July 14, 2026

The Invisible Tax on European Aluminium: How Energy and Supply Shocks Are Colliding

Few industrial sectors expose the fragility of globalised supply chains quite as starkly as primary aluminium production. Unlike most commodities, aluminium smelting is not just a mining or processing operation. It is, at its core, an electricity conversion process. Bauxite becomes alumina, and alumina becomes aluminium through one of the most power-hungry industrial reactions known to modern manufacturing. That single characteristic, more than any other, explains why the Europe aluminium market energy costs and supply disruptions cycle is absorbing a disproportionate share of pain from two simultaneous shocks that have reshaped global energy and metals markets through the first half of 2026.

Understanding what is happening requires looking beyond the headline price moves and into the structural mechanics that made European producers so exposed before the crisis even began.

When big ASX news breaks, our subscribers know first

Why European Smelters Were Already Fighting Uphill

Electricity is not merely an input cost for aluminium smelters. It is the defining variable that determines whether a facility is economically viable. Across European primary smelting operations, power accounts for between 37% and 40% of total production costs, placing the sector in a unique category of industrial vulnerability that few other manufacturing processes share.

The competitive disadvantage this creates is stark when measured against the rest of the world. Consider the following regional electricity cost comparison:

| Region | Estimated Electricity Cost Range | Cost Relative to Europe |

|---|---|---|

| Europe | €80–€120/MWh (2026) | Baseline |

| Russia | ~€25–€40/MWh | 2–3x cheaper |

| China | ~€30–€45/MWh | 2–3x cheaper |

| UAE/Gulf | ~€20–€35/MWh | 3–4x cheaper |

This disparity is not new, but it has grown dramatically more severe. Wholesale European electricity prices have risen more than fourfold since 2020, with peak prices exceeding €200/MWh during the worst periods of market stress. The European aluminium energy pressures facing producers are fundamentally structural — because aluminium trades against the London Metal Exchange benchmark, producers cannot simply pass energy cost increases onto their customers.

The consequence has been a slow haemorrhage of domestic capacity. Europe's active primary aluminium production has contracted to roughly 950,000 tonnes per year, creating an import dependency that now exceeds 90% of total consumption. The continent entered 2026 already operating on a thin buffer.

Key Insight: European aluminium producers did not arrive at this crisis in good health. Years of energy cost escalation had already eroded the financial reserves and operational flexibility that would have been needed to absorb simultaneous supply disruptions of this scale.

The Energy Price Transmission Chain: From the Strait of Hormuz to the Smelter Floor

How Does Hormuz Disruption Reach European Smelters?

The Strait of Hormuz handles approximately 20% of global LNG and oil flows, making it one of the most consequential maritime chokepoints in the world energy system. When shipping through the waterway faced disruption in early 2026, the effects did not stay contained to petroleum markets. They cascaded through the energy complex with remarkable speed, as explored in detail by Fastmarkets analysts covering aluminium's energy exposure.

The transmission mechanism works through several connected steps:

- Shipping disruptions reduce LNG availability reaching European terminals.

- Tighter gas supply pushes European natural gas spot prices higher.

- Higher gas prices feed directly into gas-fired electricity generation costs, lifting wholesale power prices.

- Elevated power prices increase the operating cost burden on aluminium smelters by hundreds of euros per tonne of output.

- With LME pricing constraining cost pass-through, smelter margins compress or turn negative.

The numbers behind this chain are significant. Furthermore, European gas price pressures rose by more than 50% following the onset of Hormuz-related disruptions, moving from approximately €30/MWh to around €46/MWh. Wholesale electricity prices climbed into the €80–€120/MWh range as a result.

According to Fastmarkets analyst Andy Farida, the prospect of sustained energy price elevation is amplified by the timing of the disruption, which coincides with Europe's summer gas storage and energy restocking season — a period of structurally heightened price sensitivity.

Analysts broadly expect that a genuine return to pre-disruption energy pricing could take between 6 and 12 months, even assuming shipping route normalisation begins soon. For smelters operating at or near breakeven, each additional month of elevated power costs increases the probability that temporary curtailments harden into permanent closures.

The Gulf Output Collapse: Quantifying the Supply Shock

The energy cost crisis unfolding inside Europe is being compounded by a supply shock originating thousands of kilometres away. The Middle East has historically supplied approximately 20% of Europe's aluminium imports, functioning as a critical balancing source for a continent that cannot self-supply its consumption needs.

That balancing mechanism has been severely disrupted. Gulf aluminium output is projected to fall by approximately 44% in 2026, declining from roughly 6.15 million tonnes in 2025 to an estimated 3.44–3.45 million tonnes. The facility-level disruptions behind this aggregate figure include:

- Aluminium Bahrain (Alba): Operating at approximately 50% of nameplate capacity as of late April 2026.

- Emirates Global Aluminium (EGA): Declared force majeure on portions of its contractual delivery obligations.

- Qatalum (Qatar): Running at approximately 60% capacity due to energy shortages, as reported by Hydro, which holds a 50% stake in the facility.

The disruption has not been limited to the Gulf. Supply tightness has extended to other key sources of aluminium that European buyers depend upon:

- South32's Mozal smelter (Mozambique): Portions of the operation placed on care and maintenance, reducing output volumes.

- Bjorkenborg smelter (Sweden): Delivery halts further tightened short-term European availability.

- Iceland: Production interruptions creating a specific problem for buyers seeking certified low-carbon metal.

Green Aluminium at Risk: Iceland and Mozambique are among Europe's most important sources of low-carbon primary aluminium. Disruptions to both simultaneously are creating a potential deficit in certified green metal that could push sustainability-linked premiums significantly higher and force procurement teams to reassess supplier diversification strategies.

The Premium Explosion: What Physical Markets Are Signalling

When physical supply tightens faster than financial markets can fully reflect, the gap shows up in regional premiums. These premiums, paid on top of the LME benchmark price to secure actual metal delivery, have become the most accurate real-time signal of how severe the supply shortage has become.

The data from the first half of 2026 is striking:

| Metric | Late February 2026 | End of May 2026 | Change |

|---|---|---|---|

| North Germany Billet Premium | USD 560–600/t | USD 1,175–1,250/t | ~+110% |

| LME Aluminium Benchmark | ~USD 3,480/t | ~USD 3,675/t | ~+5.6% |

| European Gas Price | ~€30/MWh | ~€46/MWh | ~+53% |

| Gulf Regional Output (2026 est.) | 6.15Mt (2025 base) | ~3.45Mt | ~-44% |

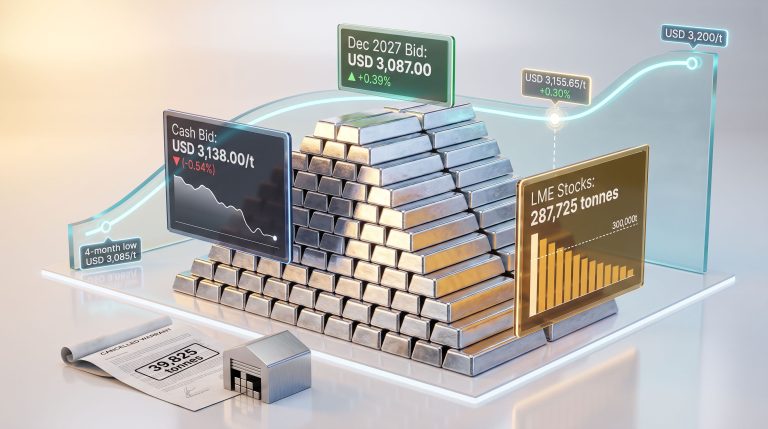

By the end of May 2026, aluminium billet premiums in North Germany had reached USD 1,175–1,250 per tonne, up from USD 560–600 per tonne in late February — representing an increase of approximately 110%. Rotterdam premiums recorded comparable gains. Physical primary aluminium premiums rose approximately 63% to $585 per tonne. These are premium levels not seen since the acute phase of the European energy crisis in 2022.

LME benchmark prices have also responded, rising from approximately USD 3,480 per tonne in early May to around USD 3,675 per tonne by month-end. As of early June 2026, benchmark prices were trading near USD 3,595 per tonne, representing a gain of approximately 44% compared to the same period one year earlier.

The divergence between Chinese and international price performance is captured in the SHFE-to-LME ratio, which declined from 7.03 in April to 6.66 in May 2026. A falling ratio signals that international prices are strengthening faster than domestic Chinese prices — a direct reflection of tighter supply conditions in the ex-China market.

Europe's Vanishing Smelter Base: Capacity Lost and Capacity at Risk

How Much Capacity Has Already Disappeared?

The demand for European aluminium has not disappeared, but the infrastructure capable of supplying it domestically has been eroding for years. Approximately 650,000 tonnes of European primary capacity has already been removed from the market in recent years, with curtailments at facilities including Aldel in the Netherlands, Uniprom's KAP smelter in Montenegro, and Speira's Rheinwerk plant in Germany.

Germany's recycled aluminium sector has also felt the pressure. Secondary production fell by 3% in Q1 2026, with producers pointing to high energy bills, compressed margins, and weakening demand from downstream industries including automotive, construction, and packaging. In addition, the broader industrial decarbonisation costs facing European manufacturers continue to compound the sector's structural difficulties.

An additional 900,000 tonnes of European capacity is considered at risk of partial or full closure if energy prices remain at current elevated levels. Against a consumption base that requires multiples of domestic production, Europe's active primary output of approximately 950,000 tonnes is structurally insufficient to buffer external supply shocks of the kind now unfolding.

The San Ciprián case study offers a more constructive data point. Alcoa's Spanish smelter, which curtailed output during the 2021 energy crisis, subsequently restarted operations after securing electricity supply agreements extending through 2027. The strategic lesson is clear: long-term power purchase agreements (PPAs) are increasingly the critical instrument separating viable European smelting operations from those exposed to spot energy price volatility.

The next major ASX story will hit our subscribers first

China's Upstream Strategy: Securing Bauxite While the West Contends With Shortages

While European producers navigate an increasingly hostile operating environment, China has been methodically reinforcing the upstream foundations of its aluminium industry. The contrast in strategic positioning is instructive, particularly when examined alongside broader China metals market dynamics that continue to reshape global supply chains.

Guinea exported 60.9 million tonnes of bauxite in Q1 2026, up from 48.6 million tonnes in the same period of 2025, representing year-on-year growth of approximately 25%. Furthermore, more than 70% of those shipments were destined for China. In March 2026 alone, China imported 18.12 million tonnes of Guinean bauxite, underscoring the scale and consistency of Beijing's raw material accumulation strategy.

This upstream consolidation has consequences for international markets. With Chinese domestic inventories remaining relatively stable and bauxite supply secure, Chinese producers face less cost pressure than their ex-China counterparts. The result is a widening structural gap between China's relatively well-supplied domestic market and the increasingly tight seaborne market serving the rest of the world.

Shanghai Metals Market has described the dynamic as accelerating export transmission — a concept referring to the growing role of Chinese aluminium exports in balancing shortages in international markets. However, tariffs, trade barriers, and geopolitical considerations continue to constrain the volume of Chinese metal that can reach Western markets directly.

Demand-Side Weakness: Why Lower Consumption Is Not Providing Relief

One of the more counterintuitive features of the Europe aluminium market energy costs and supply disruptions cycle is that weak downstream demand has done almost nothing to ease physical tightness or reduce premiums. European consumers are buying cautiously, managing inventory on a hand-to-mouth basis and avoiding forward commitments in a volatile pricing environment.

And yet premiums have still doubled. The explanation lies in the severity of the supply disruption relative to even a reduced demand base. When supply falls faster than demand weakens, markets tighten regardless of the direction of consumption.

Fastmarkets analyst James Moore has noted that a prolonged period of elevated energy costs risks placing additional pressure on manufacturing activity more broadly. Some market participants have pointed to growing backwardation in the aluminium forward curve as a mechanism that could eventually encourage inventory release. However, analysts note this dynamic has not yet materially eased physical shortages in practice.

Strategic Scenarios: Three Possible Paths for the European Market

The trajectory of the Europe aluminium market energy costs and supply disruptions outlook over the next 6 to 12 months will be shaped primarily by one variable: how long energy prices remain elevated. Three broad scenarios are plausible:

Scenario 1: Prolonged Disruption

Strait of Hormuz restrictions persist through the second half of 2026. European energy prices remain high through the winter restocking cycle. Additional smelter capacity from the 900,000 tonne at-risk pool closes permanently. Billet premiums remain near historic highs and import dependency deepens further.

Scenario 2: Partial Normalisation

Diplomatic or military developments reduce Hormuz disruption risk. Gulf smelters gradually restore output over a 6 to 12 month timeline. Energy prices ease modestly but remain structurally elevated compared to pre-2022 baselines. Premiums compress from peak levels but stay above long-run averages.

Scenario 3: Structural Transformation

Persistent energy cost disadvantage accelerates the permanent closure of uneconomic European capacity. European demand is increasingly met through imports from Canada, China, and recovering Gulf facilities. Policy interventions reshape the competitive landscape, though the form and effectiveness of such interventions remains uncertain.

The critical variable across all three scenarios is time. Each additional month of elevated energy prices increases the probability that what began as temporary curtailment hardens into permanent capacity loss, fundamentally reshaping the European aluminium production base for years, not quarters.

Practical Implications for Producers, Buyers, and Policymakers

What Should Producers Do Now?

For aluminium producers operating in Europe:

- Prioritise securing long-term power purchase agreements modelled on the San Ciprián framework, insulating operations from spot energy price exposure.

- Evaluate the operational and financial case for partial curtailment over full shutdown, preserving the optionality to restart when conditions improve.

- Monitor the SHFE-to-LME ratio as an early warning indicator of shifts in Chinese export competitiveness and the relative tightness of international markets.

How Should Buyers Respond?

For downstream buyers and manufacturers dependent on aluminium supply:

- Review supply chain diversification strategies to reduce exposure to any single import corridor, particularly Gulf-dependent supply lines.

- Assess the financial impact of further premium escalation if Gulf output recovery is delayed beyond current expectations.

- Consider structured forward hedging across both LME benchmark price and physical premium components to limit cost volatility.

The broader reshaping of how major aluminium producers are positioning themselves globally will consequently influence which supply alternatives become available to European buyers over the medium term.

For policymakers and regulators:

- The case for strategic aluminium reserves at the EU level, analogous to existing oil strategic reserve frameworks, is gaining analytical credibility as import dependency deepens.

- Industrial electricity cost support mechanisms could prevent further permanent capacity loss in a sector where restart costs are high and timelines are long.

- Carbon Border Adjustment Mechanism design should account for the competitive distortions created by the energy cost differentials illustrated in this analysis. The reshaping of European aluminium supply chains is furthermore examined in detail by industry analysts tracking secondary market shifts.

Frequently Asked Questions

What percentage of aluminium smelter costs are accounted for by electricity?

Electricity typically represents between 37% and 40% of total production costs at European primary aluminium smelters, making it the single largest variable cost driver.

How much have European aluminium billet premiums increased in 2026?

North Germany billet premiums approximately doubled between late February and the end of May 2026, rising from USD 560–600 per tonne to USD 1,175–1,250 per tonne, according to Fastmarkets assessments.

Why does the Strait of Hormuz matter for European aluminium supply?

The strait carries approximately 20% of global LNG and oil flows. Disruptions elevate European gas and electricity prices, directly increasing smelter operating costs. The waterway also borders Gulf-producing nations that historically supply around 20% of Europe's aluminium imports.

How much European capacity is at risk of permanent closure?

Approximately 650,000 tonnes has already been curtailed. A further 900,000 tonnes of capacity remains at risk of partial or full closure if energy prices remain at current levels.

What is the current LME aluminium price?

As of early June 2026, LME benchmark aluminium was trading near USD 3,595 per tonne, approximately 44% higher than the same period one year earlier.

How long could the supply disruption last?

Industry analysts estimate that recovery timelines for the Europe aluminium market energy costs and supply disruptions cycle could extend between 6 and 12 months, contingent on geopolitical developments affecting both Hormuz shipping and Gulf smelter restart schedules.

Want to Stay Ahead of Major Commodity Supply Shocks Like This One?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity market shifts into actionable investment opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure a market-leading edge before the next major opportunity emerges.