July 25, 2026

When Geopolitics Breaks the Food Chain: Understanding the Fertilizer Shock and Global Food Crisis

There is a largely invisible architecture that underpins every meal on every table on the planet. It is not built from soil or sunlight alone. It is built from nitrogen, phosphate, potash, and the vast industrial systems that synthesise and ship these nutrients across oceans to reach the fields where food is grown. When that architecture is disrupted, the consequences do not appear immediately at the grocery store. The fertilizer shock and global food crisis travels through a lagged, complex chain of agricultural decisions, growing seasons, and harvest cycles before surfacing as empty shelves or unaffordable prices. That delay is precisely what makes this situation so dangerous, and so easy to underestimate.

When big ASX news breaks, our subscribers know first

The Invisible Engine Behind Modern Food Production

Modern agriculture is fundamentally an energy conversion system. Calories consumed by humans are, in large part, calories originally derived from fossil fuels, transformed through chemical processes into plant nutrients. The most critical of these processes is the Haber-Bosch synthesis of nitrogen fertiliser, which uses natural gas supply as both a feedstock and an energy source to convert atmospheric nitrogen into ammonia, the base compound for urea and other nitrogen-based fertilisers.

This process consumes roughly 1 to 2 percent of total global energy output annually, making fertiliser production one of the most energy-intensive industrial activities on Earth. The concept of embedded energy in food captures this reality: every kilogram of grain, every head of vegetables, carries within it a hidden energy cost absorbed during the fertiliser production process. When that energy supply is disrupted, the shock does not register at the pump or in electricity bills. It registers months later, in diminished harvests.

The transmission mechanism operates through a precise sequence:

- An energy supply disruption elevates natural gas prices.

- Rising gas costs increase the synthesis cost of nitrogen fertiliser, particularly urea.

- Shipping lane restrictions prevent physical delivery of urea and phosphate to importing nations.

- Farmers facing cost pressure or outright supply gaps reduce application rates or delay planting.

- Crop yields compress relative to seasonal projections.

- Food price inflation materialises six to eighteen months after the original energy disruption.

Unlike oil price shocks, which consumers experience within days at the fuel pump, fertiliser shocks operate on a delayed fuse. The full impact on food availability and price often does not surface until the following growing season or beyond. This lag creates a dangerous window during which policymakers can underestimate the severity of what is already in motion.

The Strait of Hormuz: A Multi-Commodity Chokepoint the World Cannot Afford to Lose

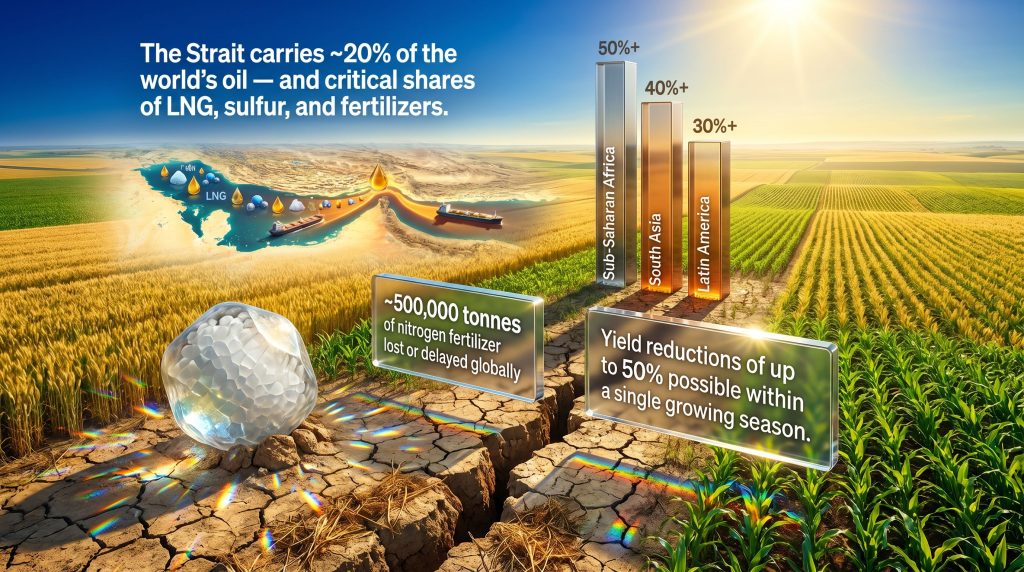

The Strait of Hormuz is a 33-kilometre-wide maritime corridor connecting the Persian Gulf to the Arabian Sea. Under normal operating conditions, approximately 20 percent of the world's oil supply transits this passage. However, framing the Strait solely as an oil route dramatically understates its strategic importance to global food systems.

The Strait simultaneously serves as a critical artery for liquefied natural gas (LNG), sulfur (a primary input for phosphate fertiliser production), ammonia, and finished fertiliser products bound for agricultural markets in Asia, Africa, and Latin America. The Food and Agriculture Organisation of the United Nations (FAO) has explicitly identified this multi-commodity role, warning that the Strait functions as a simultaneous chokepoint for energy and agricultural inputs, making its disruption categorically different from previous supply shocks.

| Commodity Affected | Normal Strait Transit Role | Disruption Impact |

|---|---|---|

| Crude Oil | ~20% of global supply | Severe price spikes, rationing in multiple countries |

| LNG | Significant share of Asian imports | Supply shortfalls, elevated spot prices |

| Urea (Nitrogen Fertiliser) | Major Gulf export corridor | Shipping delays, price surge |

| Sulfur (Phosphate Input) | Key industrial supply route | Phosphate production constraints |

| Ammonia | Regional trade flows | Synthesis cost escalation |

The International Energy Agency (IEA) has assessed that the disruption to Strait transit volumes represents the most severe energy supply crisis in recorded history. Furthermore, the concept of a supply shadow is instructive here: regions fall into fertiliser scarcity not because they border the Gulf, but because global redistribution networks fail to compensate for lost supply volumes. Sub-Saharan Africa, South Asia, and parts of Southeast Asia sit squarely within this shadow.

What the Data Actually Shows: Quantifying the Fertiliser Shortage

Nitrogen: The Most Exposed Input

Urea is the world's most widely traded nitrogen fertiliser. It is synthesised from ammonia, which is produced from natural gas. When LNG prices spike and shipping routes are severed, the cost of urea synthesis rises while physical delivery to import-dependent markets becomes structurally constrained.

Yara International, one of the world's largest fertiliser producers, has quantified the current production gap. Yara CEO Svein Tore Holsether stated in early May 2026 that approximately 500,000 tonnes of nitrogen fertiliser is not being produced globally as a direct result of the Strait disruption (BBC, May 2026). The downstream implications of this shortfall are severe. The Yara CEO warned that the crisis could eliminate as many as 10 billion meals per week globally if conditions persist, and that reduced nitrogen application could compress yields for certain nitrogen-intensive crops by as much as 50 percent within a single growing season.

Phosphate: The Compounding Pressure

Sulfur, a critical input in the conversion of phosphate rock into usable diammonium phosphate (DAP) fertiliser, also transits the Strait in meaningful volumes. Supply tightness in sulfur compounds production constraints across importing regions. In addition, phosphate and potash scarcity creates a multi-nutrient deficit scenario where farmers lack adequate access to both nitrogen and phosphate simultaneously — a condition with significantly worse yield outcomes than a single-nutrient shortage.

The Planting Window Problem

The FAO has emphasised that agriculture operates on a crop calendar that cannot be postponed. Even a shipping disruption of several weeks can produce harvest consequences that only materialise months later. There is no mechanism to retroactively compensate for a missed fertiliser application window.

The current disruption coincides with the prime planting season across the northern hemisphere. Fertiliser application windows are narrow by agronomic necessity: early-season nitrogen application supports root development and canopy establishment in ways that mid-season or late-season applications cannot replicate. The irreversibility of a missed application window is one of the most underappreciated dimensions of this crisis.

Which Regions Bear the Greatest Exposure?

Sub-Saharan Africa: Structural Vulnerability Without Buffer

Approximately 80 percent of fertiliser consumed in sub-Saharan Africa is imported, frequently at freight premiums above European import prices. African smallholder farmers, who collectively produce around 70 percent of the region's food supply, operate with the thinnest financial margins and smallest inventory buffers of any farming demographic in the world.

The International Food Policy Research Institute (IFPRI) has identified sub-Saharan Africa as one of the two regions facing the sharpest near-term food price increases as a consequence of the fertiliser shock. The IFPRI's analysis of the Yara CEO's warning highlights that the shortage risks deepening structural fertiliser underuse across the continent, where application rates are already significantly below agronomic optima. Higher freight costs mean price shocks hit African importers harder and faster than European or North Asian buyers.

South Asia: Scale Compounds Vulnerability

Densely populated nations across South Asia depend heavily on imported fertilisers and natural gas-linked production inputs. India LNG imports policy has introduced an additional complication for global markets: the government has prioritised domestic urea allocation over export commitments, effectively withdrawing supply from global trade at a moment of acute scarcity. While rational from a national food security perspective, this domestic prioritisation worsens the supply picture for other import-dependent nations.

Latin America: Food Exporters Under Input Pressure

Brazil and Argentina together account for approximately 10 percent of global wheat exports, 39 percent of global maize exports, and 66 percent of global soybean exports, according to USDA estimates. Both countries depend heavily on fertiliser imports, with significant volumes historically sourced from Persian Gulf producers.

The critical timing dimension here is often overlooked. Fertiliser bookings for second-half planting seasons in Latin America are placed months in advance. According to IFPRI analysis, both nations are currently engaged in a race to identify alternative supply chains before planting windows close. A failure to secure adequate fertiliser volumes in this procurement window would translate directly into reduced crop output for the 2026/2027 season, with consequences that ripple through global commodity markets.

Southeast Asia and Beyond

The FAO has separately flagged Southeast Asia as a region of particular concern given high import dependency and pre-existing food insecurity in several national contexts. Middle Eastern nations not directly involved in the conflict are also experiencing secondary logistical fragmentation as regional shipping networks reorganise around the disruption. Consequently, resource export disruptions are compounding an already fragile global supply picture for resource export disruptions across multiple regions simultaneously.

Institutional Warnings and Industry Assessments

The World Food Programme's deputy executive director Carl Skau has framed the situation in terms of a two-scenario outlook. In the more severe scenario, yields fall and crop failures materialise across the next growing season. In the comparatively optimistic scenario, higher input costs are absorbed into consumer food prices during the following year (PBS NewsHour, 2026). Neither scenario is benign, and both represent a deterioration from baseline food security conditions for hundreds of millions of people.

The Yara CEO's concern about a global bidding war for food deserves particular attention. In a constrained supply environment, high-income countries possess the foreign exchange capacity to outbid lower-income importers for available fertiliser and food supplies. This crowding-out mechanism can worsen food access inequality even when aggregate global production remains relatively stable.

Holsether specifically called on European nations to consider the implications of price competition for the world's most economically vulnerable populations (BBC, May 2026). The FAO has characterised the situation not merely as a geopolitical disruption but as a direct structural threat to the global agrifood system, projecting that disrupted fertiliser deliveries will reduce yields and tighten food supplies through the second half of 2026 and into 2027.

The next major ASX story will hit our subscribers first

Step-by-Step: How a Fertiliser Shortage Becomes a Food Crisis

Step 1: Farmers in import-dependent regions cannot source nitrogen or phosphate inputs at accessible prices or within required delivery timeframes.

Step 2: Under financial pressure or outright supply failure, farmers apply fertiliser below agronomically optimal rates or forgo application entirely.

Step 3: Crop yields decline relative to baseline projections. For nitrogen-intensive crops, yield reductions of up to 50 percent are possible in severe under-application scenarios.

Step 4: Aggregate food production across affected regions falls below projected levels.

Step 5: Reduced supply against sustained demand drives food price inflation, with the most acute impacts concentrated in nations with limited foreign exchange reserves.

Step 6: Households in lower-income brackets face reduced caloric access as market prices exceed purchasing capacity, triggering escalating food insecurity.

Alternative Suppliers: Can the Gap Be Filled?

| Alternative Supplier | Key Products | Capacity Assessment |

|---|---|---|

| Russia | Urea, Potash, Ammonia | Significant but constrained by sanctions regimes |

| Morocco / OCP Group | Phosphate, DAP | Partial, phosphate-focused, limited nitrogen capacity |

| Canada | Potash | Minimal nitrogen replacement capacity |

| Egypt | Urea | Moderate, domestic demand competes with export availability |

The structural reality is that no single alternative supplier or combination of suppliers can fully compensate for Gulf production and transit losses at the speed required by current planting season timelines. Logistics lead times, storage constraints, and the financial capacity of importing nations to absorb elevated spot prices all limit the practical effectiveness of supply chain diversification in the near term.

Projected Timelines for Impact

| Period | Primary Impact | Most Exposed Regions |

|---|---|---|

| Mid-2026 | Fertiliser price surge, delayed planting decisions | Northern hemisphere, South Asia |

| Late 2026 | Reduced harvest yields, food price inflation | Sub-Saharan Africa, South Asia, Latin America |

| 2027 and beyond | Compounding food insecurity, structural supply gaps | Global, worst outcomes in low-income import-dependent nations |

Could This Crisis Reshape the Long-Term Agricultural Landscape?

Beyond the immediate humanitarian dimensions, the fertilizer shock and global food crisis carries structural implications that extend well beyond the current disruption timeline. Several dynamics are worth tracking:

- Fertiliser use efficiency (FUE) has been a subject of agronomic research for years, and the current shock creates powerful new economic incentives for adoption of precision agriculture technologies including variable-rate application systems, soil sensing, and remote diagnostics. However, technology adoption barriers in smallholder farming systems remain substantial.

- Sovereign stockpiling programmes for fertilisers, analogous to strategic petroleum reserves, may emerge as a standard component of national food security policy. Several governments are already exploring this pathway, though storage capacity and capital constraints limit their near-term scale.

- Regional agricultural trade fragmentation is an underappreciated longer-term risk. If sustained disruption erodes confidence in globally integrated fertiliser and food supply chains, governments may accelerate moves toward regional self-sufficiency, reshaping commodity trade flows for years.

- IFPRI has noted that local fertiliser production capacity expansion in Africa has been chronically insufficient relative to the continent's agricultural needs. The availability of critical raw materials for domestic production remains a significant barrier, though the current crisis may generate the political and financial impetus to change that structural reality.

Frequently Asked Questions

What is causing the current global fertiliser shortage?

The disruption of the Strait of Hormuz following the US-Israeli conflict with Iran has restricted the transit of LNG, urea, sulfur, and finished fertilisers through one of the world's most critical maritime trade corridors. This simultaneously raises the production cost of nitrogen fertilisers (through LNG price increases) and restricts their physical delivery to import-dependent agricultural markets.

How does a fertiliser shortage lead to higher food prices?

Reduced fertiliser access causes farmers to lower application rates, which compresses crop yields. Lower production relative to demand creates supply shortfalls that drive food price inflation, with impacts typically materialising six to eighteen months after the original supply disruption.

Which countries are most at risk?

- Sub-Saharan Africa: 80 percent of fertiliser is imported, smallholder farmers are highly exposed, and freight premiums amplify price shocks.

- South Asia: Large import-dependent populations; India's domestic prioritisation policy withdraws supply from global markets.

- Latin America: Brazil and Argentina face input cost pressure during critical procurement windows for their globally significant crop export production.

What is urea and why does it matter?

Urea is the world's most widely traded nitrogen fertiliser. It is synthesised from ammonia derived from natural gas, and it plays a foundational role in supporting plant growth and maximising crop yields. Disruption to its supply has more immediate yield consequences than shortfalls in most other agricultural inputs.

How long could food price impacts last?

The FAO projects that the effects of disrupted fertiliser deliveries will reduce yields and tighten food supplies through the second half of 2026 and into 2027. If the Strait disruption persists beyond current expectations, compounding effects across multiple growing seasons could extend food price stress well beyond that horizon. The fertilizer shock and global food crisis, consequently, represents one of the most complex and far-reaching humanitarian challenges of the current decade.

Disclaimer: This article contains forward-looking projections sourced from the FAO, IFPRI, Yara International, and the World Food Programme. These projections are inherently uncertain and subject to revision as geopolitical and supply chain conditions evolve. Nothing in this article constitutes financial, investment, or policy advice.

Want to Invest in the Minerals Driving the Search for Food Security Solutions?

As the fertiliser shock reshapes global agricultural supply chains, demand for critical minerals — including phosphate, potash, and the energy commodities underpinning fertiliser synthesis — is intensifying, creating potential opportunities for investors tracking ASX discoveries in real time. Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries across more than 30 commodities, delivering actionable insights before the broader market reacts — explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position ahead of the next major find.