June 23, 2026

The Hidden Architecture of a Supply Chain That Was Never Really Fixed

The narrative that the electric vehicle industry solved its cobalt problem has become one of the most consequential misconceptions in modern industrial strategy. EV cobalt supply disruptions were widely assumed to be neutralised when major automakers and battery manufacturers pivoted toward cobalt-free chemistries in the early 2020s. However, that conclusion was premature, and for a significant portion of the global EV fleet, it remains dangerously wrong.

Understanding why requires stepping back from headline adoption rates and examining the structural mechanics of how cobalt actually flows through the global economy — not just through visible trade routes, but through the far larger network of indirect dependencies that conventional supply chain analysis routinely misses.

When big ASX news breaks, our subscribers know first

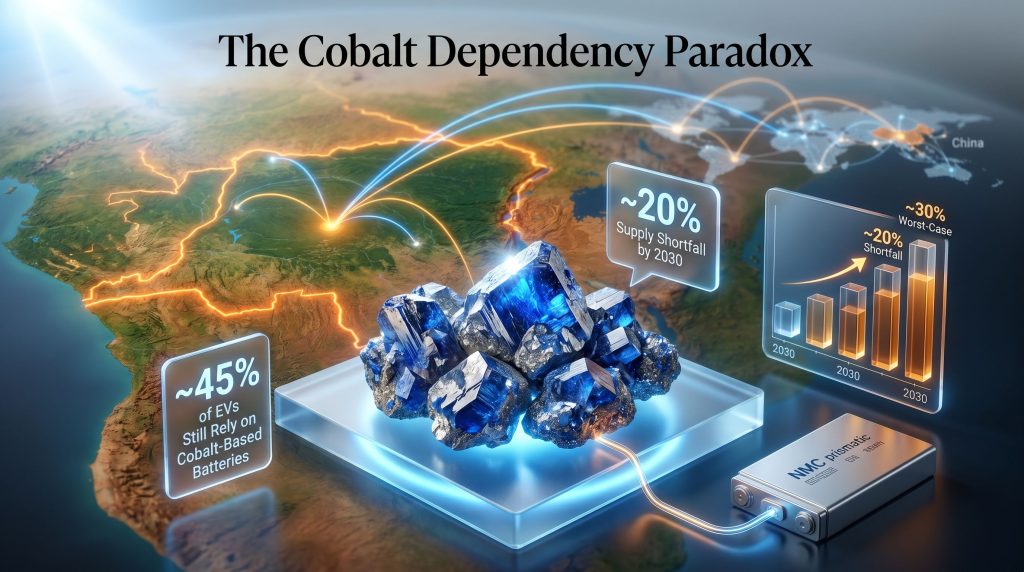

The 45% Problem: Why Cobalt Exposure Persists Across the EV Sector

Despite the high-profile adoption of Lithium Iron Phosphate batteries by manufacturers including Tesla and BYD, roughly 45% of electric vehicles produced today continue to rely on cobalt-intensive chemistries. These are primarily NMC (Lithium Nickel Manganese Cobalt) and NCA (Lithium Nickel Cobalt Aluminum) formulations, which retain a critical performance advantage: superior energy density.

For long-range passenger vehicles, premium EVs, and performance-oriented segments, that energy density gap is not merely a marketing consideration. It translates directly into vehicle range, charging cycle behaviour, and cold-weather performance. Until next-generation solid-state batteries reach commercial viability at scale, these segments remain structurally anchored to cobalt-bearing chemistries.

The widespread assumption that the EV sector has moved past cobalt dependency overlooks the roughly half of the market where LFP substitution is technically or commercially constrained. For those manufacturers, cobalt supply disruptions are not a theoretical tail risk — they are an active operational vulnerability.

This creates an asymmetric exposure profile across the industry. Budget and mid-range EV producers that have completed the LFP transition carry minimal cobalt risk. Furthermore, premium manufacturers, long-range platform developers, and aerospace-adjacent battery applications remain significantly exposed to both price volatility and physical supply constraints.

A Structural Risk Map: Geographic Concentration Across the Cobalt Value Chain

The cobalt supply chain is not merely concentrated — it is concentrated at every stage simultaneously, which is what distinguishes it from most other industrial commodities.

| Supply Chain Stage | Dominant Actor | Concentration Level | Disruption Risk |

|---|---|---|---|

| Raw Mining Output | Democratic Republic of Congo | 70–75% of global supply | Very High |

| Chemical Refining | China | ~72% of processing capacity | Critical |

| Downstream Battery Materials | China | Near-monopoly | Critical |

| Dedicated Cobalt Operations | Global | ~6% of total output | Low volume, high strategic value |

| Byproduct Mining (Copper/Nickel) | Multi-region | ~94% of total cobalt output | Indirect exposure |

The Byproduct Trap: Cobalt's Structural Vulnerability

One of the least understood features of the cobalt market is that it is not, in any meaningful sense, an independently functioning commodity market. Approximately 94% of global cobalt is extracted as a byproduct — roughly 50% from copper mining operations and 44% from nickel extraction. Only around 6% originates from dedicated cobalt mines.

This structural reality means that cobalt production volumes are not governed by EV battery demand. They are governed by the economics of copper and nickel markets. When copper prices surge, as they have during recent periods of infrastructure and electrification investment, DRC miners rationally redirect capital toward copper, deprioritising cobalt extraction even as battery demand climbs. Consequently, this dynamic has already played out in practice, with DRC operators documented pivoting toward copper output amid cobalt price underperformance.

The inverse is equally dangerous: a sustained collapse in copper or nickel prices would mechanically contract cobalt byproduct output, regardless of how robust EV demand remains. The lag between commodity price movement and cobalt supply response is typically measured in quarters to years, not weeks. Understanding the full picture of global cobalt production helps clarify just how structurally embedded these dependencies truly are.

Three Disruption Scenarios: What EV Cobalt Supply Shocks Actually Look Like

Scenario 1: DRC Instability and Export Restriction

The Katanga and Lualaba Copperbelt regions of the DRC have a well-documented history of labour actions, infrastructure failures, and abrupt regulatory shifts. Any combination of these factors applied to the 70–75% of global supply originating in this single jurisdiction creates an immediate upstream constraint.

Critically, the DRC government has shown increasing willingness to assert resource sovereignty. The DRC cobalt export ban and related licensing reviews have been used as policy instruments, and the ongoing pivot of DRC operators toward copper creates a scenario where cobalt output declines not through disruption but through deliberate commercial reallocation. The broader cobalt export ban impacts on prices and supply chains are already beginning to reverberate across the industry.

Scenario 2: Chinese Export Controls on Cobalt Processing

China's progressive use of critical mineral export controls has established a clear and increasingly well-documented strategic template. In 2024, China introduced restrictions covering gallium, germanium, and antimony — all materials with limited short-term substitution pathways. In April 2025, Beijing expanded these controls to encompass a broad range of rare earth elements.

Each tranche of restrictions has targeted materials that share a common profile: high strategic value to Western defence and technology industries, Chinese near-monopoly on processing capacity, and limited capacity for rapid supply diversification. Cobalt processing materials share every one of these characteristics.

A USGS analysis of China's cobalt battery material monopoly confirms that while China holds limited domestic cobalt reserves, it has systematically consolidated control over the global supply chain. Chinese state-affiliated entities currently own or finance approximately 15 of the 17 largest cobalt mining operations in the DRC, securing upstream feedstock flows that feed directly into Chinese industrial processing.

The timeline between a Chinese cobalt processing restriction announcement and downstream battery supply disruption at the OEM level is not measured in years. Existing stockpiles provide a buffer measured in months, after which procurement chains outside China face structural gaps that cannot be rapidly resolved.

Scenario 3: The Copper-Nickel Price Cascade

A sustained downturn in either copper or nickel markets triggers a cobalt supply contraction that operates entirely independently of EV demand signals. Because cobalt is extracted as a byproduct, falling base metal economics reduce the economic incentive to operate the mines from which cobalt is recovered.

For NMC-dependent EV manufacturers, this scenario is particularly insidious because it arrives not as a geopolitical event that triggers risk management protocols, but as a slow-moving supply squeeze that may not trigger alarm until inventory buffers are already depleted. The supply contraction lags the price decline by six to eighteen months in most historical cycles.

The Robust-Yet-Fragile Network: Why Standard Risk Models Underestimate Cobalt Exposure

Research published by the Chinese Society for Environmental Sciences introduces a framework for understanding cobalt supply chain vulnerability that diverges sharply from conventional trade risk assessments. The study characterises the global cobalt network as exhibiting a robust-yet-fragile architecture — one that can absorb numerous small, distributed shocks without systemic failure, but that collapses rapidly when disruption targets the critical nodes where concentration is highest.

Furthermore, the research team found that supply disruptions propagate through a network of potential failures approximately four times larger than the visible physical trade network itself. This means that manufacturers with no direct cobalt trade relationship with the DRC or China can still face severe downstream exposure through indirect supply chain dependencies.

The research identified specific categories of national exposure:

- High policy-driven disruption potential: China and the United States, where large production or refining bases mean that domestic policy decisions can generate global cascading effects.

- High dependency-driven vulnerability: South Africa, Indonesia, and Mexico — countries with lower production volumes but elevated import reliance that makes them acutely sensitive to upstream disruptions originating elsewhere.

Traditional metrics measuring direct trade volumes systematically miss these second and third-order relationships, leading to what the research characterises as a severe underestimation of the true network failure radius. For a broader perspective, Carnegie Mellon University's research on EV supply chains reinforces these findings with complementary supply chain modelling.

The 2030 Supply Gap: Projections the Market Hasn't Fully Priced

Demand growth projections for cobalt-intensive battery chemistries continue to outpace credible supply development scenarios. Several key figures frame the magnitude of the challenge:

| Metric | Projected Figure | Timeframe |

|---|---|---|

| Supply shortfall relative to demand | ~20% | By 2030 |

| Total deficit risk (worst-case scenario) | ~30% | By 2030 |

| Reduction in cobalt per battery (recent years) | >50% decline | Post-2020 LFP adoption |

| Cobalt as share of EV battery cost | ~25% | Current baseline |

| Battery material recovery via recycling | Up to 95% | Long-term projection |

The reduction in average cobalt content per battery reflects genuine chemistry engineering progress. However, this efficiency gain is being outpaced by the sheer volume growth in battery production, meaning aggregate cobalt demand continues rising even as per-unit intensity falls.

The recycling horizon offers a genuine long-term pathway. A recent battery recycling breakthrough has demonstrated that closed-loop processes can theoretically recover up to 95% of cobalt content from end-of-life battery packs. In addition, ethical cobalt sourcing initiatives being pursued by EV manufacturers add further impetus to developing sustainable secondary supply streams. However, the infrastructure build-out required to make this secondary supply meaningful is measured in decades, and the volume of batteries reaching end-of-life today reflects the much smaller EV fleet of a decade ago. Secondary cobalt supply will not close the 2030 gap.

The next major ASX story will hit our subscribers first

Battery Chemistry Strategy: The Risk-Performance Matrix

The competitive landscape between battery chemistries is not simply a question of cost or performance in isolation — it is a risk-adjusted strategic decision that different vehicle segments answer differently.

| Battery Chemistry | Cobalt Content | Energy Density | Cost Profile | Supply Chain Risk |

|---|---|---|---|---|

| NMC (Nickel Manganese Cobalt) | High | High | Higher | High |

| NCA (Nickel Cobalt Aluminum) | Moderate–High | Very High | Higher | High |

| LFP (Lithium Iron Phosphate) | Zero | Moderate | Lower | Low |

| Next-Gen Solid-State (projected) | Low–Zero | Very High | TBD | Emerging |

LFP batteries solve the cobalt problem completely for vehicle segments where their energy density is sufficient: urban commuter vehicles, short-range commercial fleets, and budget-tier passenger cars. For these applications, the LFP transition represents a genuine and durable risk reduction.

The ethical dimension of cobalt sourcing adds further pressure on manufacturers that remain cobalt-dependent. Artisanal cobalt mining in the DRC has been extensively documented as involving hazardous conditions. ESG-driven procurement requirements and emerging supply chain due diligence regulations in the European Union are progressively tightening the compliance burden on manufacturers sourcing cobalt without verified chain-of-custody documentation.

Strategic Responses: How the Industry Is Positioning for Cobalt Risk

OEM and Investor Hedging Strategies

Leading automakers with ongoing cobalt exposure have adopted several documented hedging approaches:

- Long-term offtake agreements that lock in cobalt supply at predetermined pricing, transferring spot market risk to producers but creating counterparty concentration risk.

- Vertical integration through upstream mining investment or equity stakes in cobalt producers, providing direct supply security but introducing commodity price balance sheet exposure.

- Chemistry diversification programmes that accelerate the internal LFP transition for eligible vehicle lines while maintaining NMC/NCA for premium platforms.

- Geographic diversification of refining relationships, seeking to reduce dependence on Chinese processing capacity by developing alternative pathways in Australia, Finland, and North America.

Understanding the full battery metals investment landscape is increasingly essential for investors navigating these hedging decisions with confidence.

The Hypothetical 2027 Price Spike Scenario

If cobalt prices were to spike by 40% in 2027, the downstream effects on NMC battery pack economics would be substantial. Given that cobalt represents approximately 25% of battery material costs in NMC configurations, a 40% price increase translates to roughly a 10% increase in battery pack costs at the material level. OEM responses under this scenario would likely include:

- Accelerated LFP transition for any remaining eligible vehicle lines.

- Cost pass-through to consumers where competitive dynamics permit.

- Margin compression in segments where price sensitivity constrains pass-through.

- Possible production volume adjustments affecting delivery timelines.

Frequently Asked Questions: EV Cobalt Supply Disruptions

What percentage of EVs still depend on cobalt-based batteries?

Approximately 45% of electric vehicles manufactured today use NMC or NCA battery chemistries that contain cobalt, primarily because of their superior energy density advantages over LFP alternatives.

Why can't the EV industry simply switch entirely to cobalt-free batteries?

LFP batteries carry lower energy density than NMC and NCA chemistries, making them unsuitable for long-range and high-performance EV segments without significant range compromises. Next-generation solid-state batteries may eventually close this gap, but commercial-scale deployment remains years away.

Which countries face the greatest cobalt supply disruption risk?

China and the United States face the highest policy-driven disruption potential due to their large production and refining bases. In addition, South Africa, Indonesia, and Mexico face elevated vulnerability due to high import dependency and lower domestic production capacity.

How does China's refining dominance amplify upstream cobalt disruptions?

Because approximately 72% of global cobalt chemical refining capacity is located in China, any upstream supply disruption in the DRC is filtered through Chinese processing infrastructure before reaching battery manufacturers. Chinese policy decisions regarding export volumes or trade restrictions can consequently amplify or redirect the effects of upstream disruptions independently of what is happening in the DRC itself.

What is the projected cobalt supply deficit by 2030?

Baseline projections indicate a supply shortfall of approximately 20% relative to demand by 2030, with worst-case scenarios reaching a 30% deficit depending on EV adoption acceleration, mining investment timelines, and the pace of battery chemistry evolution.

The Compound Risk Framework: Three Vulnerabilities That Won't Resolve Before 2030

The cobalt supply chain's deepest structural weakness is not any single point of failure. It is the simultaneous interaction of three compounding vulnerabilities that are each individually manageable but collectively capable of producing severe systemic disruption:

- Geographic concentration in both mining and processing, with the DRC and China occupying choke-point positions at opposite ends of the value chain.

- Byproduct market dependency, which decouples cobalt supply volumes from EV demand signals and ties them instead to the unrelated economics of copper and nickel markets.

- Network underestimation, where the true failure propagation radius of any cobalt disruption is approximately four times larger than what direct trade data suggests, exposing manufacturers and nations that do not consider themselves cobalt-dependent.

The battery industry's greatest cobalt risk is not a dramatic, identifiable crisis event. It is the quiet convergence of these three structural weaknesses in a window where secondary supply and chemistry alternatives are not yet scaled enough to absorb the impact.

For investors, supply chain managers, and policymakers engaged with the EV sector, the immediate priority is not to predict which disruption scenario will materialise first. It is to stress-test current procurement architectures against the realistic possibility that two or three of these vulnerabilities activate simultaneously. That is the scenario for which most of the industry remains demonstrably unprepared.

This article contains forward-looking projections, scenario modelling, and supply deficit estimates that are subject to material uncertainty. Readers should not rely on these projections as predictions of actual market outcomes. Independent analysis and professional advice should be sought before making investment or procurement decisions based on the scenarios described above.

Want to Stay Ahead of the Next Major Battery Metals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across cobalt, nickel, copper, and the broader battery metals sector — transforming complex data into actionable investment insights before the wider market reacts. Explore how major mineral discoveries have historically generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next critical supply chain opportunity.