June 17, 2026

Understanding European Gasoil Market Mechanics

The architecture of energy commodity markets reveals itself most clearly during periods of structural tension. European gasoil futures represent a sophisticated pricing mechanism where physical supply constraints, regulatory shifts, and seasonal consumption patterns converge to create distinct market conditions. When analysing ice gasoil futures backwardation, the interplay between immediate supply availability and forward delivery expectations becomes particularly pronounced.

Storage economics fundamentally drive futures curve formation. The relationship between carrying costs, convenience yield, and inventory management creates the foundation for understanding why prompt month contracts occasionally trade at premiums to deferred deliveries. This backwardation structure signals market participants' willingness to pay elevated prices for immediate physical availability rather than accepting future delivery at lower costs.

When big ASX news breaks, our subscribers know first

What Drives Backwardation in European Gasoil Markets?

Fundamental Market Structure Mechanics

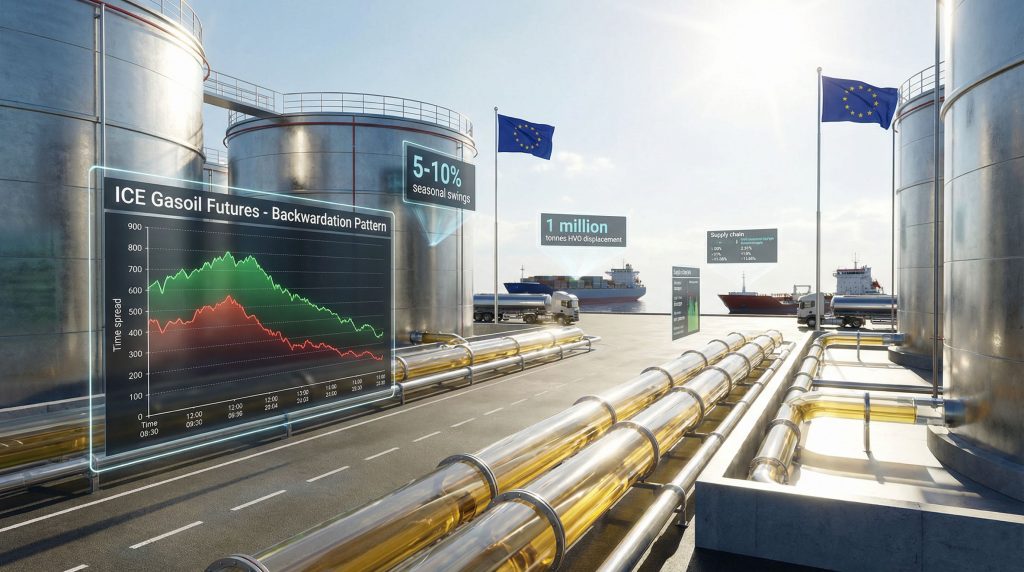

Backwardation occurs when near-term futures contracts trade above longer-dated contracts, creating an inverted price curve that contradicts normal storage economics. In European gasoil markets, this phenomenon reflects immediate supply-demand imbalances that override theoretical carrying cost calculations.

The January 2026 market conditions demonstrate these mechanics clearly. ICE January gasoil futures settled at $601/t on January 8, 2026, representing the lowest front-month settlement since May 30, 2025. Simultaneously, the January-February time spread compressed to just 50¢/t backwardation, marking the narrowest structure since May 9, 2025.

| Market Indicator | Current Level | Historical Context |

|---|---|---|

| Front-month settlement | $601/t | Lowest since May 30, 2025 |

| Jan-Feb time spread | 50¢/t backwardation | Narrowest since May 9, 2025 |

| ARA inventory levels | 4.5-month low | Week ending Dec 31, 2025 |

Time-spread compression patterns reveal market psychology shifts. The dramatic narrowing from mid-November 2025 peaks indicates fundamental supply-demand rebalancing despite persistent inventory constraints. Furthermore, this compression suggests market participants prioritise demand-side factors over supply-side concerns during seasonal transition periods.

Supply Chain Bottlenecks and Import Flow Dynamics

European gasoil import dependency creates vulnerability to supply disruption patterns that manifest in futures curve structures. The continent's reliance on seaborne imports means delivery timing variations significantly impact prompt month pricing relative to forward contracts.

Recent supply recovery patterns illustrate this dynamic. Following mid-November 2025 supply tightness caused by reduced waterborne volumes and sanctions-related disruptions, European import levels recovered substantially. This recovery contributed directly to the subsequent curve flattening observed through December 2025 and early January 2026.

ARA hub inventory management reflects these import flow variations. Independent diesel and gasoil stocks reached a 4.5-month low during the week ending December 31, 2025, despite improved import levels. However, this apparent contradiction highlights the complex relationship between arrival patterns, consumption rates, and storage operator behaviour during backwardation periods.

Key supply chain factors affecting curve structure include:

• Shipping route optimisation influences delivery timing and cost structures

• Terminal capacity utilisation at ARA facilities affects inventory accumulation

• Quality specification requirements for ICE Low Sulphur Gasoil delivery

• Blending operations necessary to meet contract specifications

How Do Seasonal Demand Patterns Shape Futures Curves?

European Diesel Consumption Cyclicality

Statistical analysis reveals consistent seasonal patterns in European diesel consumption that directly influence futures curve formation. EU diesel deliveries in January and February 2025 were approximately 5% below December 2024 levels and almost 10% lower than any non-winter months in 2024, according to Eurostat data.

This seasonality creates predictable pressure on ice gasoil futures backwardation structures during winter months. January and February consistently represent the weakest months for European road fuel consumption, establishing a structural demand trough that affects forward curve pricing relationships.

The seasonal pattern breakdown demonstrates:

• Winter months (Jan-Feb): 5-10% below annual average consumption

• Spring recovery (Mar-Apr): Gradual demand normalisation

• Summer peak (Jun-Aug): Highest consumption periods

• Autumn transition (Sep-Nov): Moderate demand levels before winter decline

Regional demand distribution varies significantly across EU member states, with northern European countries showing more pronounced seasonal variations due to heating fuel requirements. Moreover, industrial demand patterns overlay transportation fuel consumption, creating complex seasonal interactions that influence time-spread relationships.

Policy-Driven Structural Demand Shifts

The implementation of RED III represents a fundamental shift in European diesel demand dynamics that extends beyond traditional seasonal patterns. Germany's adoption of the EU's Renewable Energies Directive in 2026 adjusts greenhouse gas reduction quotas whilst abolishing double counting of advanced fuels.

Market estimates suggest at least 1 million tonnes of fossil road fuel demand will be substituted by hydrotreated vegetable oil (HVO) in Germany during 2026, with the majority affecting diesel consumption. This structural displacement creates permanent demand reduction factors that compound seasonal weakness periods.

The elimination of double counting for advanced fuels fundamentally changes compliance economics for refineries, requiring increased actual biofuel blending volumes rather than relying on counting methodologies.

RED III implementation mechanics include:

- Adjusted GHG reduction quotas requiring higher biofuel content

- Elimination of double counting for advanced biofuels

- Increased blending requirements for refineries

- Compliance cost adjustments affecting operational economics

This policy framework creates lasting structural changes in European gasoil demand fundamentals, potentially maintaining pressure on forward curve structures even during traditional demand recovery periods.

What Technical Factors Influence Time-Spread Compression?

Futures Contract Specifications and Delivery Mechanisms

ICE Low Sulphur Gasoil futures contracts enable physical delivery at Amsterdam-Rotterdam-Antwerp terminals, creating direct linkage between paper markets and physical supply conditions. Contract specifications require maximum 10ppm sulphur content, establishing quality parameters that affect delivery economics and arbitrage opportunities.

The compression of January-February time spreads to 50¢/t reflects technical market factors beyond fundamental supply-demand calculations. Settlement methodology incorporates physical delivery capabilities, meaning contract holders must consider actual logistics costs and quality specifications when evaluating time-spread trading opportunities.

Physical delivery procedures at ARA terminals include:

• Quality verification requirements for sulphur content and other specifications

• Terminal scheduling coordination for delivery timing

• Documentation procedures for title transfer and settlement

• Blending capabilities to meet contract quality standards

Market Microstructure and Trading Dynamics

Liquidity patterns between front-month and second-month contracts influence time-spread formation during market transitions. The compressed backwardation structure in early 2026 reflects reduced speculative interest in calendar spread strategies as storage economics became less favourable.

Commercial hedging patterns from refiners and distributors adapt to changing curve structures. During periods of compressed time spreads, refineries may adjust production scheduling to optimise inventory carrying costs whilst maintaining operational flexibility for unexpected demand variations.

Trading dynamics affecting curve formation:

• Algorithmic trading strategies responding to technical indicators

• Commercial hedging requirements from physical market participants

• Speculative positioning based on geopolitical and fundamental factors

• Market maker activity providing liquidity across contract months

How Do Geopolitical Events Override Fundamental Pricing?

Sanctions Impact Assessment

The scheduled implementation of EU sanctions on January 21, 2026, creates significant uncertainty for European gasoil supply chains. These sanctions will remove Indian and Turkish diesel refined from Russian crude from the European market, potentially affecting supply availability despite current inventory constraints.

Market participants exhibit a disconnect between geopolitical concerns and immediate pricing actions. Despite approaching sanctions and low ARA inventory levels, the time-spread compression suggests trader priorities focus on demand-side factors rather than supply-side risks. This disconnect mirrors broader patterns observed in oil price rally analysis where geopolitical events create temporary market disruptions.

Historical sanctions impact analysis reveals:

| Timeline | Event | Market Response |

|---|---|---|

| Mid-Nov 2025 | Peak supply disruption concerns | Maximum backwardation levels |

| Dec 2025 | Import recovery | Gradual curve flattening |

| Jan 8, 2026 | Pre-sanctions positioning | Continued compression |

| Jan 21, 2026 | Sanctions implementation | Unknown impact |

Price Discovery Inefficiencies

European traders report persistent disconnects between diesel prices and underlying fundamentals throughout early 2026. Market movements appear driven primarily by geopolitical news and sentiment rather than physical supply-demand analysis.

This price-fundamental disconnect manifests in the paradoxical narrowing of time spreads despite:

• ARA inventories at 4.5-month lows

• Impending January 21 sanctions

• Traditional seasonal supply tightness

• Reduced import volumes from sanctioned sources

Risk premium incorporation varies significantly during geopolitical uncertainty periods. Market participants appear to discount longer-term supply concerns in favour of immediate seasonal demand patterns, suggesting short-term trading horizons dominate price discovery mechanisms.

What Are the Operational Implications for Market Participants?

Refinery Optimisation Strategies

The combination of seasonally weak demand and policy-driven structural reductions requires refineries to fundamentally reassess production planning strategies. Traditional seasonal adjustments must now accommodate permanent demand displacement from biofuel substitution programmes.

Production scheduling considerations include:

• Inventory management during compressed backwardation periods

• Export market development to offset domestic demand reductions

• Blending optimisation to meet new biofuel content requirements

• Operational flexibility for unexpected geopolitical supply disruptions

Crack spread relationships change significantly during backwardation periods. Refineries must evaluate processing margins against storage costs and demand timing to optimise production run rates and inventory positions. In addition, the broader context of declining US oil production affects global refinery planning strategies.

Trading and Risk Management Applications

Compressed time spreads create specific challenges and opportunities for market participants. Storage operators face negative carry economics when backwardation premiums fail to compensate for carrying costs, whilst calendar spread traders identify potential value in curve normalisation scenarios.

Portfolio hedging effectiveness requires adjustment during flattened curve periods:

- Basis risk management becomes more complex with reduced time-spread volatility

- Storage arbitrage opportunities diminish with compressed premiums

- Forward hedging strategies must account for potential curve steepening

- Physical delivery risks increase during geopolitical uncertainty

The current 50¢/t backwardation provides insufficient compensation for typical storage costs, insurance, and capital expenses, explaining the preference for immediate consumption over inventory building despite tight supply indicators.

The next major ASX story will hit our subscribers first

How Do Storage Economics Affect Curve Structure?

ARA Terminal Capacity and Utilisation

Amsterdam-Rotterdam-Antwerp hub facilities represent Europe's primary petroleum product storage and distribution centre. Terminal capacity utilisation, booking patterns, and throughput capabilities directly influence arbitrage opportunities and subsequent curve structure formation.

The 4.5-month low in independent diesel and gasoil stocks despite improved import levels highlights complex storage operator decision-making during backwardation periods. Storage economics favour immediate sales rather than inventory accumulation when carrying costs exceed time-spread premiums.

Storage decision factors include:

• Terminal rental rates and capacity availability

• Insurance and handling costs for inventory management

• Opportunity costs of capital tied up in stored products

• Contract flexibility for delivery timing adjustments

Financial Storage Calculations

In backwardation markets, storage operators face negative carry situations where near-term prices exceed forward prices by margins insufficient to cover total carrying costs. The current 50¢/t premium fails to justify storage economics under normal cost structures.

Comprehensive carrying cost analysis incorporates:

| Cost Component | Typical Range | Impact on Storage Decision |

|---|---|---|

| Storage fees | $2-5/t/month | Primary fixed cost |

| Insurance | $0.5-1/t/month | Risk management expense |

| Interest/financing | Variable rate | Capital opportunity cost |

| Handling/logistics | $1-3/t | Operational expenses |

Contango threshold calculations demonstrate that profitable storage typically requires forward premiums exceeding $8-12/t depending on storage duration and specific cost structures. Current backwardation levels fall significantly below these thresholds, explaining low inventory accumulation despite tight supply fundamentals.

What Forward-Looking Indicators Signal Curve Evolution?

Leading Economic Indicators

European industrial production forecasts provide crucial insights into future gasoil demand patterns. Manufacturing activity correlates strongly with diesel consumption for transportation and industrial processes, creating predictive value for curve structure evolution.

Near-term catalysts affecting market structure include:

• January 21, 2026 sanctions implementation on Russian crude-derived products

• Seasonal demand recovery expected in March based on historical patterns

• RED III compliance deadlines across additional EU member states

• Industrial production trends influencing transportation fuel requirements

The combination of seasonal demand recovery and supply constraint implementation could create conditions for renewed time-spread expansion if inventory rebuilding fails to keep pace with consumption normalisation. Furthermore, tariffs global market impact considerations affect long-term supply chain planning.

Technical Analysis and Pattern Recognition

Historical backwardation duration analysis reveals typical patterns lasting 2-4 months before curve normalisation. The current eight-month low in backwardation represents significant deviation from mid-November 2025 peaks, suggesting potential for structure adjustment.

Pattern recognition elements include:

- Seasonal curve shape normalisation typically beginning in March

- Volatility surface evolution during structure transitions

- Volume patterns indicating commercial versus speculative positioning

- Cross-market correlations with crude oil and other energy futures

Options market implied volatility signals provide forward-looking indicators of expected curve movement. Current volatility levels suggest market participants anticipate continued structural adjustment rather than dramatic curve steepening.

Comparative Analysis with Other Energy Futures Markets

Cross-Commodity Curve Relationships

Brent crude time-spread relationships often provide leading indicators for refined product curve movements. The correlation between crude oil and gasoil backwardation structures reflects integrated supply chain dynamics and shared geopolitical sensitivities.

Regional comparison factors include:

• US heating oil futures structures during similar seasonal periods

• Asian gasoil markets integration with European pricing

• Natural gas seasonal patterns in European energy markets

• Currency hedging impacts on trans-Atlantic arbitrage flows

Natural gas trends in Europe demonstrate more pronounced winter-summer variations compared to gasoil, reflecting heating demand concentration. These patterns provide context for understanding relative energy commodity seasonality impacts on curve structures.

Global Gasoil Market Integration

Trans-Atlantic arbitrage economics influence European curve formation through import competition and export opportunities. Regional price differentials create arbitrage flows that affect local supply-demand balances and subsequent time-spread relationships.

Arbitrage flow considerations encompass:

• Freight rate volatility affecting arbitrage economics

• Quality specification differences between regional markets

• Regulatory compliance costs for international shipments

• Currency hedging requirements for cross-border transactions

The integration of global gasoil markets means European curve structures cannot be analysed in isolation from broader international supply-demand dynamics and competitive positioning factors. Consequently, patterns observed in oil price trade war dynamics influence regional market structures.

Market Structure Analysis Through External Perspectives

Industry analysis from Argus Media demonstrates how ICE gasoil futures and backwardation patterns align with broader commodity market trends. Their research highlights the significance of eight-month lows in current market conditions.

Furthermore, insights from diesel market strength analysis reveal persistent tightness concerns despite apparent supply recovery. These external perspectives provide valuable context for understanding ice gasoil futures backwardation within broader global energy market dynamics.

This analysis incorporates market data and insights to provide educational perspective on European gasoil futures dynamics. Market conditions remain subject to rapid change based on geopolitical developments, regulatory implementations, and fundamental supply-demand shifts. Readers should conduct independent research before making trading or investment decisions.

Looking to Capitalise on Energy Commodity Market Movements?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including energy and precious metals sectors that often correlate with broader commodity market dynamics. Subscribers gain immediate market advantages through actionable insights that transform complex mineral data into clear investment opportunities, positioning themselves ahead of market movements just like the sophisticated analysis required for European gasoil futures. Begin your 30-day free trial today and secure your competitive edge in commodity-focused investments.