August 5, 2026

When the World's Most Critical Shipping Lane Becomes Europe's Energy Problem

The liquefied natural gas trade operates on a fundamentally different logic than the pipeline networks it has replaced across much of Europe. Pipeline gas flows continuously, governed by bilateral contracts and fixed infrastructure. LNG, by contrast, moves in discrete parcels aboard specialised vessels navigating chokepoints, competing with buyers on multiple continents, and responding to spot price signals in real time. That architectural difference matters enormously when a single maritime corridor comes under sustained pressure — and it sits at the heart of the current crisis involving European gas storage and Strait of Hormuz disruptions.

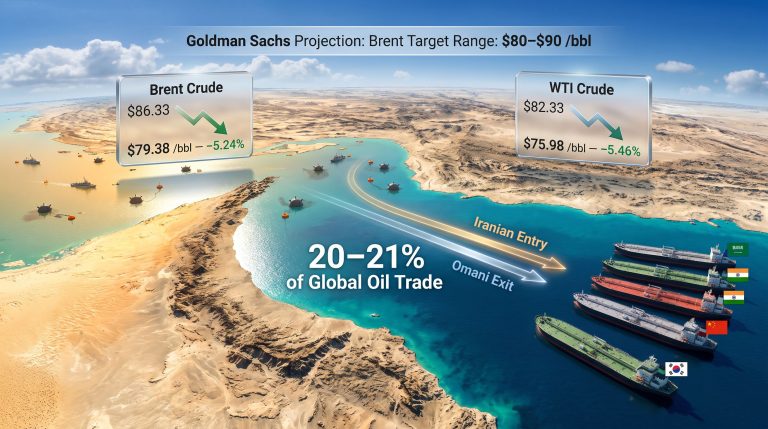

The Strait of Hormuz handles roughly one-fifth of global LNG supply, with Qatar alone accounting for a disproportionate share of seaborne gas exports flowing toward European terminals. When disruptions to this passage intensify, the consequences do not remain contained in the Persian Gulf. They propagate through global cargo markets, landing squarely on the balance sheets of European storage operators who are already operating from a historically weak baseline in 2026.

When big ASX news breaks, our subscribers know first

Why Europe's Gas Storage Position Is So Vulnerable Right Now

The Numbers Behind the Shortfall

European gas storage entered the 2026 summer injection season in a state that energy market analysts would describe, without exaggeration, as precarious. Following an exceptionally demanding winter that drew down reserves at an accelerated pace, storage hubs across the continent were left at levels not seen in nearly a decade.

The country-level data illustrates just how uneven the depletion was across major markets:

| Country | Storage Level (End of Winter 2026) | Seasonal Norm | Gap to Norm |

|---|---|---|---|

| Netherlands | ~5.8% | ~25-30% | ~20+ percentage points |

| Germany | ~20% | ~35-40% | ~15-20 percentage points |

| France | ~27% | ~35-40% | ~8-13 percentage points |

| EU Average | 28-35% | ~50% | ~15-22 percentage points |

Dutch reserves were particularly striking. The Netherlands, home to the TTF hub that serves as the European gas price benchmark, saw storage plunge to just 5.8% of capacity by the end of winter — the lowest reading in a decade. Northwest Europe as a whole saw storage drop below 30%, roughly double the EU-wide storage deficit, driven by a combination of peak household heating demand and a simultaneous spike in industrial power consumption.

As of mid-2026, the EU-wide figure has recovered to approximately 35–37% of capacity, but this remains substantially below the 50% seasonal norm typically observed by this point in the year. The mathematical task ahead is formidable: EU regulations require member states to achieve storage fill rates of between 80% and 90% of maximum capacity before the winter heating season begins. That gap cannot be closed through optimism alone.

According to research from Columbia University's Center on Global Energy Policy, Europe's gas storage entered the 2026 injection season at approximately 31 billion cubic metres, representing the lowest starting point since 2018.

Furthermore, European gas prices have been responding sharply to the tightening supply picture, compounding the financial pressure on storage operators attempting to rebuild inventories at pace.

The Backwardation Problem: When Market Structure Works Against Replenishment

One of the least-discussed but most consequential dynamics driving the current storage crisis is a breakdown in the seasonal price structure that normally incentivises injection. Under standard market conditions, summer gas prices trade below winter forward contracts, creating a profitable arbitrage window for storage operators: buy cheap in summer, sell dear in winter.

That mechanism has inverted in 2026. Dutch TTF seasonal spreads have moved into backwardation by approximately €1.3 per MWh, meaning summer spot prices are actually higher than winter forward contracts. This unusual configuration removes the financial rationale for voluntary injection, since operators purchasing gas at elevated summer spot prices and selling into cheaper winter forwards would crystallise a loss on every unit stored.

The backwardation has been driven by a convergence of forces:

- Near-term supply tightness linked to Hormuz disruptions and Qatari infrastructure constraints

- Expectations of new global LNG capacity entering service later in the year, suppressing winter forward prices

- The simultaneous phase-out of Russian LNG supply, which has compressed the pool of available spot cargoes

- Robust Asian demand competing for the same global cargo pool that Europe requires for storage replenishment

This is a structurally important dynamic that receives insufficient attention in mainstream coverage. The inverted curve does not merely make storage more expensive — it actively suppresses the volume of gas being injected at a moment when injection rates need to be running at maximum pace. Monitoring natural gas price trends closely remains essential for understanding how this backwardation is likely to evolve.

How Strait of Hormuz Disruptions Transmit Into European Gas Markets

The Three-Channel Transmission Mechanism

The relationship between European gas storage and Strait of Hormuz disruptions is not direct but operates through three interconnected market channels:

- Direct cargo reduction — Qatari LNG shipments destined for European regasification terminals face delays, rerouting costs, or outright cancellation when Hormuz transit is disrupted, tightening available supply

- Global competition intensification — Asian buyers in Japan, South Korea, China, and India compete aggressively for alternative spot cargoes, driving up prices and outbidding European procurement desks for scarce volumes

- Shipping cost escalation — War-risk insurance premiums surge for vessels transiting or operating near the affected zone, while rerouting around the Arabian Peninsula adds significant per-voyage fuel costs that ultimately inflate the landed price of gas at European terminals

Japan's crude imports from the Middle East have already fallen to record lows amid the disruption, a development that signals the scale of trade disruption rippling through Asian energy markets simultaneously with Europe's storage crisis. When Tokyo and Berlin are competing for the same pool of alternative LNG cargoes, European buyers face a structurally disadvantaged position given the physical distance from key Atlantic basin supply sources. The IEEFA analysis on Hormuz disruption risks estimates that a sustained closure could jeopardise up to 10% of Europe's LNG imports — a figure that makes the scale of the problem concrete.

The Equinor Assessment and What €90/MWh Means in Practice

Norwegian energy company Equinor, one of Europe's largest gas suppliers, has modelled the likely outcomes under two distinct disruption scenarios. The divergence between those scenarios is stark:

- Rapid resolution pathway: If Hormuz transit normalises within a matter of weeks, European storage could potentially reach approximately 75% capacity by the end of the injection season — below the EU's 80–90% target but potentially manageable with coordinated demand-side measures

- Prolonged disruption pathway (1–3 months): An extended blockage creates a critically different outcome, with Dutch TTF benchmark prices potentially climbing toward €90 per megawatt-hour and triggering a cascade of economic consequences across European industry

The projected demand response to a TTF spike toward €90/MWh is estimated at approximately 10 billion cubic metres of gas-to-power demand reduction through industrial fuel switching and power generation substitution. That scale of demand destruction carries substantial economic cost across energy-intensive manufacturing sectors.

The sectors most immediately exposed to this demand destruction cascade include chemicals, fertiliser production, ceramics, glass manufacturing, and metals processing — industries where gas is not merely a fuel source but a direct input into production processes. Switching to alternative energy sources mid-production cycle carries both technical and financial costs that persist well beyond the immediate price spike.

How Italy and Germany Are Responding to the Storage Challenge

Divergent Policy Philosophies, Shared Regulatory Obligations

The policy responses emerging at national level reveal fundamentally different philosophical approaches to the same underlying problem, despite both countries being bound by the same EU-level storage targets.

Italy's market compensation model:

Italian energy regulator ARERA and transmission system operator Snam have implemented auction-based financial compensation schemes specifically designed to overcome the backwardation problem. Under this structure, traders participate in storage injection auctions where the market manager pays the difference between elevated summer spot prices and lower winter forward prices at Italy's Virtual Trading Point (PSV). By effectively subsidising the spread, the mechanism restores the economic incentive to inject gas even when the seasonal price curve would otherwise make injection loss-making.

Germany's regulatory mandate model:

Germany has historically avoided direct state subsidies for storage injection, preferring to rely on statutory obligations backed by regulatory enforcement. The Bundesnetzagentur enforces strict filling targets, with shippers and network users legally obligated to meet specific inventory levels. Trading Hub Europe GmbH (THE) manages the financial instruments associated with strategic reserve maintenance, recovering costs through a storage neutrality charge applied to exit flows and network points.

| Policy Dimension | Italy | Germany |

|---|---|---|

| Primary mechanism | Financial auction compensation | Regulatory mandate |

| Market intervention style | Direct subsidy of seasonal spread | Legal obligation on shippers |

| Price signal approach | Corrects inverted curve artificially | Works within market structure |

| Cost recovery | Market manager absorbs spread | Neutrality charge on network exits |

| EU target alignment | Both targeting 80–90% fill | Both targeting 80–90% fill |

How 2026 Compares to Europe's 2022 Energy Emergency

Similar Vulnerability, Different Architecture

The 2022 energy crisis, triggered by the collapse of Russian pipeline gas flows following the invasion of Ukraine, has become the reference point against which all subsequent European gas disruptions are measured. However, the 2026 situation differs in ways that matter for how it will ultimately unfold.

| Dimension | 2022 Crisis | 2026 Crisis |

|---|---|---|

| Primary trigger | Russian pipeline cutoff | Strait of Hormuz LNG disruption |

| Storage entry point | Depleted, then rapidly refilled | Lowest since 2018 |

| LNG availability | Abundant (record U.S. exports) | Constrained (Qatar disruptions) |

| Price mechanism | Extreme spot spikes | Inverted seasonal curve plus spot pressure |

| Policy precedent | Limited | Strong (2022 playbook exists) |

One meaningful indicator of Europe's improved institutional resilience is Germany's advancement of the Uniper privatisation process. The utility recorded a net loss of approximately €40 billion in 2022 following the abrupt termination of Gazprom supply arrangements. Since then, Uniper has recovered financially through arbitration awards and has already begun repaying government aid.

Under European Commission state aid rules governing the 2022 rescue, Germany is legally required to reduce its shareholding to a maximum of 25% plus one share by the end of 2028. Headquartered in Düsseldorf, Uniper operates as one of Germany's largest gas importers and a central player in the continent's gas trading and storage infrastructure, making it a compelling asset for private market participants. The GECF analysis on global LNG disruption further underlines how these structural vulnerabilities threaten to undermine EU storage resilience precisely when it is most needed.

Three Scenarios for European Gas Markets Through Winter 2026

What Each Pathway Means for Energy Security

Scenario A: Rapid Hormuz Normalisation

Disruptions resolve within four to six weeks. Qatari LNG flows partially resume. European storage reaches approximately 75% by October. TTF remains elevated but well below the €90/MWh threshold. Demand-side conservation and fuel-switching measures bridge the remaining gap. Winter passes under measurable stress but without systemic shortfalls.

Scenario B: Moderate Disruption (3-Month Blockage)

Hormuz transit remains restricted through August. Global LNG spot prices spike sharply. European storage reaches 60–65% by October. TTF approaches or exceeds €90/MWh. Industrial demand destruction of 8–12 billion cubic metres occurs. Winter supply security becomes heavily weather-dependent.

Scenario C: Extended Disruption with Cold Winter Conditions

Disruption extends beyond three months and coincides with below-average temperatures. Storage enters the heating season below 60%. Emergency demand measures are activated. Mandatory industrial curtailments become operative in the most exposed markets. Significant contraction in energy-intensive industrial output follows.

The next major ASX story will hit our subscribers first

The Structural Lesson: LNG Dependency and the New Geography of Energy Risk

Europe Has Traded One Chokepoint for Another

When Russia's pipeline volumes effectively ceased following 2022, European policymakers celebrated the continent's diversification away from a single dominant supplier. That narrative was partly justified. However, the pivot toward LNG as the primary balancing mechanism has introduced a different category of geopolitical exposure rather than eliminating it entirely.

The Strait of Hormuz now occupies a structural role in European energy security that the Nord Stream pipeline network once held. The critical difference is that maritime chokepoints are subject to more unpredictable geopolitical pressures than bilateral pipeline agreements, and unlike fixed infrastructure, they cannot be bypassed through political negotiation alone.

A less widely appreciated dimension of this vulnerability involves the asymmetry of LNG market information. Unlike pipeline flows that are metered and reported continuously, LNG cargo routing decisions are made by commercial operators responding to real-time price signals across multiple markets simultaneously. This means European storage operators often lack visibility into how many cargoes are actually bound for their terminals versus being diverted toward higher-bidding Asian buyers until vessels are already en route.

The structural policy responses that could address this vulnerability over the medium term include:

- Developing EU-level strategic LNG reserve frameworks analogous to the strategic petroleum reserve model used for crude oil

- Embedding demand flexibility clauses into large industrial gas contracts to enable rapid response without mandatory curtailment

- Further diversifying LNG import sources beyond Qatar toward U.S., Australian, and East African supply chains

- Accelerating investment in renewable energy solutions and demand-side flexibility infrastructure, including heat pumps and industrial electrification, to reduce winter gas dependence structurally

The only genuinely durable solution to Hormuz exposure is reducing the volume of LNG Europe needs to import during peak demand periods. That requires an energy transition timeline measured in years rather than months — well beyond the window of the current crisis.

The 2026 storage situation is not yet a catastrophe. However, it sits uncomfortably close to the threshold where a single additional shock — a colder-than-average winter, a further escalation in Middle Eastern shipping disruptions, or a significant industrial supply outage in a major exporting nation — could convert a managed difficulty into a genuine crisis. The intersection of European gas storage and Strait of Hormuz disruptions has created a risk environment where the margin for error is exceptionally thin.

This article is intended for informational and educational purposes only and does not constitute investment advice. Scenario projections and price forecasts referenced herein are drawn from analyst modelling and carry inherent uncertainty. Readers should conduct independent research before making any investment or energy procurement decisions.

Want To Stay Ahead Of The Market Moves Driving Energy And Commodities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including those tied to the commodities at the centre of global energy disruptions — instantly translating complex data into actionable opportunities for both traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.