June 7, 2026

When Chemistry Becomes Strategy: How the ESS and Alsym Sodium-Ion Battery Cells LOI Reframes Stationary Storage

Battery chemistry selection has rarely been considered a strategic differentiator in the energy storage sector. The ESS and Alsym sodium-ion battery cells LOI challenges that assumption directly. For most of the past decade, procurement decisions defaulted to lithium-ion almost as a matter of reflex, with lithium iron phosphate emerging as the dominant chemistry for stationary applications due to its relatively stable cost curve and established supply chains. However, beneath that consensus, a more complicated picture has been forming, shaped by geopolitical risk, thermal safety constraints, and the growing pressure to diversify away from materials concentrated in politically sensitive supply regions.

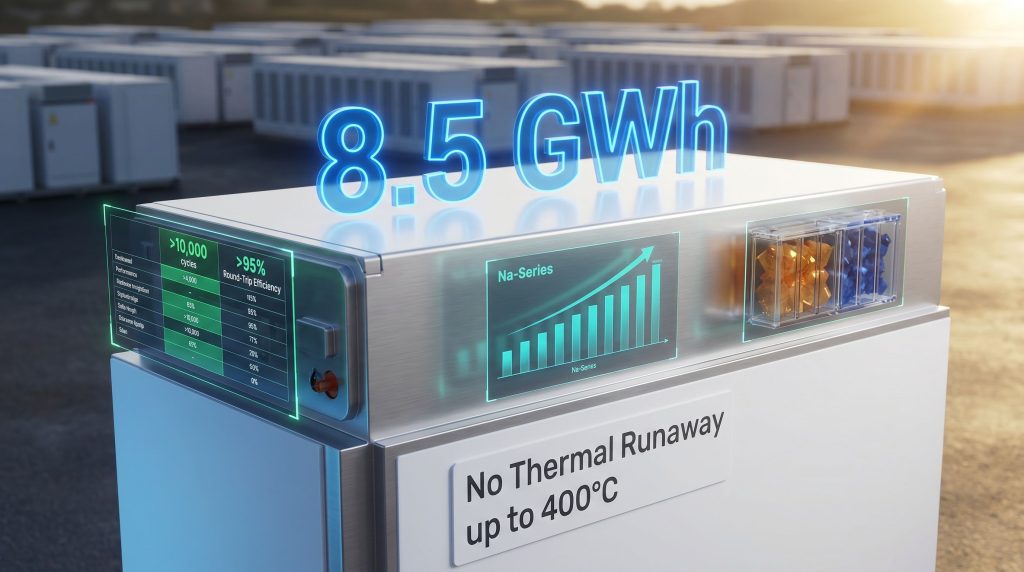

That structural tension has now produced one of the more consequential procurement signals in the US stationary storage market this year. ESS Tech (NYSE: GWH) has signed a letter of intent with Alsym Energy to procure 8.5 GWh of sodium-ion battery cells and modules, reported by Renewables Now on April 30, 2026. The scale of this preliminary agreement positions it as one of the larger publicly announced sodium-ion procurement commitments in the US market to date, and its strategic implications extend well beyond a single supply transaction.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Readers should conduct their own due diligence before making investment decisions. Forward-looking statements and performance projections involve inherent uncertainty and may not materialise as described.

When big ASX news breaks, our subscribers know first

Why Lithium-Ion's Dominance in Stationary Storage Is Under Structural Pressure

Lithium-ion technology, particularly LFP chemistry, has delivered impressive cost reductions over the past decade. Yet its dominance in stationary storage now faces compounding headwinds that go beyond price competition. Furthermore, the battery raw materials landscape is shifting in ways that make alternative chemistries increasingly attractive.

The first pressure point is thermal safety infrastructure. Lithium-ion battery installations, including those using LFP chemistry, carry thermal runaway risk that necessitates significant balance-of-plant investment. Fire suppression systems, dedicated HVAC thermal management, setback requirements, and specialised permitting add capital and complexity to every project. In dense urban environments and high-value industrial zones, these requirements have historically excluded battery storage from locations where it would otherwise be most economically valuable.

The second pressure is supply chain concentration. The minerals underpinning lithium-ion chemistries, including lithium, cobalt, nickel, and manganese, are geographically concentrated in a relatively small number of countries. In some cases, these are processed predominantly by entities classified under US Foreign Entity of Concern (FEOC) restrictions. For US-based developers operating under domestic content requirements and navigating clean energy incentive frameworks, FEOC exposure creates both regulatory risk and financing complexity.

The third pressure is duration diversity. Grid operators and large commercial energy buyers are increasingly recognising that no single chemistry optimally serves every storage duration segment. Short-duration frequency response, medium-duration peak shaving, and long-duration renewable firming each carry different performance requirements. Procurement strategies that lock developers into a single chemistry constrain their ability to serve the full spectrum of customer needs.

These three pressures collectively create the market conditions in which alternative chemistries, and sodium-ion specifically, can move from experimental validation to commercial-scale deployment. Indeed, the critical minerals demand outlook reinforces why supply chain diversification is becoming a strategic imperative rather than a peripheral concern.

Where Sodium-Ion Technology Sits Within the Evolving Storage Hierarchy

Sodium-ion chemistry has been studied academically for decades, but practical commercialisation has accelerated meaningfully only in the past several years. The fundamental electrochemical mechanism is similar to lithium-ion, with sodium ions moving between anode and cathode during charge and discharge cycles. The critical differences emerge in the materials used and the physical properties of sodium as an element.

Sodium is the sixth most abundant element in the Earth's crust, is geographically distributed across virtually every major nation, and does not share the FEOC-linked supply chain risks associated with lithium, cobalt, or nickel. This material abundance directly translates into a structurally advantaged supply chain for US-based manufacturers and project developers. Consequently, advances in lithium extraction technology are no longer the only avenue developers are exploring to improve supply chain resilience.

Beyond supply chain resilience, sodium-ion chemistry carries inherent electrochemical properties that confer meaningful safety advantages. The lower energy density of sodium-ion cells relative to high-nickel lithium-ion is often cited as a limitation, but for stationary storage applications where weight and volume constraints are far less critical than for electric vehicles, this trade-off is commercially irrelevant. What matters in stationary storage is cycle life, round-trip efficiency, depth of discharge usability, total cost of ownership, and safety at the system level.

Comparing sodium-ion against LFP across these stationary-relevant metrics reveals a more competitive picture than the headline energy density comparison suggests:

| Performance Metric | Lithium-Ion (LFP) | Sodium-Ion (Na-Series, Alsym) |

|---|---|---|

| Thermal Runaway Risk | Moderate | Eliminated (tested to 400°C) |

| Cycle Life | ~4,000 to 6,000 cycles | Over 10,000 cycles |

| Round-Trip Efficiency | ~92 to 95% | Over 95% |

| FEOC Material Exposure | High | Low (abundant sodium base) |

| Fire Suppression Required | Yes | No |

| Full Depth of Discharge | No (typically 80 to 90% usable) | Yes (100% usable) |

| Operating Temperature Flexibility | Limited | Wide range |

The combination of superior cycle life and full depth of discharge usability is particularly significant. A battery system that can use 100% of its rated capacity across more than 10,000 cycles delivers substantially more cumulative energy throughput over its operational life than an LFP system constrained to 80 to 90% usable depth over fewer cycles. From a project finance perspective, that difference compounds meaningfully across a 20-year asset life.

The Technical Architecture Behind Alsym's Na-Series Chemistry

Alsym's sodium-ion formulation is built around a cathode chemistry designated NFPP+, which stands for sodium iron phosphate pyrophosphate. This specific molecular architecture was developed using physics-informed AI, a methodology that integrates fundamental electrochemical physics into machine learning models to accelerate material optimisation.

Traditional battery material development relies on iterative laboratory synthesis and testing, a process that can span years for each marginal improvement. Physics-informed AI compresses this timeline by predicting electrochemical behaviour before physical synthesis, enabling researchers to eliminate underperforming candidate materials computationally rather than through costly and time-consuming physical experimentation. This approach positions Alsym's R&D pipeline to iterate faster than organisations relying solely on conventional laboratory methods.

The resulting Na-Series cell specifications, as outlined in Alsym's technical positioning, include:

| Technical Specification | Na-Series Performance |

|---|---|

| Gravimetric Energy Density | 135 Wh/kg |

| Volumetric Energy Density | 250 Wh/L |

| Cycle Life | Over 10,000 cycles (~20-year operational life) |

| Round-Trip Efficiency | Over 95% |

| Charge Rate | 2C |

| Discharge Rate | 4C |

| Usable Depth of Discharge | 100% |

| Thermal Runaway Threshold | No thermal runaway up to 400°C (ARC tested) |

| Nail Penetration Safety | Passes without fire or rupture |

The 4C discharge rate capability deserves particular attention. For stationary storage applications that require rapid power delivery, such as frequency response, demand charge management, or commercial peak shaving, the ability to discharge at four times the rated capacity in 15 minutes provides performance headroom that many competing chemistries cannot match at equivalent safety profiles.

The ARC (Accelerated Rate Calorimetry) thermal runaway testing result is perhaps the most commercially significant specification. ARC testing is a standardised method for identifying the onset temperature of self-heating and thermal propagation in battery cells. A result confirming no thermal runaway up to 400 degrees Celsius means that even under extreme external heating conditions that would be catastrophic for lithium-based chemistries, the Na-Series cell does not enter an uncontrolled exothermic reaction. This fundamentally changes the risk profile for project permitting, insurance underwriting, and urban deployment approvals.

What the Safety Profile Actually Means for Project Economics

The elimination of thermal runaway risk is not merely a safety compliance achievement. It carries direct financial consequences for project developers:

- Fire suppression systems for lithium-ion battery installations typically represent a meaningful capital line item, with costs varying by jurisdiction, system size, and local fire code requirements

- Active HVAC thermal management infrastructure adds both capital expenditure and ongoing operational costs across the asset life

- Jurisdictions with strict fire safety codes or proximity restrictions for lithium-ion installations create additional permitting complexity and potential site exclusions

- Insurance underwriting for battery storage assets increasingly reflects thermal safety performance in premium calculations

Each of these cost categories is reduced or eliminated for sodium-ion installations that pass ARC testing at 400 degrees Celsius. For projects in urban cores, commercial districts, or proximity to occupied buildings, the permitting pathway itself may be materially simplified, reducing both timeline and legal cost.

Manufacturing Scalability: The Underappreciated Competitive Advantage

One of the most strategically important and least widely understood aspects of Alsym's position is its manufacturing compatibility with existing lithium-ion production infrastructure. Battery gigafactory construction typically requires billions of dollars in capital investment and multi-year construction timelines. Greenfield sodium-ion manufacturers face the same infrastructure burden as lithium-ion entrants, which has historically been a barrier to rapid commercialisation.

Alsym's NFPP+ chemistry is designed to be produced on manufacturing equipment architecturally compatible with existing lithium-ion production lines. This compatibility means that contract manufacturing partners, repurposed capacity from existing gigafactories, or brownfield manufacturing investments can be leveraged to scale sodium-ion production without the full greenfield capital burden. The speed-to-market and capital efficiency implications of this are substantial.

Alsym's production roadmap proceeds through two key milestones:

- H1 2026: Initial cell and module shipments from the pilot manufacturing facility in Massachusetts, including 1 kWh module configurations suitable for demonstration and early commercial deployment

- 2027: Transition to high-volume production, leveraging manufacturing compatibility to scale capacity without greenfield capital requirements

This timeline aligns directly with the delivery expectations embedded in the ESS and Alsym sodium-ion battery cells LOI. The pilot phase provides ESS with early product validation and the opportunity to integrate Na-Series modules into system designs before full-volume commercial deployments begin in 2027.

What the ESS–Alsym Letter of Intent Actually Signals About Market Direction

ESS Tech built its commercial identity around long-duration iron flow battery technology, a chemistry occupying the multi-hour storage segment that lithium-ion cannot serve economically. The decision to pursue a letter of intent with Alsym for 8.5 GWh of sodium-ion cells targeting commercial, industrial, and utility-scale short- and medium-duration applications represents a fundamental strategic repositioning.

Rather than competing exclusively in the long-duration niche, ESS is constructing a multi-chemistry platform capable of addressing the full duration spectrum from sub-hour to multi-day storage. This transition from single-chemistry specialist to full-service stationary storage platform has significant implications:

| Business Model Dimension | Single Chemistry Specialist | Multi-Chemistry Platform |

|---|---|---|

| Market Addressability | Narrow (duration-specific) | Broad (short to long duration) |

| Customer Relationship Depth | Transactional | Strategic partnership |

| Revenue Diversification | Limited | High |

| Supply Chain Complexity | Lower | Moderate |

| Competitive Moat | Technology-specific | Platform and integration capability |

| Project Finance Appeal | Niche | Broad |

The multi-chemistry platform model is increasingly relevant as large commercial and industrial energy buyers seek single-vendor relationships that can address multiple storage requirements within a unified commercial framework. A storage developer capable of offering both long-duration iron flow and short-to-medium-duration sodium-ion under one contract is positioned to capture more of each customer's total storage spend than a single-chemistry provider can access.

It is worth noting that a letter of intent is a non-binding preliminary agreement. Progression to a binding supply contract represents a subsequent and distinct commercial milestone. Investors and project developers should treat this announcement as a signal of strategic intent rather than a confirmed commercial commitment.

The next major ASX story will hit our subscribers first

Supply Chain Sovereignty and the FEOC Calculus for US Developers

A dimension of this partnership that deserves more attention than it typically receives in deal coverage is the FEOC supply chain positioning. US-based storage developers are operating in an environment where domestic content requirements and FEOC restrictions shape not only regulatory compliance but project financing eligibility and, in some frameworks, incentive qualification.

Sodium as a base material does not face the same sourcing constraints as lithium, cobalt, or nickel. Its geographic distribution means that domestic or allied-nation supply chains are structurally accessible in ways that lithium-ion critical mineral supply chains currently are not. For developers seeking to maximise incentive eligibility under domestic clean energy frameworks, a FEOC-free sodium-ion supply chain offers a structurally differentiated procurement pathway.

This consideration is particularly salient given broader supply chain restructuring trends. Advances in Chinese battery recycling and the disposition of Chinese-owned manufacturing assets in the United States reflect the active restructuring of clean energy supply chains in response to domestic content and FEOC frameworks. Furthermore, sodium-ion chemistries built around abundant, geographically distributed materials are structurally better positioned to navigate this environment than lithium-based alternatives dependent on concentrated, FEOC-exposed supply chains.

The evolving battery supply chain alliances forming across the Indo-Pacific region further underscore why supply chain diversification is accelerating. However, for US developers, a domestically accessible sodium-ion supply chain may ultimately prove more strategically durable than any offshore partnership arrangement.

Frequently Asked Questions: ESS and Alsym Sodium-Ion Battery Cells LOI

What is the total procurement volume covered under the ESS–Alsym LOI?

The letter of intent covers 8.5 GWh of sodium-ion battery cells and modules, making it one of the more significant publicly announced sodium-ion procurement commitments in the US stationary storage market to date.

What applications are targeted for the Na-Series cells within ESS's product portfolio?

The cells are intended for stationary energy storage applications across commercial, industrial, and utility-scale project categories, with particular focus on short- and medium-duration storage segments that complement ESS's existing long-duration iron flow capabilities.

When will Alsym begin delivering cells and modules?

Alsym has targeted the first half of 2026 for initial cell and module shipments from its Massachusetts pilot facility, with high-volume production capacity expected to come online during 2027.

Why does the elimination of thermal runaway risk matter for project developers?

Projects deploying sodium-ion cells that pass ARC thermal testing can avoid the capital cost of fire suppression infrastructure and active HVAC thermal management, while also simplifying permitting in jurisdictions where fire safety codes create significant barriers for lithium-ion installations. The cumulative effect is a lower total cost of ownership and reduced permitting complexity.

Is the LOI a binding supply commitment?

No. A letter of intent establishes commercial intent and preliminary terms but does not create binding supply obligations. A subsequent binding supply agreement would represent the next commercial milestone for both parties.

How does sodium-ion compare to LFP for grid-scale storage?

Across the metrics most relevant to stationary storage, sodium-ion's Na-Series chemistry demonstrates competitive or superior performance versus LFP, including longer cycle life, eliminated thermal runaway risk, full depth of discharge usability, and FEOC-free supply chain positioning. The one area where LFP retains an advantage is energy density per kilogram, though this is a secondary consideration in stationary applications where weight constraints are minimal.

Key Takeaways for Storage Developers, Project Financiers, and Industry Observers

The ESS and Alsym sodium-ion battery cells LOI does more than announce a procurement intention. It provides a window into how the competitive logic of stationary storage is evolving at the platform level. Several conclusions are worth drawing:

- 8.5 GWh at the LOI stage signals that sodium-ion is transitioning from proof-of-concept to commercial procurement scale in the US market, a threshold that materially changes how technology risk is assessed by project financiers and insurers

- The ESS strategic pivot toward multi-chemistry platforms reflects a broader market shift away from single-technology storage providers toward integrated platforms capable of serving the full duration spectrum

- Alsym's NFPP+ chemistry addresses the three most persistent barriers to sodium-ion adoption simultaneously: energy density competitiveness for stationary applications, demonstrable safety performance, and manufacturing scalability via LFP-compatible production infrastructure

- The intersection of FEOC supply chain requirements and domestic content frameworks creates a structural procurement advantage for sodium-ion technologies built on geographically abundant materials

- For project financiers, the combination of ARC-tested thermal safety, extended cycle life, and full depth of discharge usability represents a risk-adjusted value proposition that warrants rigorous evaluation against LFP alternatives in project modelling

The broader storage market context reinforces why this moment matters. The US Energy Information Administration has forecast solar, wind, and battery storage additions exceeding 80 GW in the year ahead. Against that deployment backdrop, the chemistry diversity and supply chain resilience questions raised by this partnership are not peripheral considerations. They are central to how the industry navigates the next phase of growth at scale.

For further coverage of the evolving US battery energy storage landscape and sodium-ion technology developments, Energy Storage News provides ongoing reporting on global storage deals, project announcements, and technology trends across the sector.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

The rapidly evolving energy storage sector is driving unprecedented demand for critical minerals, and Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant mineral discoveries are announced — turning complex data across 30+ commodities into clear, actionable opportunities for both traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the market.