July 10, 2026

The Crack Spread Realignment Reshaping European Refinery Decisions in 2026

Refinery economics have never operated in a straight line. Over multi-decade cycles, operators have repeatedly reconfigured their output strategies in response to sudden demand dislocations, geopolitical supply shocks, and evolving feedstock economics. What makes the current moment in European refining particularly instructive is not simply that margins have shifted, but that the direction of that shift runs counter to the dominant energy transition narrative. The European refinery economics shift back to road fuels in mid-2026 is a case study in how short-cycle pricing signals can override longer-term strategic planning, and why refinery yield flexibility remains one of the most underappreciated tools in the operator's arsenal.

When big ASX news breaks, our subscribers know first

The Structural Tension Defining European Refining Today

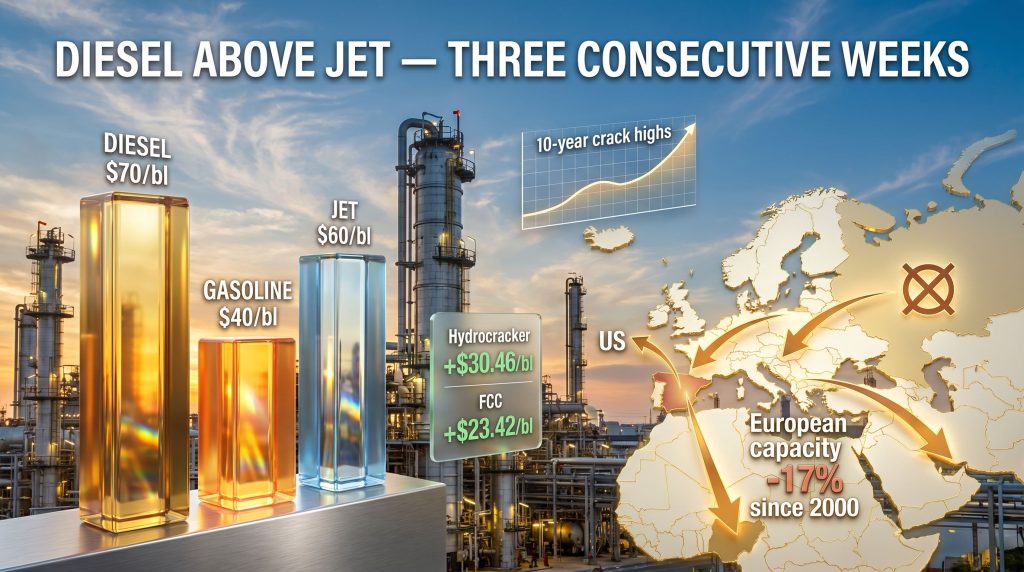

European refining has been contracting for over two decades. Since 2000, regional processing capacity has declined by approximately 17%, even as Asian refinery capacity has expanded by roughly 74% over the same period. The competitive disadvantage this creates is structural, not cyclical. Mega-complexes in the Middle East and Asia can process crude at significantly lower unit costs, and their product slates are generally better configured for export flexibility.

Yet capacity rationalisation in Europe has paradoxically created pockets of tightness in specific product segments at precisely the moments when demand signals are sharpest. The post-2022 sanctions period provided European refiners with a temporary reprieve from further closure decisions, as Russian product displacement created new market opportunities. That window, however, is narrowing. The fundamental competitive pressures have not gone away; they have simply been deferred.

Against this backdrop, the current crack spread realignment is best understood not as a reversal of energy transition progress, but as a rational economic response to a temporary though significant recalibration across the middle distillate complex. Furthermore, the energy transition trends shaping European policy continue to exert structural pressure on long-term operator planning. Operators are, consequently, doing what refinery economics have always demanded: following the margin.

Diesel at Three-Month Highs: What Is Driving the Surge?

Diesel crack spreads have recovered to approximately $70 per barrel as of early July 2026, reaching their highest level in three months after secondary unit margins were trading at outright discounts to crude in early June. The speed of that recovery, moving from sub-crude economics to a $30.46/bl premium for a typical hydrocracker configuration within roughly six weeks, has been exceptional by historical standards.

The primary supply-side catalyst was Russia's announcement on 8 July of a ban on diesel exports. Russia occupies the position of the world's second-largest diesel exporter, and its withdrawal from export markets represents a meaningful structural shock to global supply balances. The immediate consequence has been intensified competition for non-Russian cargoes, with Turkey and North African buyers who previously relied on Russian supply now competing directly in the same spot market as European buyers.

The United States has capacity to partially offset the European shortfall through increased diesel exports. However, the geographic pull is not exclusively toward Europe. Brazilian demand for US diesel cargoes creates a competing destination, limiting the volume practically available for European buyers and maintaining upward pressure on transatlantic freight economics.

Notably, diesel has now priced above jet fuel for three consecutive weeks as of early July 2026, the first sustained period this year in which the diesel-over-jet relationship has held. Market expectations suggest this pricing configuration will persist over the coming months, reinforcing the economic case for refinery yield reconfiguration. Understanding crude oil price trends in this context helps clarify why operators are responding with such urgency.

Gasoline Cracks at Four-Year Highs: A Demand-Side Story

While diesel's strength is largely supply-driven, the gasoline market's tightening tells a different story rooted in demand recovery and blending component scarcity. Gasoline crack spreads have reached approximately $40/bl, their highest level in four years, driven by a combination of regional consumption recovery and surging export demand.

Consumption has strengthened notably across the Mediterranean basin and in Germany, with traders citing a broad pickup in road fuel activity. Export demand from Europe's secondary markets has reinforced this trend, with shipments to Brazil, Canada, Egypt, Libya, and Syria all expected to increase sharply through July 2026. The collective signal is that demand is outrunning available supply across multiple buyer geographies simultaneously.

The blending component dynamic adds an additional layer of complexity. Refiners have ramped up blending activity in recent weeks, drawing down stocks of blending components in the process. Naphtha prices have responded by rallying to 10-year crack highs, supported simultaneously by gasoline blenders competing with petrochemical buyers for the same feedstock. This dual demand for naphtha from two distinct industrial segments represents a structural tightening of the gasoline production pool that is not easily or quickly resolved.

Jet Fuel's Relative Softening: Supply Normalisation in Motion

The contrast between road fuel and jet fuel fundamentals in mid-2026 is stark. Jet crack spreads have retreated to approximately $60/bl, down materially from peaks above $100/bl recorded between March and June 2026. That earlier jet fuel spike was driven by disruptions to Middle Eastern supply flows connected to the US-Iran conflict, which began in late February 2026. European refiners responded by materially increasing jet fuel output to capture those outsized margins.

The supply normalisation that followed has been swift. European jet fuel imports reached an eight-month high in June 2026, underpinned by record delivery volumes from the United States and Nigeria. Additional supply arriving from east of Suez, combined with increasing Chinese jet fuel export quotas, is expected to further ease regional balances in the weeks ahead.

The critical takeaway for refinery operators is that Europe's demonstrated ability to absorb the loss of Middle Eastern flows without a prolonged supply crisis has materially reduced the jet fuel risk premium. With the geopolitical supply disruption partially resolved through alternative sourcing channels, the rationale for maintaining elevated jet fuel production ratios has weakened considerably.

How Refineries Reconfigure Output: The Mechanics of Yield Shifting

Understanding how the European refinery economics shift back to road fuels translates into operational decisions requires familiarity with secondary processing unit mechanics. Not all refineries are equally flexible, but operators with hydrocrackers and fluid catalytic crackers (FCCs) have meaningful scope to redirect output between product pools.

| Unit Type | Primary Yield Configuration | Margin vs. ICE Brent (Early July 2026) | Margin vs. ICE Brent (Early June 2026) |

|---|---|---|---|

| Hydrocracker | 70% diesel / 30% gasoline | +$30.46/bl premium | Discount to crude |

| Fluid Catalytic Cracker (FCC) | 70% gasoline / 30% diesel | +$23.42/bl premium | Discount to crude |

The significance of these figures extends beyond the headline numbers. Both units moved from negative economics relative to crude to strong positive premiums within approximately six weeks. That kind of margin swing is a powerful operational trigger, particularly for operators who had previously justified elevated jet fuel production on economic grounds.

One of the less widely understood aspects of this yield shift involves the routing of heavier naphtha-grade material. During the period of elevated jet fuel margins, some refiners directed this material into the kerosine pool, and certain operators had been extracting larger kerosine fractions from petrochemical processing units to capture the jet crack premium. As diesel and gasoline economics now outperform, this heavier naphtha material is expected to return to the gasoline blending pool, effectively increasing the available blending component supply and contributing to gasoline output growth.

Spain's Repsol has already begun the operational pivot, scaling back the jet fuel production increases it implemented in the earlier part of 2026 and reorienting output toward diesel and gasoline. This represents one of the first publicly confirmed yield reconfiguration responses to the current crack spread environment, and broader industry follow-through is widely anticipated as the economic signals remain compelling. According to recent analysis by OPIS, European refineries have been under sustained pressure to reduce output, making the current margin recovery a particularly significant turning point.

The next major ASX story will hit our subscribers first

Geopolitical Context: The Supply Disruption Architecture of 2026

The current market configuration cannot be fully understood without appreciating the geopolitical architecture that produced it. The US-Iran conflict, which escalated in late February 2026, created a period of acute supply vulnerability for European jet fuel markets. Attacks on infrastructure and shipping across the Mideast Gulf disrupted Middle Eastern product flows at precisely the moment when European inventories were not positioned to absorb extended supply gaps.

The consequence was a jet crack spike of historic proportions, with margins exceeding $100/bl during the March to June period. European refiners responded rationally by boosting jet fuel output. The supply ecosystem then adapted through rerouting of US and Nigerian cargoes, and the crisis eased.

Russia's diesel export ban of 8 July introduces a different but equally significant supply disruption. Where the jet fuel shock was driven by an acute geopolitical event affecting transit routes, the diesel shock is driven by a deliberate policy decision that removes a structurally important exporter from global markets. In addition, the broader oil market disruption risks stemming from geopolitical tensions continue to amplify volatility across the entire refined product spectrum. The supply void created is more persistent in character, and the competition for alternative cargoes among European, Turkish, and North African buyers is expected to sustain elevated diesel crack spreads for several months.

The Risk That Refiners Must Not Ignore

The economics strongly favour a pivot toward road fuels. However, this reconfiguration carries a risk that deserves serious attention: the latent vulnerability in European jet fuel supply.

European jet fuel inventories remain significantly depleted following the supply disruptions of early 2026. Industry forecasts suggest that inventory rebuilding is unlikely to be completed before early 2027, meaning there is an extended window during which the European jet fuel market has minimal buffer capacity. If refinery operators collectively reduce jet fuel output in response to the current crack spread configuration, and any new supply disruption emerges before inventories are rebuilt, the market would face a structural exposure with limited ability to absorb the shock.

Key risk scenarios that warrant monitoring include:

- Further geopolitical escalation in the Mideast Gulf affecting shipping or infrastructure

- Unexpected refinery outage events reducing secondary unit throughput capacity

- OPEC's influence on oil production decisions altering crude quality and availability for European feedstock requirements

- Seasonal demand acceleration in jet fuel during the northern hemisphere summer travel peak

- Any reversal in Chinese export quota policy reducing the anticipated east-of-Suez supply increment

The jet fuel inventory depletion problem will not resolve itself quickly. Operators reconfiguring away from kerosine production are, in effect, making a calculated bet that the geopolitical environment remains stable enough for the supply normalisation trend to continue. That is not an unreasonable bet given current conditions, but it is a bet with meaningful asymmetric downside.

Long-Term Structural Trajectory: The Road Fuel Paradox

Despite the compelling near-term economics, European road fuel refining faces irreversible long-term structural headwinds. The tension between short-cycle crack spread signals and medium-term demand destruction trajectories is one of the defining strategic paradoxes confronting European refinery operators today.

On the demand side, EV fleet penetration continues to advance across key European markets. Euro 6/VI emissions standards and the Renewable Energy Directive II (RED II) biofuel blending mandates are progressively reshaping the composition of the road fuel pool. Research published by the European Climate Foundation highlights that over 1 million tonnes of German fossil fuel road demand is projected to migrate toward renewable substitutes by 2026, with the pace of substitution expected to accelerate beyond that horizon.

The strategic responses emerging across the European refinery landscape reflect this long-term reality:

- Dual-track operating models that maintain road fuel production economics in the near term while investing in low-carbon product stream optionality

- Partial asset conversion toward biofuels, sustainable aviation fuel (SAF), and circular economy feedstock processing

- Hydrogen integration at existing refinery sites as a long-term decarbonisation pathway

- Capacity rationalisation focused on retiring the least competitive units while maintaining flexibility in high-conversion secondary processing assets

The coexistence of a near-term road fuel margin premium with a medium-term demand erosion trajectory does not resolve itself neatly. Operators who reconfigure too aggressively toward diesel and gasoline today may find themselves having invested capital in optimising assets for a market that contracts meaningfully over the following decade. Those who hold back may leave significant near-term margin on the table.

Frequently Asked Questions: European Refinery Economics and Road Fuel Markets

Why are European refiners shifting back to diesel and gasoline production?

Diesel crack spreads reaching approximately $70/bl and gasoline cracks at approximately $40/bl have made road fuel production substantially more attractive than jet fuel output, which has retreated to around $60/bl. Russia's diesel export ban has amplified the supply-side signal by removing a major global exporter from the market.

What is a crack spread and why does it matter for refinery decisions?

A crack spread measures the margin a refiner earns between the cost of crude oil inputs and the value of refined product outputs. Tracking oil futures and Brent benchmarks alongside product values helps operators assess when diesel or gasoline crack spreads widen relative to competing products such as jet fuel. Operators then have a direct financial incentive to reconfigure yield ratios toward the higher-margin products using secondary processing unit flexibility.

How quickly can a refinery switch between jet fuel and diesel production?

The speed of the transition depends on unit configuration and feedstock characteristics. Operators with hydrocrackers and FCCs can typically redirect a portion of output between the kerosine and gasoil pools with relative operational flexibility, though the scale of the achievable shift is constrained by the specific design parameters of each facility.

What impact does Russia's diesel export ban have on European markets?

Russia's status as the world's second-largest diesel exporter means its export ban removes a significant volume from global supply, forcing European buyers to compete more aggressively for US, Middle Eastern, and other alternative cargoes. This intensified competition among multiple buyer regions is a key driver of the current diesel crack spread elevation.

Is the shift back to road fuels a sign that the energy transition is reversing?

The current shift reflects short-cycle economic rationality in response to temporary crack spread dynamics rather than a structural reversal of energy transition trajectories. EV adoption, regulatory mandates, and refinery repurposing investment continue to exert sustained downward pressure on European fossil road fuel demand over the medium and long term.

What happens to jet fuel supply if refiners cut output?

European jet fuel inventories remain at significantly depleted levels following the early 2026 supply disruptions. A sustained industry-wide reduction in refinery jet fuel output could leave the market poorly positioned to absorb any new supply disruption before inventories are rebuilt, a process not expected to complete until early 2027 at the earliest.

Strategic Outlook: Key Takeaways for Market Participants

The European refinery economics shift back to road fuels is a multi-layered phenomenon that resists simple characterisation. The table below summarises the key dimensions of the current market configuration:

| Dimension | Near-Term Signal | Medium-Term Outlook |

|---|---|---|

| Diesel crack spreads | ~$70/bl, three-month high | Sustained elevation expected; Russia ban persists |

| Gasoline crack spreads | ~$40/bl, four-year high | Dependent on export demand sustainability |

| Jet fuel crack spreads | ~$60/bl, retreating from >$100/bl peak | Further softening expected as supply normalises |

| Hydrocracker margins | +$30.46/bl vs. ICE Brent | Positive while road fuel cracks outperform |

| FCC margins | +$23.42/bl vs. ICE Brent | Positive while gasoline premium holds |

| Jet fuel inventory position | Heavily depleted | Rebuild not expected before early 2027 |

The current environment rewards operators with secondary processing flexibility, particularly those capable of reconfiguring between kerosine and gasoil pools at meaningful scale. Repsol's early operational pivot signals where the industry's yield configuration is likely to move over the coming months.

For market participants and industry observers, the period ahead will test whether the current crack spread configuration sustains long enough to justify the capital and operational decisions that refinery yield reconfiguration entails. What is certain is that the interplay between geopolitical supply shocks, seasonal demand patterns, and the long shadow of the energy transition will continue to generate the kind of rapid margin volatility that makes European refinery economics one of the most dynamic analytical domains in global commodity markets.

This article is intended for informational and analytical purposes only. It does not constitute financial, investment, or trading advice. Crack spread figures, margin data, and market projections referenced throughout are derived from industry sources and are subject to change. Readers should conduct their own due diligence before making any commercial or investment decisions based on the information presented.

Want to Capitalise on the Next Major Commodity Market Shift Before the Broader Market Catches On?

The same geopolitical supply shocks and crack spread dislocations reshaping European refinery economics in 2026 create ripple effects across ASX-listed energy and resources companies — and Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering actionable alerts the moment significant mineral and commodity discoveries are made public. Explore historic examples of major discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the market.