June 25, 2026

Europe's Energy Supply Is Facing a Regulatory Reckoning

Across global commodity markets, the most consequential disruptions rarely announce themselves clearly in advance. They accumulate quietly through regulatory timelines, procurement cycles, and contractual constraints until the window for orderly adjustment has already closed. That is precisely the dynamic now unfolding across Europe's energy import framework, where EU methane regulations and Europe's oil and gas supply are on a direct collision course — driven by a legally binding methane regulation moving toward enforcement dates that a significant majority of the world's energy exporters cannot meet.

The scale of potential disruption is not a matter of speculation. Independent industry analysis cited in a formal diplomatic communication sent on June 24, 2026 indicates that nearly all EU crude oil imports and a substantial proportion of EU natural gas imports will be non-compliant with the EU Methane Regulation beginning in January 2027. Understanding why requires examining how the regulation actually works, what it demands, and why its current design creates structural tensions that discretionary non-enforcement cannot resolve.

When big ASX news breaks, our subscribers know first

What the EU Methane Regulation Actually Does

Regulation EU 2024/1787 entered into force in August 2024 as part of the EU's broader effort to reduce methane emissions across the energy sector. The regulation operates on two distinct levels. Domestically, it imposes methane monitoring, reporting, and verification (MRV) obligations on European energy producers. For third-country suppliers, it requires that importers demonstrate their overseas sources meet standards equivalent to EU domestic requirements.

This equivalence framework is the regulation's most consequential and contested element. It does not simply ask exporters to reduce emissions. It requires them to demonstrate compliance through a specific MRV architecture that matches EU standards in methodology, data quality, and reporting frequency. Furthermore, for many exporting nations, this infrastructure does not yet exist at the scale or precision the regulation demands. The EU's official guidance on methane emissions outlines the full scope of these requirements in detail.

Understanding Methane Intensity: The Metric That Defines Market Access

Methane intensity refers to the volume of methane emitted per unit of energy produced or transported. It is a ratio, not an absolute figure, which means a large-volume producer can still achieve a low methane intensity if its leak detection and emission control systems are sufficiently advanced.

This distinction matters enormously for market access. The EUMR's post-2030 framework does not simply cap total methane emissions from imported energy. It imposes maximum methane intensity values, meaning that exporters must demonstrate their emissions per unit of output fall below a defined threshold. Consequently, suppliers that cannot verify this figure through EU-equivalent MRV systems face effective exclusion from the European market, regardless of their long-standing commercial relationships or the volume of energy they supply.

The EUMR does not simply regulate emissions. It restructures market access itself. Exporters unable to demonstrate MRV equivalence face effective exclusion from the EU market, irrespective of their energy relationship with Europe.

The EUMR Compliance Timeline: Phase by Phase

The regulation's obligations do not arrive as a single deadline. They are structured as a phased escalation across six years, each stage adding new requirements that build toward full enforcement.

| Compliance Phase | Effective Date | Core Requirement |

|---|---|---|

| Contract Clause Insertion | August 4, 2024 | New and renewed supply contracts must include third-country MRV obligations |

| Annual Supplier Reporting | May 5, 2025 | Importers begin reporting on supplier methane monitoring data |

| MRV Equivalence Threshold | January 1, 2027 | All new gas import contracts require EU-equivalent MRV standards |

| Methane Intensity Reporting | August 5, 2028 | Annual reporting on emissions per unit of gas commences |

| Maximum Intensity Cap | August 5, 2030 | Imports exceeding maximum methane intensity values face significant financial penalties |

Why January 2027 Is the Critical Threshold

The January 2027 date is not simply the next milestone on a gradual timeline. It is the point at which new natural gas import contracts must demonstrate full MRV equivalence, creating an immediate and binding compliance obligation for procurement decisions being made right now.

Energy markets do not operate on a just-in-time basis. Import contracts for 2027 delivery volumes are already being negotiated and structured. Procurement cycles for LNG cargoes, pipeline gas allocations, and crude oil supply agreements typically run twelve to eighteen months ahead of delivery. This means the January 2027 deadline is not a distant regulatory horizon. For energy traders and procurement teams, it is already present tense.

The four-nation diplomatic letter sent on June 24, 2026 made this point explicitly, noting that importers had already commenced purchasing oil and natural gas destined for 2027 delivery storage, and that as of that date no viable compliance pathway existed.

Penalties, Energy Security, and an Unresolved Legal Tension

Member states are empowered under the EUMR to impose penalties of up to 20% of a company's annual turnover for non-compliance. For major energy importers operating at scale, this creates exposure measured in billions of euros per entity.

The regulation simultaneously includes provisions stating that energy security must not be endangered by its enforcement. This creates a structural paradox. If the majority of EU energy imports are non-compliant, full enforcement would trigger precisely the energy security crisis the regulation is designed to operate alongside safely. However, the energy security provisions are safeguards, not exemptions. They do not automatically suspend compliance obligations or create legal certainty for importers and exporters entering multi-year contracts.

The European Commission is reportedly preparing non-binding guidelines that would recommend against penalising non-compliant imports during a transitional period. However, as the joint letter from the four energy ministers clearly articulates, non-binding guidance does not override binding legal obligations under EU law. Counterparties to contracts valued in the tens of billions of euros cannot structure commercial agreements around the assumption of discretionary non-enforcement.

A regulation that contains energy security safeguards but relies on discretionary non-enforcement to operationalise them is not a functioning compliance framework. It is a deferred crisis.

How Much of Europe's Energy Supply Is Actually Exposed?

The non-compliance exposure identified in independent industry analysis is striking in its scope.

| Energy Sector | At-Risk Import Volume | Share of Total EU Imports |

|---|---|---|

| Natural Gas | ~114 billion cubic metres | ~43% of EU gas imports |

| Crude Oil | ~9.8 million barrels per day | ~87% of EU crude oil imports |

Based on 2024 import volumes and independent industry analysis referenced in the June 2026 joint ministerial letter

The crude oil figure is particularly significant. An 87% non-compliance exposure does not reflect widespread producer unwillingness to reduce methane emissions. It reflects the structural reality that upstream measurement infrastructure capable of satisfying EU MRV equivalence requirements does not currently exist across the majority of global producing regions.

For natural gas, LNG supply chains present particular verification challenges. Methane emissions occur across multiple stages including wellhead production, processing, liquefaction, shipping, and regasification. Attributing and measuring emissions across this chain with the precision EU MRV equivalence requires is technically demanding even for well-resourced producers. In addition, for suppliers in developing-economy contexts, the timeline is simply not achievable without substantial infrastructure investment that cannot be completed before January 2027. This is a central concern examined by analysts reviewing the impact of the EU methane regulation on global supply chains.

The Four Nations That Formally Objected and Why Their Positions Matter

On June 24, 2026, the energy ministers of the United States, Qatar, Nigeria, and Algeria sent a joint open letter to the President of the European Commission, the President of the European Council, and EU Member State leaders. The letter requested three specific interim measures before formal legislative amendments could be completed.

- A stop-the-clock mechanism to pause enforcement timelines while workable compliance methodologies are developed

- Grandfathering of new contracts signed during the legislative adjustment period to protect them from retroactive compliance obligations

- Removal of financial penalties for non-compliance during the transitional window

Each of the four signatories occupies a distinct and strategically significant position in Europe's energy supply architecture. These concerns also intersect with broader questions around critical minerals and energy security that are reshaping global resource diplomacy.

United States

Following the energy security disruptions of 2022, U.S. LNG exports to Europe expanded dramatically. American LNG now forms a meaningful part of European gas supply diversification strategy. U.S. LNG export facilities operate under domestic regulatory frameworks administered by the Federal Energy Regulatory Commission and environmental agencies that differ in methodology from EU MRV equivalence standards. Bridging that gap requires bilateral negotiation, not unilateral compliance.

Qatar

Qatar is among the world's largest LNG producers and has signed or extended long-duration supply agreements with multiple European utilities. These contracts, often structured over ten to twenty-five years, create acute exposure to multi-year compliance uncertainty. Qatari producers have made significant capital investment in methane emission reduction infrastructure, yet the pace of MRV equivalence development cannot be legislated into existence on a fixed deadline.

Nigeria

Nigeria exports both crude oil and LNG to European markets through complex joint-venture upstream structures involving multiple international operators. The practical challenge of deploying EU-equivalent MRV systems across these disaggregated operational arrangements is compounded by the infrastructure investment constraints that characterise developing-economy energy producers. The EUMR's binary compliance threshold, in this context, functions as a structural trade barrier regardless of whether that was the regulation's intention.

Algeria

Algeria is Europe's third-largest pipeline gas supplier, connected directly to Southern European markets through physical infrastructure. Geographic proximity and long-standing commercial relationships do not resolve the regulatory gap between Algerian upstream monitoring standards and EU MRV equivalence requirements. Furthermore, for pipeline suppliers, there is no LNG market alternative to redirect volumes if EU market access is compromised.

Industry Progress on Methane Reduction: Real But Insufficient for the Timeline

A critical and frequently mischaracterised aspect of this dispute is that the four signatory nations are not objecting to methane reduction as a policy objective. The joint letter explicitly acknowledges that energy producers across all four nations have made substantial capital investment in methane emissions reduction programmes and intend to continue these efforts in alignment with EUMR objectives.

The Global Methane Pledge targets a 30% reduction in global oil and gas sector methane emissions by 2030. The dispute is not about that goal. It is about the specific MRV equivalence mechanism and the January 2027 implementation timeline, which requires a level of measurement infrastructure that the global industry has not yet had time to build at the required scale.

This distinction matters for how the regulatory standoff should be interpreted. This is not a confrontation between climate ambition and energy security. It is a dispute about the operational feasibility of a specific compliance architecture within a specific timeframe — one with significant consequences for Europe's critical minerals supply chain and broader industrial dependencies.

The next major ASX story will hit our subscribers first

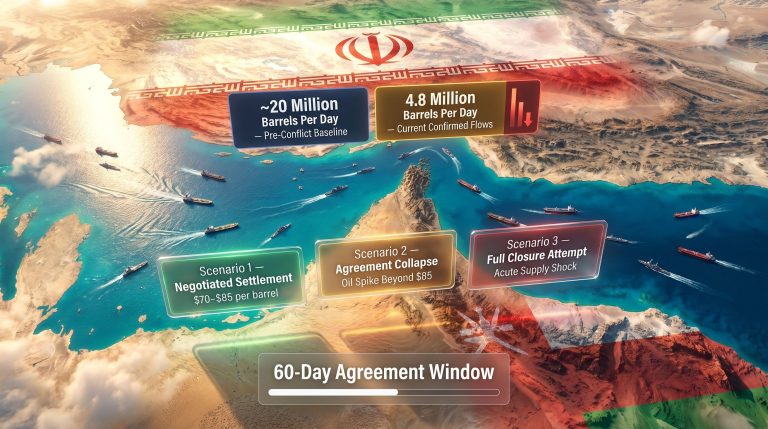

Price Impact Scenarios: What Different Outcomes Mean for European Energy Costs

| Scenario | Compliance Rate | Expected Market Impact |

|---|---|---|

| Full Enforcement (No Amendments) | ~13-57% of current imports eligible | Severe supply shortfall; significant price spike |

| Partial Enforcement (Discretionary) | Variable by Member State | Market fragmentation; legal uncertainty for long-term contracts |

| Stop-the-Clock Plus Amendments | Extended timeline for all suppliers | Temporary stabilisation; compliance pathway development |

| Phased Equivalence Standards | Graduated thresholds by region | Most operationally viable; preserves supply continuity |

The economic consequences extend beyond energy prices. Europe's industrial base, particularly energy-intensive sectors such as steel, chemicals, and fertiliser production, is already operating under significant cost pressure relative to global competitors. A supply-side price shock driven by regulatory non-compliance would compound existing competitiveness challenges across precisely the sectors that underpin European industrial output.

The geopolitical dimension is equally significant. The fact that the United States, Qatar, Nigeria, and Algeria — representing different geopolitical blocs and very different bilateral relationships with the EU — have aligned formally on this issue signals that the EUMR is now being interpreted internationally as a trade barrier embedded within a climate framework. That perception, if it hardens, could reshape the geopolitical mining landscape and affect EU trade and investment relationships extending well beyond the energy sector.

What a Workable Path Forward Requires

Three distinct policy pathways exist, each with different risk profiles.

Option 1: Legislative Amendment with Timeline Extensions

Formally amending the EUMR to introduce phased MRV equivalence thresholds calibrated to regional infrastructure capacity would provide the legal certainty that non-binding guidance cannot. Grandfathering provisions for contracts signed during the adjustment period would allow procurement to resume. A formally legislated stop-the-clock mechanism would replace discretionary forbearance with binding legal clarity.

Option 2: Bilateral MRV Equivalence Agreements

Negotiating country-specific equivalence frameworks with major exporting nations would allow graduated compliance pathways that recognise existing industry investment and infrastructure realities. A formal certification mechanism could provide legal certainty for both sides of the transaction without requiring full country-level infrastructure deployment by a fixed date.

Option 3: Current Regulation with Non-Binding Guidance

Proceeding with January 2027 implementation while relying on Member State discretion to avoid penalising non-compliant imports preserves regulatory ambition on paper. In practice, it fails to resolve the contractual and legal uncertainty already deterring new supply agreements. As the joint letter notes, exporters and importers are unwilling to enter into contracts that knowingly violate EU law regardless of informal assurances against enforcement.

The most operationally viable path forward combines a formally legislated timeline extension with bilateral MRV equivalence agreements structured around the Global Methane Pledge's 2030 objectives. This approach preserves the EUMR's environmental goals while preventing a structural disruption to European energy supply. The trade war economic impact of mismanaged regulatory implementation serves as a broader cautionary example of how policy timelines can outpace commercial realities.

Frequently Asked Questions: EU Methane Regulations and Europe's Oil and Gas Supply

What is the EU Methane Regulation?

Regulation EU 2024/1787, known as the EUMR, requires importers of oil and natural gas into the EU to demonstrate that their suppliers meet methane monitoring, reporting, and verification standards equivalent to EU domestic requirements. It entered into force in August 2024 and introduces escalating obligations through to 2030, culminating in maximum methane intensity caps for all imports.

When does the EUMR begin affecting import contracts?

The most immediate critical threshold takes effect on January 1, 2027, when all new natural gas import contracts must demonstrate MRV equivalence. Given that procurement cycles for 2027 delivery volumes are already underway, this deadline is operationally present for energy market participants right now.

Why is crude oil exposure so high at 87%?

The 87% non-compliance exposure reflects structural measurement gaps across global producing regions, not producer unwillingness. EU MRV equivalence standards were designed around European operational contexts and require a precision of measurement that most exporting nations' upstream infrastructure cannot currently deliver within the prescribed timeline.

What penalties can EU Member States impose?

Member states can impose penalties of up to 20% of a company's annual turnover for non-compliance, though the regulation includes provisions stating that penalties must not endanger energy security. The tension between these two elements remains legally unresolved. A critical raw materials facility established at European level could offer one model for how the EU structures compliance infrastructure in practice.

Which nations formally objected to the EUMR?

Energy ministers from the United States, Qatar, Nigeria, and Algeria jointly wrote to EU leadership on June 24, 2026, requesting a stop-the-clock mechanism, contract grandfathering, and removal of transitional penalties. The letter was signed by U.S. Secretary of Energy Chris Wright, Qatari Minister of State for Energy Affairs Saad Sherida Al-Kaabi, Nigerian Minister of State for Petroleum Resources Ekperikpe Ekpo, and Algerian Minister of State for Hydrocarbons Mohamed Arkab.

Is the EU likely to amend the EUMR before January 2027?

The European Commission is reportedly considering a "sufficient share" standard for country-level compliance and non-binding guidance discouraging penalties. However, no formal legislative amendments have been adopted as of the time of writing, and the January 2027 deadline remains legally operative.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Projections, compliance scenarios, and market impact estimates are based on available independent analysis and should not be relied upon as definitive forecasts. Regulatory frameworks may change. Readers are encouraged to consult primary legal and regulatory sources for decisions dependent on EUMR compliance requirements. For official statements and primary source documentation, the U.S. Department of Energy Newsroom at energy.gov publishes official correspondence, policy analyses, and energy trade-related announcements.

Want to Track the Investment Opportunities Emerging From Global Energy and Commodity Disruptions?

As regulatory frameworks like the EU Methane Regulation reshape energy supply chains and accelerate demand for alternative commodities, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex market shifts into actionable investment opportunities the moment they are announced. Explore historic discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.