June 15, 2026

European steel mills are implementing unprecedented pricing strategies in 2026, with planned increases of €50-70 per tonne across long product categories marking a fundamental shift toward sustainable profitability. The tariff impact on markets and evolving regulatory landscape have created unique opportunities for margin expansion among domestic producers. Furthermore, the convergence of geopolitical tensions, environmental regulations, and infrastructure bottlenecks has reshaped competitive positioning across European long product markets, fundamentally altering the strategic landscape for both integrated mills and specialty processors.

This shift represents more than cyclical pricing adjustments. Industry participants are witnessing structural changes in procurement strategies, with buyers increasingly prioritising supply security over pure cost optimisation. The implications extend beyond immediate pricing decisions, affecting everything from inventory management protocols to long-term sourcing partnerships across the continental steel ecosystem.

Strategic Margin Recovery Through Disciplined Price Leadership

European steel mills are implementing coordinated pricing strategies that prioritise sustainable profitability over volume maximisation. Recent industry communications indicate planned price increases of €50-70 per tonne across long product categories, representing a strategic departure from traditional market share competition.

Industry sources emphasise that current pricing approaches reflect calculated responses to evolving cost structures rather than opportunistic market exploitation. Market participants have articulated that maintaining pricing discipline in the face of import competition is preferable to accepting orders at unsustainable price points.

Key Regional Price Movements:

- German rebar producers targeting €710/t delivered, representing a €50/t increase from recent trading levels

- Italian mills pursuing increases exceeding €50/t from current ex-works pricing around €650/t

- Cross-border offers from Italian producers reaching €670-680/t delivered in Polish markets

The strategic framework underlying these adjustments suggests that European mill management views the current competitive environment as an opportunity to establish sustainable price floors. This perspective represents a significant shift from volume-driven strategies that dominated the sector through 2025.

Mill Source Perspectives on Volume vs. Margin Trade-offs

Industry participants have emphasised that losing orders at higher price points creates superior long-term positioning compared to winning business at unsustainable levels. This philosophy reflects broader industry consolidation around margin discipline rather than market share maximisation.

Market acceptance timelines are anticipated to compress significantly by mid-May 2026, with inventory dynamics playing a crucial role in the transition period. While import inventories present temporary pricing headwinds, the heterogeneity of product specifications limits the effectiveness of import stocks as long-term pricing constraints.

When big ASX news breaks, our subscribers know first

Cost Structure Transformation Enabling Sustained Price Leadership

Multiple economic forces are converging to support European mills' pricing power, creating barriers to import competition while simultaneously justifying higher domestic price levels. Additionally, the impact of trade war supply chains has significantly altered global steel market dynamics.

Energy Market Disruptions and Cost Escalation

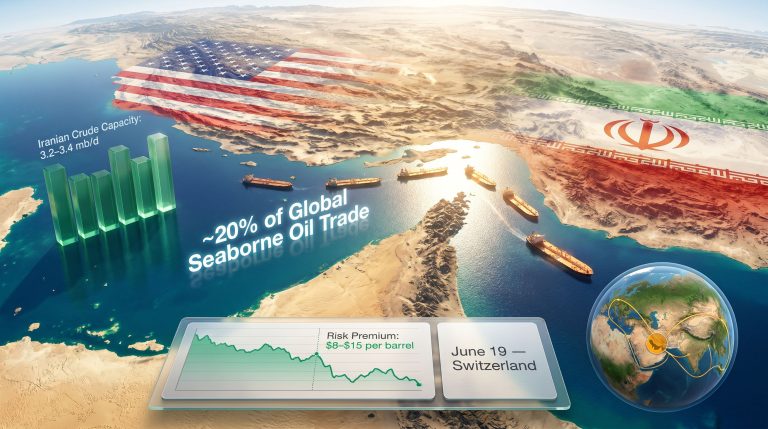

Geopolitical developments beginning in March 2026 have significantly impacted global energy supply chains, with particular effects on European industrial electricity and natural gas markets. The disruption of traditional shipping routes through the Strait of Hormuz has created cascading effects across energy commodity markets.

Ocean freight rate escalation has reached approximately $80/t for India-to-Europe shipments of 25,000-40,000 tonne volumes, compared to previous levels of $50-60/t. Alternative routing through Jeddah and Sohar ports has added €20-30/t in additional logistics costs for Asian suppliers.

Moreover, US natural gas forecasts indicate continued volatility in energy markets, which directly impacts steel production costs across European facilities.

Carbon Border Adjustment Mechanism Implementation Impact

The CBAM framework creates differential cost structures between domestic producers and import competitors, fundamentally altering competitive economics across steel product categories.

CBAM Implementation Timeline:

| Phase | Timeline | Cost Impact | Market Effect |

|---|---|---|---|

| Reporting Requirements | 2026 | Administrative burden | Importer compliance costs |

| Financial Obligations | 2027 | Estimated €25-35/t | Direct cost addition to imports |

| Full Implementation | 2028 | Potential €40-60/t | Substantial import cost disadvantage |

The mechanism operates through standardised import price calculations that account for embedded carbon costs not covered by equivalent EU ETS charges. Steel product coverage includes hot-rolled coil, rebar, wire rod, and merchant bars, directly affecting long product import economics.

EU Safeguard Modifications and Import Protection

Scheduled safeguard adjustments from July 2026 will reduce import allowances by an estimated 15-20% across key product categories. This regulatory tightening particularly affects hot-rolled coil import volumes and long products from Turkish and Asian suppliers.

The combination of CBAM costs and tightened quotas creates a dual-barrier system that progressively favours domestic production over import alternatives. However, global iron ore market impact continues to influence raw material costs for European producers.

Regional Market Segmentation and Acceptance Patterns

European long product markets demonstrate significant geographic variation in price acceptance capabilities, with Northern European buyers showing greater tolerance for price increases compared to Southern European counterparts.

Northern European Market Dynamics

German buyers demonstrate stronger willingness to absorb price increases, supported by robust construction activity and limited alternative supply sources. Project pipeline visibility provides buyers with confidence in demand continuation, making price increases more acceptable within procurement budgets.

The €710/t delivered target price for German rebar represents approximately 7.6% margin expansion from recent trading levels around €660/t, establishing a clear price leadership signal for the Northern European market.

Southern European Market Complexity

Italian markets present more complex dynamics with multiple pricing tiers simultaneously present. According to European steel industry reports, mills are signalling continued price pressure.

Italian Rebar Pricing Structure:

- Ex-works mill offers: €680/t

- Actual domestic traded prices: €650/t (indicating buyer resistance)

- Export market pricing: €670-680/t delivered to Poland

This multi-tier structure suggests differential market power across segments, with higher price realisation possible in export markets compared to domestic spot trading.

Wire Rod Market Vulnerabilities

Wire rod processors face unique challenges due to limited regulatory protection until 2028. The sector confronts potential margin compression from upstream price increases of €100-140/t over March-April without corresponding downstream protection mechanisms.

Cost-Price Squeeze Analysis:

- Upstream increases: €100-140/t wire rod price escalation

- Downstream protection: Minimal safeguard coverage for processed products

- Required pass-through rates: 60-70% to maintain processor viability

Processors are evaluating vertical integration opportunities to secure raw material access and margin stability, while exploring geographic diversification to access lower-cost production regions.

Strategic Risk Assessment and Market Response Scenarios

Aggressive pricing policies carry inherent risks related to demand destruction and competitive response patterns that could undermine long-term market positioning. Furthermore, commodities volatility and hedging strategies are becoming increasingly crucial for steel market participants.

Demand Destruction Thresholds

Substantial import inventories across European markets create 4-6 week pricing pressure windows where buyers can resist price increases. End-users may explore alternative materials or postpone projects if price escalation exceeds absorption capacity.

Interest-sensitive sectors including construction and automotive manufacturing present particular vulnerability to demand contraction if steel price increases compound broader cost pressures.

Asian Producer Adaptations

Import competitors are implementing strategic adaptations to maintain market access despite cost disadvantages:

Pricing Term Modifications:

- Shift from CFR to FOB pricing terms, transferring freight risk to buyers

- Route diversification through alternative ports adding €20-30/t logistics costs

- Production reallocation toward domestic and regional markets

These adaptations suggest that import competition will persist, albeit at reduced volume levels and altered economic terms.

Regulatory Framework Evolution and Market Structure Impact

The intersection of carbon regulations, trade protection measures, and supply chain localisation trends is creating a new competitive architecture for European steel markets.

CBAM Mechanism and Cost Transmission

Carbon border adjustments operate through detailed methodologies that calculate embedded emissions factors for specific steel products. The cost adjustment formula considers reference prices, embedded emissions, and ETS credit payments to determine import price modifications.

Technical Implementation Framework:

- Product coverage: Hot-rolled coil, rebar, wire rod, merchant bars

- Cost calculation: (Reference Price × Embedded Emissions Factor) – (ETS Credits Paid)

- Compliance requirements: Quarterly reporting and annual financial adjustments

Supply Chain Localisation as Strategic Response

European buyers are increasingly prioritising supply security over pure cost optimisation, representing a strategic shift from traditional procurement approaches. This transition supports domestic pricing power by reducing buyer sensitivity to price differentials.

The unpredictability of inventory depletion across product specifications creates additional supply security considerations that favour domestic sourcing relationships over spot import purchasing.

Wire Rod and Downstream Processing Sector Implications

The wire rod processing ecosystem faces distinctive challenges from regulatory asymmetries that create cost-price squeeze scenarios through 2028.

Regulatory Protection Gaps

Wire rod processors lack CBAM and safeguard protection until 2028, creating potential margin compression as upstream costs increase without corresponding downstream protection. This regulatory asymmetry could force significant industry restructuring.

Processor Response Strategies:

- Backward integration: Securing raw material access through mill ownership or long-term contracts

- Geographic optimisation: Relocating production to access lower-cost supply regions

- Customer segmentation: Focusing on high-value applications that can absorb cost increases

Investment Implications for Processing Industry

The combination of upstream price increases and limited downstream protection suggests consolidation opportunities within the processing sector. Companies with integrated supply chains or flexible geographic footprints will likely outperform pure processors dependent on spot market purchasing.

The next major ASX story will hit our subscribers first

Market Positioning Framework for Q2-Q3 2026

The convergence of regulatory changes, cost pressures, and supply chain disruptions requires strategic positioning adjustments across the steel value chain. Additionally, trading economics data suggests continued volatility in global steel commodity markets.

Procurement Strategy Optimisation

For Steel Buyers:

- Strategic inventory building: Establishing 6-8 week stock positions before full price implementation

- Contract restructuring: Negotiating flexible terms that accommodate price volatility

- Supplier diversification: Developing alternative sourcing channels including regional suppliers

- Material substitution: Evaluating alternative materials where technically feasible

For Steel Producers:

- Margin discipline: Prioritising sustainable pricing over market share gains

- Customer segmentation: Implementing differentiated pricing based on relationship value

- Cost structure optimisation: Accelerating efficiency improvements to support pricing power

- Market positioning: Establishing clear price leadership in key product segments

Investment and Risk Management Considerations

European steel sector consolidation is creating oligopolistic pricing dynamics that support margin recovery, though volume growth remains constrained by macroeconomic headwinds. The regulatory framework evolution through 2028 provides structural support for domestic producers while gradually reducing import competition.

Key Risk Factors:

- Potential demand destruction if price increases exceed end-market absorption capacity

- Competitive response from import suppliers through alternative routing and pricing terms

- Macroeconomic deterioration affecting construction and manufacturing demand

- Geopolitical developments impacting energy and logistics costs

Investment Opportunities:

- Domestic steel producers with integrated supply chains and efficient operations

- Wire rod processors with backward integration capabilities or flexible geographic positioning

- Supply chain technology providers supporting localisation and inventory optimisation

What's the Future Outlook for European Steel Mills Price Hikes?

The european steel mills price hikes represent more than cyclical market adjustment. They reflect structural transformation toward sustainable margin recovery supported by regulatory frameworks, supply chain localisation, and strategic industry consolidation. Market participants who adapt their strategies to this new competitive architecture while managing transitional risks will be positioned to capitalise on the evolving market structure through 2028 and beyond.

However, the sustainability of these price increases depends largely on demand resilience and the effectiveness of regulatory barriers in limiting import competition. Consequently, the steel industry must balance aggressive pricing strategies with maintaining market accessibility for key customer segments.

This analysis is based on market data available as of April 2026 and should not be considered investment advice. Steel market dynamics involve significant volatility and regulatory uncertainty that may affect actual outcomes.

Seeking Opportunities in Metals and Mining Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities in steel raw materials and mining sectors ahead of the broader market. Start your 14-day free trial today and gain the market-leading advantage needed to navigate evolving commodity landscapes with confidence.