May 23, 2026

Global aluminium markets are experiencing a fundamental transformation as export incentive structures undergo systematic revision across major producing nations. This shift reflects broader macroeconomic pressures, where fiscal consolidation objectives increasingly conflict with industrial competitiveness requirements. The ongoing debate over exemption for aluminium exports from RoDTEP cuts has become central to India's trade policy discussions. Furthermore, the interplay between domestic tax policy and international trade dynamics has created complex scenarios requiring careful navigation by aluminium producers worldwide, particularly as US tariffs and inflation continue to reshape global economic conditions.

Understanding India's Export Incentive Policy Restructuring

India's Remission of Duties and Taxes on Exported Products (RoDTEP) framework has undergone significant recalibration, fundamentally altering the competitive landscape for the nation's aluminium sector. The policy mechanism, operational since 2021, was designed to refund embedded taxes, duties, and levies that exporters encounter during manufacturing and distribution processes. However, recent changes have intensified discussions about exemption for aluminium exports from RoDTEP cuts among industry stakeholders.

RoDTEP Framework Evolution and Budget Dynamics

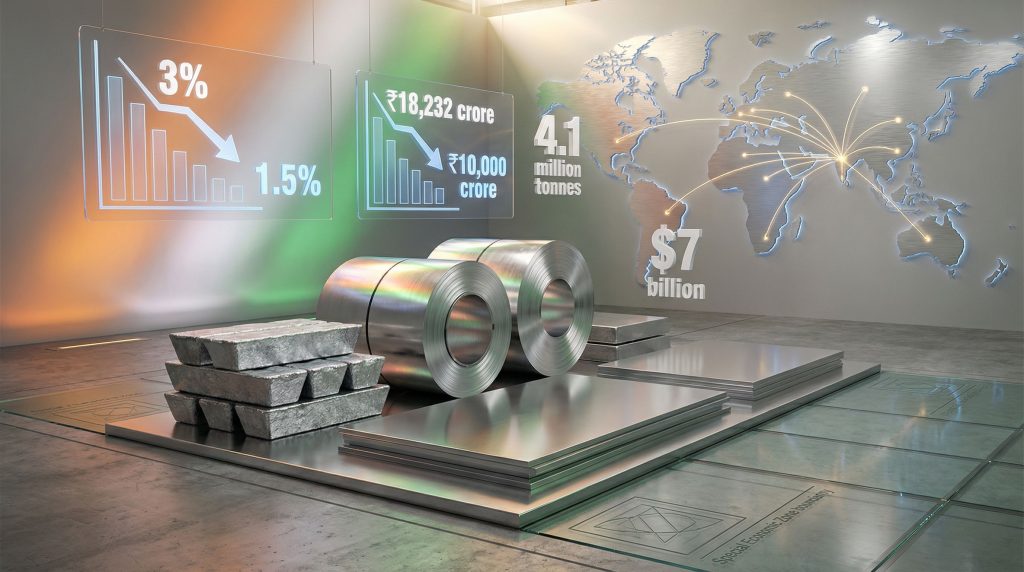

The scheme's budget allocation underwent dramatic revision between fiscal years, revealing the tension between policy ambition and fiscal reality. Initial allocations for FY 2025-26 were established at ₹18,232 crore (USD 2.0 billion), with proposals to expand this to ₹21,709 crore (USD 2.35 billion) for FY 2026-27. However, actual budget allocation contracted substantially to ₹10,000 crore (USD 1.08 billion), representing a significant reduction from proposed figures.

This budgetary constraint culminated in a notification issued on February 23, 2026, implementing a flat 50 percent reduction across RoDTEP rates for all sectors. The rebate structure, which previously ranged between 0.3 percent and 3.9 percent across different product categories, was uniformly halved across manufacturing sectors.

Prior to this adjustment, aluminium exports qualified for RoDTEP rates of approximately 3 percent for Domestic Tariff Area (DTA) units and 2.2 percent for Special Economic Zone (SEZ) units. Following the reduction, these rates declined to 1.5 percent and 1.1 percent respectively.

Sectoral Treatment Patterns and Policy Logic

The policy modification revealed differential treatment across industrial sectors, with agricultural products under ITC HS Chapters 01-24 receiving explicit exemption from the 50 percent rate reduction. This selective application underscores the government's prioritisation framework, where food security considerations appear to outweigh manufacturing competitiveness concerns.

Manufacturing sectors, including aluminium classified under ITC HS Chapter 76, faced the full impact of rate reductions despite their strategic importance to industrial growth objectives. This differential treatment has prompted industry associations to seek equivalent exemptions for critical manufacturing sectors. Consequently, the debate over exemption for aluminium exports from RoDTEP cuts has gained momentum across the industry.

The Aluminium Association of India has formally appealed to the Director General of Foreign Trade (DGFT) requesting that aluminium and articles thereof receive protection from the rate cuts, mirroring the protection extended to agricultural products. Industry representatives have highlighted concerns about aluminium industry urging government action to maintain export competitiveness.

Disclaimer: Policy proposals and industry appeals represent sector-specific perspectives and may not reflect final government decisions. Export incentive policies remain subject to periodic review based on fiscal and trade considerations.

When big ASX news breaks, our subscribers know first

Quantifying the Impact on Indian Aluminium Export Competitiveness

The 50 percent reduction in RoDTEP rates creates measurable economic impact across different facility types, fundamentally altering the cost structure for Indian aluminium producers in global markets. This situation has amplified discussions about securing exemption for aluminium exports from RoDTEP cuts to maintain international competitiveness.

Economic Impact Assessment Across Facility Types

The mathematical impact of incentive reduction reveals significant gaps between policy support and actual tax burdens. Industry analysis suggests that actual unrebated tax burdens stand at 8-9 percent for DTA units and 6-7 percent for SEZ units, substantially exceeding the reduced RoDTEP rates now available.

| Facility Type | Pre-Reduction Rate | Post-Reduction Rate | Actual Tax Burden | Coverage Gap |

|---|---|---|---|---|

| DTA Units | 3.0% | 1.5% | 8-9% | 6.5-7.5% |

| SEZ Units | 2.2% | 1.1% | 6-7% | 4.9-5.9% |

This disparity suggests that even pre-reduction RoDTEP rates provided incomplete compensation for embedded tax costs, with the current reduction creating more pronounced coverage gaps. The reduced rates fail to address the fundamental taxation burden that prompted the creation of export incentive mechanisms.

Global Market Positioning Under New Cost Structures

Indian aluminium exports face a complex multi-layered tariff environment that compounds the impact of reduced domestic support. International trade barriers create additional cost pressures that interact with domestic policy changes, making the tariffs' impact on markets increasingly significant for industry planning.

The European Union's Carbon Border Adjustment Mechanism (CBAM) imposes indirect tariff barriers ranging from 7 percent to 50 percent on aluminium imports, effectively creating additional cost burdens for Indian producers. United States Section 232 duties maintain 50 percent tariffs on aluminium imports, substantially restricting market access.

Mexico has announced plans to escalate customs duties on aluminium products to between 10 percent and 35 percent starting January 2026, further constraining traditional export destinations. These international barriers create cumulative cost pressures that interact negatively with reduced domestic export support, particularly in the context of broader US–China trade strategies affecting global supply chains.

Competitive dynamics are intensifying through Chinese-funded capacity expansion in Indonesia, creating new supply sources with potentially lower cost structures. This capacity addition threatens to displace Indian exports in Asian markets where transportation costs provide natural advantages.

Disclaimer: International tariff rates and trade policies are subject to change based on bilateral negotiations and evolving trade relationships. Market access conditions may vary significantly across specific product categories and trading partners.

Special Economic Zones and Export Strategy Dependencies

India's aluminium export architecture demonstrates significant structural dependence on preferential policy frameworks, with Special Economic Zones and related facilities contributing substantially to national export volumes.

Production Facility Distribution and Contribution Analysis

Approximately 45 percent of India's total aluminium exports originate from units operating under preferential frameworks, including Advance Authorisation (AA) holders, Export Oriented Units (EOU), and Special Economic Zones (SEZ). This concentration indicates substantial structural reliance on policy frameworks designed to enhance export competitiveness.

India's aluminium production capacity stands at 4.1 million tonnes annually, positioning the nation as the second-largest global producer. More than USD 20 billion has been invested in domestic production capacity expansion, representing significant capital commitment to manufacturing infrastructure within these preferential frameworks.

The high concentration of exports from AA/EOU/SEZ facilities reflects the cost advantages these frameworks provide through duty concessions and streamlined regulatory processes. However, this dependence also creates vulnerability to policy modifications affecting these facility types.

Regulatory Framework Complexities and Timeline Pressures

The interaction between multiple policy frameworks creates complex regulatory environments for aluminium producers. SEZ operations benefit from base duty concessions on imported inputs, whilst RoDTEP provides additional refunds for embedded taxes not covered by other mechanisms.

A critical temporal constraint emerges with the March 31, 2026 deadline for SEZ benefit extension decisions. This timeline introduces urgency into policy discussions regarding continuation or modification of support mechanisms for export-oriented manufacturers.

The combination of reduced RoDTEP rates and potential changes to SEZ frameworks could fundamentally alter the economic viability of export-oriented production strategies. Manufacturers operating under these frameworks face uncertainty regarding long-term policy stability, particularly as Trump tariffs implications continue to evolve globally.

Current global trade uncertainties, including escalating tariff barriers and supply chain disruptions, amplify the importance of maintaining supportive domestic policy frameworks. Industry representatives emphasise that policy stability becomes crucial during periods of external trade volatility.

International Trade Barriers and Domestic Policy Interaction

The convergence of reduced domestic export support with escalating international trade barriers creates compounded challenges for Indian aluminium producers seeking to maintain global market position. In addition, the ongoing uncertainty about securing exemption for aluminium exports from RoDTEP cuts further complicates strategic planning.

Multi-Layered Tariff Environment Assessment

Indian aluminium exports face an increasingly complex tariff landscape across major markets, with barriers operating at multiple levels:

European Market Access:

- CBAM indirect tariffs: 7-50% range

- Carbon compliance requirements increasing administrative costs

- Regulatory complexity affecting small and medium producers disproportionately

North American Trade Dynamics:

- US Section 232 duties: 50% on aluminium imports

- Reduced market access for primary aluminium products

- Preference for value-added products with lower tariff exposure

Latin American Market Evolution:

- Mexico customs duty escalation: 10-35% starting January 2026

- Regional trade agreement implications

- Shifting competitive dynamics favouring other suppliers

Supply Chain Vulnerability and Competitive Positioning

Global aluminium production capacity is experiencing significant geographical shifts that affect Indian producers' competitive positioning. Chinese-funded capacity expansion in Indonesia represents a strategic challenge to traditional supply relationships.

Indonesian capacity additions benefit from lower energy costs and proximity to key Asian markets. These facilities potentially offer cost structures that challenge Indian producers' traditional competitive advantages in regional markets.

Simultaneously, import surge patterns affecting the domestic Indian market create pressure on producers to focus on export markets for profitability. However, escalating international barriers limit export opportunities, creating a challenging strategic environment.

The convergence of reduced domestic support and increased international barriers effectively squeezes profit margins from both directions. This dual pressure threatens the viability of expansion investments and long-term competitiveness, with potential relief through proposed tariff breaks remaining uncertain.

Disclaimer: International trade policy developments and competitive dynamics are subject to rapid change based on geopolitical factors and bilateral trade relationships. Market positioning strategies require continuous adaptation to evolving conditions.

Industry Advocacy and Policy Reform Proposals

The Aluminium Association of India has developed comprehensive policy reform proposals designed to address the competitive challenges created by reduced export incentives and escalating international trade barriers. These proposals centre on securing meaningful relief from current policy constraints.

Strategic Rate Calculation Methodology

Industry proposals emphasise restructuring RoDTEP rate calculations to reflect actual tax burdens rather than applying uniform percentage reductions across sectors. The association advocates for rates based on demonstrated, quantifiable tax costs embedded in the aluminium production and export process.

Proposed rate calculation methodology includes:

For DTA Operations:

- Comprehensive tax burden analysis covering central, state, and local levies

- Input tax credit gaps identification

- Unrebated cost components quantification

- Target rate: 8-9% reflecting actual burden levels

For SEZ Operations:

- Modified tax burden assessment accounting for existing concessions

- Residual cost identification after duty exemptions

- Administrative and compliance cost inclusion

- Target rate: 6-7% reflecting net unrebated burdens

Facility Coverage Extension Arguments

The association emphasises extending comprehensive RoDTEP coverage to all production facility types, arguing that current global trade uncertainties require uniform support mechanisms across the aluminium sector. Furthermore, recent developments highlight the need for government addressing export concerns across multiple industries.

Given that AA/EOU/SEZ facilities contribute 45 percent of national aluminium exports, policy modifications affecting these units carry disproportionate weight in determining overall export competitiveness. The concentration of exports in these facility types makes sector-wide support crucial for maintaining market position.

Timeline considerations focus on the March 31, 2026 SEZ benefit extension deadline, with industry representatives arguing for prompt policy clarification to enable production planning and investment decision-making.

Global Aluminium Trade Flow Implications

The reduction in Indian export incentives occurs within a broader context of shifting global aluminium production patterns and evolving trade relationships that could reshape international market dynamics.

Market Rebalancing Scenarios and Volume Projections

India's aluminium export volumes, valued at approximately USD 7 billion annually and representing 2 percent of the country's total goods exports, face potential redistribution among alternative suppliers under current policy constraints.

Reduced competitiveness from lower export incentives could create market share opportunities for competing producers. Key beneficiaries may include:

Regional Competitors:

- Indonesian smelters with Chinese backing

- Middle Eastern producers with energy cost advantages

- Russian suppliers in markets without sanctions restrictions

Market Segment Shifts:

- Primary aluminium vs. value-added products

- Regional trade pattern evolution

- Supply chain relationship modifications

Investment Decision Framework Implications

The policy modification introduces new variables into long-term investment planning for Indian aluminium producers. Capacity expansion decisions must now account for reduced export incentive support and uncertain policy stability.

Investment considerations include:

Domestic Market Focus:

- Increased emphasis on domestic demand growth

- Value-added product development for local consumption

- Supply chain localisation strategies

Technology and Efficiency:

- Production cost reduction through technology upgrades

- Energy efficiency improvements to offset incentive reductions

- Automation investments to enhance competitiveness

Market Diversification:

- Exploration of non-traditional export markets

- Product mix optimisation for different regulatory environments

- Strategic partnership development with international players

The next major ASX story will hit our subscribers first

Export Incentive Policy Design Lessons

India's RoDTEP modification reveals broader challenges in designing export incentive policies that balance fiscal sustainability with industrial competitiveness objectives.

Fiscal Consolidation vs. Industrial Competitiveness Trade-offs

The dramatic budget allocation reduction from proposed ₹21,709 crore to actual ₹10,000 crore illustrates the tension between expansive industrial support and fiscal discipline requirements. This reduction reflects broader macroeconomic priorities where debt sustainability concerns outweigh sectoral competitiveness considerations.

Policy effectiveness requires careful calibration between support levels and actual cost burdens. When incentive rates fall substantially below genuine tax burdens they are designed to address, the competitive benefits diminish significantly.

Key Design Principles:

- Rate calculation based on empirical cost analysis rather than budgetary constraints

- Sector-specific assessment rather than uniform percentage applications

- Regular review mechanisms to account for changing cost structures

- Long-term policy stability to support investment planning

International Best Practices and Comparative Approaches

Export support mechanisms in competing economies demonstrate alternative approaches to maintaining industrial competitiveness whilst managing fiscal constraints.

Alternative Models Include:

- Direct production subsidies rather than export-specific incentives

- Technology upgrade support programmes

- Infrastructure development focused on export competitiveness

- Trade finance facilitation mechanisms

Effective export policy design requires integration with broader trade policy objectives, including market access negotiations and international trade relationship management. Unilateral incentive modifications without corresponding international engagement may prove insufficient for maintaining competitive position.

Disclaimer: Policy analysis and recommendations represent industry perspectives and may not reflect government policy priorities or fiscal constraints. Export incentive policy design involves complex trade-offs between multiple economic and political considerations.

Frequently Asked Questions About India's Aluminium Export Policy Changes

Will aluminium receive exemption for aluminium exports from RoDTEP cuts?

Current policy status indicates no confirmed exemption for aluminium products from the 50 percent RoDTEP rate reduction. The Aluminium Association of India has submitted formal appeals to the Director General of Foreign Trade requesting exemption similar to that granted for agricultural products under ITC HS Chapters 01-24.

Industry appeals emphasise that aluminium and articles thereof, classified under ITC HS Chapter 76, merit equivalent protection given the sector's strategic importance to industrial growth and export earnings. However, government response timelines and decision criteria remain unclear.

Alternative support mechanisms under consideration include revised rate calculation methodologies based on actual tax burdens rather than uniform percentage reductions. The March 31, 2026 timeline for SEZ benefit decisions may influence broader policy modifications.

How do rate changes affect different production facility types?

The 50 percent RoDTEP reduction affects facility types differently based on their existing tax burden structures and regulatory frameworks:

Domestic Tariff Area (DTA) Units:

- Previous RoDTEP rate: 3.0%

- Reduced rate: 1.5%

- Actual tax burden: 8-9%

- Impact: Increased unrebated burden of approximately 6.5-7.5%

Special Economic Zone (SEZ) Units:

- Previous RoDTEP rate: 2.2%

- Reduced rate: 1.1%

- Actual tax burden: 6-7%

- Impact: Increased unrebated burden of approximately 4.9-5.9%

Export Oriented Units (EOU) and Advance Authorisation (AA) holders:

- Similar rate reduction patterns

- Varied impact based on specific operational frameworks

- Combined facilities represent 45% of national aluminium exports

What are the broader implications for manufacturing competitiveness?

The RoDTEP modification establishes precedent for export incentive policy across manufacturing sectors, potentially affecting industrial competitiveness beyond aluminium. Key implications include:

Cross-Sector Policy Framework:

- Uniform percentage reductions may not account for sector-specific cost structures

- Budget-driven rather than competitiveness-based policy modifications

- Potential for similar reductions in other manufacturing sectors

Long-term Industrial Strategy:

- Shift from export promotion to domestic market focus

- Emphasis on value-addition and technology upgrades

- Integration with broader manufacturing strategy objectives

Global Supply Chain Positioning:

- Reduced attractiveness for export-oriented manufacturing investment

- Potential supply chain displacement to competing economies

- Need for alternative competitiveness enhancement strategies

The policy modification reflects broader challenges in maintaining export competitiveness during periods of fiscal consolidation. Successful adaptation requires comprehensive industrial strategy development rather than reliance solely on export incentive mechanisms.

Disclaimer: Policy implications and strategic assessments represent analytical perspectives based on available information. Actual policy outcomes may vary based on government decisions and evolving economic conditions. Manufacturing investment decisions should consider multiple factors beyond export incentive availability.

Ready to Capitalise on Commodity Market Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant aluminium and commodity discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.