June 14, 2026

The Complex Relationship Between Energy Markets and Currency Stability

Global financial markets operate through intricate transmission mechanisms where commodity price shocks create cascading effects across multiple asset classes. Energy-dependent economies face particularly acute vulnerabilities when geopolitical tensions disrupt crude oil supply chains, triggering immediate balance-of-payments pressures that manifest through currency depreciation. Understanding these interconnected dynamics becomes essential for investors navigating periods of heightened uncertainty.

The current energy crisis stemming from Middle East conflicts demonstrates how quickly external shocks can destabilise emerging market currencies. As crude oil prices surge beyond critical psychological thresholds, energy-importing nations experience dual pressures: increased import costs straining current accounts and portfolio capital flight as investors reassess risk premiums. These forces combine to create sustained depreciation cycles that central banks struggle to contain through conventional intervention tools. The Iran war impact on Indian rupee exemplifies these complex transmission mechanisms in real-time market conditions.

When big ASX news breaks, our subscribers know first

Understanding Energy Import Dependencies and Economic Vulnerabilities

Critical Infrastructure Dependencies in Oil-Importing Nations

India's energy security framework reveals the structural challenges facing emerging economies during geopolitical crises. With approximately 85% of crude oil requirements sourced through imports, the nation experiences direct exposure to price volatility and supply disruption risks. This dependency creates immediate balance-of-payments pressure when global energy costs escalate rapidly.

The transmission mechanism operates through multiple channels simultaneously. Current account deficit expansion becomes inevitable as energy import bills consume larger portions of foreign exchange earnings. Historical data shows that during previous oil price surges, India's current account deficit has deteriorated from baseline levels of 2.1% of GDP to stressed levels exceeding 3.4% of GDP, representing a 62% increase in fiscal burden.

Energy import costs directly influence currency demand patterns. Indian importers must acquire additional US dollars to settle petroleum payments, creating sustained upward pressure on USD/INR exchange rates. The magnitude of this pressure correlates with both the absolute price increase and the duration of elevated energy costs. Furthermore, this dynamic is amplified by the oil price rally affecting global markets.

Currency Depreciation Mechanisms During Supply Shocks

Foreign exchange markets respond to energy crises through predictable yet complex pathways. Direct impact channels include increased dollar demand from importers seeking to hedge future energy purchases, while indirect channels operate through investor sentiment shifts and portfolio rebalancing decisions.

The Iran war impact on Indian rupee demonstrates these transmission mechanisms in real-time. Portfolio investors typically reduce exposure to energy-dependent currencies during prolonged supply disruptions, anticipating sustained economic headwinds. This behavioural response amplifies currency weakness beyond levels justified by trade balance deterioration alone.

Market participants employ sophisticated risk assessment frameworks during geopolitical crises. Foreign institutional investors evaluate energy dependency ratios, foreign exchange reserve adequacy, and central bank credibility when determining portfolio allocations. Countries with higher energy import dependencies experience sharper capital outflows during crisis periods. Moreover, Saudi exploration licenses and regional supply developments significantly influence these investor calculations.

Immediate Market Responses to Regional Supply Disruptions

Energy Price Escalation and Regional Impact Assessment

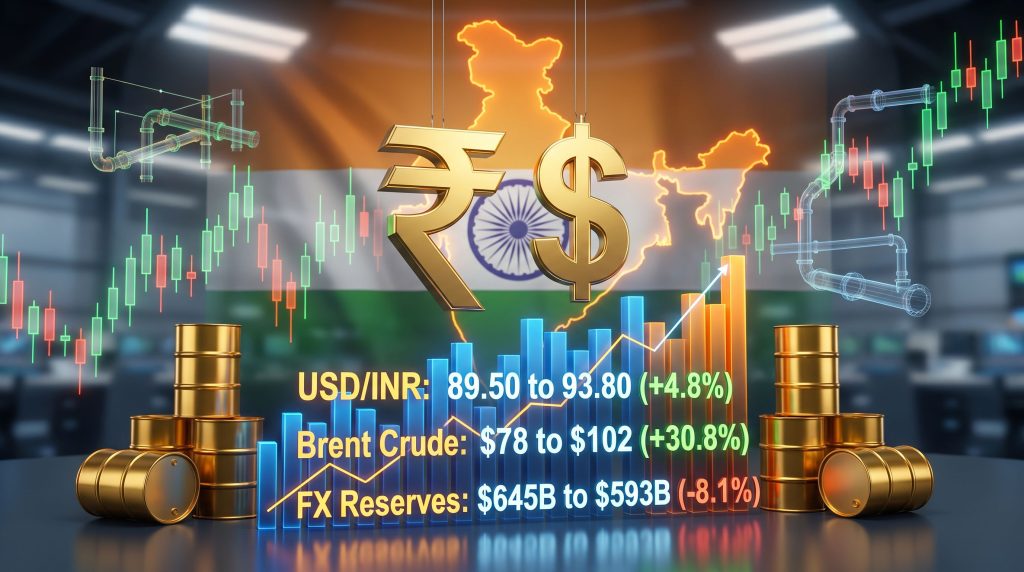

Brent crude price movements during the Strait of Hormuz crisis illustrate the sensitivity of global energy markets to chokepoint disruptions. Prices surged from $78 per barrel to $102 per barrel, representing a 30.8% increase that exceeded typical geopolitical risk premiums.

This pricing environment creates particularly acute challenges for Asian economies dependent on Middle Eastern oil supplies. The Strait of Hormuz handles approximately 20-25% of global seaborne oil traffic daily, making any disruption threat capable of triggering significant premium pricing across regional markets. Consequently, oil price movements during such crises often exceed fundamental supply-demand imbalances.

Supply chain disruption multipliers extend beyond immediate price impacts. Insurance costs for tanker shipments increase substantially during conflict periods, adding 2-5% premiums to delivered crude prices. Alternative shipping routes through the Cape of Good Hope add 10-12 days to transit times, forcing inventory accumulation and increasing carrying costs throughout the supply chain.

Regional Currency Performance Analysis

Asian currency markets during the current crisis demonstrate varying degrees of sensitivity to energy price shocks. Comparative depreciation data reveals significant performance divergences:

| Currency | 3-Week Performance | Energy Dependency |

|---|---|---|

| Philippine Peso | -3.2% | High import dependency |

| Indian Rupee | -2.8% | 85% import reliance |

| Indonesian Rupiah | -2.1% | Moderate exposure |

| Chinese Yuan | +0.1% | 50-55% import dependency |

The Philippine peso's sharper decline reflects both higher portfolio investment sensitivity and smaller foreign exchange reserve buffers relative to import coverage ratios. Indonesia's more moderate depreciation benefits from substantial energy export revenues that partially offset import cost increases.

China's yuan outperformance during this period demonstrates the advantages of lower energy import dependency and larger foreign exchange reserves exceeding $3.4 trillion. Chinese authorities also maintain more extensive capital controls, limiting speculative positioning against the currency.

Central Bank Intervention Strategies During Currency Crises

Reserve Bank of India's Market Stabilisation Efforts

Central bank foreign exchange interventions during the Iran war impact on Indian rupee crisis reveal sophisticated policy coordination mechanisms. The Reserve Bank of India deployed approximately $51.7 billion in dollar sales, representing roughly 8% of total foreign exchange reserves that previously stood at $645 billion.

This intervention intensity indicates significant policy commitment to preventing disorderly currency adjustment. State-run banks, particularly the State Bank of India, serve as operational intermediaries for RBI forex operations, selling dollars to approved dealers and commercial importers to create supply pressure on exchange rates. For instance, India's central bank maintained its policy stance to avoid policy errors during the war uncertainty.

The effectiveness of intervention depends critically on market perception of central bank resolve. During the current crisis, intervention prevented the rupee from weakening beyond the 94.00 level, maintaining relative stability around 93.80 per dollar despite sustained energy price pressures.

Regulatory Framework Adjustments and Market Controls

Macroprudential measures implemented during currency stress periods include position limits restricting commercial banks' net foreign exchange exposures. Current regulations impose $100 million caps on bank forex positions, preventing excessive speculative accumulation that might amplify depreciation pressures.

Non-deliverable forward (NDF) market restrictions target offshore rupee trading that can create artificial selling pressure disconnected from underlying economic flows. The majority of INR NDF trading occurs in London and Singapore, requiring international coordination to implement effective controls.

Re-booking prohibitions prevent rapid reversal cycles in forward foreign exchange contracts that might indicate speculative activity rather than legitimate hedging. These measures require minimum 2-3 day intervals between contract reversals and new bookings, reducing market volatility from excessive turnover. Additionally, currency crisis concerns have prompted authorities to strengthen monitoring mechanisms.

Broader Economic Implications of Sustained Energy Conflicts

Sectoral Impact Distribution Across the Economy

Extended energy price elevations create heterogeneous effects across different sectors of the Indian economy. Transportation-intensive industries including cement, steel, and retail distribution experience immediate margin compression as fuel surcharges increase operational costs.

Manufacturing sectors utilising petroleum-derived inputs face dual pressures from higher raw material costs and increased logistics expenses. Chemical, pharmaceutical, and textile industries demonstrate particular sensitivity to sustained energy price shocks.

Consumer spending patterns shift measurably during energy crises as household budgets absorb higher transportation and utility costs. Discretionary spending categories including recreation, dining, and non-essential retail experience reduced allocation as consumers prioritise essential transportation and heating fuel purchases.

Inflation Dynamics and Monetary Policy Constraints

Energy price pass-through effects typically manifest in headline inflation within 2-3 months of initial crude oil price increases. Core inflation measures exclude direct energy components but capture second-round effects through transportation and manufacturing cost channels.

The Reserve Bank of India faces complex policy trade-offs during energy-driven currency crises. Interest rate increases might attract portfolio flows and support currency stability but risk amplifying economic slowdown effects from higher energy costs. Conversely, accommodative policy risks accelerating inflation pass-through while providing insufficient currency support.

Government fiscal pressures intensify during energy crises as subsidy obligations expand to protect consumers from full price impact. India's fuel subsidy programmes create direct budget strains when crude prices remain elevated for extended periods, potentially requiring fiscal consolidation that further dampens economic growth. However, gold as inflation hedge strategies become increasingly attractive during such periods.

Investment Positioning Strategies During Geopolitical Energy Crises

Currency Risk Management Approaches

Sophisticated investors employ multiple derivative instruments to manage rupee exposure during energy-driven volatility periods. Forward contract structures provide predictable hedging for import-heavy businesses, while options strategies offer asymmetric downside protection without capping potential currency recovery benefits.

Currency swap arrangements with major trading partners provide alternative financing mechanisms that reduce dollar dependency for energy imports. India's bilateral swap facilities with Japan, Singapore, and other partners create additional liquidity sources during crisis periods.

Portfolio managers typically increase defensive sector allocations during sustained geopolitical uncertainty. Utilities, consumer staples, and healthcare sectors demonstrate lower correlation with energy price movements and currency volatility compared to transportation, materials, and discretionary consumer sectors. In addition, concerns about US inflation and debt dynamics influence global portfolio positioning decisions.

Long-term Strategic Positioning Considerations

Energy security investment themes gain prominence during sustained supply disruptions. Companies involved in strategic petroleum reserve expansion, alternative energy development, and energy efficiency technologies attract increased investor interest.

Currency internationalisation trends accelerate during dollar-dominated energy crisis periods. India's efforts to expand rupee trade settlement mechanisms with major partners reduce vulnerability to dollar funding stress during future geopolitical events.

Regional economic integration initiatives including energy cooperation frameworks provide diversification benefits that reduce single-supplier dependency risks. Investors increasingly value companies and countries with diversified energy sourcing strategies.

The next major ASX story will hit our subscribers first

Frequently Asked Questions About Energy Crisis Currency Impact

Duration and Recovery Timeline Expectations

Historical analysis suggests geopolitical energy crises typically persist for 3-6 months before reaching resolution or market adaptation. Currency recovery patterns depend heavily on underlying economic fundamentals and central bank credibility rather than energy price normalisation alone.

Recovery phases usually begin with stabilisation of forward volatility measures before spot exchange rates improve. Options market implied volatility provides early signals of investor confidence restoration in currency stability.

Investment protection strategies during extended energy conflicts emphasise inflation-hedged assets including commodities, infrastructure securities, and inflation-linked bonds that provide purchasing power protection during cost-push inflation periods.

Key Metrics and Quantitative Analysis Framework

Statistical Overview of Current Crisis Impact

| Economic Indicator | Pre-Crisis Level | Current Level | Percentage Change |

|---|---|---|---|

| USD/INR Exchange Rate | 89.50 | 93.80 | +4.8% |

| Brent Crude Price | $78/barrel | $102/barrel | +30.8% |

| India FX Reserves | $645 billion | $593 billion | -8.1% |

| Current Account Deficit | 2.1% of GDP | 3.4% of GDP | +62% |

These metrics demonstrate the comprehensive nature of energy crisis transmission effects across multiple economic indicators simultaneously. The correlation between energy prices and currency weakness appears particularly strong during the current episode compared to historical precedents.

Regional Comparative Performance Assessment

Energy-dependent economy rankings during the crisis period reveal India's relative position among emerging market peers. The rupee's -2.8% depreciation places it in the middle range of regional currency performance, suggesting neither exceptional vulnerability nor unusual resilience.

Capital flow monitoring through SWIFT payment system data provides early warning indicators of foreign investment withdrawal patterns. Sustained outflows exceeding $2-3 billion monthly typically indicate deeper structural concerns beyond temporary energy price volatility.

Strategic Outlook and Risk Scenario Planning

Policy Response Effectiveness Evaluation

Central bank intervention success depends critically on coordination with fiscal authorities and consistency with underlying economic fundamentals. The current $51.7 billion intervention deployment represents substantial commitment but requires complementary policy measures to ensure lasting effectiveness.

International coordination mechanisms including swap line activation and multilateral facility access provide additional policy tools during severe currency stress. India's membership in various regional financial arrangements creates backup liquidity sources if domestic measures prove insufficient.

Future Vulnerability Assessment

Structural reforms targeting energy import dependency reduction become increasingly urgent following each crisis episode. Investment in renewable energy capacity, energy efficiency improvements, and strategic reserve expansion can reduce future vulnerability to similar shocks.

Financial market development including deeper domestic bond markets and expanded local currency trade settlement reduces reliance on dollar funding during stress periods. These structural improvements require sustained policy commitment extending beyond immediate crisis management timeframes.

The Iran war impact on Indian rupee demonstrates the interconnected nature of geopolitical events, commodity markets, and currency stability in emerging economies. Understanding these transmission mechanisms enables more effective risk management and strategic positioning during periods of heightened uncertainty. Investors and policymakers must prepare for potentially extended periods of energy market volatility while building longer-term resilience against similar future disruptions.

Disclaimer: This analysis is for educational purposes and should not be considered as investment advice. Currency markets involve substantial risk, and past performance does not guarantee future results. Readers should consult qualified financial advisors before making investment decisions.

Want to Capitalise on Energy Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including energy and resource companies positioned to benefit from global supply disruptions. Stay ahead of market movements by accessing Discovery Alert's comprehensive discoveries page to see how major finds have generated substantial returns, then begin your 14-day free trial today to gain a critical edge during volatile market conditions.