May 23, 2026

The Illusion of Price Discovery in a Fractured Energy World

Energy markets have historically struggled to price tail risks correctly. From the 1973 Arab oil embargo to the 2021 European gas crisis, financial markets consistently underestimated the velocity and depth of supply shocks until the physical reality became undeniable. That pattern appears to be repeating itself in 2026, as oil markets ignore red flags as global energy crisis deepens, with a constellation of structural failures now converging across global energy supply chains while benchmark crude prices, though elevated, remain stubbornly detached from the full severity of the disruption unfolding beneath the surface.

ICE Brent trading above $104 per barrel signals genuine market tension. Yet institutional analysts and forward-market pricing both suggest that current levels still fall well short of reflecting the compounding risks now accumulating simultaneously across multiple geographies, production systems, and transit corridors. Understanding why requires moving beyond headline price data and examining the structural mechanics at work.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: A Chokepoint the World Cannot Reroute Around

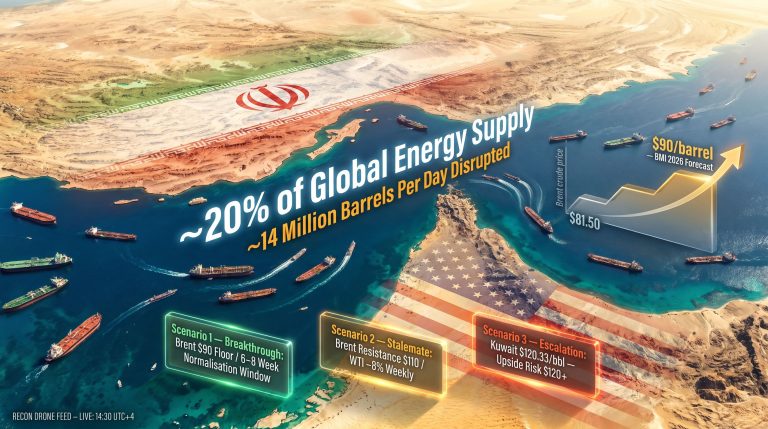

The Strait of Hormuz is not merely a geographic feature. It is the single most consequential energy infrastructure node on the planet, and unlike pipelines or refineries, it cannot be bypassed, duplicated, or engineered around at any meaningful scale. At its narrowest point, the waterway spans just 24 miles, yet it serves as the transit corridor for approximately 20% of the world's daily oil supply.

Recent weeks have seen a fragile resumption of tanker movements, with confirmed reports of five supertankers carrying approximately 6 million barrels exiting the strait. However, war-risk insurance premiums have surged dramatically, a signal JPMorgan has explicitly flagged as a leading indicator of market stress that has yet to be fully reflected in spot prices. Furthermore, the oil geopolitical risks associated with Hormuz transit have become a material commercial consideration, not merely a risk management footnote.

The cascading mechanics of a sustained Hormuz disruption follow a predictable but devastating sequence:

- Tanker slowdowns and transit uncertainty reduce effective export capacity from Gulf producers

- Storage facilities at destination ports reach saturation thresholds as delivery timing becomes unreliable

- Refiners begin drawing down strategic reserves and spot inventories to compensate

- Gulf producers face mandatory output curtailments as they lose the ability to move product to market

- Global benchmark prices spike as physical shortages materialise faster than financial markets anticipated

JPMorgan's scenario analysis suggests Gulf producers could face forced production cuts within weeks if transit disruption persists, a development that would represent not just a price shock but a structural rupture in the global oil supply architecture. According to IEEFA's analysis of the Middle East crisis impact, such disruptions carry consequences well beyond short-term price volatility.

Iran, Oman, and the Emerging Toll-Gate Model

One of the least discussed but potentially most consequential developments involves reported discussions between Iran and Oman regarding the formalisation of joint maritime control over Hormuz transit traffic through a permanent toll system. If implemented, such an arrangement would fundamentally alter the economics of global energy trade by embedding a geopolitical surcharge into every barrel of Gulf crude and every LNG cargo passing through the strait.

For Asian importers, who lack viable alternative supply corridors at comparable scale, this scenario represents a structural cost increase with no near-term remedy. European nations dependent on Middle Eastern LNG would face equivalent exposure. The political implications extend well beyond energy pricing, as a formalised Hormuz toll system would represent one of the most significant restructurings of global maritime sovereignty in decades.

OPEC+ Credibility and the Production Quota Paradox

| Indicator | Current Status |

|---|---|

| OPEC+ July quota increase planned | +188,000 b/d |

| Estimated Gulf output decline since Hormuz disruption | ~10 million b/d |

| Saudi crude export volumes | Multi-year lows (JODI data) |

| Saudi Arabia fuel oil imports | Rising, as domestic gas output falls |

The disconnect between OPEC+ quota decisions and physical delivery capacity has reached a level that undermines the cartel's pricing credibility. OPEC's market influence is increasingly being tested as Gulf state output has simultaneously plunged by an estimated 10 million barrels per day since Hormuz disruptions commenced, even while the seven remaining OPEC+ members are expected to approve an additional 188,000 barrels per day increase to July production quotas.

Paper production quotas and physical barrel delivery are two entirely different things. When the world's most prolific export corridor is compromised, quota decisions become largely symbolic, and markets that price on quota headlines rather than physical flows are operating on incomplete information.

Saudi Arabia's situation encapsulates this paradox particularly sharply. JODI data confirms that Saudi crude exports have sunk to record lows, while the kingdom has simultaneously been forced to increase fuel oil imports as domestic natural gas output declines. Consequently, a nation that has historically defined global supply capacity is now itself navigating an energy adequacy challenge.

Regional Exposure: Who Bears the Sharpest Pain

Egypt and the Eastern Mediterranean Gas Collapse

Egypt's gas production has deteriorated to levels not recorded since the country began publishing official output data in 2011. March 2026 production came in at just 3.34 billion cubic metres, or approximately 108 million cubic metres per day, a figure that reflects both structural reservoir decline and the collapse of Israeli pipeline imports that had previously supplemented domestic supply.

This dual failure — falling domestic output compounded by the loss of cross-border imports — has severe implications for North African energy security and for European LNG markets that increasingly competed with Egypt for flexible supply. The Energean dividend cut following the Israeli gas shutdown is an early financial signal of how rapidly the Eastern Mediterranean gas network is destabilising.

Asia's Structural Vulnerability

Japan, China, and India each face distinct but interconnected exposure to the current disruption:

-

Japan: Middle East crude imports have fallen to their lowest level on record. Japan's largest utility, JERA, has filed with the US Federal Energy Regulatory Commission to initiate regulatory review of its Longboard LNG project in Hawaii's Oahu, which would involve a floating regasification unit connected to an onshore gas power plant. This is an emergency infrastructure pivot that signals deep anxiety about long-term Middle East import dependency.

-

China: Beijing's National Development and Reform Commission has raised domestic retail fuel price caps for the second time in three months, setting limits at approximately $1.33 per litre for gasoline and $1.38 per litre for diesel. Simultaneously, China is boosting strategic oil stockpiles despite a sharp drop in total imports. Chinese fuel exports remain suppressed under ongoing government export restrictions.

-

India: Power demand has hit record highs, driven by extreme heat accelerating coal consumption. India is actively evaluating direct Gulf oil loading arrangements designed to reduce Hormuz dependency, while IEA data confirms the broader oil shock is accelerating Indian EV adoption at a pace that would otherwise have taken years longer to materialise.

Europe's Triple Compression Problem

Europe faces a uniquely uncomfortable convergence of pressures. Macroeconomic indicators have posted their weakest readings since 2023. The EU has formally warned that energy prices are expected to remain structurally elevated through 2027. Meanwhile, the UK government has taken a pragmatic but geopolitically uncomfortable step of suspending restrictions on diesel and jet fuel refined from Russian crude in third countries such as Turkey and India, citing Middle East supply disruption as justification.

The Amsterdam-Rotterdam-Antwerp bunkering hub is displaying an additional symptom of supply chain stress: marine fuel quality has deteriorated, with surveyors reporting elevated sediment levels and substandard blending components including shale oil derivatives. Quality failures at the world's most important marine fuel hub signal that the disruption is filtering down into refined product supply chains in ways that go beyond crude pricing.

Europe is simultaneously navigating an energy affordability crisis, a geopolitical supply dependency challenge, and a self-reinforcing regulatory tightening cycle. These three forces are structurally incompatible with near-term energy price relief.

Scenario Analysis: Three Pathways Forward

| Scenario | Key Assumption | Brent Price Range | Estimated Timeline |

|---|---|---|---|

| Diplomatic Breakthrough | U.S.-Iran deal reached, Hormuz reopens | $75-$85/bbl | 4-8 weeks |

| Prolonged Disruption | Conflict continues, strait partially impaired | $105-$125/bbl | 3-6 months |

| Systemic Supply Shock | Hormuz formally controlled, Gulf output curtailed | $130-$160+/bbl | 6-18 months |

The IEA has flagged a July-August 2026 window as a critical threshold for global oil market tightening, describing conditions that would constitute a severe demand-over-supply imbalance. Goldman Sachs has issued fresh warnings about the pace of global stockpile depletion, even as US crude inventories recorded their largest-ever single-period decline. The IEA's assessment of options to ease oil price pressures on consumers provides important context for understanding how policy responses might evolve under each scenario.

Forward markets currently price Brent above $81 per barrel for the next 12 months, and Barclays has issued explicit warnings that its $100 per barrel 2026 forecast now carries material upside risk. The asymmetry here is notable: the diplomatic breakthrough scenario offers limited price downside from current levels, while the systemic shock scenario carries catastrophic upside implications that markets have yet to fully discount.

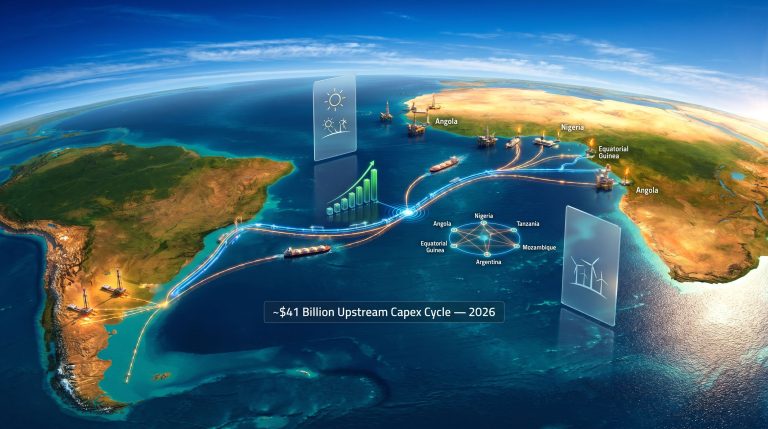

Supply Diversification Attempts and Their Limitations

Several non-Gulf producers are attempting to fill the void, with varying degrees of credibility:

-

Nigeria is targeting a 100,000 b/d output increase, and the 650,000 b/d Dangote Refinery is targeting a September IPO with reportedly $2 billion in private investor interest already accumulated.

-

Indonesia has launched a tender for 13 new exploration blocks, with the government targeting a 50% increase in domestic output to reach 1 million b/d. The majority of acreage is located in underdeveloped eastern provinces carrying higher geological risk and longer development timelines.

-

Norway has exceeded April production forecasts, with Equinor signing a new long-term gas supply deal with Eneco to bolster European supply security.

-

Venezuela continues attempting to attract international investment. However, ConocoPhillips CEO Ryan Lance stated publicly that a 95% aggregate government take on production revenues falls fundamentally short of what would be required to attract serious capital commitments, citing unresolved contract security concerns.

The next major ASX story will hit our subscribers first

Geopolitical Wildcards Adding Systemic Uncertainty

Alberta Premier Danielle Smith has confirmed an October referendum asking voters whether Canada's most prolific oil-producing province should initiate a formal separation process. Alberta accounts for approximately 85% of Canada's total oil production. Regardless of the referendum outcome, the political uncertainty itself introduces a new layer of supply risk into North American energy markets, affecting pipeline infrastructure planning, export capacity projections, and US energy import dependency calculations.

The Codelco scandal in Chile adds a separate but structurally important dimension. The world's largest copper producer fired an executive and initiated disciplinary proceedings after an audit revealed that 2025 production reporting had been manipulated, with finished product tallies artificially inflated. Copper is fundamental to electrification infrastructure, meaning that data integrity failures at state-controlled commodity producers create systemic mispricing risks across the very supply chains that markets are relying on as a long-term alternative to fossil fuel dependency.

The Crisis-Driven Energy Transition Acceleration

Perhaps the most consequential long-term signal embedded within the current crisis is the measurable acceleration of energy transition investment. The energy transition shift is gaining momentum as IEA data confirms the oil price shock is driving a statistically significant surge in global EV sales. Wind and solar power generation have overtaken gas-fired electricity for the first time on record. US energy storage installations posted a record first quarter in 2026. China's solar panel exports are surging as global demand for fossil fuel alternatives reaches new intensity.

TotalEnergies moving to sell over $100 million in European solar and wind portfolio stakes represents a strategic capital rotation signal worth monitoring closely. Whether this reflects opportunistic profit-taking or a broader portfolio rebalancing toward higher-return assets will become clearer over coming quarters.

The Woodside CEO's public assessment that markets are fundamentally underestimating the severity of the LNG supply outlook problem, compounded by industrial action at two Australian LNG facilities following collapsed wage negotiations, reinforces the conclusion that the supply disruption is broader and deeper than current pricing implies. In addition, the earlier oil price rally driven by tariff uncertainty has left markets ill-prepared for the compounding pressures now materialising across multiple fronts simultaneously.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario projections, and price ranges cited reflect analyst estimates and institutional research available at time of writing. Energy markets are subject to rapid change. Readers should conduct their own due diligence before making any investment decisions.

Want to Stay Ahead of the Commodity Discoveries Driving the Next Market Cycle?

As energy market dislocations reshape global commodity demand, Discovery Alert's proprietary Discovery IQ model scans the ASX in real time, delivering instant notifications on significant mineral discoveries — from copper critical to electrification infrastructure through to energy commodities — so subscribers can act on actionable opportunities before the broader market catches on. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major find.