June 28, 2026

The global mining sector stands at a pivotal intersection where environmental accountability meets unprecedented demand for renewable energy infrastructure. As governments worldwide commit to aggressive decarbonisation targets, the extraction of energy transition minerals has emerged as both an enabler of clean energy and a source of climate concern. Understanding the true emissions footprint of mining operations becomes essential for investors, policymakers, and industry leaders navigating this complex landscape.

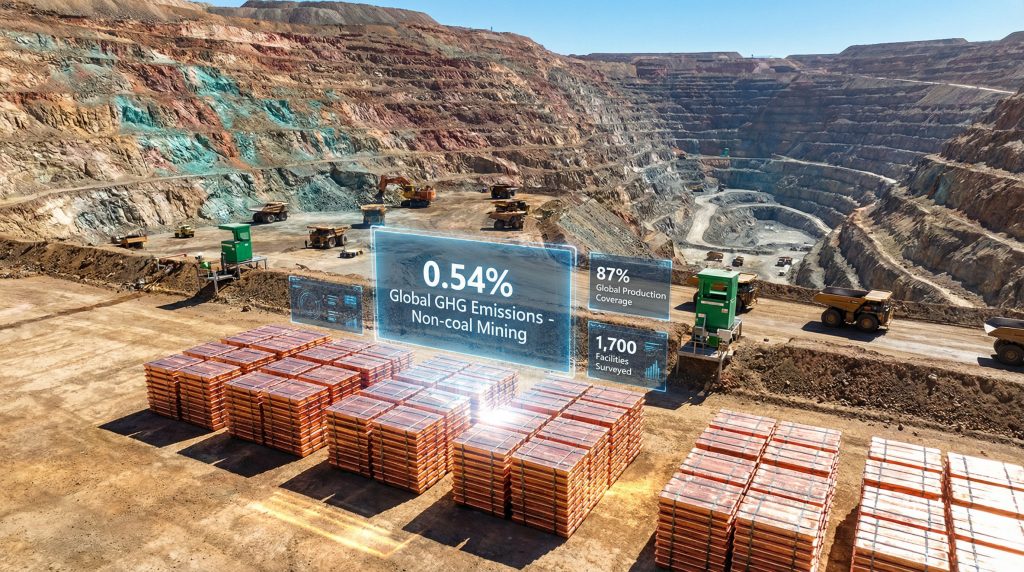

Quantifying Mining's True Climate Impact Through Comprehensive Data Analysis

The ICMM Energy Transition Minerals Report represents the most comprehensive assessment of global mining sector emissions to date, surveying 1,700 facilities across 14 commodity categories. This dataset covers 87% of global production volumes, with statistical modelling applied to estimate the remaining 13% of mining activities worldwide.

The methodology employed by ICMM focuses on Scope 1 and Scope 2 emissions measurement, capturing both direct emissions from mining operations and indirect emissions from purchased electricity. This dual-scope approach provides unprecedented transparency into an industry that has historically lacked comprehensive emissions tracking.

Global Mining Emissions Distribution

The mining and metals sector contributed 11% of total global greenhouse gas emissions in 2024, comprising 3% from mining activities and 8% from metal production. Within this framework, 93% of emissions were classified as Scope 1 (direct emissions) while 7% represented Scope 2 (indirect emissions from purchased electricity).

| Emission Source | Percentage of Sector Emissions | Global GHG Contribution |

|---|---|---|

| Steel production | 55% | 6.05% |

| Coal mining | 23% | 2.53% |

| Aluminium production | 15% | 1.65% |

| Other mining activities | 7% | 0.77% |

Steel production emerges as the dominant contributor, representing 55% of sector emissions due to the prevalence of highly carbon-intensive blast furnace-basic oxygen furnace (BF-BOF) processes. Approximately 70% of global steel production currently relies on these energy-intensive methods, creating substantial opportunities for technological transformation.

Regional Concentration of Mining Emissions

Asia generates 80% of global mining sector emissions, reflecting its dual role as both a primary mining centre and the dominant processing hub for most commodities. This concentration creates both efficiency advantages through economies of scale and vulnerabilities through geographic concentration of high-emissions activities.

Europe demonstrates extreme specialisation, with 93% of its mining-related emissions originating from steel production. This pattern indicates that European operations have largely transitioned away from primary extraction while retaining energy-intensive processing activities.

In Africa and the Middle East, aluminium production accounts for 40% of regional mining emissions, highlighting the significance of bauxite processing and smelting operations in these regions. The Americas exhibit more diversified commodity portfolios, distributing emissions risk across multiple mineral extraction and processing activities.

When big ASX news breaks, our subscribers know first

Reframing Energy Transition Mineral Extraction Within Global Emissions Context

The ICMM Energy Transition Minerals Report fundamentally challenges assumptions about the climate burden of renewable energy material sourcing. Non-coal mining activities contributed only 0.54% of global greenhouse gas emissions in 2024, while fugitive emissions from coal mining alone accounted for 2.46% of global emissions.

This 4.6-fold differential demonstrates that extracting minerals essential for energy transition generates substantially lower emissions per unit than traditional fossil fuel extraction. The comparison directly addresses concerns that renewable energy infrastructure development might carry comparable climate costs to fossil fuel systems.

Critical Minerals Versus Traditional Resource Extraction

"The data fundamentally challenges assumptions about energy transition mining being a major emissions driver compared to traditional fossil fuel extraction."

The distinction between energy transition minerals and conventional resources becomes particularly significant when examining extraction methodologies. Copper mining for electrical systems, lithium extraction for batteries, and cobalt mining for energy storage collectively fall within the 0.54% global emissions contribution from non-coal mining.

Traditional coal extraction, by contrast, involves both direct mining emissions and substantial fugitive methane releases during extraction and transportation. These fugitive emissions represent unavoidable consequences of coal extraction that persist throughout the mining lifecycle.

Production Intensity Analysis

Between 2020 and 2024, greenhouse gas emissions from mining and metal production increased 3% in absolute terms. This growth reflects the dual pressures of extraction intensity and rising global demand for commodities driven by energy transition requirements.

The relatively modest increase suggests that efficiency improvements are partially offsetting demand pressures, though absolute decarbonisation remains challenging. The mining sector faces the complex task of scaling production to meet renewable energy demand whilst simultaneously reducing emissions intensity.

Strategic Supply Chain Implications for Energy Transition Materials

The transition to renewable energy systems creates unprecedented demand pressures across critical mineral supply chains. Understanding these dynamics becomes essential for strategic planning across multiple stakeholder groups.

Demand Acceleration Across Key Commodities

Copper requirements are projected to double by 2050, reflecting copper's essential role in electrical transmission, generation equipment, and battery systems. This doubling represents cumulative demand over the next 24 years that will exceed total historical copper extraction.

Cobalt demand faces a 20-fold increase by 2040, driven by its critical role in battery cathode chemistry for current lithium-ion technology. This extraordinary escalation represents an average annual growth rate of approximately 22%, exponentially higher than historical cobalt production patterns.

Lithium extraction confronts distinct scaling challenges including:

- Extremely high water consumption requirements

- Geographic concentration of economically viable deposits

- Technology trade-offs between brine extraction and hard-rock mining methods

- Long development timelines for new production capacity

Furthermore, the surge in critical minerals demand creates complex bottlenecks that could constrain battery production scaling, though specific demand projections vary significantly across forecasting methodologies.

Primary Mining Development Constraints

New primary mining projects typically require 10-20 years from discovery to full production, highlighting the critical importance of early investment and planning. This extended timeline creates structural challenges for meeting accelerated renewable energy deployment schedules.

The development timeline encompasses:

- Exploration and resource definition (2-5 years)

- Feasibility studies and permitting (3-7 years)

- Construction and commissioning (3-5 years)

- Ramp-up to full production (1-3 years)

Recycling Potential and Limitations

Recycling could offset 25-40% of critical mineral demand by 2050, providing partial relief for primary mining pressure. However, recycling capacity is projected to address less than 10% of demand by 2030, indicating continued reliance on primary extraction throughout the critical transition decade.

Current recycling infrastructure faces several constraints:

- Limited collection and processing capacity for end-of-life renewable energy equipment

- Technology limitations for extracting materials from complex battery chemistries

- Economic challenges where recycled materials compete with primary extraction costs

- Geographic misalignment between renewable energy deployment and recycling facilities

Technological Pathways for Mining Sector Decarbonisation

The mining industry possesses multiple technological levers for reducing emissions intensity whilst scaling production to meet energy transition demands. Consequently, companies are exploring various approaches to implement sustainable mining transformation across their operations.

Steel Production Transformation Strategies

Global steel decarbonisation centres on transitioning away from blast furnace-basic oxygen furnace (BF-BOF) crude steel production toward lower-emissions electric arc furnace (EAF) methods. This technological shift offers several advantages:

- Increased scrap steel utilisation, reducing demand for primary iron ore extraction

- Reduced coal dependency in production processes

- Improved flexibility for renewable electricity integration

- Lower capital requirements for new production capacity

EAF technology currently processes approximately 30% of global steel production, with expansion potential constrained primarily by scrap steel availability rather than technological limitations.

Aluminium Smelting Electrification

Aluminium production represents one of the most electricity-intensive industrial processes, consuming approximately 3% of global electricity generation. Decarbonisation strategies focus on:

- Renewable electricity procurement for smelting operations

- Grid infrastructure development to support renewable energy integration

- Energy storage integration to manage intermittent renewable electricity supply

- Process optimisation to reduce overall electricity consumption

The capital-intensive nature of aluminium smelting facilities, with operating lives exceeding 50 years, creates particular challenges for rapid technological transition.

Mining Fleet and Operations Electrification

Mining operations increasingly deploy electric vehicle fleets and renewable energy systems to reduce direct emissions:

- Electric haul trucks and excavators for reduced diesel consumption

- Solar and wind installations at remote mine sites

- Battery storage systems for grid stabilisation and backup power

- Process optimisation software for energy efficiency improvements

Investment Framework for Mining Sector Transformation

The combination of growing demand and decarbonisation requirements creates complex investment dynamics across the mining sector. Moreover, understanding mining innovation trends becomes crucial for strategic decision-making.

Capital Allocation Priorities

Mining companies face competing demands for capital investment across multiple priorities:

| Investment Category | Time Horizon | Risk Profile | Strategic Importance |

|---|---|---|---|

| Technology infrastructure | 5-10 years | Medium-High | Critical for competitiveness |

| Processing facility modernisation | 10-20 years | High | Essential for decarbonisation |

| Renewable energy integration | 3-7 years | Medium | Regulatory compliance |

| Supply chain diversification | 7-15 years | High | Geopolitical risk management |

Risk-Adjusted Returns Analysis

Investment decisions increasingly incorporate environmental compliance costs, carbon pricing impacts, and ESG performance metrics. Key analytical frameworks include:

- Carbon pricing scenario modelling across different regulatory environments

- Technology adoption learning curves for emerging extraction and processing methods

- Regulatory change impact assessments for environmental compliance requirements

- Market positioning strategies for sustainable commodity premiums

Market Differentiation Through Low-Carbon Production

Mining companies pursuing differentiation through sustainable production methods can potentially command premium pricing for low-carbon commodities. This strategy requires:

- Transparent emissions measurement and reporting across production processes

- Third-party verification of environmental performance claims

- Long-term offtake agreements with environmentally-conscious buyers

- Technology partnerships for continuous improvement in emissions intensity

Policy Framework Development for Sustainable Mining

Effective policy design must balance environmental objectives with supply security requirements for energy transition materials. However, implementing renewable energy integration across mining operations presents both opportunities and challenges.

Regulatory Mechanism Design

Carbon border adjustment mechanisms represent emerging policy tools for addressing emissions intensity differences across jurisdictions. These mechanisms could significantly impact mining sector competitiveness by:

- Creating cost advantages for low-carbon production methods

- Incentivising technology adoption in high-emissions jurisdictions

- Potentially disrupting established supply chain relationships

- Requiring sophisticated measurement and verification systems

Mining-specific emissions standards face implementation challenges due to:

- Geological variability in ore grades and extraction requirements

- Technology availability constraints for certain commodity types

- Economic impacts on remote communities dependent on mining employment

- International coordination requirements for globally traded commodities

Economic Incentive Optimisation

Tax policy structures can accelerate mining sector decarbonisation through:

- Accelerated depreciation for clean technology investments

- Research and development tax credits for emissions reduction innovation

- Infrastructure investment coordination between public and private sectors

- Trade policy alignment with climate objectives

The next major ASX story will hit our subscribers first

Alignment with Global Climate Targets

The COP28 commitment to triple renewable energy capacity by 2030 creates unprecedented demand for critical minerals whilst requiring simultaneous decarbonisation of extraction and processing operations.

Supply Adequacy Assessment

Meeting renewable energy capacity targets requires coordinated expansion across multiple mineral supply chains:

- Copper supply scaling for electrical infrastructure development

- Lithium production expansion for energy storage systems

- Rare earth element availability for wind turbine and solar panel manufacturing

- Steel production capacity for renewable energy project construction

Current mining sector expansion plans may not align with renewable energy deployment timelines, creating potential supply bottlenecks that could constrain climate target achievement.

Emissions Reduction Pathway Modelling

Multiple decarbonisation scenarios demonstrate different potential outcomes for mining sector emissions:

| Pathway | 2030 Target | 2050 Target | Key Dependencies |

|---|---|---|---|

| Technology adoption | 15% reduction | 45% reduction | EAF/renewable uptake |

| Demand optimisation | 8% reduction | 25% reduction | Circular economy growth |

| Policy intervention | 20% reduction | 60% reduction | Global coordination |

Navigating Investment Opportunities in Sustainable Mining

The convergence of growing demand and decarbonisation requirements creates distinct investment themes across the mining sector value chain.

For Mining Companies

Strategic priorities should emphasise renewable energy integration across all operations, recognising that electricity procurement represents the most immediate opportunity for emissions reduction. Companies must develop comprehensive decarbonisation roadmaps with measurable interim targets that align with broader climate commitments.

Investment in next-generation processing technologies becomes critical for maintaining competitive positioning as environmental standards tighten. Strategic partnerships with technology providers, renewable energy developers, and downstream customers can accelerate transformation whilst distributing risk.

For Financial Investors

ESG performance metrics integration into mining investment decisions reflects both regulatory requirements and market demand for sustainable returns. Investors should evaluate long-term carbon pricing impacts on project economics, recognising that high-emissions operations face increasing cost pressures.

Geographic and commodity diversification strategies help manage concentration risks whilst supporting technology innovation through targeted capital allocation toward companies demonstrating measurable emissions reduction progress.

For Policymakers

Clear regulatory frameworks for sustainable mining must balance environmental protection with supply security objectives for energy transition materials. International cooperation protocols become essential given the global nature of mineral supply chains and the need for coordinated standards.

Incentive structures should facilitate technology adoption whilst avoiding market distortions that could undermine supply chain resilience or create unintended competitive disadvantages for domestic mining operations.

Understanding the Path Forward for Mining Decarbonisation

The ICMM Energy Transition Minerals Report demonstrates that concerns about the climate impact of energy transition mineral extraction may have been overstated relative to the emissions burden of traditional fossil fuel extraction. Non-coal mining's 0.54% contribution to global emissions provides important context for policy discussions about renewable energy infrastructure development.

However, absolute emissions from mining and metals production continue growing at 3% annually, indicating that efficiency improvements have not yet overcome demand growth pressures. The sector's 11% contribution to global emissions, concentrated heavily in steel and aluminium production, represents both a significant decarbonisation challenge and opportunity.

Success in mining sector transformation requires coordinated action across technology development, investment allocation, and policy framework design. The extended timelines for primary mining development, combined with aggressive renewable energy deployment schedules, create structural tensions that demand early action and strategic planning.

In addition, comprehensive analysis from mining industry experts confirms that the mining of critical minerals contributes significantly less to global emissions than previously anticipated, providing important context for future policy development.

Investors should conduct thorough due diligence and consider consulting with financial advisors when making investment decisions in the mining sector. The information presented here is for educational purposes and should not be considered as personalised investment advice. Past performance does not guarantee future results, and all investments carry inherent risks.

Exploring Opportunities in Energy Transition Mining Companies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across energy transition commodities, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage with Discovery Alert.