July 25, 2026

The Future of Energy Storage: How Resource Abundance Could Transform Australia's Position

The global transition toward electrification has created unprecedented demand for specialized materials that power next-generation energy systems. Among these critical resources, one mineral stands out for its dual advantage of technical necessity and supply chain vulnerability. Understanding how resource endowment intersects with processing capabilities reveals pathways for nations to capture substantial value in emerging clean energy markets.

Australia's mineral wealth extends far beyond traditional exports, encompassing materials essential for modern battery technologies. The question of can graphite help charge Australia's battery market opportunity emerges as global supply chains face concentration risks and demand accelerates across multiple sectors.

When big ASX news breaks, our subscribers know first

What Makes Graphite Australia's Hidden Battery Goldmine?

The Critical Mineral Behind Every Electric Vehicle

Graphite functions as the primary anode material in lithium-ion batteries, comprising approximately 25-30% of total battery mass in typical electric vehicle applications. This substantial proportion makes graphite the largest mineral component by weight in standard lithium-ion cells, according to International Graphite Association data and peer-reviewed battery chemistry research.

The technical specifications driving EV performance standards require high-purity natural graphite with over 99% carbon content and specific particle size distribution, typically 15-30 micrometers for spheroidized material. These electrochemical requirements include maintaining electrical conductivity above 100 S/cm and reversible lithium intercalation capacity of approximately 372 mAh/g.

Performance standards extend beyond basic composition to thermal stability requirements, where graphite anodes must maintain structural integrity across operating temperatures from -20°C to +60°C in automotive battery packs. A Tesla Model 3 battery pack utilizes approximately 8-12 kg of graphite anode material per vehicle, demonstrating the scale of material requirements for mass EV adoption.

Australia's Untapped Resource Advantage

Australia ranks eighth globally for natural graphite reserves with approximately 4% of world reserves as of December 2023, according to Geoscience Australia data. The nation's confirmed resource base encompasses approximately 130 million tonnes of identified graphite resources distributed across key geological formations.

Geographic distribution spans multiple states with distinct geological advantages:

- South Australia: Primary graphite regions include the Adelaide Geosyncline formations

- Western Australia: Significant deposits in the Pilbara and Yilgarn Craton regions

- Queensland: Graphite occurrences across various geological structures

The CSIRO report "Australian graphite: A path to a global battery market opportunity," developed in collaboration with Geoscience Australia and Stanford University, emphasises that Australia's resource position creates substantial strategic opportunities for domestic value capture through processing development.

Current domestic graphite demand for batteries reaches an estimated 5,000-8,000 tonnes annually, with projections indicating growth to 50,000+ tonnes by 2033 according to Geoscience Australia resource demand modelling. This trajectory reflects both domestic EV adoption and potential export market development.

How Could Australia Transform Raw Resources Into Battery-Grade Gold?

The Value Chain Transformation Opportunity

The economic potential of downstream processing becomes apparent through price differential analysis. Raw graphite concentrate at 95% purity commands approximately USD $200-300 per tonne at export pricing, while spherical anode material reaches USD $8,000-15,000 per tonne for battery-grade specifications, representing a 40-75x price multiplier according to International Graphite Association and Benchmark Mineral Intelligence data.

Processing technology requirements encompass multiple stages of refinement and preparation. Purification involves removing impurities through acid leaching or advanced flotation techniques, while spheroidization processes utilise specialised equipment with precise temperature control ranging from 600-1200°C.

| Processing Stage | Investment Range (AUD) | Timeline | Production Capacity |

|---|---|---|---|

| Concentrate Production | $50-150 million | 2-3 years | 50,000-100,000 tpa |

| Spherical Graphite | $200-400 million | 3-4 years | 20,000-40,000 tpa |

| Integrated Operations | $500-800 million | 4-5 years | 100,000+ tpa |

Infrastructure development requires substantial capital allocation across multiple operational areas. Modern processing facilities demand automated quality control systems, real-time particle analysis capabilities, and environmental compliance infrastructure for acid neutralisation and waste management.

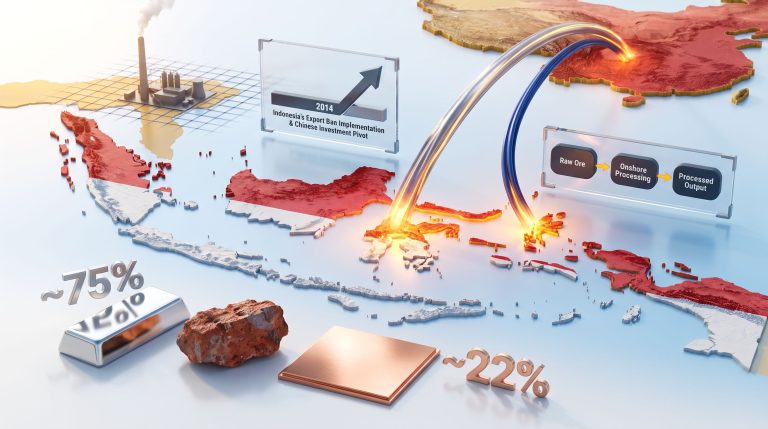

Breaking China's Processing Monopoly

China's downstream processing dominance reaches approximately 95% of global anode material production, creating systemic supply chain vulnerability for international battery manufacturers. This concentration encompasses roughly 400,000+ tonnes of annual anode material production controlled by major Chinese processors including Shanshan Co., BTR New Material Group, and Jiangxi Zichen Technology.

The CSIRO assessment identifies that Australia's primary competitive challenge stems not from resource availability but from the absence of established downstream processing infrastructure. Developing battery-grade graphite processing capabilities represents a critical opportunity for capturing substantially higher domestic value retention.

Supply chain vulnerability assessments indicate that average automotive battery producers source 60-80% of graphite requirements from China, with typical lead times of 6-8 weeks creating potential inventory gaps of 2-3 months during supply disruptions, according to Benchmark Mineral Intelligence supply chain resilience studies.

Alternative processing hub development could leverage Australia's geographic position within trusted geopolitical alliance structures, renewable energy abundance, and established mining infrastructure to create strategic supplier diversification for global battery manufacturers. Furthermore, this mining technology innovations approach aligns with broader industry transformation trends.

What Economic Scenarios Could Unfold for Australia's Battery Market?

Market Growth Projections and Revenue Potential

Global lithium-ion battery markets currently reach USD 130-150 billion annually with projected compound annual growth rates of 15-20% through 2033, driven by accelerating EV adoption and grid storage deployment according to BloombergNEF and International Energy Agency analysis.

| Scenario | 2025 Market Size | 2033 Projected Size | CAGR |

|---|---|---|---|

| Conservative | AUD 4.2 billion | AUD 7.8 billion | 8.3% |

| Moderate | AUD 5.1 billion | AUD 9.6 billion | 8.4% |

| Aggressive | AUD 6.3 billion | AUD 12.1 billion | 9.2% |

Australia's current battery market encompasses approximately AUD 2.5-3.0 billion including manufacturing, recycling, and supply components according to Australian Industry Commission and CSIRO critical minerals analysis. The domestic market trajectory indicates substantial expansion potential driven by multiple demand vectors.

Processing margins demonstrate significant economic leverage, with 200-400% gross margins achievable on finished anode material compared to raw concentrate. Capital recovery periods typically span 7-10 years for integrated processing facilities operating at full capacity, with operating leverage providing substantial profitability scaling opportunities.

Grid-Scale Storage Driving Domestic Demand

Australia's renewable energy deployment targets of 400+ GW capacity by 2030 imply 50-80 GWh annual battery storage requirements, representing approximately 20,000-30,000 tonnes of graphite demand for grid-scale applications. Each megawatt-hour battery system requires approximately 300-400 kg of graphite material.

EV adoption trajectories show 17.9% of new car sales in 2024 with government policy targets reaching 50%+ by 2030 according to Electric Vehicle Council Australia data. First major battery replacement cycles for 2015-era EVs expected during 2025-2028 will create additional aftermarket demand for anode materials.

Market segmentation analysis reveals:

- Electric vehicle batteries: 65-70% of graphite demand

- Grid-scale energy storage systems: 20-25% of demand (fastest growing segment)

- Portable electronics and consumer batteries: 5-10% of demand

Which Processing Pathways Offer the Greatest Strategic Advantage?

Traditional vs. Synthetic Graphite Production Routes

Natural graphite purification demonstrates significant economic and environmental advantages over synthetic alternatives. Natural graphite processing costs range from AUD $500-1,000 per tonne compared to AUD $2,000-3,500 per tonne for synthetic production, with natural graphite facilities requiring 40-50% lower capital investment according to International Graphite Association analysis.

Energy consumption comparisons reveal substantial efficiency gains for natural graphite processing. Synthetic graphite production requires 8-12 MWh per tonne for high-temperature furnace operation, while natural graphite purification and spheroidization consumes 1.5-3 MWh per tonne.

Environmental impact assessments show natural graphite from renewable-powered facilities generates 2-5 tonnes CO₂e per tonne of anode material compared to 8-15 tonnes CO₂e per tonne for synthetic graphite from conventional energy sources, according to IVL Swedish Environmental Research Institute lifecycle assessments.

The CSIRO research emphasises that Australia's natural graphite deposits combined with abundant renewable energy resources create distinctive competitive advantages for producing low-carbon, battery-grade materials. This environmental differentiation increasingly represents market advantages as battery manufacturers face Scope 3 emissions reporting requirements.

Regional Processing Hub Development Strategies

State-by-state infrastructure analysis reveals comparative advantages across different processing approaches. Additionally, this development coincides with broader EV battery transformation trends reshaping the industry landscape.

Flotation-based purification:

- Selective reagent chemistry separating graphite from silicate minerals

- Produces concentrates of 95-98% carbon purity

- Capital requirements: AUD $50-100 million for 50,000 tpa facilities

Acid leaching purification:

- Sulfuric or hydrochloric acid removal of mineral impurities

- Achieves higher purity levels (98-99.5%) with acid waste neutralisation requirements

- Capital requirements: AUD $80-150 million for integrated facilities

Spheroidization and coating:

- High-temperature thermal treatment at 600-1200°C for particle rounding

- Silicon oxide or carbon coating application for enhanced electrochemical performance

- Capital requirements: AUD $200-400 million for fully integrated operations

Port access and logistics optimisation favour coastal processing locations with proximity to renewable energy sources. South Australia, Western Australia, and Queensland each offer distinct advantages for different scales and types of processing operations.

How Will Global Supply Chain Disruptions Shape Australia's Opportunity?

Geopolitical Risk Assessment

Chinese processor concentration creates systemic vulnerabilities for global battery supply chains. The top three Chinese processors control approximately 60-70% of global downstream capacity, with trade restrictions implemented multiple times between 2018-2024 affecting battery material access according to Bloomberg NEF supply chain analysis.

The European Union's Critical Raw Materials Act (2023) and US Department of Commerce Critical Minerals List recognise graphite supply vulnerability as strategic national security concerns. These regulatory frameworks create policy incentives for supply chain diversification away from single-source dependencies.

Australia's position within trusted geopolitical alliance structures, combined with resource endowment and processing capability potential, creates strategic supplier alternatives for Western battery manufacturers and governments pursuing energy security objectives. However, the US–China trade impact continues to influence global supply chain decisions.

Technology transfer restrictions limit access to proprietary Chinese spheroidization and coating techniques, creating opportunities for domestic innovation in processing methods and equipment development.

ESG-Driven Market Differentiation

Sustainable mining practices increasingly represent competitive advantages in global battery material markets. Carbon footprint reduction through renewable-powered processing aligns with automotive manufacturer sustainability mandates and ESG investment criteria.

Certification standards and traceability requirements create premium pricing opportunities for materials produced under verifiable environmental and social governance frameworks. Australian operations can leverage established regulatory compliance systems and transparency standards.

Water management strategies, dust control requirements, and acid neutralisation protocols demonstrate operational excellence capabilities that differentiate Australian processing from alternatives in regions with less stringent environmental oversight.

The next major ASX story will hit our subscribers first

What Investment Scenarios Could Unlock Australia's Graphite Potential?

Capital Requirements for Market Entry

Investment thresholds for commercial-scale operations vary significantly based on integration levels and production targets. Modular facility development approaches can reduce initial capital requirements while maintaining expansion flexibility.

Processing facility cost breakdown:

- Ore processing plants: AUD $50-150 million

- Purification facilities: AUD $100-200 million

- Spheroidization equipment: AUD $200-400 million

- Quality assurance laboratories: AUD $20-50 million

- Environmental compliance systems: AUD $30-70 million

Standard processing yields achieve 70-85% of input material as usable anode product, with remainder requiring recycling or alternative applications. Production cycles typically span 6-8 weeks from extraction to finished anode material.

Public-Private Partnership Models

Government co-investment frameworks can provide risk-sharing mechanisms aligned with critical minerals strategy and national security objectives. Export finance and trade promotion support structures facilitate market access and customer relationship development.

Strategic timing considerations include market entry windows before competitor capacity expansion, technology maturation cycles, and regulatory approval timelines. Optimal investment phases align with demand growth trajectories and supply gap emergence.

Long-term supply agreements with 5-10 year contract durations provide revenue stability for capital recovery while offering customers supply security. Pricing mechanisms typically incorporate base prices with volume adjustments and quality premiums. Furthermore, considerations around battery metals investment trends continue to shape market dynamics.

Which Market Segments Present the Highest Value Opportunities?

Electric Vehicle Battery Demand Scenarios

Tesla's projected 3+ million annual production capacity represents approximately 30,000+ tonnes of annual graphite requirements at current battery specifications. Similar scaling across global automotive manufacturers creates substantial addressable market growth.

Australian EV adoption trajectories and battery replacement cycles generate both domestic consumption and export market potential to Asia-Pacific manufacturing hubs. Premium pricing opportunities exist for high-purity anode materials meeting advanced battery chemistry specifications.

Market concentration risks include exposure to Tesla, BYD, and CATL, which collectively represent over 60% of global battery production. Diversification strategies across multiple end-use applications reduce customer dependency vulnerabilities.

Energy Storage System Integration

Utility-scale battery project pipelines demonstrate accelerating deployment schedules aligned with renewable energy integration requirements. Grid storage applications typically require different material specifications than automotive applications, creating market segmentation opportunities.

Residential storage market growth expands addressable demand beyond utility-scale applications, with different quality requirements and supply chain structures. Industrial applications including backup power systems and manufacturing process storage create additional demand vectors.

What Technological Innovations Could Accelerate Market Penetration?

Next-Generation Processing Technologies

Advanced purification methods focus on reducing environmental impact while improving cost competitiveness. Automation and digitalisation technologies enhance quality control consistency and reduce labour requirements for commercial operations.

Real-time particle analysis systems enable continuous quality optimisation during processing, reducing waste and improving yield rates. These technological capabilities differentiate Australian processing from conventional approaches.

Alternative feedstock development includes biomass-derived synthetic graphite commercialisation pathways and recycling technologies for end-of-life battery materials. Hybrid production models combining natural and synthetic sources optimise cost-performance characteristics. Additionally, the emerging battery recycling breakthrough technologies from China present both competitive challenges and collaborative opportunities.

Alternative Feedstock Development

Technology disruption scenarios must consider potential impacts from silicon-dominant anodes or solid-state batteries on graphite demand projections. However, current technical and commercial timelines suggest graphite will remain dominant for the foreseeable investment horizon.

The emerging recycling innovations in Australia, including research at Charles Sturt University into creating graphite from hair and wool waste, demonstrate alternative pathways for sustainable battery material production.

Recycling capability development creates circular economy opportunities while reducing primary resource requirements. End-of-life battery processing can recover high-quality graphite for reprocessing into new anode applications.

How Should Australia Position for Long-Term Market Leadership?

Strategic Timing Considerations

Market entry timing requires balancing first-mover advantages with technology maturation and demand certainty. Current supply-demand dynamics create favourable conditions for new capacity development before major competitor expansion phases.

Regulatory approval timelines for processing facilities typically span 2-4 years depending on environmental assessment complexity and community engagement requirements. Strategic positioning requires early initiation of permitting processes aligned with market timing objectives.

Competitive positioning frameworks must balance cost leadership strategies with differentiation approaches based on sustainability, quality, or supply chain reliability advantages.

Competitive Positioning Framework

Vertical integration opportunities across the value chain enable capture of multiple processing margins while reducing supply chain dependencies. Strategic partnerships with battery manufacturers and original equipment manufacturers create demand security and market intelligence advantages.

Technology transfer and intellectual property protection strategies ensure competitive advantages in processing methods and quality systems. Workforce development and skills training programmes create operational excellence capabilities supporting long-term competitiveness.

What Risk Mitigation Strategies Ensure Sustainable Growth?

Market Volatility Management

Demand forecasting accuracy becomes critical for capacity planning flexibility given substantial capital requirements and long asset lifecycles. Price hedging mechanisms and long-term supply agreements provide revenue stability during market volatility periods.

Currency exposure management addresses AUD vs. USD exchange rate impacts on export revenue, with natural hedging opportunities through domestic cost structures and international revenue diversification.

Diversification across multiple end-use applications reduces dependence on single market segments while capturing growth across different demand drivers and cycle timing.

Operational Excellence Requirements

Environmental compliance and community engagement protocols ensure sustainable social licence for operations. These frameworks become increasingly important as ESG considerations influence customer selection and investment decisions.

Market psychology factors include investor sentiment toward critical minerals, battery technology adoption rates, and geopolitical supply chain security concerns. Understanding these dynamics enables better strategic decision-making and risk management.

Water consumption requirements typically reach 100-150 tonnes per tonne of processed graphite, necessitating sustainable water management strategies particularly in arid regions of Australia where graphite deposits are located.

Key Insight: The convergence of resource endowment, market timing, and strategic necessity creates unprecedented opportunities for Australia to establish critical supply chain positions while capturing substantial value-addition through domestic processing capabilities that reduce global dependence on concentrated supply sources.

Investment Disclaimer: This analysis contains forward-looking projections and market assessments that involve inherent uncertainties. Commodity prices, technology adoption rates, and geopolitical factors may significantly impact actual outcomes compared to scenarios presented. Readers should conduct independent due diligence and consult qualified advisors before making investment decisions.

Looking to Capitalise on Australia's Battery Materials Revolution?

Discovery Alert's proprietary Discovery IQ model provides instant notifications when ASX companies announce significant mineral discoveries, including graphite and other critical battery materials driving the energy storage transformation. With Australia's graphite processing opportunity potentially worth billions and major discoveries historically generating substantial returns for early investors, subscribers gain immediate access to actionable insights ahead of the broader market. Begin your 30-day free trial today to position yourself at the forefront of Australia's battery materials opportunity.