May 21, 2026

The Structural Fault Line in Every Major Trade Deal

Across decades of transatlantic trade negotiations, one pattern repeats with near-mechanical consistency: the broader framework gets resolved, implementation timelines get agreed, and then steel and aluminium bring everything to a grinding halt. These two commodities occupy a unique intersection of industrial policy, national identity, and political economy that makes them almost impossible to treat like ordinary traded goods.

The EU trade pact with US aluminium and steel tariffs at its centre is the latest chapter in this long-running story. Understanding why these materials remain unresolved, what the current agreement actually contains, and what the path forward looks like requires stepping beyond the headlines and into the structural mechanics of how transatlantic metals trade actually works.

When big ASX news breaks, our subscribers know first

What the Turnberry Framework Actually Established

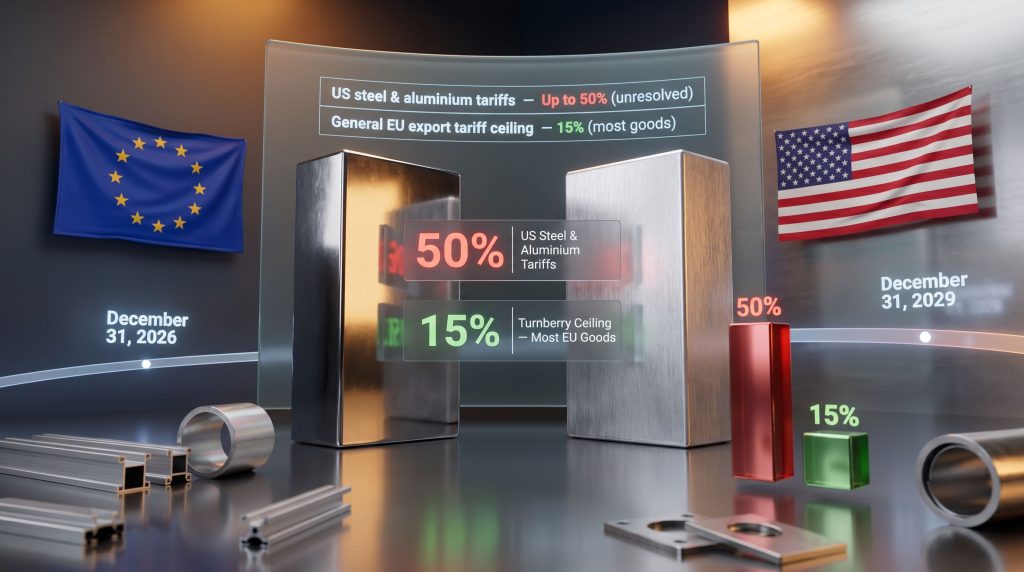

The trade agreement reached at Turnberry in 2025 represented a meaningful step toward reducing transatlantic tariff friction. Under the framework, a 15% ceiling was applied to the majority of EU goods entering the US market, while the EU reciprocated by removing or reducing import duties on a range of American industrial goods and specific agricultural products.

One of the more notable concessions on the EU side was the extension of tariff-free access for US lobster into European markets for an additional five years, building on an arrangement first introduced in 2020. This element of the deal holds particular symbolic importance for Washington as a visible deliverable.

However, the Turnberry deal contained a significant structural gap: steel, aluminium, and their downstream derivatives were explicitly carved out of the 15% tariff ceiling. Furthermore, US steel and aluminium tariffs on EU derivative exports remained as high as 50%, more than three times the general ceiling applied to other goods.

| Trade Element | Status Under Turnberry Framework |

|---|---|

| General EU export tariff ceiling | 15% (most goods) |

| US tariffs on EU steel and aluminium derivatives | Up to 50% (unresolved) |

| EU tariffs on US industrial goods | Removed or reduced |

| US lobster access to EU market | Tariff-free for 5 years |

| Steel and aluminium derivatives | Ongoing negotiation |

| Tariff-rate quota framework for metals | Exploratory, not binding |

The 50% Gap and Why It Matters to EU Industry

The difference between a 15% tariff and a 50% tariff is not merely numerical. For manufacturers whose products sit at the end of complex supply chains incorporating steel or aluminium components, that gap can represent the difference between commercially viable export pricing and effective market exclusion.

Steel-Intensive Exports Under Pressure

EU export categories most exposed to elevated US metals duties include:

- Machinery and industrial equipment with embedded steel components

- Automotive parts and sub-assemblies

- Structural fabrications and engineered steel products

- Precision manufacturing incorporating aluminium castings or extruded profiles

European steel industry groups, including Eurofer, have consistently highlighted that the 50% tariff rate has caused measurable damage to downstream manufacturers. Indeed, according to Eurofer, uncertainty remains even as cooperation on steel is confirmed, with the 50% tariff continuing to weigh heavily on industry. The compliance burden intensified further in September 2025 when the US expanded origin-proof requirements for metal-containing goods, adding significant administrative overhead for EU exporters.

Why Aluminium Derivatives Are a Distinct Problem

A critical distinction often overlooked in broader trade coverage is the difference between primary aluminium and aluminium derivatives for tariff classification purposes. The US aluminium tariffs impact on downstream processed products is particularly severe, covering categories such as:

- Extruded profiles used in construction, transport, and industrial applications

- Rolled sheet and plate used in packaging, aerospace, and automotive manufacturing

- Aluminium castings used across mechanical and structural applications

These derivative categories attract elevated duties under the current US tariff schedule, creating a compounding problem for European producers. EU aluminium manufacturing already operates under significant cost pressure due to European energy market dynamics, where electricity prices remain structurally higher than in competing production regions. When restricted US export access is layered on top of elevated production costs, the margin pressure for European aluminium producers becomes acute.

European steel and aluminium producers have made the case that taxing finished derivative products at 50% effectively penalises the value-added manufacturing process itself, not just the raw material inputs. The downstream impact extends well beyond primary smelters and rolling mills into fabricators, component manufacturers, and systems integrators across the European industrial base.

The Safeguards the EU Built Into the Agreement

Recognising that a full resolution on metals was not achievable within the Turnberry negotiating window, EU negotiators secured a set of conditional protections designed to preserve leverage without terminating the broader agreement.

How the Suspension Mechanism Works

The European Commission obtained the legal right to suspend tariff preferences granted to the United States if Washington continues applying duties above 15% on EU steel and aluminium derivatives beyond December 31, 2026. This is not an automatic trigger but an activatable mechanism, meaning the Commission retains political discretion over whether and when to use it.

The mechanism functions as a structured deterrent. Its value lies not only in the action it permits but in the credible threat it creates, giving Washington a concrete incentive to resolve the metals question before the year-end deadline.

The Sunset Clause and Its Political Significance

The regulation implementing the trade pact is set to expire automatically on December 31, 2029, unless the European Parliament and EU member states vote to renew it. This built-in expiry serves multiple purposes:

- It prevents the EU from being locked into a framework that may no longer reflect trade conditions

- It provides a formal renegotiation window every four years

- It gives EU lawmakers ongoing leverage over the agreement's continuation

Both the sunset clause and the enhanced suspension mechanism were introduced at the insistence of EU Parliament negotiators rather than the original Commission proposal. Bernd Lange, who led Parliament's trade committee engagement on the file, characterised the final text as a substantially improved version of what the Commission had initially tabled.

Three-Layer Protection Architecture:

The EU's approach embeds a conditional suspension trigger (activatable if US duties on derivatives exceed 15% past end-2026), a hard expiry date (December 2029), and a parliamentary ratification requirement. This structure ensures the framework remains reversible rather than permanent.

The Political Dynamics Behind the Metals Deadlock

Section 232 and the Weight of Domestic US Politics

US tariffs on steel and aluminium trace their origin to Section 232 of the Trade Expansion Act of 1962, which allows the President to impose trade restrictions on national security grounds. The US steel tariffs analysis shows that measures introduced in 2018 established a 25% rate on steel and 10% on aluminium, with subsequent adjustments pushing derivative tariffs higher. These measures were deliberately constructed with domestic political constituencies in mind, particularly manufacturing regions with high employment in metals production.

Any US administration seeking to reduce these tariffs faces significant political exposure, regardless of the broader trade policy direction. This structural reality explains why steel and aluminium negotiations are consistently the last chapter resolved, or left unresolved, in any US trade agreement.

The Asymmetry Between EU and US Priorities

EU Trade Commissioner Maroš Šefčovič described steel discussions as probably the most difficult chapter of the entire negotiating process, and the asymmetry of the two sides' positions explains why. The US had already secured its primary concessions: the EU's commitment to tariff-free lobster access and reduced barriers on American industrial goods. Washington's key deliverables were embedded in the Turnberry deal from the outset.

The EU, by contrast, is still seeking resolution on its primary concern: bringing metal derivative duties down to the 15% ceiling or establishing a workable tariff-rate quota framework. This negotiating imbalance creates an inherent drag on progress.

The US stakeholders Šefčovič engaged with following the agreement's announcement included Commerce Secretary Howard Lutnick, Treasury Secretary Scott Bessent, and US Trade Representative Jamieson Greer, reflecting the breadth of Washington departments with equities in the metals question.

Parliamentary Dynamics in Brussels

Some MEPs had delayed approval of tariff reductions specifically over concerns about unresolved US duties on European metals. Željana Zovko, lead negotiator for the centre-right European People's Party, framed the safeguards as mechanisms designed to shield European businesses from ongoing commercial uncertainty rather than as political commentary on any particular US administration.

Member states with significant steel and aluminium manufacturing bases, including Germany, France, Italy, and Spain, applied sustained pressure to ensure the suspension mechanism was operationally credible rather than symbolic. In addition, nearly half of EU metals exports risk higher US tariffs, reinforcing why parliamentary scrutiny of the metals chapter has remained so intense.

Tariff-Rate Quotas as a Potential Resolution Path

How the TRQ Model Functions

A tariff-rate quota permits a defined volume of goods to cross a border at a preferential or zero tariff rate, with standard (higher) rates applying to volumes above the quota threshold. In metals negotiations, TRQs are attractive because they allow both sides to claim partial victories:

- The US retains its protective tariff structure above the quota volume, satisfying domestic producers

- The EU secures preferential market access for a defined volume of derivative exports

- Both sides can point to the arrangement as evidence of cooperative trade management

The 2021 temporary suspension of Section 232 tariffs under the Biden administration, which introduced a TRQ framework for EU steel, provided a working precedent for this approach. That arrangement permitted a defined volume of EU steel exports to enter the US at pre-232 tariff levels.

The Complexities of Applying TRQs to Aluminium Derivatives

Aluminium derivatives present more complex TRQ design challenges than primary metals:

- Quota volume calibration must balance EU industry access needs against US domestic producer opposition

- Rules-of-origin compliance is complicated by the multi-stage processing involved in derivative production, where aluminium from multiple sources may be incorporated into a single finished product

- Global overcapacity dynamics affect quota utilisation patterns, as third-country producers may attempt to route product through the EU to access preferential quota volumes

Both the EU and US have acknowledged the threat posed by expanding global aluminium production capacity, particularly from Chinese and Gulf region producers. The global commodity tariff impacts of these overcapacity pressures theoretically create a basis for coordinated trade defence rather than bilateral friction, but the current tariff standoff diverts political bandwidth away from that potential alignment.

The next major ASX story will hit our subscribers first

How the Broader Aluminium Market Absorbs the Disruption

Trade Flow Redirection and Pricing Effects

Elevated US tariffs on EU aluminium derivatives do not eliminate trade flows; they redirect them. EU producers facing a 50% tariff barrier on US market access shift volumes toward alternative destinations, increasing competitive pressure in other markets. Meanwhile, US buyers of aluminium derivatives face a narrower supplier base, which can support higher domestic pricing in the short term but creates supply chain concentration risks over time.

For European aluminium producers, the combination of restricted US market access and competition from lower-cost producers in Asia, the Middle East, and increasingly North Africa creates a structural squeeze. The Gulf Cooperation Council region in particular has expanded aluminium production capacity significantly in recent years, leveraging access to subsidised energy to compete on cost in markets where EU producers previously held positioning.

The EU trade pact with US aluminium and steel tariffs does not occur in isolation. With global aluminium production capacity continuing to expand, the longer the transatlantic dispute persists, the harder it becomes for Western producers to maintain competitive positioning in third markets where they are not protected by domestic trade barriers.

The Energy Cost Dimension

A factor that receives insufficient attention in trade policy discussions is the structural energy cost disadvantage facing European aluminium producers. Aluminium smelting is among the most electricity-intensive industrial processes, with energy typically representing 30–40% of primary production costs. European electricity prices have remained elevated relative to competing production regions, meaning EU producers compete on quality and technical specification rather than cost.

When US tariffs reduce the premium that EU producers can extract in their most technically demanding export market, the commercial rationale for maintaining European smelting capacity weakens. This creates a long-term structural risk to European aluminium production that extends well beyond individual trade negotiations.

Key Milestones and Scenarios Through 2026–2029

The December 2026 Decision Point

The end of 2026 represents the first hard political deadline in the metals resolution process. If US duties on EU steel and aluminium derivatives remain above 15% past December 31, 2026, the European Commission gains the legal basis to activate the suspension mechanism and withdraw tariff preferences on US goods. This creates a concrete incentive structure for Washington to act.

Ratification and the Member State Factor

Before the pact can be fully implemented, both the European Parliament and EU member states must vote to ratify the final text. Member states with significant metals industry exposure may push for stronger protective language before completing ratification, potentially extending the timeline. Consequently, the steel market challenges facing European producers will remain a central point of debate throughout ratification discussions.

Resolution Scenarios

| Scenario | Assessment | Outcome for EU Metal Exporters |

|---|---|---|

| US reduces derivative tariffs to 15% by end-2026 | Moderate likelihood | Full pact implementation; suspension mechanism not triggered |

| TRQ framework agreed before December 2026 | Moderate likelihood | Quota-based market access restored; partial relief |

| US maintains 50% tariffs; EU activates suspension | Lower but credible | Escalation risk; broader trade relationship under strain |

| Ratification delayed by EU Parliament | Low to moderate | Continued uncertainty; industry planning disrupted |

| Full renegotiation of metals chapter required | Low likelihood | Lengthy process; short-term market volatility |

Disclaimer: The scenario assessments above represent analytical perspectives based on publicly available information. They do not constitute investment advice or definitive predictions of policy outcomes. Trade negotiations involve complex political variables that can shift rapidly.

Frequently Asked Questions: EU Trade Pact and Aluminium and Steel Tariffs

What is the current US tariff rate on EU aluminium and steel derivatives?

As of mid-2026, US tariffs on EU steel and aluminium derivatives remain as high as 50%, despite the broader Turnberry agreement establishing a 15% ceiling on most other EU goods entering the US market.

What does the EU's suspension mechanism actually do?

It gives the European Commission the legal right to withdraw tariff preferences granted to the US if Washington continues applying duties above 15% on EU metal derivatives past the end of 2026. It is an activatable tool, not an automatic response.

Why does the sunset clause matter?

The regulation implementing the pact automatically expires on December 31, 2029, unless renewed by the EU Parliament and member states. This prevents the EU from being permanently bound to terms that may no longer reflect trade realities, and preserves ongoing renegotiation leverage.

What is a tariff-rate quota and how might it apply to metals?

A TRQ permits a defined export volume to enter a market at a reduced tariff rate, with higher rates applying above the threshold. For EU-US metals negotiations, a TRQ would allow EU producers to access the US market at preferential rates up to an agreed quota, with standard tariffs applying above it.

Why are aluminium derivatives harder to resolve than primary aluminium?

Derivative products involve multi-stage processing, complex rules-of-origin compliance, and broader downstream industry exposure. The tariff classification system treats extruded profiles, rolled sheet, and castings differently from ingot or billet, meaning the derivative category captures a much wider range of affected products.

Why Metals Always Sit at the End of the Negotiating Table

The pattern visible in the EU trade pact with US aluminium and steel tariffs is not unique to this negotiation. Across the history of US trade agreements, including NAFTA, the Korea-US Free Trade Agreement, and multiple rounds of multilateral negotiations, steel and aluminium have either been excluded from core tariff commitments or left as the final unresolved chapter.

The reason is structural. Metals industries carry political weight in both the US and EU that is disproportionate to their direct GDP contribution, because of their geographic concentration in regions with significant electoral and political influence. Beyond politics, both sides increasingly frame metals access through the lens of industrial resilience and supply chain security, not simply comparative advantage. When strategic framing is applied to a commodity, commercial logic alone cannot resolve the impasse.

The December 2026 deadline is now the most significant near-term test of whether the Turnberry framework can move beyond its current partial state, and whether transatlantic trade relations can establish a durable resolution to what has become one of the longest-running disputes in the bilateral trade relationship.

Want to Stay Ahead of the Resource Opportunities Emerging From Global Trade Disruptions?

When tariff disputes reshape commodity markets — creating pressure on steel, aluminium, and their downstream derivatives — early identification of significant mineral discoveries can position investors ahead of broader market moves. Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex commodity data into actionable opportunities; explore historic discoveries and their remarkable returns or start your 14-day free trial today to gain a market-leading edge.