June 27, 2026

The Processing Chokepoint That Redefined Global Trade Strategy

When historians examine the structural turning points in twenty-first century geopolitics, the gradual weaponisation of mineral processing capacity may rank alongside oil embargoes and semiconductor controls as a defining inflection point. Unlike most commodity markets, where production is spread across dozens of countries and pricing reflects genuine competitive dynamics, critical mineral supply chains operate on an entirely different logic. The bottleneck is not the ground itself but what happens after ore is extracted, and that bottleneck sits overwhelmingly within a single country's industrial infrastructure.

This reality arrived at the centre of global trade diplomacy on 6 May 2026, when G7 critical minerals trade talks convened in Paris with mineral supply security explicitly positioned as the most urgent structural challenge facing member economies. The gathering, held under France's G7 presidency, produced a joint statement committing member nations to ensure that attempts to weaponise economic dependencies would fail. However, beneath that unified language, significant fault lines remained, both between Washington and Brussels and between competing visions for how the West can realistically disentangle itself from Chinese supply chain dominance.

When big ASX news breaks, our subscribers know first

Why Mineral Processing Concentration Is Strategically Different From Mining Concentration

Understanding why G7 critical minerals trade talks have become so politically charged requires distinguishing between two different kinds of market power. Mining concentration, where one country produces a disproportionate share of raw ore, creates leverage but remains vulnerable to disruption by competing producers. Processing concentration, by contrast, creates near-irreversible structural dependency because processing infrastructure, refineries, separation plants, and metallurgical facilities require decades of industrial investment and specialised expertise to replicate.

China has achieved dominance across both dimensions for rare earth elements and a wide range of other critical minerals, but its processing advantage is the more strategically durable of the two. Even where ore deposits exist in Australia, Canada, Africa, or South America, the refined materials required by EV manufacturers, defence contractors, and electronics producers flow almost entirely through Chinese facilities before reaching end users. The critical minerals demand surge projected for this decade only intensifies that dependency.

French Finance Minister Roland Lescure articulated this dynamic plainly during the Paris talks, noting that China's concentration across mineral markets used in electric vehicles, wind turbines, consumer electronics, and defence systems is significant enough that it can move pricing to levels that eliminate competing producers from commercial viability. This is not conventional market competition. It describes a form of structural pricing power that functions below the threshold of traditional trade warfare, making it difficult to challenge through standard WTO mechanisms.

The strategic implication is stark: a nation does not need export bans to control a supply chain. The ability to suppress prices long enough to bankrupt alternative producers achieves the same result with far greater deniability.

What the G7 Paris Meeting Actually Produced

The 6 May 2026 G7 trade ministers meeting brought together key figures from across the alliance, including France's Foreign Trade Minister Nicolas Forissier, EU Trade Commissioner Maros Sefcovic, US Trade Representative Jamieson Greer, and German Economy Minister Katherina Reiche. France's goals for the session were explicitly ambitious. Forissier framed concrete progress on rare earths and critical mineral supply chains as a flagship deliverable ahead of the mid-June G7 leaders' summit, describing the objective as ensuring that G7 economies are not held hostage by foreign suppliers.

The collective statement issued after the meeting drew on this framing, committing member nations to building resilient supply chains that cannot be leveraged for geopolitical coercion. However, the agreement masked genuine divergence on implementation. Officials familiar with the discussions confirmed that while broad consensus existed on the need to reduce Chinese supply dependency, two competing frameworks remained unresolved: one from the European side and one from the United States.

The European approach leans toward regulatory mandates, including quota systems and mandatory supply chain diversification requirements for companies operating in strategic sectors. The American approach under the Trump administration emphasises bilateral mineral framework agreements and price floor mechanisms negotiated directly with resource-holding nations. These frameworks reflect a deeper philosophical divide between Brussels, which tends toward regulatory architecture, and Washington, which under the current administration favours executive-directed bilateral deal-making.

The Transatlantic Fault Line: Automotive Tariffs Complicating Mineral Unity

Overlaying the minerals agenda was a separate and potentially destabilising dispute over automobiles. President Trump's statement that the US would raise tariffs on EU-manufactured cars from 15% to 25% introduced significant friction into what was meant to be a unified G7 session. The proposed increase, a 67% escalation in tariff rates, directly impacts Germany's automotive export sector, which is already navigating weakening Chinese demand, slower global growth, and elevated labour and input costs.

Forissier characterised Trump's tariff comments not as a breakdown but as pressure toward faster implementation of the Turnberry Agreement, the trade framework negotiated between the US and EU in Scotland in 2025. EU Trade Commissioner Sefcovic confirmed that he and Greer had discussed Turnberry implementation during a bilateral meeting in Paris the previous day, with both sides emphasising that delivering on commitments made in Scotland remained the shared priority.

German Economy Minister Katherina Reiche confirmed that intensive bilateral negotiations with US counterparts were actively underway. Meanwhile, EU lawmakers were working to finalise common legislative text to implement the Turnberry framework, though internal EU divisions over safeguard provisions were slowing the process.

The automotive tariff dispute illustrates a structural tension within the G7 mineral agenda: achieving supply chain unity against China requires internal trade cohesion, but bilateral US trade pressures are generating exactly the kind of friction that undermines multilateral coordination.

According to reporting from Reuters on the Paris talks, the ministers were acutely aware that internal divisions risked undermining the very unity the joint statement sought to project.

The Strategic Architecture Already in Place

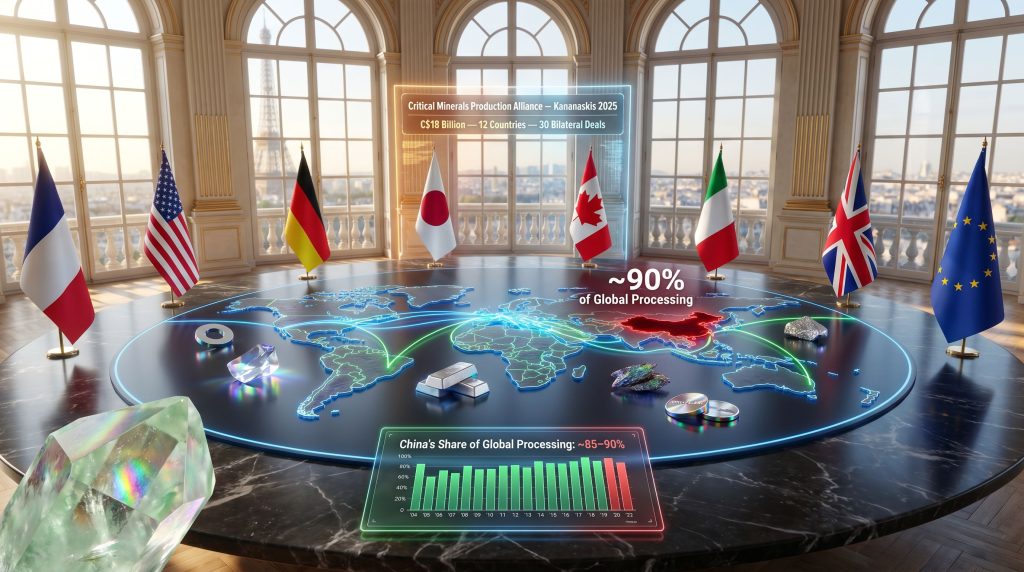

The Paris talks did not occur in a vacuum. The G7 has been constructing institutional infrastructure for strategic supply chain transformation since at least mid-2025. The Critical Minerals Production Alliance, established at the G7 Leaders' Summit in Kananaskis, Alberta in June 2025, represents the most comprehensive multilateral framework assembled to address Chinese market concentration. The Alliance operates across three strategic pillars:

-

Standards-Based Marketplace Development establishes traceability benchmarks and responsible sourcing thresholds, creating preferential trade conditions for nations meeting compliance requirements.

-

Capital Mobilisation coordinates financing across multilateral development banks, private sector lenders, and G7 sovereign financing vehicles, with the objective of making Western-backed projects commercially competitive against Chinese-financed alternatives.

-

Innovation and R&D Collaboration targets processing technology, extraction efficiency improvements, and supply chain resilience through coordinated research programmes across member nations.

Canada has emerged as one of the most active participants in translating this architecture into tangible outcomes. Since October 2025, Canada has signed approximately 30 bilateral deals with 12 countries, representing roughly C$18 billion in mining and technology investments. Those agreements span materials including graphite, rare earth elements such as scandium and gadolinium, lithium, and nickel, with linkages explicitly made to NATO defence spending commitments. An estimated C$6.4 billion of that investment capacity connects directly to defence and advanced manufacturing capability.

Australia joined the G7 critical minerals production framework in March 2025, expanding the coalition beyond the core seven nations. South Korea, India, and other resource-significant economies have been incorporated as partner countries within the broader structure.

Competing National Strategies Within the G7

One of the more analytically interesting features of the current G7 critical minerals trade talks is that member nations are not pursuing a single unified strategy. Instead, a range of distinct national approaches are operating simultaneously, creating both complementary coverage and potential fragmentation risk.

| Nation / Bloc | Primary Strategic Approach | Core Mechanism |

|---|---|---|

| France | Supply chain regulation | Import quotas; mandatory diversification for strategic sectors |

| Japan | Investment-led diversification | Subsidies for Western Hemisphere mining and processing projects |

| Canada | Collective procurement | Coordinated "buyers' club" sourcing model |

| United States | Bilateral deal-making | Mineral framework agreements; price floor mechanisms |

| European Union | Regulatory and diplomatic | EU Critical Raw Materials Act; parallel China engagement |

The US bilateral track deserves particular attention. Under the Trump administration, the United States has negotiated or initiated mineral framework agreements with a range of nations including Australia, Japan, Malaysia, Thailand, Ukraine, Saudi Arabia, the Democratic Republic of Congo, and Pakistan. This creates what analysts describe as a hub-and-spoke architecture, with Washington at the centre of a network of bilateral supply commitments that may operate in parallel to, or occasionally in tension with, the multilateral G7 framework.

Furthermore, Japan's subsidy-led approach addresses a different but equally critical problem: commercial viability. Many Western Hemisphere mining and processing projects remain structurally uncompetitive against Chinese-backed alternatives due to higher labour costs, stricter environmental permitting requirements, and longer project development timelines. Direct subsidisation of qualifying projects reduces this gap, but requires sustained fiscal commitment across multiple political cycles, a challenge for any democratic government.

China's Export Controls: The Catalyst That Accelerated Everything

The urgency driving these negotiations was significantly amplified by China's rare earth export restrictions in 2025, imposed in direct response to US tariff measures. This action demonstrated what Roland Lescure's price-suppression argument had implied: that Beijing was willing to deploy its supply chain position as an active geopolitical instrument rather than merely a passive economic advantage.

The export controls validated years of warnings from Western analysts about the risks of concentrated mineral dependency. They also provided political cover for the scale of capital commitment and regulatory intervention required to build genuinely competitive alternatives. Before the controls, supply chain diversification was a medium-term aspiration. After them, it became a strategic imperative with measurable urgency.

From an investor perspective, this shift has significant implications. Projects and companies operating in critical mineral supply chains outside China moved from niche strategic interest to front-line geopolitical assets. The policy environment supporting diversification projects has strengthened materially, though investors should note that policy support does not guarantee commercial outcomes, and the timeline for developing competitive non-Chinese processing infrastructure is measured in decades, not years.

The next major ASX story will hit our subscribers first

The Institutional Architecture Question: Building for Durability

One of the most consequential discussions emerging from the Paris meeting concerns whether the G7 critical minerals agenda can be institutionalised beyond the annual summit cycle. Discussions are underway to establish a permanent dedicated unit within the G7 framework to provide ongoing oversight of the mineral supply chain agenda.

The rationale is straightforward: critical mineral supply chain transformation operates on decade-long capital cycles that are fundamentally incompatible with annual summit communiqués as the primary governance mechanism. A permanent oversight body would provide:

- Continuity of strategic direction across rotating G7 presidencies

- Coordinated monitoring of alliance commitments and capital deployment

- A dispute resolution mechanism for divergent national approaches

- Sustained engagement with partner nations in Africa, Latin America, and Asia

France's G7 presidency has positioned this institutional question as a priority deliverable for the mid-June 2026 leaders' summit. Whether it achieves consensus will depend in part on whether the automotive tariff dispute can be contained before it contaminates broader G7 cooperation dynamics.

Risks That Could Derail the Western Minerals Agenda

Strategic ambition and institutional architecture are necessary but not sufficient conditions for supply chain transformation. Several structural risks could impede the G7's critical minerals objectives:

Internal Cohesion Fragility

The US-EU automotive tariff dispute is a live demonstration that G7 unity is not automatic. Bilateral US trade pressure on European partners can fracture exactly the kind of coordinated action required for effective mineral supply chain diversification. If member nations are simultaneously negotiating against each other on trade, building a unified front against Chinese dominance becomes structurally difficult.

Commercial Viability Gaps

Western mining and processing projects continue to face significant cost disadvantages relative to Chinese-backed competitors. Higher environmental compliance costs, longer permitting timelines, and greater labour cost structures create permanent headwinds. Japan's proposed subsidy approach addresses this directly, but subsidy programmes require sustained political commitment and fiscal capacity that may not survive government changes.

Resource Holder Leverage

Nations in Africa, Latin America, and Southeast Asia that hold significant critical mineral deposits are increasingly sophisticated about playing competing powers against each other to maximise deal terms. The G7 cannot simply dictate supply arrangements. Partner nations will seek maximum concessions, and some will prioritise Chinese offers if they provide better infrastructure, technology transfer, or financing terms. Consequently, Europe's critical minerals supply chain strategy has had to adapt its engagement approach considerably with these resource-holding nations.

The Durability of Diplomatic Truces

Even if US-China negotiations produce short-term relief on export controls, the G7's own strategic assessment holds that negotiated agreements cannot substitute for structural supply chain diversification. History suggests that diplomatic commitments in strategic industries are fragile when geopolitical incentives shift.

WTO Reform Gridlock

The Paris meeting also addressed Chinese industrial overcapacity and WTO reform. Beijing's state-subsidised overproduction across critical mineral sectors creates pricing distortions that undermine Western alternatives. As analysis from The Straits Times noted, reforming WTO mechanisms to address state-directed overcapacity has historically proceeded at glacial speed, leaving Western producers exposed to market distortion for years even under optimistic reform scenarios.

Key Milestones Shaping the G7 Minerals Agenda

| Date | Event |

|---|---|

| March 2025 | Australia joins G7 critical minerals production framework |

| June 2025 | Critical Minerals Production Alliance launched at Kananaskis G7 Summit |

| October 2025 | Canada announces 26 investments and C$18B in bilateral deals across 12 countries |

| 2025 | China imposes rare earth export controls in response to US tariff measures |

| May 6, 2026 | G7 trade ministers convene in Paris; joint statement on weaponised dependencies issued |

| Mid-June 2026 | G7 Leaders' Summit; critical minerals expected as flagship deliverable |

| July 13, 2026 | First status update due on US Commerce/USTR critical minerals negotiations (180-day directive deadline) |

The Defence and Energy Transition Nexus

Critical minerals sit at the intersection of two of the most consequential policy domains of the 2020s: defence modernisation and the clean energy transition. G7 initiatives explicitly connect mineral supply security to NATO defence spending obligations, and for good reason. Considerations of energy security and critical minerals have become inseparable from broader national security frameworks across the alliance.

Rare earth permanent magnets are essential components in precision-guided munitions, radar systems, satellite technology platforms, and next-generation fighter aircraft. Supply chain vulnerability in these inputs is now formally classified as a national security issue, not merely a trade or economic concern.

The clean energy transition compounds this challenge. EV manufacturing, grid-scale battery storage, and offshore wind energy all depend on the same mineral supply chains currently dominated by Chinese processing infrastructure. G7 nations face what might be described as a strategic paradox: achieving the energy transition they have publicly committed to requires scaling mineral supply chains that, at present, run almost entirely through a geopolitical competitor. The rare earth supply chain importance to both defence and clean energy objectives cannot be overstated in this context.

The Production Alliance framework is structurally designed to resolve this paradox by building alternative supply infrastructure before the energy transition reaches peak mineral demand. Whether the capital mobilisation and institutional coordination required can be achieved at sufficient speed remains the central unresolved question of the G7 critical minerals trade talks, and one that the mid-June 2026 leaders' summit will need to address with considerably more specificity than Paris provided.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and analyses of policy outcomes involve inherent uncertainty. Readers should conduct independent research before making investment decisions related to companies or sectors discussed.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths, lithium, nickel, and more than 30 other commodities — turning complex data into actionable investment insights before the broader market reacts. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself at the forefront of the critical minerals opportunity.