July 20, 2026

Maritime transportation networks face unprecedented stress when strategic waterways become inaccessible, fundamentally disrupting contractual relationships that underpin global energy markets. These disruptions trigger cascading legal mechanisms designed to protect suppliers from performance obligations during extraordinary circumstances, while simultaneously creating supply chain vulnerabilities that ripple through international commodity flows. Furthermore, the declaration of force majeure on oil shipments amid Strait of Hormuz blockade scenarios represents one of the most significant risks facing global energy security.

Understanding Force Majeure in Global Energy Supply Chains

Force majeure provisions serve as critical risk allocation mechanisms within international energy contracts, allowing suppliers to suspend delivery obligations when genuinely unforeseeable events prevent contract fulfillment. These contractual safeguards become particularly relevant during maritime chokepoint disruptions that block traditional shipping routes.

Legal Framework and Contractual Protections

Modern energy contracts incorporate sophisticated force majeure clauses that specify triggering conditions with increasing precision. Industry standard applications include production facility damage from natural disasters, government-imposed export restrictions, transportation infrastructure destruction, and labour strikes affecting critical operations.

Documentation Requirements and Legal Burden

Suppliers invoking force majeure on oil shipments amid Strait of Hormuz blockade scenarios must satisfy stringent legal requirements:

• Written notification within 24-48 hours of the triggering event

• Demonstration that circumstances fall within contractual definitions

• Evidence of reasonable mitigation efforts undertaken

• Ongoing communication regarding situation status and recovery prospects

The legal burden requires suppliers to prove the event occurred genuinely, was unforeseeable in specific terms, remained beyond their control, and that reasonable preventive steps were attempted. Performance must become genuinely impossible rather than merely difficult or expensive.

Historical Precedents in Energy Markets

Qatar LNG Force Majeure (2011-2012)

Qatar Liquefied Gas Company declared force majeure on multiple LNG delivery contracts due to declining North Field reserves, affecting approximately 2 million tons annually of contracted supply. The declarations lasted 18 months while Qatar restructured its export portfolio and implemented production optimisation strategies.

Equatorial Guinea LNG Facility (2013-2014)

EG LNG facility operators invoked force majeure following compressor station damage that reduced facility capacity by 60%. The declaration affected contracts representing 1.5 million tons annually, with recovery taking 14 months due to specialised equipment replacement requirements.

COVID-19 Pandemic Applications (2020-2021)

Multiple oil and gas operators declared force majeure during pandemic restrictions, though courts subsequently disputed whether pandemic conditions met traditional contractual thresholds for extraordinary circumstances beyond supplier control.

When big ASX news breaks, our subscribers know first

How Maritime Chokepoint Disruptions Trigger Supply Chain Failures

Strategic Vulnerability Assessment of Critical Waterways

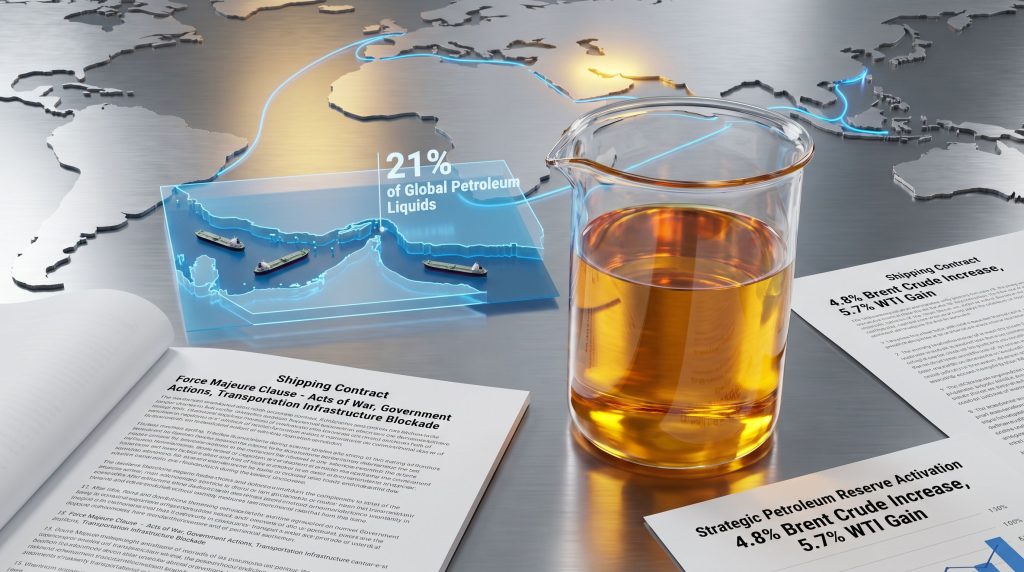

The Strait of Hormuz represents the world's most strategically vulnerable energy transportation corridor, with 21% of global petroleum liquids transiting this narrow waterway annually. According to U.S. Energy Information Administration data, approximately 21 million barrels per day pass through the Strait, creating a single point of failure for global energy supply chains.

In addition to these vulnerabilities, recent oil price rally insights have highlighted how geopolitical tensions can amplify market volatility during supply disruptions.

Geographic and Physical Constraints

| Characteristic | Measurement | Strategic Implication |

|---|---|---|

| Narrowest shipping point | 21 nautical miles | Limited manoeuvring space |

| Established traffic lanes | 2 nautical miles each direction | Congestion vulnerability |

| Annual commercial transits | 18,000-20,000 vessels | High traffic density |

| Deep water channel depth | 800+ metres minimum | Suitable for VLCCs |

The Strait's physical limitations create structural vulnerabilities where relatively small disruptions generate disproportionate global market impacts. International maritime security literature defines chokepoints using specific criteria including geographic constriction, strategic trade importance exceeding 5-10% of global commodity flows, limited alternative routing, and controllability by single jurisdictions.

Alternative Route Analysis and Cost Implications

Cape of Good Hope Routing

When Strait access becomes restricted, tankers must reroute around Africa's southern cape, adding approximately 8,500 nautical miles to typical Gulf-to-Europe journeys. This extended routing increases transportation costs by 30-40% while extending delivery timeframes by 14-21 days, depending on vessel speed and destination ports.

Suez Canal Bypass Options

Alternative Gulf exports through Red Sea routes add roughly 6,000 nautical miles compared to direct Strait transit, generating 15-25% higher transport costs. However, pipeline capacity limitations restrict this alternative to approximately 5-7 million barrels per day maximum throughput across all regional producers.

Overland Pipeline Constraints

Existing pipeline infrastructure provides limited alternatives with significant capacity restrictions. The Trans-Arabian Pipeline system offers partial relief but serves primarily Saudi Arabian production facilities, leaving other regional producers completely dependent on maritime routes through the Strait.

Economic Modelling of Supply Disruption Scenarios

Short-Term Market Response Mechanisms

When major suppliers simultaneously declare force majeure on oil shipments amid Strait of Hormuz blockade, markets experience rapid price discovery as traders quantify immediate supply gaps and longer-term availability concerns. Historical precedents suggest initial market reactions represent only preliminary adjustments to more dramatic sustained price movements.

Moreover, understanding OPEC production impact becomes crucial during these scenarios, as coordination among major producers can either stabilise or exacerbate market volatility.

Strategic Petroleum Reserve Activation

Global strategic petroleum reserves provide temporary supply buffers during crisis periods:

| Reserve Holder | Capacity (Million Barrels) | Maximum Daily Release | Duration at Peak Rate |

|---|---|---|---|

| United States | 714 | 4.4 million | 162 days |

| China | 500-700 (estimated) | 1.5-2.0 million | 250-467 days |

| European Union | 120+ (collective) | 1.2 million | 100 days |

| Japan | 145+ | 0.8 million | 181 days |

These reserves can collectively provide approximately 7.9-8.4 million barrels per day for 100-180 days, potentially offsetting significant portions of Gulf supply disruptions during extended crises.

Regional Producer Dependencies and Vulnerabilities

Kuwait's Strategic Position

Kuwait's geographic location creates complete dependence on Strait of Hormuz access for seaborne crude exports, with zero alternative routing capacity. According to Reuters reports, Kuwait recently faced such challenges when declaring force majeure on oil shipments amid regional tensions. Historical production data shows Kuwait typically exports 2.4-2.8 million barrels daily, representing nearly 85% of total production for revenue generation.

Unlike Saudi Arabia, which maintains limited Red Sea export capability via the Yanbu pipeline system, Kuwait possesses no geographic alternatives to Gulf export terminals. This creates what energy security analysts term structural vulnerability that cannot be mitigated through infrastructure diversification.

Comparative Regional Exposure Analysis

| Producer | Daily Production | Gulf Export Dependency | Alternative Capacity |

|---|---|---|---|

| Saudi Arabia | 10.1 million bbl/day | ~70% of exports | 5 million bbl/day (Yanbu) |

| Iraq | 4.5 million bbl/day | ~95% (southern fields) | 0.6 million bbl/day (Turkey) |

| UAE | 3.2 million bbl/day | ~85% | Minimal |

| Kuwait | 2.7 million bbl/day | ~100% seaborne | None |

| Iran | 3.0-3.2 million bbl/day | ~95% | Limited overland |

This analysis reveals asymmetric vulnerability patterns, with Kuwait and Iraq facing the highest exposure to Strait disruptions relative to their total export capacity.

Risk Management Frameworks for Energy Market Participants

Corporate Response Strategies During Force Majeure Events

Energy companies operating in affected regions implement tiered response protocols designed to balance operational continuity with contractual obligations during crisis periods.

Immediate Assessment Phase (0-48 Hours)

• Operational safety evaluation and personnel security assessment

• Contract review and legal consultation regarding force majeure provisions

• Customer notification preparation and communication strategy development

• Alternative logistics assessment and transportation route evaluation

Short-Term Mitigation (2-30 Days)

• Force majeure declaration filing with proper documentation

• Alternative delivery route exploration and cost analysis

• Production rate adjustment to match available transportation capacity

• Inventory management optimisation to maintain operational flexibility

Extended Disruption Planning (30+ Days)

• Contract renegotiation initiation with affected customers

• Alternative market development and customer diversification

• Infrastructure investment evaluation for future risk mitigation

• Political risk insurance claims processing and recovery planning

Downstream Market Participant Adaptations

Refinery Feedstock Substitution Requirements

Refineries dependent on Gulf crude face immediate operational challenges requiring rapid feedstock substitution and process optimisation when suppliers declare force majeure:

| Original Crude Type | Substitute Options | Processing Adjustments | Yield Impact |

|---|---|---|---|

| Kuwait Export Crude | West Texas Intermediate | Reduced heavy fuel production | +3-5% petrol yield |

| Iraqi Basra Light | Norwegian Johan Sverdrup | Desulfurisation modifications | Similar product slate |

| Saudi Arab Light | Brazilian Lula | Density compensation | +2% middle distillate |

These substitutions require significant operational adjustments including equipment reconfiguration, process parameter modifications, and product quality monitoring to maintain refining efficiency and output specifications.

Long-Term Strategic Implications for Global Energy Security

Infrastructure Investment Acceleration

Sustained chokepoint disruptions historically accelerate strategic infrastructure investments designed to reduce single-point-of-failure vulnerabilities across global energy transportation networks.

However, the broader implications extend beyond energy security, as tariffs impact on markets can compound these vulnerabilities through trade policy disruptions.

Pipeline Development Priorities

Regional producers prioritise pipeline capacity expansion projects following major maritime disruptions:

• Trans-Arabian Pipeline capacity enhancement from 5 million to 8+ million barrels daily

• East-West crude oil pipeline development connecting Gulf production to Red Sea terminals

• Strategic petroleum product pipeline networks for refined product distribution

• Cross-border interconnection projects enabling supply diversification

Alternative Transportation Infrastructure

• Rail transportation capacity expansion for petroleum product movement

• Strategic storage facility positioning near alternative export terminals

• Emergency response capability enhancement including vessel chartering agreements

• Cross-regional supply chain integration projects

Geopolitical Risk Pricing Evolution

Insurance Market Adaptations

Marine cargo and political risk insurance markets rapidly adjust pricing models following major chokepoint disruptions, incorporating enhanced risk assessment methodologies:

• War risk premium calculations reflecting regional stability assessments

• Transit route diversification requirements for coverage eligibility

• Coverage exclusion refinements based on evolving threat patterns

• Claims processing acceleration protocols for crisis response

Contract Structure Evolution

Long-term energy supply contracts increasingly incorporate sophisticated provisions designed to maintain supply security during crisis periods:

• Enhanced force majeure definitions with specific geographic trigger events

• Alternative delivery mechanism specifications including route substitution

• Graduated pricing structures reflecting transportation cost variations

• Shared risk allocation frameworks between suppliers and purchasers

Downstream Supply Chain Resilience Strategies

Strategic Inventory Management

Energy market participants develop enhanced inventory strategies recognising chokepoint vulnerability patterns and regional supply concentration risks.

Commercial Storage Optimisation

• Crude oil storage capacity expansion near alternative transportation hubs

• Product inventory diversification across multiple geographic regions

• Seasonal stock building programmes anticipating potential disruption periods

• Emergency reserve protocols coordinated with national strategic petroleum programmes

Supply Chain Diversification

• Multi-region sourcing strategies reducing dependence on single geographic areas

• Long-term contract portfolio balancing across diverse supplier bases

• Transportation route flexibility incorporating multiple shipping alternatives

• Regional refining capacity development reducing import dependence

Technology Integration for Crisis Response

Real-Time Monitoring Systems

• Satellite tracking integration for vessel movement and route optimisation

• Automated contract monitoring systems triggering force majeure protocols

• Supply chain visibility platforms enabling rapid alternative sourcing

• Predictive analytics for disruption probability assessment and preparation

Digital Contract Management

• Smart contract integration enabling automated force majeure declaration processing

• Blockchain-based documentation systems ensuring secure record keeping

• Digital communication platforms facilitating crisis coordination

• Automated alternative sourcing systems activating during supply disruptions

The next major ASX story will hit our subscribers first

Market Psychology and Investor Behaviour During Supply Crises

Price Discovery Mechanisms

Energy market price discovery during force majeure on oil shipments amid Strait of Hormuz blockade scenarios follows predictable patterns reflecting supply uncertainty quantification and risk premium incorporation.

Consequently, these disruptions often coincide with broader economic uncertainties, as highlighted in analyses of US economic pressures that can amplify market volatility.

Volatility Amplification Factors

• Speculative trading activity increases exponentially during crisis periods

• Algorithmic trading systems amplify price movements based on news sentiment

• Physical market participants compete aggressively for available supplies

• Financial market participants incorporate extended uncertainty periods into pricing models

Risk Premium Calculations

Market participants incorporate multiple risk factors when pricing energy commodities during chokepoint disruptions:

• Disruption duration probability assessments ranging from weeks to months

• Alternative supply availability and transportation cost premiums

• Strategic petroleum reserve utilisation scenarios and replacement costs

• Geopolitical escalation probability and expanded disruption scenarios

Investment Strategy Implications

Energy Security Investment Themes

• Pipeline infrastructure companies benefiting from route diversification demand

• Strategic storage facility operators experiencing increased utilisation rates

• Alternative energy transportation companies including rail and truck logistics

• Energy efficiency technology providers reducing overall consumption requirements

Portfolio Risk Management

Institutional investors adjust portfolio allocations recognising chokepoint vulnerability patterns and regional supply concentration exposures across energy sector investments and broader economic implications.

Furthermore, comprehensive analysis of global recession insights reveals how energy supply disruptions can catalyse broader economic downturns, making risk management even more critical.

What Triggers Force Majeure Declarations in Oil Markets?

Force majeure declarations typically stem from events genuinely beyond operator control, including natural disasters, political instability, infrastructure destruction, or regulatory restrictions that prevent contract performance.

How Long Do Force Majeure Periods Typically Last?

Duration varies significantly based on underlying causes, ranging from weeks for temporary disruptions to multiple years for major infrastructure reconstruction projects or sustained geopolitical conflicts.

Industry analysis from Oil Price suggests that recent declarations reflect escalating regional tensions that could persist for extended periods.

Can Buyers Challenge Force Majeure Declarations?

Buyers can dispute declarations through arbitration or court proceedings, challenging whether events truly meet contractual definitions or whether suppliers failed to implement reasonable mitigation measures.

Disclaimer: This analysis presents hypothetical scenarios for educational purposes regarding energy market dynamics and contractual mechanisms. Specific market movements, force majeure declarations, and supply disruptions referenced may represent forward-looking scenarios rather than verified historical events. Readers should conduct independent research and consult qualified professionals before making investment or business decisions based on this information.

Ready to Navigate Market Volatility from Energy Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify opportunities that often emerge during global commodity market disruptions. Explore how major discoveries can generate substantial returns by examining Discovery Alert's track record, then begin your 14-day free trial today to position yourself ahead of market volatility.