June 23, 2026

The Hidden Economics of Brownfield Gold: Why Permitted Past-Producers Are Junior Mining's Most Coveted Asset Class

Across the junior mining sector, a quiet but powerful capital reallocation is underway. Investors and developers alike are increasingly turning away from the speculative romance of greenfield exploration and towards something far more pragmatic: permitted, past-producing assets with established infrastructure and documented resource bases. In an environment where gold price outlook indicators have climbed to multi-year highs and permitting timelines in many jurisdictions stretch beyond a decade, the scarcity value of a fully approved, previously operational gold mine has never been more commercially significant.

It is against this backdrop that Galantas acquires Andacollo Oro project in Chile takes on a meaning well beyond a single corporate transaction. This deal represents a case study in how capital-efficient brownfield M&A is reshaping junior gold development strategy across Latin America in 2026.

When big ASX news breaks, our subscribers know first

Chile's Coquimbo Region: A Tier-1 District With Underappreciated Gold Potential

When mining investors think of Chile, copper dominates the conversation. The country's position as the world's leading copper producer, responsible for roughly 27% of global supply according to the U.S. Geological Survey, tends to overshadow its equally compelling gold endowment. Yet the Coquimbo Region, situated in north-central Chile approximately 55 km southeast of La Serena, has a well-documented track record as a producing gold and copper district with geological characteristics that continue to attract serious developer interest.

Coquimbo sits within the Chilean Iron Belt, a north-south trending metallogenic province that hosts IOCG deposits alongside porphyry and epithermal gold systems. This geological diversity creates a district with multiple deposit types and therefore multiple entry points for developers at different stages of the capital cycle. For junior gold companies specifically, the region offers something increasingly rare: brownfield opportunities with existing permits, community relationships, and operational precedent.

Chile's regulatory framework, administered through a combination of SERNAGEOMIN (the National Geology and Mining Service) and the SEA (Servicio de Evaluación Ambiental), is comparatively transparent by Latin American standards. While Chile has introduced revisions to its mining royalty structure in recent years, its underlying permitting and environmental approval system remains one of the more predictable in the region — a factor that matters enormously when developers are modelling capital deployment timelines.

Understanding the Andacollo Oro Gold Project: Asset Depth Before the Deal

A Production History That Sets This Asset Apart

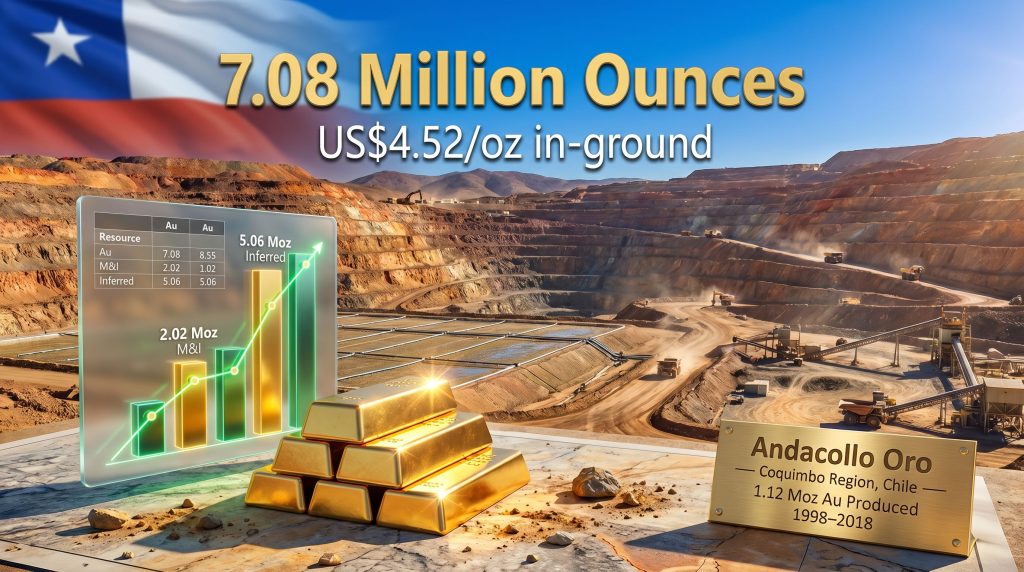

The Andacollo Oro Gold Project is not a speculative exploration-stage deposit. It is a large-scale, open-pit heap leach gold operation with a production history spanning two decades. Between 1998 and 2018, the project produced approximately 1.12 million ounces of gold, with peak annual output reaching 125,000 ounces during its most productive years. That production history is not merely a marketing point; it carries profound technical and economic implications for any developer assessing restart feasibility.

From a geological standpoint, a mine that operated continuously for twenty years has generated an exceptionally rich technical dataset. Drill logs, metallurgical recovery data, grade control records, geotechnical assessments, and hydrological studies accumulated over two decades of operation provide incoming owners with a level of subsurface understanding that no amount of pre-feasibility drilling on a greenfield site could replicate in a comparable timeframe. This informational asset is frequently undervalued in headline acquisition price discussions but represents significant embedded value for developers planning restart programmes.

The Resource Base: Scale, Grade, and Conversion Opportunity

The Andacollo Oro resource base is substantial, even by mid-tier development standards. The table below summarises the project's current resource inventory:

| Resource Category | Tonnage | Grade (g/t Au) | Contained Gold |

|---|---|---|---|

| Measured and Indicated | 130 Mt | 0.48 | 2.02 Moz Au |

| Inferred | 358 Mt | 0.45 | 5.06 Moz Au |

| Total | 488 Mt | ~0.46 | ~7.08 Moz Au |

A grade of 0.48 g/t Au in the Measured and Indicated categories is competitive for open-pit heap leach operations globally. Furthermore, understanding the cut-off grade economics is essential here — heap leach gold operations typically require minimum economic grades ranging from approximately 0.3 g/t to 0.6 g/t depending on strip ratios, reagent costs, and metallurgical recovery rates. Andacollo Oro's M&I grade sits comfortably within that economic window, particularly given the existing infrastructure that would reduce capital intensity at restart.

Perhaps the most strategically significant feature of the resource is the ratio of Inferred to Measured and Indicated ounces. With 5.06 Moz Au sitting in the Inferred category against 2.02 Moz Au in M&I, the project carries a substantial resource conversion opportunity. In practical terms, targeted infill drilling across the Inferred inventory could materially upgrade the project's economic profile before a final production decision is made. This optionality is embedded in the acquisition price and represents a potential value unlock that does not require a single ounce to be mined.

How Was the Acquisition Structured? Deal Architecture and Risk Distribution

The Layered Corporate Structure: Why It Matters

Galantas Gold did not acquire the Andacollo Oro project directly. Instead, the company acquired 100% of Sol de Oro Mining Ltd., which wholly owns Compañía Minera OXI SpA, which in turn holds Dragones SpA, the registered Chilean entity that controls the project. This nested corporate structure is a deliberate and commonly used approach in Latin American mining transactions.

The strategic logic is straightforward: by acquiring the holding company rather than the underlying Chilean mining concessions directly, Galantas inherits all existing contracts, environmental approvals, community agreements, and operational permits without triggering the re-permitting obligations that would arise from a direct asset transfer under Chilean regulatory frameworks. For developers targeting a 2027 production restart, this structural efficiency is not a minor procedural detail — it is a material time and capital saving.

Payment Staging: Preserving Liquidity While Locking In the Asset

The total consideration comprises US$32 million in staged cash payments spread across four years, plus the assumption of approximately US$3.0 million in existing project debt, bringing total effective consideration to approximately US$35 million. The staged payment model deserves analytical attention beyond its face value.

Staged acquisition structures in junior mining serve a dual function: they reduce the buyer's immediate capital burden while simultaneously signalling that the vendor retains sufficient confidence in the asset's development potential to accept deferred payment rather than demanding full upfront consideration.

The comparison below illustrates how different payment architectures distribute risk across buyer and seller:

| Payment Structure | Upfront Capital Risk | Seller Confidence Signal | Buyer Cash Flow Pressure |

|---|---|---|---|

| Lump-Sum | High | High | Immediate |

| Staged Over 4 Years | Moderate | Moderate to High | Distributed |

| Royalty-Based | Low | Variable | Long-term |

For Galantas Gold, the four-year payment runway allows the company to pursue restart financing without being simultaneously constrained by acquisition debt servicing. Consequently, management can allocate capital planning attention towards restart engineering studies and potential drilling programmes rather than immediate debt reduction.

Transaction Approval: Near-Unanimous Shareholder Endorsement

Shareholder support for the transaction was exceptional. At the vote conducted on June 15, 2026, 99.99% of votes cast were in favour of the acquisition — a figure that reflects not just institutional confidence but the absence of any meaningful opposition among retail shareholders. The transaction received conditional approval from the TSX Venture Exchange, with final exchange approval confirmed by June 2026. The deal formally closed during the same month.

The Environmental Approval Factor: Chile's SEA Confirmation as a De-Risking Catalyst

What No New Permitting Actually Means in Practice

Chile's Sistema de Evaluación de Impacto Ambiental is the country's primary gateway for assessing the environmental viability of industrial projects. For mining operations, SEA approval is typically the longest-lead and highest-uncertainty item in the development timeline. Projects in comparable Latin American jurisdictions have experienced delays of three to seven years navigating environmental review processes, with some projects facing outright rejection after multi-year assessment periods.

The SEA's confirmation that Andacollo Oro's existing environmental approval remains valid for both restart operations and life extension effectively removes this risk category from the development equation entirely. This is not a trivial distinction. It means that Galantas Gold can advance directly from acquisition to engineering and restart planning without the uncertainty of an open environmental review process hanging over capital allocation decisions.

Water Access: The Operational Risk That Demands Attention

Coquimbo is one of Chile's driest regions, and the country as a whole has experienced persistent drought conditions affecting multiple consecutive water years. For a heap leach operation, water management is a central operational variable. Heap leach gold recovery relies on the continuous application of cyanide solution across ore stacks, followed by carbon adsorption or Merrill-Crowe precipitation to extract gold from the pregnant leach solution.

This process requires reliable water access and robust solution recycling infrastructure to minimise freshwater consumption. The Andacollo district has existing water management infrastructure from its operational period, including solution ponds and recycling circuits. However, any restart programme will need to demonstrate compliance with Chile's evolving water rights framework, particularly given increased regulatory scrutiny of mining operations in water-stressed watersheds. This is a known and manageable risk, but one that investors should model explicitly when evaluating development timeline and capital cost assumptions.

Three Restart Scenarios: What the Path to 2027 Production Could Look Like

Scenario A: Phased Heap Leach Reactivation

The lowest-capital, fastest-to-cash-flow pathway involves reactivating existing heap leach infrastructure in a phased sequence. This approach targets the 2.02 Moz M&I resource base using already-constructed leach pads, solution ponds, and gold recovery circuits. The primary technical risk unique to this scenario involves the multi-year operational pause between 2018 and 2026.

Residual solution chemistry within dormant leach pads can alter liner integrity and solution management parameters in ways that require careful assessment before full reactivation. This is a solvable engineering challenge, not a fundamental barrier, but it demands thorough technical remediation planning.

Scenario B: Full-Scale Open-Pit Resumption

A more aggressive restart targets the full operational scale that the project achieved at peak output, approaching the historical maximum of 125,000 oz Au per annum. This scenario requires higher upfront capital for equipment mobilisation, mining fleet reactivation, and potential infrastructure upgrades, but delivers proportionally greater cash flow once operational.

The viability of this pathway is highly sensitive to the gold price trajectory through the second half of 2026 and into 2027, as well as Galantas Gold's ability to secure restart financing at acceptable terms.

Scenario C: Inferred Resource Conversion First

The most patient but potentially most value-accretive strategy involves prioritising infill drilling across the 5.06 Moz Inferred inventory before committing restart capital. Interpreting gold drilling results from an infill programme at Andacollo Oro could convert a meaningful portion of Inferred ounces to the Indicated or Measured category, materially strengthening the project's economic study inputs and potentially improving financing terms for the ultimate restart programme. The tradeoff is timeline: resource conversion drilling typically requires twelve to twenty-four months before results can be incorporated into an updated resource estimate.

The strategic tension at the heart of Galantas Gold's near-term decision-making is a classic junior mining dilemma: prioritise early cash flow using existing resources, or invest time and capital in upgrading the resource base to optimise long-term project economics. The company's financing position and prevailing gold prices will likely determine which pathway is pursued.

The next major ASX story will hit our subscribers first

Benchmarking the Deal: How Andacollo Oro Compares to Regional Peers

In-Ground Acquisition Cost: A Critical Investor Metric

At US$32 million for approximately 7.08 million ounces of total gold resources, the implied in-ground acquisition cost is approximately US$4.52 per ounce on a total resource basis, or roughly US$15.84 per ounce against the M&I resource alone. Industry benchmarks for permitted, past-producing heap leach assets in Latin America vary considerably, but deals involving fully approved open-pit gold operations with existing infrastructure have historically traded at significant premiums to pure exploration-stage assets in the same jurisdictions.

| Metric | Andacollo Oro (Galantas Gold) | Typical Junior Gold Project (Latin America) |

|---|---|---|

| Historical Production | 1.12 Moz Au | Often pre-production |

| M&I Resource | 2.02 Moz Au | 0.5 to 1.5 Moz typical |

| Inferred Resource | 5.06 Moz Au | Variable |

| Processing Method | Open-pit heap leach | Variable |

| Permitting Status | Fully permitted for restart | Often pending |

| Acquisition Cost | US$32M + US$3M debt | Variable |

The combination of full permitting, documented production history, extensive existing infrastructure, and a 7+ Moz resource base at an implied acquisition cost below US$5 per total ounce represents a structurally differentiated value proposition relative to the broader universe of junior Latin American gold development opportunities.

Key Risks Investors Should Understand

Operational and Technical Risks

- Heap leach pad reactivation after an eight-year dormancy period introduces residual chemistry and liner integrity risks that require systematic pre-restart engineering assessment.

- Grade variability across a 488 Mt resource base is an inherent geological reality that could affect metallurgical recovery rates and mine plan sequencing.

- Water availability in the Coquimbo Region represents a persistent operational constraint given Chile's multi-year drought cycle.

Financial and Market Risks

- Galantas Gold must simultaneously manage staged acquisition payments and restart capital expenditure, creating potential financing pressure if gold prices weaken or equity capital market conditions deteriorate.

- Currency dynamics between USD-denominated acquisition obligations and Chilean peso-denominated operational costs introduce foreign exchange exposure.

- Chile's mining royalty framework has undergone legislative revision in recent years, and further changes cannot be excluded from medium-term project economics modelling.

Jurisdictional and Community Risks

- Andacollo is an established mining community with a long history of mineral extraction, which provides some degree of social licence precedent. However, community consultation requirements under Chilean environmental law must be satisfied throughout any restart process.

- Environmental conflict risk, flagged as a thematic consideration by regional industry observers, is a real variable in Chilean mining districts where water competition between agricultural, municipal, and industrial users has intensified under drought conditions.

What This Transaction Signals for Junior Mining M&A in 2026

The case of Galantas acquires Andacollo Oro project in Chile is not an isolated event. It is part of a broader strategic pivot within the junior mining sector towards brownfield assets that offer compressed development timelines, defined resource bases, and regulatory certainty. In addition, gold M&A activity globally reflects how capital markets are increasingly impatient with the multi-decade development arcs of greenfield projects, expanding the premium placed on permitted, infrastructure-rich past-producers.

Chile specifically is emerging as a focus jurisdiction for this type of transaction. Its combination of political stability relative to several neighbouring mining nations, an established regulatory framework, world-class geological endowment, and functional infrastructure corridor from mine to port creates an operating environment that junior developers can model with reasonable confidence.

The gold sector within Chile remains relatively underdeveloped compared to its copper dominance, which means capable acquirers with the right assets can access significant resource scale without competing against the deep-pocketed majors that control the country's copper pipeline. Furthermore, an updated mineral resource estimate published ahead of the shareholder vote provided additional technical validation for the transaction's strategic rationale.

The Andacollo Oro transaction offers a replicable blueprint for junior gold developers seeking capital-efficient growth: acquire a fully permitted, past-producing asset with large-scale resources, distribute payment obligations to preserve liquidity, and leverage existing infrastructure to minimise the capital expenditure required to reach production. The risk-adjusted development pathway this creates is meaningfully superior to greenfield alternatives in the current financing environment.

Andacollo Oro Acquisition: At-a-Glance Summary

| Factor | Detail |

|---|---|

| Acquirer | Galantas Gold Corporation |

| Project | Andacollo Oro Gold Project |

| Location | Coquimbo Region, Chile (~55 km SE of La Serena) |

| Deal Value | US$32M staged over 4 years + ~US$3M debt assumption |

| M&I Resource | 2.02 Moz Au at 0.48 g/t (130 Mt) |

| Inferred Resource | 5.06 Moz Au at 0.45 g/t (358 Mt) |

| Historical Production | 1.12 Moz Au from 1998 to 2018 |

| Peak Annual Output | 125,000 oz Au |

| Permitting Status | Fully permitted, no new approvals required |

| Shareholder Approval | 99.99% in favour (June 15, 2026) |

| Transaction Close | June 2026 |

| Production Restart Target | 2027 |

This article contains forward-looking statements and scenario analysis based on publicly available information. It does not constitute financial or investment advice. Readers should conduct independent due diligence and consult a qualified financial adviser before making investment decisions related to any company or project discussed herein.

Want to Identify the Next Major Gold Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into clear, actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure a market-leading edge on the next major find.