June 21, 2026

The Architecture of Ambition: Why EU Critical Minerals Policy Has a Price Problem

The history of commodity markets is littered with policy frameworks that solved the wrong problem. Governments have repeatedly invested in supply diversification, infrastructure development, and permitting reform, only to watch strategically important industries collapse when prices moved against them. The EU's current approach to critical minerals carries echoes of that pattern, and nowhere is the tension more visible than in the growing debate over EU critical minerals policy and lithium price floor mechanisms.

The European Union has made significant structural progress in recent years. However, the question confronting policymakers, producers, and investors alike is whether structural reform without price protection can ever deliver genuine supply security, or whether it simply relocates the vulnerability from one part of the supply chain to another.

When big ASX news breaks, our subscribers know first

From Trade Dependency to Strategic Legislation: How Europe Got Here

For decades, Europe's approach to mineral processing was essentially an outsourcing model. The logic was straightforward: let lower-cost jurisdictions handle extraction and refining, then purchase the output on open markets. That model generated efficiency gains but accumulated structural fragility at scale.

The acceleration of EV adoption across Europe, combined with a wave of gigafactory announcements from manufacturers including Northvolt, CATL, and ACC, transformed what had been a theoretical supply chain risk into an acute operational challenge. Battery-grade lithium, refined rare earth oxides, and permanent magnets were suddenly materials that European industry needed in volume, on a predictable basis, over decadal timeframes.

China's dominance across these value chains was not simply a matter of market share. It reflected decades of deliberate industrial policy investment in refining capacity, processing technology, and vertical integration that Western economies had not matched. By the time European policymakers recognised the full extent of the exposure, China controlled an estimated 80–90% of global rare earth processing capacity and held commanding positions across lithium refining and battery precursor manufacturing.

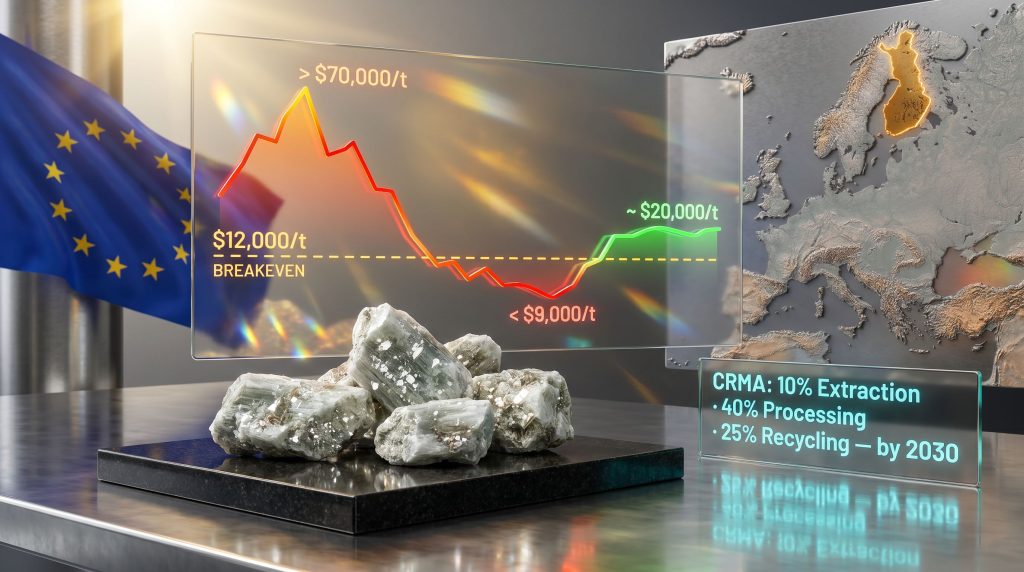

The EU's legislative response, the Critical Raw Materials Act (CRMA) adopted in 2024, represents the most ambitious European attempt to rebalance this structural dependency. Its targets are specific and binding:

- 10% of annual EU consumption to be met through domestic extraction by 2030

- 40% of annual consumption to be processed within EU borders by 2030

- 25% of annual consumption to be sourced from recycled materials by 2030

- Streamlined permitting pathways through a Strategic Projects designation process

- New joint procurement frameworks and coordinated stockpiling mechanisms

- A ReSourceEU funding architecture designed to catalyse public-private investment in critical mineral value chains

These are meaningful commitments. However, they address supply chain architecture, not supply chain economics. That distinction matters enormously for the companies being asked to deliver the infrastructure.

The Investor Calculus: What Producers Are Actually Asking For

Understanding why EU critical minerals policy and lithium price floor advocacy have become inseparable requires stepping inside the investment model of a hard-rock lithium mine. These are not short-cycle assets. A major lithium operation typically requires five to ten years from discovery to production, involves capital expenditure that may run into billions, and needs to generate returns over a twenty to thirty year asset life to justify the investment.

Permitting reform shortens the development timeline at the front end. Financing coordination reduces the cost of capital. But neither instrument addresses the central risk: that prices may be driven below breakeven at any point during that thirty-year window, not by genuine market oversupply, but by deliberate capacity deployment from a geopolitically motivated competitor.

Furthermore, Europe's critical minerals supply chain faces compounding vulnerabilities when price instability is combined with structural dependency. The table below summarises how the CRMA's tools map against what producers are actually requesting:

| Policy Tool | EU CRMA Approach | Producer Requirements |

|---|---|---|

| Permitting reform | Streamlined via Strategic Projects | Addressed |

| Financing access | ReSourceEU, public-private coordination | Partially addressed |

| Off-take agreements | Encouraged but not mandated | Voluntary only |

| Price floor mechanism | Not currently included | Absent |

| Stockpiling coordination | New framework established | Addressed |

| Supplier concentration limits | 60% cap on single non-G7 supplier by 2030 | Addressed at supply level |

The gap in the middle of that table is where the policy debate is currently concentrated.

The Lithium Price Collapse: A Geopolitical Event, Not a Market Correction

To understand why European producers are pushing so hard for a lithium price floor, it is essential to understand what happened to lithium prices between 2022 and 2024. This was not a conventional commodity cycle.

Lithium carbonate equivalent prices peaked at above $70,000 per tonne in late 2022, driven by a combination of surging EV demand, constrained spodumene supply from Australian hard-rock operations, and speculative positioning. The price signal was so strong that it triggered a global wave of project development and expansion announcements.

Then prices collapsed. By late 2023 and into 2024, spot prices had fallen to below $9,000 per tonne, a decline exceeding 87% from peak. Many analysts attribute this collapse not to organic demand destruction but to a deliberate Chinese overcapacity strategy, with Chinese producers expanding output at a pace that overwhelmed the lithium carbonate market and forced prices below the breakeven costs of non-Chinese competitors.

This matters because it reveals a critical asymmetry in how lithium market disruptions function. A Chinese producer operating with state backing and lower cost structures can sustain production below $9,000 per tonne for extended periods. An Australian spodumene operation or a European lithium hydroxide refinery typically cannot. The price suppression therefore functions as a selective culling mechanism, removing Western producers from the supply landscape while preserving Chinese market share for the eventual demand recovery.

Analysts broadly agree that the 2023–2024 lithium price event was not a standard market correction driven by demand weakness. It reflected a structural pricing dynamic in which production capacity was deployed in a manner inconsistent with normal commercial logic, with effects concentrated among non-Chinese producers.

Prices have since recovered to approximately $20,000 per tonne as of mid-2026. That partial recovery has restored viability to some operations. However, the memory of the collapse, and the recognition that it could be repeated, is shaping every investment decision in the sector.

Keliber: The Real-World Test Case for EU Supply Chain Policy

No project illustrates the stakes of the EU critical minerals policy and lithium price floor debate more concretely than the Keliber lithium operation in Finland. Commissioned in April 2026 at a capital investment value of approximately R18 billion, Keliber represents exactly the kind of domestic European critical mineral asset the CRMA was designed to incentivise.

The mine is designed to supply battery-grade lithium hydroxide directly to European EV battery manufacturers, closing the loop on a supply chain that currently requires European manufacturers to source refined lithium from Asian processors. It is, in the language of the CRMA, a Strategic Project delivering domestic processing capacity.

But as of mid-2026, Keliber is producing spodumene concentrate rather than refined lithium hydroxide. The progression to downstream refinery operations — which is where the strategic value of the project is ultimately realised — depends on price conditions sufficient to justify activating that additional processing infrastructure.

With a breakeven cost of approximately $12,000 per tonne and current prices around $20,000 per tonne, the project's economics are supportive. According to Sibanye-Stillwater CEO Richard Stewart, at current prices the refinery would generate good returns based on the company's internal studies (as reported by MiningMX, June 2026). The operative concern is not present-day pricing but the risk of a second Chinese-driven price suppression cycle that forces prices back below the breakeven threshold.

Stewart's position, as reported by MiningMX, is that the EU cannot ask producers to make irreversible capital commitments in service of European supply security and then leave those producers to absorb the full financial consequences of geopolitically-driven price manipulation. The asymmetry of that arrangement — where the EU gains supply security while producers bear commodity risk — is precisely what a price floor mechanism would address.

The Spodumene-to-Hydroxide Transition: Why It Matters

There is a technical dimension to this debate that is often overlooked. Spodumene concentrate, which is what Keliber is currently producing, is an intermediate product. It requires further processing through either a sulphate or hydroxide conversion route to produce battery-grade lithium compounds.

The decision to activate that downstream processing capacity is economically sensitive. Lithium hydroxide refineries are capital-intensive, energy-intensive, and operationally complex. In addition, a producer operating a refinery at prices close to breakeven is not generating the returns required to service the debt on that infrastructure or to justify the next round of capital expenditure. This is why price certainty matters not just at the mine level but across the entire value chain, including through direct lithium extraction technologies that are emerging as complementary processing pathways.

What a Price Floor Would Actually Look Like in Practice

The EU critical minerals policy debate has sometimes treated the price floor concept as a binary question. In practice, price stabilisation mechanisms can take several forms, each with different implications for market function, public expenditure, and trade law:

- Hard regulatory floors: Legally binding minimum prices enforced through domestic trade law or procurement regulation. Administratively straightforward but potentially incompatible with WTO frameworks.

- Contractual floors: Embedded within government-backed off-take agreements or strategic procurement contracts. Commercially flexible but dependent on government willingness to enter long-term supply contracts at above-market prices during suppression events.

- Trigger-based support mechanisms: Government intervention activated when spot prices fall below a predefined threshold, providing top-up payments to qualifying domestic producers. Fiscally targeted and time-limited, but requires robust monitoring and enforcement infrastructure.

The US approach under recent industrial policy frameworks leans toward contractual and trigger-based mechanisms, embedding price support within the procurement architecture of defence and energy agencies rather than as standalone commodity regulation. The US and EU approaches to critical minerals diverge significantly here, with the EU having historically resisted this model, partly on philosophical grounds around market intervention and partly due to concerns about WTO compliance.

However, the logic of the G7 framework agreed at the June 2026 summit in France creates a potential multilateral pathway. If G7 members align their stockpiling strategies, share supply monitoring data through the new IEA-backed platform, and coordinate procurement policies, the effective floor for allied-nation producers could emerge from collective buying behaviour rather than individual regulatory mandates.

The next major ASX story will hit our subscribers first

G7 Alignment: The Scaffolding for a Multilateral Price Mechanism

The June 2026 G7 summit produced critical minerals commitments that, while not explicitly including price floors, create institutional infrastructure that could support them over time. The key outcomes included:

- Coordination of national stockpiling strategies across G7 member states

- Launch of a new mineral supply monitoring platform backed by the International Energy Agency

- Agreement to reduce dependence on any single non-G7 supplier for rare earths and permanent magnets to below 60% by 2030, with a longer-term target of 50%

The concentration limit is particularly significant. A commitment to source no more than 60% of rare earth and permanent magnet supply from any single non-G7 nation is, in practical terms, a commitment to pay a premium for allied-nation supply. That implicit price premium, if formalised through procurement contracts, is functionally equivalent to a soft price floor.

What the G7 framework does not yet contain is an explicit mechanism for translating stockpiling coordination into price signals that reach individual producers. That gap between institutional architecture and commercial reality is where the policy work remains incomplete.

The Growing Alignment Among European Mining Companies

One development that may accelerate the regulatory timeline is the increasing cohesion among European mining companies around the price floor argument. Sibanye-Stillwater's CEO Richard Stewart noted in a June 2026 interview with MiningMX that there has been real movement in terms of alignment among mining companies operating in Europe, with the industry shifting from fragmented engagement with EU institutions toward coordinated advocacy on shared policy positions.

This matters because the EU's legislative process is responsive to organised industry representation, particularly where that representation aligns with strategic policy objectives. A fragmented mining sector making disparate arguments about different minerals and different cost structures is relatively easy for policymakers to defer. A unified industry coalition making a single coherent argument about price stabilisation is considerably harder to ignore.

Furthermore, the battery raw materials market dynamics reinforce the urgency of this advocacy, as downstream manufacturers increasingly seek long-term supply certainty that current volatile pricing cannot provide. Stewart also noted that EU policymakers have demonstrated genuine receptiveness to the underlying argument, with progress achieved in communicating the nature of the problem.

The translation of that receptiveness into binding regulation, however, remains a work in progress. In his assessment, there is still a meaningful distance to travel before hard regulation emerges from the EU legislative process.

Scenario Analysis: Three Price Pathways and Their Consequences

Understanding the stakes of the EU critical minerals policy and lithium price floor debate requires mapping outcomes across plausible price scenarios:

| Scenario | Lithium Price Path | EU Policy Response | European Project Outcome |

|---|---|---|---|

| Baseline stability | Stabilises at $18,000–22,000/t | CRMA implemented, no floor | Projects viable but exposed to downside |

| Adverse suppression | China drives prices below $10,000/t again | No floor mechanism in place | European producers curtail or exit market |

| Supported floor | Floor set at $12,000–15,000/t | Trigger mechanism activated | European supply chain maintained through cycle |

The adverse scenario is not a theoretical extreme. It is a replication of conditions observed in 2023–2024. In that scenario, the entire investment thesis behind European critical mineral development — including the Keliber project, Finnish processing infrastructure, and the broader CRMA architecture — is rendered commercially unsustainable regardless of how well the structural policy has been designed.

FAQ: EU Critical Minerals Policy and the Lithium Price Floor

What is the Critical Raw Materials Act?

The CRMA is EU legislation adopted in 2024 establishing binding targets for domestic extraction (10%), processing (40%), and recycling (25%) of critical minerals by 2030. It also creates the Strategic Projects designation, streamlined permitting, and joint procurement frameworks designed to reduce dependence on non-EU sources. Establishing a critical raw materials facility within the EU is central to these ambitions.

Does the EU currently have a lithium price floor mechanism?

No. As of mid-2026, no explicit price floor exists within EU critical minerals policy. The CRMA relies primarily on financing tools, supply diversification, and off-take encouragement rather than direct price stabilisation.

Why are producers pushing for a floor rather than other forms of support?

Mining projects require price certainty over investment horizons of twenty to thirty years. Permitting reform and financing support address development-phase risks but do not protect against geopolitically-motivated price suppression during the operational phase — which is when capital commitments are already locked in and irreversible.

How does the US approach differ from Europe's?

The United States has moved more explicitly toward price stabilisation frameworks embedded within defence and energy procurement architecture. The EU has historically preferred market-compatible financing and diversification tools, though industry observers note that EU policymakers are closely monitoring US policy developments, including recent critical minerals price floor announcements that have reshaped the competitive landscape.

What is the breakeven cost for projects like Keliber?

The Keliber project in Finland has a reported breakeven cost of approximately $12,000 per tonne of lithium. With current prices around $20,000 per tonne, the project is economically viable, but it remains exposed to renewed price suppression below that threshold.

The Road Ahead: Three Conditions That Would Accelerate EU Action

The trajectory of EU critical minerals policy and lithium price floor adoption will depend heavily on external catalysts. Three conditions would most likely accelerate movement from political receptiveness to binding regulation:

- A second major lithium price suppression event driven by Chinese overcapacity, demonstrating conclusively that market forces cannot sustain European production without price protection

- US price floor implementation that creates a competitive asymmetry, putting EU-based producers at a structural disadvantage relative to their US counterparts competing for allied-nation procurement contracts

- Failure of voluntary off-take frameworks to attract sufficient private capital into European critical mineral development, creating visible gaps in the CRMA's capacity to meet its 2030 benchmarks

Europe's critical minerals policy has built the right architecture. The CRMA addresses supply chain structure in a sophisticated and comprehensive way. What it has not yet resolved is the price dynamics question, which determines whether that architecture can be populated with commercially viable projects. A lithium price floor is not a subsidy request. It is a proposal to share the financial risk of the supply security the EU is asking producers to deliver.

The institutional momentum from the G7 framework, combined with growing industry cohesion and increasing EU awareness of the US policy trajectory, suggests the conditions for regulatory movement are gradually assembling. Consequently, whether that movement arrives before the next price suppression cycle tests Europe's supply chain resilience remains the critical unanswered question.

Disclaimer: This article contains forward-looking analysis, scenario projections, and references to market forecasts. These elements involve uncertainty and should not be interpreted as investment advice. Readers should conduct independent research and consult qualified financial advisors before making investment decisions in the mining or critical minerals sector. Price projections and breakeven figures referenced are sourced from publicly available industry reporting and are subject to revision.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, cutting through the complexity of over 30 commodities to surface actionable opportunities for both traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.