May 11, 2026

The Energy Security vs. Clean Transition Balancing Act

Global energy markets are witnessing an unprecedented shift as economic powerhouses navigate the complex terrain between maintaining reliable energy supplies and transitioning toward sustainable alternatives. This delicate equilibrium has become particularly pronounced in regions where fossil fuel dependency intersects with ambitious decarbonization timelines, creating policy frameworks that must simultaneously address short-term energy security and long-term environmental objectives.

The strategic approach to energy planning in major economies reflects a pragmatic recognition that rapid transitions require decades to implement effectively. When consumption patterns exceed 5.5 billion tons of coal equivalent annually, maintaining grid stability while introducing intermittent renewable sources becomes a multifaceted engineering and economic challenge. Furthermore, this reality has shaped energy security doctrines that prioritise domestic production capacity buffers, strategic reserve accumulation, and grid reliability protocols requiring dispatchable backup power sources.

Geopolitical Tensions and Production Priorities

The intersection of energy independence and geopolitical considerations has fundamentally altered domestic production strategies across major economies. Supply chain vulnerabilities exposed during 2021-2022 demonstrated how external dependencies could threaten industrial competitiveness and economic stability. Consequently, these experiences reinforced government preferences for domestic capacity utilisation, even when marginal costs exceed imported alternatives.

Key Strategic Priorities Include:

• Domestic production capacity maintenance during transition periods

• Strategic fuel reserves covering 2-3 months of consumption requirements

• Grid integration protocols for managing renewable intermittency

• Import substitution policies reducing external supply dependencies

• Dual-track development expanding both traditional and alternative energy sources

The dual-track strategy represents more than hedging against supply risks; it reflects institutional learning from crisis periods when over-reliance on single technology pathways created systemic vulnerabilities. Coal's structural dominance, accounting for approximately 56-57% of total primary energy consumption in major economies, cannot be rapidly displaced without comprehensive infrastructure development and storage solutions. In addition, these strategic considerations align with broader OPEC oil production impact on global energy markets.

When big ASX news breaks, our subscribers know first

Decoding the Production-Consumption Disconnect

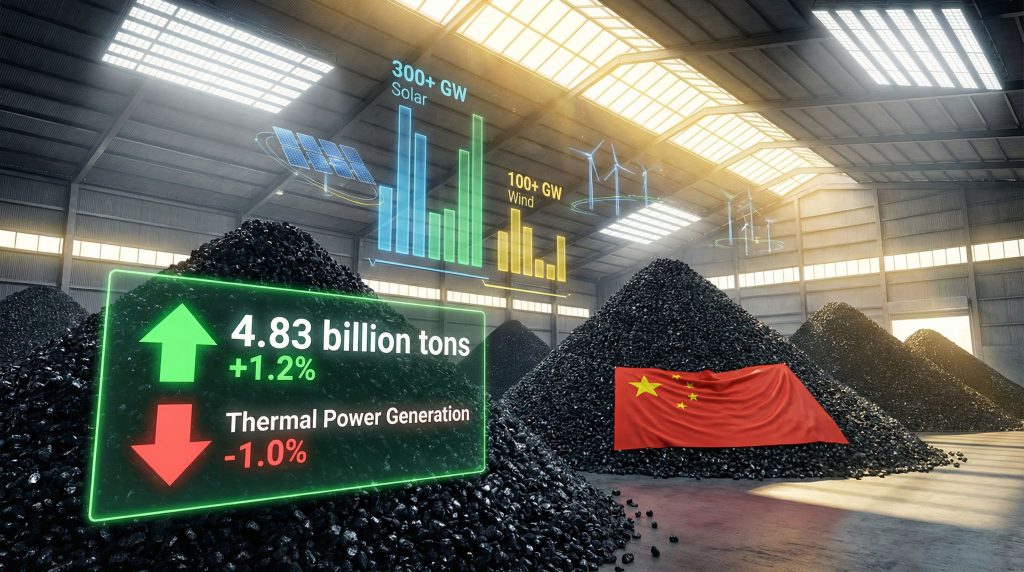

China's coal output record 2025 exemplifies the complex dynamics emerging in global energy markets, where production volumes diverge dramatically from consumption patterns. The nation achieved record coal production of 4.83 billion tons in 2025, representing a 1.2% increase from the previous year's 4.76 billion tons, while simultaneously experiencing its first annual decline in thermal power generation in a decade.

This apparent paradox reflects deliberate stockpiling strategies designed to provide insurance against multiple risk scenarios. Economic analysis reveals that maintaining higher utilisation rates at existing facilities costs significantly less than maintaining surge capacity idle or opening new capacity during crisis periods. However, with thermal coal spot prices reaching four-year lows during summer 2025, the cost of capital for holding additional inventory decreased substantially.

| Metric | 2024 | 2025 | Change |

|---|---|---|---|

| Domestic Production | 4.76B tons | 4.83B tons | +1.2% |

| Thermal Power Generation | Baseline | Declined | -1.0% |

| Coal Imports | 541M tons | 490M tons | -9.6% |

| Spot Price Performance | Elevated | 4-year minimum | Significant decline |

Market Dynamics Behind Inventory Accumulation

The production-consumption disconnect stems from several interconnected factors that create economic incentives for stockpiling despite reduced immediate demand. Marginal production costs at existing operations remain competitive with maintaining idle capacity, while renewable deployment variability creates demand uncertainty requiring flexible response capabilities.

Primary Economic Drivers:

- Marginal Cost Advantages: Operating existing mines at higher utilisation rates versus emergency capacity activation

- Inventory Financing Economics: Reduced holding costs during low-price environments

- Grid Planning Uncertainty: Weather-dependent renewable generation requiring backup reserves

- State Policy Coordination: Production targets independent of immediate consumption requirements

- Import Substitution Benefits: Domestic capacity utilisation reducing external dependencies

The strategic logic becomes clearer when considering renewable energy's intermittency challenges. While new wind and solar installations can meet average electricity demand, peak consumption periods and weather-related generation shortfalls require dispatchable backup capacity. For instance, coal stockpiles provide this flexibility without requiring immediate consumption decisions.

International Trade Flow Disruptions

The shift toward domestic energy security has created significant disruptions across international commodity markets, particularly affecting traditional coal exporters. China's coal output record 2025 contributed to a 9.6% reduction in coal imports, falling to approximately 490 million tons from 541 million tons in 2024, representing the largest annual import contraction in recent years.

This import reduction signals a structural transformation in global coal trade patterns, with major exporters facing direct revenue impacts and market share losses. Australia, historically supplying 60-80% of seaborne coal imports, confronts particular challenges as domestic production substitutes for imported thermal coal. Similarly, Indonesia's low-quality sub-bituminous coal, traditionally destined for coastal power plants, faces similar displacement pressures.

Regional Market Adaptations

| Market Segment | Typical Margin | Impact Assessment |

|---|---|---|

| Seaborne Thermal Coal | $5-15/ton | Compressed margins, reduced shipping demand |

| High-Energy Specialty Grades | Premium pricing | Selective demand maintains stability |

| Pacific Shipping Routes | Variable rates | Lower bulk carrier utilisation |

The trade flow disruptions extend beyond direct buyer-seller relationships to affect broader commodity infrastructure. Shipping costs on Pacific routes have compressed as reduced Chinese import demand decreases bulk carrier utilisation. Regional price arbitrage opportunities have narrowed significantly, constraining profitable trading activities and forcing geographic market rebalancing.

Market Adaptation Strategies:

• Australian exporters seeking alternative Asian markets (Japan, South Korea, India)

• Indonesian producers targeting emerging Southeast Asian consumers

• Shipping companies adjusting fleet deployment to different trade routes

• Commodity traders reducing arbitrage activities due to compressed spreads

• Mining companies reassessing expansion capital expenditure plans

Commodity Price Dynamics and Forward Market Implications

The convergence of oversupply conditions and reduced export demand has created textbook commodity bear market dynamics across thermal coal markets. Record production increases meeting declining consumption generated inventory accumulation and significant price compression, with thermal coal spot prices reaching four-year lows during summer 2025.

Forward curve analysis reveals market expectations of continued structural headwinds for thermal coal demand. Negative slope forward curves, where future prices trade below current spot levels, typically signal weak underlying demand expectations and restrain new capacity development. Consequently, mining companies historically reduce expansion capital expenditures when forward prices fail to justify new project economics.

Investment Decision Framework

The current price environment has fundamentally altered investment decision frameworks across the coal mining sector. Production cost curves indicate that many operations remain economically viable despite price compression, but new project development faces significant hurdles. Furthermore, coking coal markets maintain separate dynamics supporting metallurgical applications, but thermal coal faces persistent demand destruction pressures.

Investment Considerations by Timeframe:

• Short-term (1-2 years): Inventory management and production optimisation

• Medium-term (3-5 years): Renewable integration impacts and storage deployment

• Long-term (10+ years): Stranded asset risks and transition planning

• Technology factors: Clean coal initiatives and carbon capture potential

• Regulatory environment: Environmental standards and carbon pricing mechanisms

Regional price differentials have compressed significantly, reducing profitable arbitrage opportunities for commodity traders. Australian seaborne exports typically commanded $3-8/ton premiums over benchmark prices, while Indonesian domestic consumption enjoyed $5-10/ton discounts due to transportation cost savings. However, these spreads have narrowed substantially as oversupply conditions affect all market segments.

Learning from Historical Crisis Management

The 2021 energy crisis fundamentally reshaped energy policy architecture across major economies, providing critical lessons about supply chain vulnerabilities and transition planning risks. Rolling blackouts during Q3-Q4 2021 demonstrated how over-reliance on renewable deployment without adequate storage infrastructure could create systemic vulnerabilities during peak demand periods.

Government responses prioritised redundancy in energy supply systems, implementing dual-track development approaches that simultaneously expanded renewable capacity while maintaining fossil fuel backup capabilities. This strategic framework recognises that energy transitions require decades of coordinated infrastructure development rather than rapid single-technology deployment. In addition, this approach requires comprehensive investment strategies guide to navigate the transition effectively.

The 2021 crisis occurred when coal supply constraints coincided with surging post-pandemic electricity demand and restricted imports from major suppliers due to geopolitical tensions. Manufacturing disruptions and widespread power rationing highlighted the economic costs of energy supply interruptions.

Policy Response Evolution

State Council and National Development and Reform Commission directives issued following the 2021 crisis mandated increased coal mining capacity and established output targets for provincial governments and state-owned enterprises. These policies directly contributed to the production increases observed in 2025, representing institutional commitment to maintaining energy security buffers.

Crisis Response Framework:

- Emergency Production Mandates: Immediate capacity activation during supply shortfalls

- Strategic Reserve Building: 2-3 month consumption coverage through stockpiles

- Import Diversification: Reduced reliance on single-source suppliers

- Grid Infrastructure Investment: Enhanced transmission and storage capabilities

- Technology Integration: Advanced coal plant efficiency and emissions reduction

The lessons learned approach emphasises maintaining optionality rather than committing irreversibly to single technology pathways. This framework acknowledges that successful energy transitions require comprehensive infrastructure development, adequate storage solutions, and reliable backup capacity during intermittency periods.

Renewable Energy Integration and Grid Management

The rapid deployment of renewable energy capacity has begun reshaping fundamental demand patterns for traditional power sources. New solar capacity exceeding 300 GW and wind installations surpassing 100 GW in 2025 provided sufficient clean energy generation to meet growing electricity demand without increased thermal power output, marking a significant milestone in energy transition progress.

Provincial case studies demonstrate the scale and pace of this transformation. Shanxi province, historically the largest coal-producing region, achieved alternative energy output of 118 billion kWh in 2025, representing 26% growth and reaching approximately 50% of total generation capacity. Consequently, this transition occurred alongside continued coal production increases, illustrating the dual-track development strategy.

Grid Integration Challenges

Wind and solar capacity reaching 78.8 GW in traditional coal-producing regions creates complex grid management challenges. Intermittent renewable generation requires sophisticated load balancing mechanisms and backup power capabilities during low-wind or cloudy periods. Furthermore, coal plants increasingly serve peaking and grid stability functions rather than baseload power generation.

Technical Integration Requirements:

• Advanced grid control systems managing variable renewable output

• Energy storage deployment enabling load shifting and frequency regulation

• Transmission infrastructure connecting renewable generation centres to demand centres

• Backup power coordination during renewable generation shortfalls

• Market mechanisms pricing grid stability services and capacity reserves

The economic implications of this transition extend beyond generation patterns to affect coal plant utilisation rates and financial viability. Capacity factors at thermal facilities decline as they operate fewer hours annually, potentially undermining project economics and requiring alternative revenue streams for grid stability services.

The next major ASX story will hit our subscribers first

Global Energy Infrastructure Development Trends

Coal plant construction patterns reveal the complex relationship between capacity expansion and utilisation expectations. Approximately 55 GW of new coal-fired capacity planned for 2026 represents the majority of 63 GW global additions, but these facilities increasingly serve backup and peaking roles rather than continuous baseload operation.

This infrastructure development reflects recognition that energy transitions require maintaining dispatchable power capabilities while renewable capacity scales up. Advanced coal plant technologies incorporating improved efficiency and reduced emissions per unit of power provide bridge capabilities during transition periods. Moreover, carbon capture and storage pilot programmes at new facilities explore pathways for continued fossil fuel use with reduced environmental impact.

Technology and Efficiency Improvements

Modern coal facilities incorporate significant technological advances compared to older generation plants. These improvements include higher thermal efficiency ratings, advanced emissions control systems, and enhanced grid flexibility capabilities supporting renewable integration. Grid flexibility enhancements enable rapid ramping capabilities responding to renewable generation variability.

Technology Integration Benefits:

- Efficiency Gains: Higher energy output per unit of fuel consumed

- Emissions Reduction: Advanced control systems minimising environmental impact

- Grid Flexibility: Rapid response capabilities supporting renewable integration

- Operational Optimisation: Automated control systems improving plant performance

- Maintenance Efficiency: Predictive maintenance reducing downtime and costs

Investment in these technologies reflects long-term strategic planning recognising that coal infrastructure will operate for decades during energy transition periods. Enhanced capabilities ensure these assets contribute positively to grid stability and reliability while renewable infrastructure matures.

Safety Regulations and Production Management

Government safety inspection campaigns significantly impacted production patterns during the second half of 2025, demonstrating how regulatory priorities can override pure economic considerations. Monthly production declines followed intensified investigation protocols, creating tension between worker safety mandates and energy security objectives.

The mining industry has adapted to enhanced safety protocols through increased investment in safety technology, worker training programmes, and operational procedures. These compliance costs affect production economics but reflect long-term commitments to sustainable operating practices and social responsibility.

Operational Efficiency Considerations

Balancing safety compliance with production targets requires sophisticated operational management and technology integration. Modern mining operations employ advanced monitoring systems, automated equipment, and predictive safety analytics to maintain both productivity and safety standards.

Safety-Production Balance Strategies:

• Advanced monitoring systems providing real-time safety data

• Automated mining equipment reducing worker exposure to hazardous conditions

• Predictive analytics identifying potential safety risks before incidents occur

• Enhanced training programmes ensuring worker competency and safety awareness

• Investment in safety technology improving both protection and efficiency

Long-term productivity implications of stricter oversight include improved operational practices, reduced accident-related downtime, and enhanced workforce retention. While compliance costs impact short-term margins, safety improvements contribute to sustainable operational excellence and community acceptance.

Diversified Energy Portfolio Development

Natural gas and crude oil production achievements complement coal output trends, demonstrating comprehensive domestic energy resource development strategies. Natural gas output achieved its 33rd consecutive annual record, while crude oil production surpassed 2015 highs, indicating systematic efforts to reduce single-fuel dependency risks across multiple energy sources.

This diversification strategy provides flexibility during energy transition periods while maintaining supply security across different economic sectors. Natural gas serves as a cleaner alternative for industrial applications and power generation, while petroleum products remain essential for transportation and petrochemical industries. Additionally, these trends align with broader US natural gas forecasts for the energy sector.

Critical Minerals and Energy Storage

The energy transition requires significant quantities of critical minerals including lithium, cobalt, and rare earth elements supporting renewable infrastructure and energy storage systems. Battery storage deployment enables better integration of intermittent renewable generation while providing grid stability services traditionally supplied by conventional power plants. This critical minerals strategy becomes increasingly vital for supply chain security.

Supply Chain Security Considerations:

| Mineral Category | Primary Applications | Supply Chain Risks |

|---|---|---|

| Lithium | Battery storage, electric vehicles | Geographic concentration |

| Rare earth elements | Wind turbines, solar panels | Processing capacity limitations |

| Cobalt | Energy storage systems | Geopolitical supply risks |

| Copper | Grid infrastructure, renewable systems | Demand growth exceeding supply |

Energy storage deployment creates new demand patterns for critical minerals while enabling coal plants to serve load balancing functions rather than continuous operation. This technological integration supports grid stability during renewable intermittency periods without requiring constant fossil fuel consumption. However, securing these critical raw materials transition remains a key challenge.

Investment Framework and Market Psychology

Understanding the divergent signals from China's coal output record 2025 requires sophisticated analysis of short-term versus long-term investment implications. Near-term coal demand benefits from energy security priorities and stockpiling strategies, while medium-term headwinds emerge from accelerating renewable deployment and storage technology advancement.

Regional mining company exposure varies significantly based on market positioning and geographic focus. Australian thermal coal exporters face reduced Chinese demand and must adapt to changing trade patterns, while Indonesian producers seek alternative Southeast Asian markets. Furthermore, domestic Chinese miners benefit from import substitution policies but confront long-term demand decline scenarios.

Investment Decision Matrix

| Investment Category | Short-Term Outlook | Long-Term Outlook | Primary Risk Factors |

|---|---|---|---|

| Chinese Domestic Mining | Positive (stockpiling demand) | Neutral (gradual decline) | Policy shifts, safety regulations |

| Thermal Coal Exporters | Negative (reduced imports) | Negative (demand destruction) | Stranded assets, market access |

| Renewable Equipment | Positive (capacity growth) | Very Positive (transition acceleration) | Technology disruption, competition |

| Energy Storage Technology | Very Positive (grid integration) | Very Positive (transition enabler) | Cost reduction pressure, scaling |

Market psychology reflects uncertainty about transition timelines and policy consistency. Investors must balance energy security imperatives supporting continued coal demand against accelerating renewable deployment and storage technology advancement. Forward-looking analysis suggests that coal's role will increasingly shift toward grid stability and backup functions rather than primary energy supply. China's coal production surge continues despite changing demand patterns.

Risk Assessment Framework

Investment decisions require comprehensive risk assessment encompassing regulatory changes, technology development, and demand evolution patterns. Carbon pricing mechanisms, environmental regulations, and international climate commitments create additional uncertainty layers affecting long-term asset valuations.

Key Risk Categories:

- Regulatory Risk: Environmental standards and carbon pricing policies

- Technology Risk: Renewable cost reduction and storage advancement

- Demand Risk: Economic growth patterns and energy efficiency improvements

- Geopolitical Risk: Trade relations and supply chain security considerations

- Stranded Asset Risk: Long-term demand destruction and facility obsolescence

Successful investment strategies require acknowledging these transition dynamics while identifying opportunities in both traditional and alternative energy sectors. Portfolio diversification across energy sources and technology categories provides exposure to transition benefits while managing downside risks from demand shifts.

Environmental Progress and Climate Policy Integration

Despite record coal production levels, carbon intensity improvements demonstrate progress toward environmental objectives through efficiency gains and clean energy offsetting. Emissions per unit of economic output continue declining as renewable energy meets incremental electricity demand growth, indicating pathway compatibility with pre-2030 carbon peak commitments.

International climate diplomacy benefits from renewable energy leadership credentials while acknowledging continued coal dependence during transition periods. Technology transfer opportunities in clean energy sectors create cooperative frameworks supporting global decarbonisation objectives while maintaining energy security priorities. Coal power declines globally despite production increases.

Carbon Market Participation

Global carbon market participation and offset mechanisms provide pathways for continued fossil fuel use with environmental impact mitigation. Carbon capture and storage initiatives at new coal facilities explore technological solutions reducing emissions intensity while maintaining energy security capabilities.

Climate Policy Integration Strategies:

• Efficiency improvements reducing emissions per unit of energy produced

• Renewable energy acceleration offsetting fossil fuel consumption growth

• Technology development enabling cleaner coal utilisation methods

• Carbon market participation providing economic incentives for emissions reduction

• International cooperation supporting global climate objectives while maintaining energy security

The environmental trajectory suggests that absolute coal consumption may decline even while production capacity remains elevated for security purposes. This dynamic enables climate progress through demand reduction while maintaining supply capabilities for emergency situations or renewable intermittency management.

Disclaimer: This analysis involves forecasts, market projections, and speculation about future energy market developments. Investment decisions should consider multiple factors including regulatory changes, technology advancement, and market volatility. Past performance and current trends do not guarantee future results. Readers should consult qualified financial and industry advisors before making investment decisions based on this analysis.

Ready to Capitalise on Energy Market Transitions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across energy transition materials and traditional resources, instantly empowering investors to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in navigating complex energy infrastructure investments.