July 20, 2026

The Structural Fault Line Running Through Europe's Industrial Economy

When an entire continent's manufacturing base depends on a raw material it can no longer produce in sufficient quantities, the consequences extend far beyond commodity price volatility. Aluminium sits at the intersection of virtually every major European industrial transition currently underway: electric vehicle production, renewable energy infrastructure, sustainable packaging, and lightweight construction. Yet the architecture of aluminium supply in Europe is quietly fracturing, and the recycling sector, despite its genuine strengths, is being asked to carry more weight than it was ever designed to bear alone.

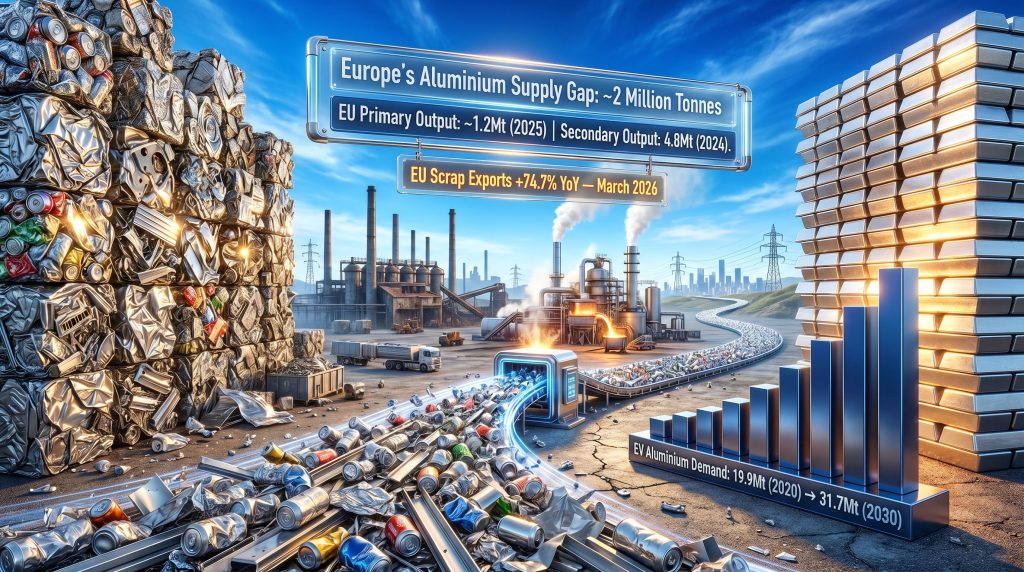

Understanding the Europe aluminium recycling supply gap requires looking beyond headline recycling statistics. Europe recycles more of its available aluminium scrap than any other major industrial region on earth, and yet it still runs a structural supply deficit of an estimated 2 million tonnes annually. That paradox is the central puzzle driving industry debate, policy reform, and billions of euros in capital allocation decisions.

When big ASX news breaks, our subscribers know first

The Numbers Behind the Crisis

Global aluminium demand reached 116 million tonnes in 2024, with approximately 74 million tonnes (64%) sourced from primary production and around 42 million tonnes (36%) supplied by secondary, or recycled, aluminium. Within Europe, the picture is considerably more strained.

| Metric | Figure | Context |

|---|---|---|

| Global aluminium demand | 116 million tonnes | 2024 |

| Primary production share | ~74 million tonnes (64%) | 2024 |

| Recycled aluminium share | ~42 million tonnes (36%) | 2024 |

| Europe secondary output | 4.8 million tonnes | 2024 |

| EU primary production | ~1.2 million tonnes | 2025 |

| EU primary output decline | ~60% contraction | Since 2005 |

| Estimated European supply gap | ~2 million tonnes | Current |

| Annual scrap exported from Europe | ~1.4 million tonnes | Current |

| EU scrap export growth YoY | +74.7% | March 2026 |

| EU scrap export growth since 2014 | +66% | Long-term trend |

| Beverage can recycling rate | 76.3% | Europe, 2023 |

| Automotive/construction recycling | >90% | Current |

Despite achieving an 81% recycling rate on potentially available scrap, Europe remains a net exporter of aluminium scrap, shipping approximately 1.4 million tonnes offshore each year. This outflow directly contradicts the circular economy ambitions embedded in EU industrial policy and materially worsens the feedstock shortage facing domestic manufacturers. Furthermore, the broader policy landscape — including the EU metals action plan — has yet to translate into meaningful reductions in this outflow.

How Primary Production Collapsed Over Two Decades

The Energy Economics of Smelting

Primary aluminium production is one of the most electricity-intensive industrial processes in existence. The Hall-Heroult electrolysis process that converts alumina into aluminium metal requires between 13 and 16 MWh of electricity per tonne produced. Electricity accounts for roughly 40% of total primary production operating costs, making European smelters extraordinarily exposed to energy price movements.

When wholesale European electricity prices surged following 2021, the financial arithmetic of domestic primary smelting broke down rapidly. Nearly 50% of Europe's primary smelting capacity was either curtailed or permanently closed between 2021 and 2023. The smelters that remain operational are increasingly struggling to compete with facilities in regions where electricity costs are a fraction of European levels. Initiatives such as aluminium operations repowering in other regions demonstrate how competitive the global landscape has become.

A Two-Decade Structural Retreat

| Year | European Primary Output | Import Volume |

|---|---|---|

| 2002 | 4.9 million tonnes | 2.6 million tonnes |

| 2005 | ~2.9 million tonnes (EU) | Rising |

| 2021-2023 | ~50% EU capacity cut | Accelerating |

| 2025 | 3.4 million tonnes | 4.4 million tonnes |

The trajectory is unambiguous. In 2002, Europe produced 4.9 million tonnes of primary aluminium and imported 2.6 million tonnes to supplement domestic demand. By 2025, the equation had inverted completely: domestic output had fallen to 3.4 million tonnes while imports climbed to 4.4 million tonnes. Europe had transitioned from a net producer to a structurally import-dependent region.

Within the EU specifically, the deterioration is even sharper. Primary output declined from 2.9 million tonnes in 2005 to approximately 1.2 million tonnes by 2025, a contraction of close to 60% over two decades. This is not a cyclical downturn. It represents the systematic hollowing out of a foundational industrial capability.

What the Energy Consumption Data Reveals

Eurostat data places Europe's average industrial energy consumption at approximately 4,000 TWh. Per International Aluminium Institute figures, around 2.75% of that total, equating to roughly 108,446 GWh, was consumed in the production of approximately 6.99 million tonnes of primary aluminium across the continent. At the EU level specifically, total industrial energy consumption in 2024 settled at around 8,835 PJ, essentially flat year-on-year with a marginal 0.1% increase versus 2023.

Western and Central European primary aluminium production consumed an estimated 36.76 to 45.25 TWh of that total in 2024. These figures illustrate both the scale of energy dependency in primary production and the magnitude of potential savings available if secondary production were to absorb a greater share of output.

The Recycling Sector: Strengths, Limits, and the Scrap Leakage Problem

Secondary Aluminium's Remarkable Growth Trajectory

Europe's secondary aluminium sector has expanded consistently over the past two decades. Output grew from 3.9 million tonnes in 2002 to 4.8 million tonnes in 2024, and secondary production overtook primary output as early as 2012. This structural shift reflects both deliberate investment and the economic logic of recycling in a high-energy-cost environment.

The energy efficiency case for secondary production is compelling:

- Secondary aluminium production requires approximately 600 to 800 kWh per tonne

- Primary production requires 13,000 to 16,000 kWh per tonne

- This represents a 95% reduction in energy consumption

- Producing 6.99 million tonnes via secondary processes would require only approximately 5,422 GWh of electricity

- The implied energy saving versus primary production exceeds 103,000 GWh

In a continent where energy costs are a defining competitive variable, those figures carry considerable weight. The economic and environmental case for maximising secondary output is not seriously contested. Industry analysts examining aluminum and alumina markets have similarly noted the growing primacy of secondary production economics in shaping long-term investment decisions.

The Scrap Leakage Paradox

Europe recycles 81% of its potentially available aluminium scrap, the highest rate globally, yet continues to export approximately 1.4 million tonnes of that scrap offshore each year. This scrap leakage is the single most consequential driver of the feedstock shortage facing European manufacturers.

The mechanics of scrap leakage are straightforward but stubborn. Asian buyers, who absorb approximately 75% of all EU aluminium scrap exports, consistently offer prices that European recyclers cannot economically match. This is not a market failure in the conventional sense; it reflects a genuine cost differential rooted in lower energy prices, different regulatory environments, and scale advantages in Asian processing capacity.

The scale of this outflow has accelerated dramatically. EU aluminium scrap exports surged 74.7% year-on-year in March 2026 and have risen 66% since 2014. The trajectory is moving in precisely the wrong direction at precisely the wrong time, as downstream manufacturers face intensifying feedstock competition. According to supply chain analysis on the recycling gap, the structural drivers of this leakage require coordinated intervention across trade, regulation, and industrial policy to be meaningfully addressed.

A critical but often overlooked dimension of this problem is the quality mismatch it creates. When high-grade scrap is exported in volume, what remains within Europe tends to be of lower quality or less efficiently sorted, which increases processing costs for domestic recyclers and reduces the yield of usable alloy-grade material.

Why Recycling Rates Alone Cannot Solve the Problem

Europe's recycling performance is genuinely impressive across key sectors:

- Beverage cans: 76.3% recycling rate (2023)

- Automotive sector: above 90%

- Construction sector: above 90%

- Overall scrap capture rate: 81% of potentially available material

Yet even at these world-leading rates, a structural 2-million-tonne deficit persists. The reason is that recycling efficiency at the collection and processing stage is undermined by the volume of material exiting the domestic system entirely. Reaching a hypothetical 100% domestic recycling rate would help, but the export channel means that the effective feedstock pool available to European recyclers is significantly smaller than aggregate scrap generation figures imply.

There is also a metallurgical ceiling to what secondary aluminium can deliver. Repeated recycling cycles introduce trace element contamination that affects alloy performance in demanding applications. High-specification aerospace components, advanced electrical systems, and certain automotive structural alloys require primary aluminium with tightly controlled compositions that recycled metal cannot reliably replicate at scale.

The Demand Acceleration That Raises the Stakes

Electrification and the New Aluminium Intensity

The structural supply challenge described above is colliding with a demand surge of considerable magnitude. Global aluminium consumption is projected by the International Aluminium Institute to rise approximately 40% between 2020 and 2030, requiring an additional 33.3 million tonnes across all sectors.

| Sector | 2020 Demand | Projected 2030 Demand |

|---|---|---|

| Electric vehicles | 19.9 million tonnes | 31.7 million tonnes |

| Solar & power transmission | Baseline | +5.2 million tonnes |

| Construction | Baseline | +4.6 million tonnes |

| Food & beverage packaging | 7.2 million tonnes | 10.5 million tonnes |

For Europe specifically, the energy transition alone could add approximately 5 million tonnes of annual aluminium demand by 2040, representing roughly 30% growth above current consumption levels. The convergence of declining domestic primary output and rising downstream demand creates a supply gap that grows wider with each passing year of inaction. Consequently, leading aluminium mining companies are repositioning their strategies in anticipation of these demand shifts.

Policy Architecture: What the EU Has Built and Where It Falls Short

The Regulatory Framework

The EU has assembled a meaningful policy architecture oriented toward circular aluminium supply. The key instruments and their direct relevance to the recycling gap are summarised below:

| Policy Instrument | Primary Objective | Aluminium Recycling Impact |

|---|---|---|

| EU Waste Framework Directive | Resource efficiency, waste prevention | Moves industry away from linear models |

| Packaging & Packaging Waste Regulation (PPWR) | Mandate recyclability, require Deposit Return Schemes | Boosts beverage can collection rates |

| Waste Shipment Regulation (WSR) | Restrict scrap exports to non-OECD countries | Potential to reduce scrap leakage |

| Critical Raw Materials Act (CRMA) | Strengthen domestic supply chains | Encourages recycling infrastructure investment |

| End-of-Life Vehicle Circularity Rules | Improve automotive material recovery | Increases aluminium scrap from end-of-life vehicles |

European industry, through collective investment, has committed approximately EUR 700 million to new recycling plants, capacity expansions, and advanced processing technologies. The broader economic footprint of the European aluminium industry is substantial: approximately EUR 40 billion in annual revenue, 250,000 direct employees with roughly 90% concentrated in downstream and recycling activities, and an estimated 1 million indirect jobs supported across the value chain.

Where the Policy Framework Has Structural Gaps

The Waste Shipment Regulation holds the most direct potential for reducing scrap leakage, but its effectiveness depends on implementation timelines and enforcement mechanisms that remain uncertain. More fundamentally, regulatory measures cannot override the price differential that makes exporting scrap to Asian buyers economically rational for scrap collectors and traders operating within the EU.

Deposit Return Schemes represent a meaningful lever for improving beverage can collection rates, but their scope does not extend to industrial and post-production scrap streams, where volume is largest and leakage most severe. However, the aluminium tariffs impact on global trade flows adds a further layer of complexity to the scrap export dynamic, as redirected material seeks new markets in response to shifting trade barriers. Industry bodies such as Recycling Europe have called for more robust trade measures to ensure sufficient domestic availability of aluminium scrap.

The next major ASX story will hit our subscribers first

What a Realistic Pathway Forward Looks Like

A Scenario Analysis: Halving Scrap Leakage

If Europe retained an additional 700,000 tonnes of currently exported scrap annually, representing a 50% reduction in outflows, this would close roughly 35% of the estimated 2-million-tonne supply gap. Combined with incremental recycling rate improvements driven by expanded Deposit Return Schemes and new end-of-life vehicle recovery rules, this scenario could materially reduce import dependence within a 5 to 7 year horizon.

The critical variable is energy cost competitiveness. Without targeted relief for energy-intensive recycling operations, the economic incentive to sell scrap to higher-bidding overseas buyers remains structurally intact regardless of what the regulatory framework prescribes.

Three Strategic Priorities That Must Be Addressed Simultaneously

- Scrap retention through enforced trade measures that reduce the volume of aluminium scrap leaving the EU, particularly toward non-OECD markets where material recovery standards are lower

- Energy cost competitiveness through targeted industrial energy policy that allows European recyclers and remaining primary smelters to operate on a viable cost basis relative to overseas competitors

- Design for recyclability embedded across automotive, construction, and packaging sectors to improve both the quality and volume of recoverable scrap entering the domestic system

No single intervention resolves the Europe aluminium recycling supply gap in isolation. The case for a dual-track strategy — one that maximises secondary output wherever technically viable while preserving competitive low-carbon primary production capacity for applications where recycled metal cannot substitute — is increasingly well-supported by the data.

Recycling is not a replacement for primary aluminium production. It is the foundation of a more resilient, lower-carbon supply architecture. The strategic objective is integration rather than substitution, and the gap between where Europe is today and where it needs to be by 2030 makes the urgency of that integration difficult to overstate.

Frequently Asked Questions

What is the Europe aluminium recycling supply gap?

The Europe aluminium recycling supply gap refers to the estimated 2-million-tonne shortfall between the volume of recycled aluminium feedstock available to European manufacturers and the volume those manufacturers require to meet current and projected demand. The gap persists despite Europe achieving the highest aluminium scrap recycling rate of any major global region.

Why does Europe continue to export aluminium scrap?

Asian buyers, who account for approximately 75% of EU aluminium scrap export destinations, consistently offer prices that European recyclers cannot match given the latter's elevated energy and operating costs. EU scrap exports have grown 66% since 2014, reflecting a sustained price-driven structural trend rather than a temporary market anomaly.

How much energy does secondary aluminium production save versus primary?

Secondary production consumes approximately 600 to 800 kWh per tonne compared to 13,000 to 16,000 kWh per tonne for primary production, a reduction of approximately 95%. Scaled to an output of 6.99 million tonnes, secondary production would require roughly 5,422 GWh versus more than 108,000 GWh for primary, implying a saving exceeding 103,000 GWh.

Can EU policy alone close the supply gap?

Policy instruments including the PPWR, WSR, and CRMA establish a supportive regulatory framework but cannot independently resolve the gap. Market forces, particularly the energy cost disadvantage facing European recyclers relative to overseas competitors, require complementary industrial energy policy interventions that the current framework does not fully address.

Disclaimer: This article contains forward-looking projections and demand forecasts sourced from industry bodies including the International Aluminium Institute. These projections represent estimates based on current data and modelling assumptions and should not be interpreted as guaranteed outcomes. Readers making investment or operational decisions should conduct independent analysis and consult qualified advisers.

Want to Track the ASX Companies Positioned to Benefit From Surging Global Aluminium Demand?

As European primary production contracts and downstream demand accelerates toward 2030, the structural supply gap is reshaping capital flows across the global aluminium sector — including exploration and mining opportunities on the ASX. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data into actionable insights, so subscribers can identify emerging opportunities ahead of the broader market — start your 14-day free trial today or explore historic discovery returns to understand the scale of what early-stage positioning can deliver.