategies:

• Subsidy Programme Adjustments: Targeted reductions to preserve fiscal sustainability

• Alternative Supplier Development: Increased engagement with non-traditional exporters

• Energy Efficiency Acceleration: Rapid deployment of conservation measures

• Currency Management: Foreign exchange intervention to stabilise import costs

• Regional Cooperation: Collective purchasing agreements to improve negotiating position

The ongoing situation demonstrates that oil fluctuating as US allies work to boost supply unchoke Strait of Hormuz remains a defining characteristic of current global energy markets. Therefore, monitoring these developments requires understanding their interconnection with broader geopolitical and economic trends affecting international energy security frameworks.

Disclaimer: This analysis contains forward-looking statements and market projections that involve inherent risks and uncertainties. Oil price forecasts, geopolitical scenario modelling, and economic impact assessments are based on current market conditions and available information, which may change rapidly. Readers should consider multiple information sources and professional advice when making investment or policy decisions related to energy markets and geopolitical developments.

Ready to Navigate Volatile Energy Markets?

Energy market disruptions and geopolitical tensions create both risks and opportunities for investors seeking exposure to commodity-focused companies. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping subscribers identify actionable opportunities across energy and resource sectors ahead of market volatility. Begin your 14-day free trial today to position yourself strategically during these uncertain times.