July 1, 2026

When Moral Mandates Meet Market Reality: The New Era of Faith-Based Investor Activism

Institutional investing has long operated under the assumption that financial returns and ethical values exist in separate spheres. That assumption is cracking. Across the globe, a growing class of institutional investors governed by explicit moral mandates is demonstrating that capital allocation can function as a direct instrument of corporate accountability. Mining companies, historically shielded from the sharpest edges of ESG scrutiny by the essential nature of their output, are now discovering that faith-based investors are among the most disciplined, patient, and ultimately uncompromising forces reshaping expectations in the sector.

The decision by the Jesuits in Britain divesting from Rio Tinto over environmental concerns, following three to four years of unresolved shareholder engagement, is not an isolated act of institutional frustration. It is a case study in how ethical capital behaves when dialogue fails, and what that failure signals to the broader investment community.

When big ASX news breaks, our subscribers know first

The Architecture of Faith-Based Institutional Capital

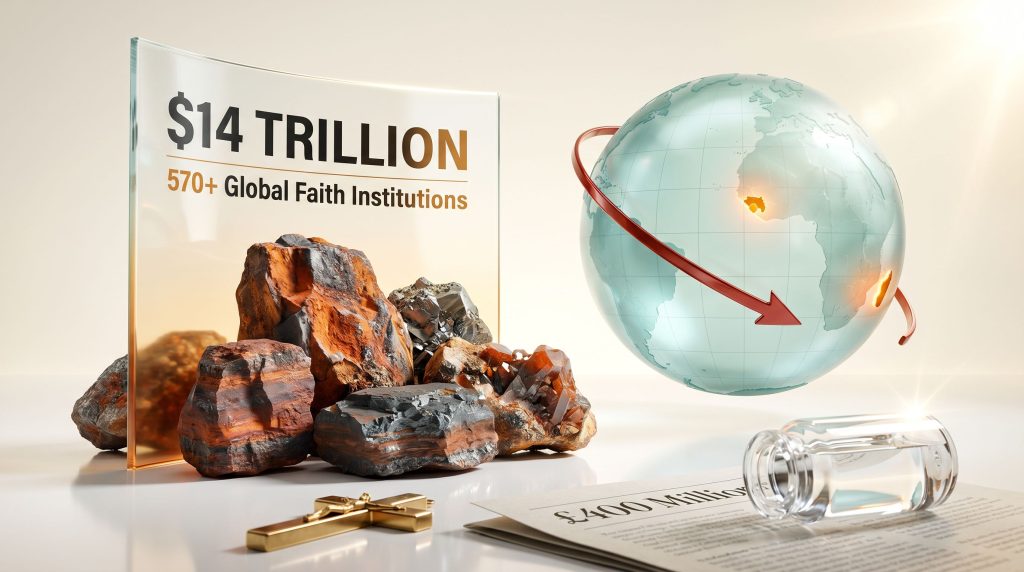

To understand why faith-based divestment carries weight beyond its symbolic resonance, it helps to understand the structural reality of values-aligned capital in global markets. Religious institutions collectively manage portfolios that run into the hundreds of billions of dollars across pension funds, endowments, land holdings, and equity portfolios. The Jesuits in Britain alone oversee an equity portfolio estimated at approximately £400 million, dedicated to investment decisions aligned with the order's ethical principles.

This is not a marginal pool of capital. Furthermore, when faith-based institutions act in coordination, their combined influence becomes a meaningful signal to the broader market. Cumulative fossil fuel divestment commitments from faith-aligned and values-driven institutions globally have reached extraordinary scale, reshaping perceptions of reputational and capital risk for companies in extractive industries.

The theological underpinning for this activism has been sharpening for more than a decade. Pope Francis's 2015 encyclical Laudato Si' reframed ecological responsibility as a moral imperative rather than an optional policy preference, providing Jesuit and broader Catholic investment bodies with explicit doctrinal grounds for screening out investments incompatible with environmental stewardship. This translated into concrete portfolio action: the Jesuits in Britain completed full divestment from fossil fuel extractors in 2020, and Jesuit provinces across Europe and Canada pursued comparable commitments throughout the late 2010s.

Faith-based divestment strategies differ structurally from mainstream ESG fund exclusions. They are not purely risk-adjusted decisions. They operate on value-driven mandates that can accelerate the divestment timeline regardless of a company's financial performance.

The implication for mining companies is significant. A company cannot simply outperform expectations on earnings or production targets to neutralise a faith-based investor's environmental objections. The decision calculus is different, and the threshold for engagement failure can arrive more quickly than it would for a purely financially motivated institutional holder. Broader Rio Tinto investor impact considerations are also influencing how markets interpret these developments.

Three Environmental Concerns Driving the Divestment Review

The Jesuits in Britain's review of their Rio Tinto position did not emerge from a single incident. It reflects a multi-year accumulation of unresolved concerns across three distinct environmental and governance domains.

| Concern Area | Location | Specific Issue |

|---|---|---|

| Water contamination | Southern Madagascar | Elevated uranium and lead concentrations downstream of mining operations |

| Transparency failures | Madagascar | Late, incomplete, or absent water quality reporting |

| Scope 3 emissions | Global supply chain | Indirect greenhouse gas emissions not adequately addressed |

| Large-scale project risk | Guinea (Simandou) | Environmental and community governance concerns at iron ore megaproject |

Water Contamination in Southern Madagascar

Environmental groups have spent years raising concerns about water quality downstream of Rio Tinto's southern Madagascar operations, specifically around QIT Madagascar Minerals. The concerns centre on elevated concentrations of uranium and lead in water sources that local communities depend on for drinking.

The health stakes here are not abstract. Lead exposure is well-documented in scientific literature as a neurological hazard, particularly for children, where even low-level chronic exposure is associated with irreversible cognitive impairment and developmental delays. Uranium contamination, meanwhile, presents a distinct risk profile: its primary health concern is nephrotoxicity, meaning prolonged exposure damages kidney tissue. For communities with no alternative water source and limited access to healthcare, these are not hypothetical risks.

What amplifies the Jesuits' concern beyond the contamination itself is the pattern of reporting failures. The engagement with Rio Tinto revealed that water quality reports were arriving late, lacking required detail, or failing to materialise at all. This is a governance failure distinct from the environmental one. It suggests that the mechanisms designed to detect and communicate risk are themselves unreliable, which makes independent verification of remediation outcomes nearly impossible.

Rio Tinto Chair Dominic Barton responded at the company's AGM by stating that external assessments confirm regulated metals remain consistently below laboratory detection limits. This is a compliance-framed answer to an accountability-framed question. The distinction matters enormously. Regulatory compliance confirms that concentrations fall within legally permitted thresholds, but it does not resolve questions about reporting timeliness, methodological transparency, chain-of-custody integrity of water samples, or the adequacy of those thresholds for communities with no alternative water sources.

The Simandou Project: Scale, Governance, and Greenfield Risk

Rio Tinto's Simandou iron ore project in Guinea represents one of the world's largest undeveloped iron ore deposits. Its environmental footprint extends across a biodiversity-sensitive region, and the governance challenges of operating at scale in a complex regulatory environment draw heightened scrutiny from ESG-focused investors. The iron ore market challenges associated with large greenfield projects in ecologically sensitive regions introduce a compounding risk: the potential for harm is greatest precisely when environmental governance systems are least established.

Faith-based investors, whose mandates extend beyond financial risk to encompass community welfare and ecological integrity, view projects like Simandou as a forward-looking test of Rio Tinto's commitment to substantive rather than procedural environmental governance.

Scope 3 Emissions: The Accountability Blind Spot

Scope 3 emissions represent the indirect greenhouse gas emissions generated across a company's entire value chain, including the downstream use of extracted materials. For a mining company whose iron ore becomes steel, or whose operations supply industrial inputs to energy-intensive industries, Scope 3 typically constitutes between 80% and 95% of total emissions but has historically been excluded from corporate climate commitments due to measurement complexity.

Faith-based and values-aligned investors are increasingly unwilling to accept this exclusion. If a miner's climate strategy addresses only the emissions generated within its operational boundaries while ignoring the vastly larger downstream footprint, the resulting climate commitment is structurally incomplete. The Jesuits' inclusion of Scope 3 emissions as a divestment trigger signals that their standard has moved beyond what most regulatory frameworks currently require.

A Decade of Faith-Based Divestment: The Pattern Behind the Decision

The Jesuits in Britain's current review of Rio Tinto sits within a broader institutional trajectory that has been building momentum across Catholic and broader Christian investment bodies for more than ten years.

| Year | Institution | Action Taken |

|---|---|---|

| 2015 | Pope Francis | Published Laudato Si', establishing ecological responsibility as Catholic moral teaching |

| 2016 | Jesuits in English Canada | Committed to fossil fuel divestment over five-year horizon |

| 2017 | Italian Jesuits | Joined the fossil fuel divestment movement |

| 2018 | Church of England Pensions Board | Filed shareholder resolution against Rio Tinto urging withdrawal from coal lobbying bodies |

| 2020 | Jesuits in Britain | Completed full divestment from fossil fuel extractors |

| 2024 | 570+ global faith institutions | Declared fossil fuel investment incompatible with faith values ahead of COP29 |

| 2026 | Jesuits in Britain | Evaluating divestment from Rio Tinto over environmental and emissions concerns |

The Church of England Pensions Board's 2018 shareholder resolution against Rio Tinto is particularly instructive. By formally requesting Rio Tinto's withdrawal from coal industry lobbying bodies, including the Minerals Council of Australia, the Board established a precedent for using formal shareholder mechanisms as accountability tools rather than relying solely on closed-door engagement. This escalation pathway — from private dialogue to formal resolution to potential divestment — is precisely the sequence the Jesuits in Britain appear to be following.

The convergence of multiple faith-based institutions arriving independently at similar divestment thresholds with Rio Tinto suggests the company faces a systemic accountability deficit rather than an isolated communications failure with a single investor.

As reported by Reuters UK, the Jesuits' public statement at Rio Tinto's AGM marked a significant escalation in the formal engagement process, drawing attention from institutional observers globally.

Does Faith-Based Divestment Actually Change Corporate Behaviour?

This is the critical question that separates divestment as a moral act from divestment as a strategic tool. The evidence is nuanced.

The engagement-first model that preceded the Jesuits' divestment review serves several functions beyond its primary objective of producing corporate change. It creates a documented record demonstrating that the investor made good-faith efforts to resolve concerns through dialogue. It establishes credibility for the eventual divestment decision. And it forces corporate management to engage with specific, detailed concerns rather than deflecting with general sustainability commitments.

Where engagement demonstrably fails, divestment carries a different kind of signal. When a credible institutional investor with an explicit ethical mandate publicly exits a position after exhausting dialogue options, several downstream effects can follow:

- Reputational amplification: media attention and analyst scrutiny intensify around the specific concerns raised

- Regulatory attention: documented environmental concerns raised by institutional investors can attract regulatory review

- Coordinated action risk: other faith-based or ESG-aligned institutions may reassess their own positions

- Financing cost implications: ESG credentials increasingly influence insurance premiums, green financing eligibility, and debt covenant structures in major markets

The compounding effect when multiple faith-based and ESG institutions divest simultaneously is qualitatively different from isolated exit decisions. Individual divestments become data points in a larger narrative about whether a company's environmental governance is structurally functional or chronically deficient.

Rio Tinto's ESG Track Record: Context the Numbers Don't Capture

The current engagement over Madagascar and Guinea does not exist in a vacuum. Rio Tinto's ESG history includes significant reputational events that have shaped how institutional investors evaluate the company's governance culture. The 2020 destruction of the Juukan Gorge sacred site in Western Australia — a 46,000-year-old Aboriginal heritage site — was among the most damaging self-inflicted reputational events in modern Australian mining history.

It resulted in the resignation of the company's chief executive and the departure of several senior executives, but more importantly, it raised fundamental questions about whether Rio Tinto's operational decision-making adequately weighs irreversible community and heritage impacts.

For faith-based investors whose mandates explicitly encompass justice for vulnerable communities and respect for sacred heritage, Juukan Gorge was not a discrete incident but a data point confirming a pattern. The Madagascar water reporting failures and the Simandou governance questions are evaluated against this backdrop. In addition, ongoing Rio Tinto tax pressures and rising regulatory obligations across multiple jurisdictions are adding further complexity to the company's institutional investor relationships.

The investor sentiment shift underway across the mining sector is moving from disclosure-based ESG assessment toward outcome-based accountability. Companies that demonstrate regulatory compliance while resisting genuine transparency are increasingly treated as failing a qualitatively different standard. Mining sustainability transformation demands that firms go beyond tick-box compliance, and the consideration of natural capital in mining is rapidly becoming central to how institutional investors measure long-term value.

Mining Weekly's coverage of the Jesuits' engagement with Rio Tinto highlights how the sector is grappling with a new generation of accountability standards that go well beyond conventional ESG disclosure frameworks.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Faith-Based Divestment and Mining Accountability

What Is Divestment and How Does It Differ from ESG Screening?

Divestment involves the deliberate sale of financial holdings in a company or sector on ethical, environmental, or social grounds. The investor makes an active decision to exit an existing position rather than simply avoiding it in future allocation decisions. Negative ESG screening, by contrast, prevents initial investment in companies that fail defined criteria but does not require the sale of existing holdings. Divestment is generally a more powerful signal because it represents a reversal of a prior investment decision, implying that something has changed about the company's conduct or the investor's assessment of it.

Why Do Faith-Based Institutions Often Move Faster Than Mainstream ESG Funds?

Religious investment mandates derive from doctrinal frameworks that do not require the same evidentiary thresholds as risk-adjusted financial models. A mainstream ESG fund typically needs to demonstrate that an environmental concern constitutes a material financial risk before acting. A faith-based investor can act on the basis that a practice is incompatible with the institution's values regardless of whether the financial materiality has been formally established. This means faith-based divestment timelines can be shorter, and the decision can be made on moral rather than financial grounds alone.

What Are Scope 3 Emissions and Why Does Their Exclusion Matter?

Scope 3 covers all indirect greenhouse gas emissions that occur across a company's value chain outside its direct operational control. For miners, this includes emissions generated when customers process iron ore into steel, when coal is combusted for energy, or when industrial gases are used in downstream manufacturing. Because Scope 3 typically represents the overwhelming majority of a mining company's total emissions footprint, a climate strategy that addresses only Scope 1 and Scope 2 accounts for a fraction of the actual impact. Faith-based investors with climate mandates are increasingly treating Scope 3 disclosure and reduction commitments as minimum standards rather than optional disclosures.

Has the Jesuits in Britain Confirmed a Final Divestment Decision?

As of May 2026, no final divestment decision has been confirmed. The Jesuits in Britain are actively evaluating their position following the conclusion of a three-to-four-year direct engagement process. The public statement at Rio Tinto's AGM signals that the review is formal and that continued holding is contingent on satisfactory engagement outcomes, but no exit has been announced.

What Is the Simandou Project and Why Does It Draw Environmental Scrutiny?

Simandou is an iron ore deposit located in Guinea, West Africa, widely regarded as one of the largest untapped iron ore resources globally. Its scale and location in a region of significant biodiversity sensitivity, combined with the governance complexities inherent to large-scale resource extraction in West Africa, make it a focal point for ESG-focused investors assessing Rio Tinto's forward-looking environmental and community governance standards.

The Strategic Outlook: What This Signals for the Mining Sector

The Jesuits in Britain divesting from Rio Tinto over environmental concerns, should they proceed, would represent more than one institution's portfolio decision. It would be a measurable data point in a structural trend: the convergence of faith-based divestment campaigns, mainstream institutional ESG requirements, and tightening regulatory disclosure frameworks across the EU, UK, and Australia.

For mining companies, the emerging accountability environment creates a clear strategic calculus. Environmental transparency is no longer a public relations function or a compliance obligation. It is becoming a prerequisite for access to the full spectrum of institutional capital. Companies that treat water quality reporting as a tick-box exercise, that tolerate reporting delays and incomplete disclosure, and that frame regulatory compliance as the ceiling rather than the floor of their environmental obligations, are accumulating narrative risk that compounds over time.

Community water rights are emerging as a particularly high-stakes accountability domain. The combination of heavy metal and radioactive element contamination allegations, asymmetric health impacts on vulnerable populations, and documented reporting deficiencies creates a category of risk that faith-based investors, ESG analysts, and eventually mainstream institutional holders treat with increasing severity.

Mining companies that treat environmental transparency as a strategic asset rather than a compliance burden will be structurally better positioned to retain access to the full spectrum of institutional capital as faith-based, ESG, and regulatory pressures continue to converge.

Rio Tinto has the operational scale and financial resources to address the specific concerns raised by the Jesuits in Britain. The question is whether the company views the engagement as a reputational risk management exercise or as a genuine opportunity to demonstrate that its environmental governance systems are capable of rebuilding institutional trust. The answer will matter not just to the Jesuits in Britain, but to the growing class of investors for whom that distinction defines whether a company belongs in their portfolio at all.

This article is intended for informational purposes only and does not constitute financial advice or an investment recommendation. Statements about potential divestment outcomes, corporate governance trajectories, and market impacts involve forward-looking elements subject to uncertainty. Readers should conduct independent due diligence before making investment decisions.

Want To Stay Ahead of Significant ASX Mineral Discoveries as They Happen?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into clear, actionable insights for investors at every level — explore historic examples of exceptional discovery returns to understand the potential at stake, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.