June 13, 2026

Global iron ore markets are experiencing unprecedented shifts as emerging producers challenge established supply chains and pricing mechanisms. While traditional powerhouses like Australia and Brazil have dominated international trade for decades, new geological discoveries across Africa's mineral-rich regions are fundamentally altering competitive dynamics. The Gâra Djebilet iron ore mine production represents one of the most significant developments in this transformation, encompassing technological innovation in beneficiation processes, infrastructure development in previously inaccessible regions, and strategic partnerships that blur conventional boundaries between state-controlled resources and private capital deployment.

The North African mining corridor represents a particularly compelling case study in this evolution, where vast untapped reserves intersect with urgent economic diversification imperatives. Understanding these developments requires examining not just resource quantities, but the complex interplay of metallurgical challenges, transportation logistics, and market positioning strategies that determine long-term viability in increasingly sophisticated global commodity markets. Furthermore, these shifts are occurring against a backdrop of iron ore price trends that reflect changing global demand patterns.

Resource Scale and Geographic Positioning Within Global Iron Ore Markets

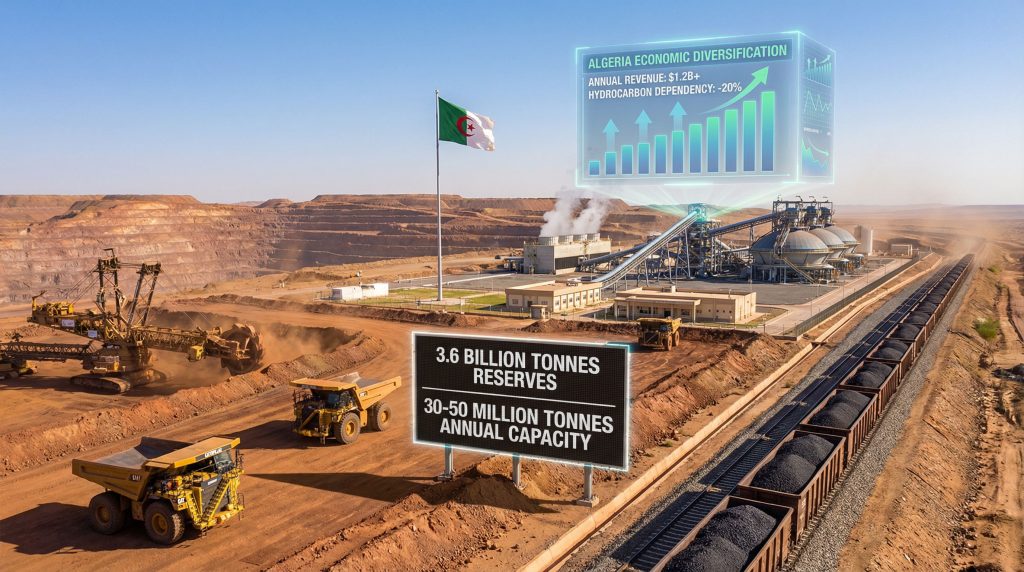

Algeria's Gâra Djebilet iron ore mine production represents one of the most significant mining developments in North Africa's recent history. The deposit contains approximately 3.6 billion tonnes of iron ore reserves, with 1.7 billion tonnes classified as recoverable using current extraction and processing technologies.

The mine's geographic positioning in Tindouf province creates both opportunities and challenges for market access. Located in Algeria's western region, the deposit requires substantial infrastructure investment to connect with international markets. The recently completed 950-kilometer railway line linking the mine to processing facilities and export terminals demonstrates the scale of logistical commitment required for such remote operations.

Comparative Analysis Against Major African Iron Ore Deposits

When evaluated against other significant African iron ore developments, Gâra Djebilet's scale becomes apparent. Additionally, this positioning occurs whilst the industry faces global price challenges that affect investment decisions across all major projects.

| Deposit | Location | Reserves (Billion Tonnes) | Infrastructure Status | Market Position |

|---|---|---|---|---|

| Gâra Djebilet | Algeria | 3.6 total / 1.7 recoverable | Railway operational 2026 | Export phase beginning |

| Simandou | Guinea | 2.4+ high-grade | Railway under development | Pre-production |

| Guelb Moghrein | Mauritania | 0.3+ operating | Established rail/port | Active exporter |

| Sishen | South Africa | 1.2+ remaining | Mature infrastructure | Declining production |

The project's technical specifications reveal the engineering complexity involved. The mine spans over 125 million square metres, making it one of the world's top iron ore mines by surface area. This massive footprint requires coordinated extraction planning across multiple zones to maintain consistent ore quality and production volumes.

Processing Technology and Quality Management

China's Sinosteel Corporation has constructed an $800 million processing facility at the Gâra Djebilet site, addressing the deposit's primary metallurgical challenge: elevated phosphorus content. High phosphorus levels in iron ore require specialised beneficiation techniques to meet international export standards, typically involving flotation processes, magnetic separation, or reverse flotation methods.

The processing plant's capacity and technology specifications remain closely guarded. However, industry standards suggest the facility must achieve phosphorus reduction from potentially 0.15-0.25% down to 0.08% or lower for premium export grades. This processing requirement significantly impacts production economics, as beneficiation costs can range from $8-15 per tonne depending on ore characteristics and recovery rates.

When big ASX news breaks, our subscribers know first

Production Scaling Framework and Economic Integration Strategy

Algeria's approach to developing Gâra Djebilet iron ore mine production follows a phased production model designed to minimise operational risk while maximising long-term revenue potential. The initial production milestone occurred in early 2026, with the first train carrying over 1,000 tonnes of processed iron ore from the mine to export terminals.

Production Timeline and Capacity Targets

Government projections indicate production will scale gradually to reach 40-50 million tonnes annually by 2040. This 15-year development timeline reflects the substantial infrastructure investments required, including rail capacity expansion, port terminal upgrades, and processing plant optimisation. These developments come at a time when surging iron ore demand creates opportunities for new market entrants.

Phase 1 (2026-2030): Infrastructure Validation

- Annual capacity target: 4-12 million tonnes

- Focus: Operational efficiency and quality consistency

- Investment priority: Rail system optimisation and processing plant fine-tuning

- Market strategy: Domestic steel industry supply and select export contracts

Phase 2 (2030-2035): Commercial Scale-Up

- Annual capacity target: 15-30 million tonnes

- Focus: Export market penetration and logistics cost reduction

- Investment priority: Port capacity expansion and shipping infrastructure

- Market strategy: Regional market development in Europe and Middle East

Phase 3 (2035-2040): Full Production Capacity

- Annual capacity target: 40-50 million tonnes

- Focus: Market share consolidation and value-added processing

- Investment priority: Downstream steel production integration

- Market strategy: Global market positioning as tier-one supplier

Economic Diversification Impact Analysis

Algeria's economic transformation strategy positions mining sector development as crucial for addressing fiscal challenges. The country faces a projected $40 billion budget deficit in 2026, driven primarily by declining hydrocarbon revenues and increasing domestic spending pressures.

The Gâra Djebilet project represents a cornerstone of efforts to reduce hydrocarbon dependency, which currently accounts for over 90% of export revenues and approximately 60% of government budget receipts. Mining law reforms implemented in August 2025 opened the sector to foreign investment, creating frameworks for technology transfer and capital deployment that support projects like Gâra Djebilet iron ore mine production.

Economic Diversification Metrics:

- Current non-hydrocarbon exports: Less than 5% of total exports

- Projected mining sector contribution by 2030: 8-12% of export revenues

- Employment generation potential: 15,000-25,000 direct and indirect jobs

- Fiscal impact timeline: Meaningful revenue contribution beginning 2028-2030

Operational Challenges and Technical Solutions

The successful development of Gâra Djebilet iron ore mine production faces several critical operational hurdles that require sophisticated technical solutions and strategic partnerships.

Metallurgical Processing Requirements

The primary technical challenge involves managing the ore's phosphorus content while maintaining efficient recovery rates. Standard iron ore export specifications require phosphorus levels below 0.08%, while many steel producers prefer concentrates with less than 0.05% phosphorus for direct blast furnace feed.

The Sinosteel processing facility employs multiple beneficiation stages:

Primary Processing:

- Crushing and grinding to optimal liberation size (typically 150-200 microns)

- Magnetic separation to remove low-grade magnetite fractions

- Gravity separation for density-based mineral sorting

Secondary Beneficiation:

- Reverse flotation to reduce silica and phosphorus content

- Filtration and dewatering to achieve 8-10% moisture content

- Quality control testing for Fe content, impurities, and physical properties

The processing plant's design capacity must accommodate variable ore characteristics across different mining zones. This flexibility requires sophisticated blending protocols and real-time quality monitoring systems to ensure consistent product specifications.

Transportation Infrastructure and Logistics Economics

The 950-kilometer railway connecting Gâra Djebilet to Algeria's export infrastructure represents one of Africa's most significant mining logistics projects. The rail line's capacity, gradient management, and maintenance requirements directly impact production economics. Moreover, these railway logistics improvements demonstrate industry-wide focus on transportation efficiency.

Railway Specifications and Performance Metrics:

- Track gauge: Standard gauge (1,435mm) for international compatibility

- Maximum axle load: 25-30 tonnes per axle (industry standard for iron ore)

- Operating speed: 40-60 km/h loaded, considering terrain and safety requirements

- Annual capacity: 50+ million tonnes (designed for full production phase)

Transportation costs typically represent 15-25% of total production expenses for remote iron ore operations. The railway's operational efficiency becomes crucial for maintaining competitive pricing in international markets, particularly when competing against established suppliers with mature logistics networks.

Port Infrastructure and Shipping Logistics

Export operations require significant port infrastructure investments to handle large-scale iron ore shipments. The connection to Algeria's export terminals, likely including upgrades to facilities at Oran and potentially other coastal locations, must accommodate:

- Bulk handling equipment: Ship loaders capable of 2,000-4,000 tonnes per hour loading rates

- Storage capacity: 1-2 million tonnes of stockpiled ore for shipping schedule optimisation

- Shipping channel access: Accommodation for Capesize vessels (150,000+ tonnes capacity) to minimise freight costs per tonne

The Mediterranean shipping routes provide access to European steel producers, while positioning for potential Middle Eastern market development through Red Sea routing creates strategic flexibility for market diversification.

Global Market Positioning and Competitive Analysis

The emergence of Gâra Djebilet iron ore mine production occurs within a global iron ore market experiencing significant structural changes. Traditional supply dominance by Australia's Pilbara region and Brazil's iron ore mines faces increasing pressure from new entrants, shifting demand patterns, and evolving quality requirements.

Market Share Projections and Competitive Dynamics

At full production capacity of 40-50 million tonnes annually, Gâra Djebilet would represent approximately 2.5-3% of global iron ore trade, positioning Algeria as a significant mid-tier supplier. This scale places the operation among the world's top 15 iron ore mines and establishes Algeria as Africa's second-largest iron ore exporter after South Africa.

Competitive Positioning Analysis:

| Producer | Annual Capacity (Million Tonnes) | Fe Content (%) | Key Advantages | Market Focus |

|---|---|---|---|---|

| Vale (Brazil) | 300+ | 65-67% | Established logistics, high grade | Global markets |

| Rio Tinto (Australia) | 280+ | 61-62% | Proximity to Asia, scale | Asia-Pacific focus |

| BHP (Australia) | 250+ | 62-63% | Integrated operations, efficiency | Asian steel mills |

| Gâra Djebilet (Algeria) | 40-50 | 60-65%* | European proximity, competitive costs | Europe, Middle East |

*Estimated grade post-beneficiation; actual specifications may vary based on processing optimisation

Regional Market Opportunities

Algeria's geographic positioning creates distinct competitive advantages for specific market segments. The Mediterranean location provides cost-effective shipping access to European steel producers, while maintaining flexibility for Middle Eastern market development.

European Market Dynamics:

- Current import requirements: 150+ million tonnes annually

- Primary suppliers: Australia (35%), Brazil (30%), other sources (35%)

- Quality preferences: High Fe content, low impurities, consistent specifications

- Logistics preferences: Smaller vessel sizes, frequent deliveries, port flexibility

Middle Eastern Market Potential:

- Growing steel production capacity in UAE, Saudi Arabia, Turkey

- Quality requirements: Variable, depending on steel production technology

- Price sensitivity: High, given regional competition and cost structures

- Logistics advantages: Shorter shipping distances than traditional suppliers

What Makes Gâra Djebilet Cost-Competitive?

The long-term viability of Gâra Djebilet iron ore mine production depends critically on achieving competitive cost structures relative to established suppliers. Mining operations in remote locations face inherent cost disadvantages that must be offset through operational efficiency, quality premiums, or logistics advantages.

Estimated Cost Structure Components:

- Mining and extraction: $15-25 per tonne (depending on ore characteristics and depth)

- Processing and beneficiation: $8-15 per tonne (high due to phosphorus removal requirements)

- Rail transportation: $12-18 per tonne (for 950-kilometer distance)

- Port handling and shipping: $6-10 per tonne (to European destinations)

- Total delivered cost estimate: $41-68 per tonne to European markets

These cost estimates position Gâra Djebilet competitively during periods of strong iron ore pricing (above $80-90 per tonne) but create margin pressure during commodity downturns. The operation's success requires careful market timing, operational efficiency improvements, and potential quality premiums for consistent, low-phosphorus concentrate products.

Investment Framework and Partnership Structure

The development of Gâra Djebilet represents a $7-10 billion capital investment spanning infrastructure, processing technology, and operational capabilities. This scale of investment requires sophisticated partnership structures and risk-sharing mechanisms between state entities and international technology providers.

Public-Private Partnership Architecture

Algeria's state-owned mining entity Feraal manages operational oversight, while leveraging international partnerships for technology transfer and specialised expertise. The partnership with China's Sinosteel Corporation exemplifies this approach, combining Algerian resource control with Chinese processing technology and project management capabilities.

Investment Allocation Framework:

- Infrastructure (40-45%): Railway construction, port facilities, power supply systems

- Processing facilities (25-30%): Beneficiation plants, quality control systems, maintenance facilities

- Mining equipment (20-25%): Extraction equipment, mobile machinery, support vehicles

- Working capital and contingency (5-10%): Operational reserves, unforeseen cost coverage

The Sinosteel processing plant investment of approximately $800 million represents roughly 10-12% of total project costs, indicating the sophisticated nature of the beneficiation technology required for phosphorus management and quality consistency.

Technology Transfer and Capacity Building

International partnerships extend beyond capital investment to encompass knowledge transfer, operational training, and technical capability development. The Sinosteel collaboration provides Algeria with access to advanced iron ore processing technologies, while creating opportunities for local technical capacity development.

Technology Transfer Components:

- Beneficiation process optimisation and control systems

- Quality management protocols and testing methodologies

- Equipment maintenance procedures and spare parts supply chains

- Operational efficiency monitoring and continuous improvement practices

These partnerships create long-term value beyond initial capital deployment, establishing technical capabilities that support sector expansion and operational independence over time.

Long-Term Strategic Implications for Regional Development

The successful development of Gâra Djebilet iron ore mine production creates broader implications for North Africa's mining sector development and regional economic integration. The project serves as a demonstration of technical feasibility, investment frameworks, and market access strategies that can inform future mineral resource developments across the region.

Industrial Cluster Development Potential

Large-scale iron ore production creates opportunities for downstream industrial development, including steel production facilities, fabrication industries, and supporting service sectors. The availability of domestically produced iron ore reduces input costs for potential steel projects while creating employment multiplier effects across related industries.

Industrial Development Scenarios:

- Scenario 1: Import substitution focus – meeting domestic steel demand estimated at 3-5 million tonnes annually

- Scenario 2: Regional integration – supplying North African steel production hubs in Egypt, Morocco, Tunisia

- Scenario 3: Value-added exports – developing direct-reduced iron (DRI) or steel billet production for international markets

Each scenario requires different investment levels, technology partnerships, and market development strategies, but all benefit from secure, cost-effective iron ore supply from domestic production.

Regional Mining Sector Transformation

Algeria's mining law reforms and successful project implementation create demonstration effects for other North African countries with significant mineral resources. The regulatory frameworks, partnership structures, and operational models developed for Gâra Djebilet provide templates for mineral resource development across the region.

Regional Mining Development Indicators:

- Morocco: Phosphate production expansion and diversification into other minerals

- Tunisia: Lead, zinc, and phosphate sector modernisation initiatives

- Egypt: Golden Triangle mineral exploration and development programmes

- Libya: Post-conflict mineral sector rehabilitation and development

The success of Gâra Djebilet's development could catalyse broader regional mining investment, technology transfer, and infrastructure development that benefits multiple countries and mineral sectors.

The next major ASX story will hit our subscribers first

Risk Assessment and Market Dynamics

The long-term success of Gâra Djebilet iron ore mine production faces several categories of risk that require ongoing management and strategic adaptation. Understanding these risk factors enables better evaluation of project viability and investment returns over the 15-20 year development timeline.

Commodity Price Volatility and Market Risks

Iron ore prices exhibit significant volatility driven by global steel demand, supply disruptions, and macroeconomic conditions. Historical price ranges from $40-220 per tonne over the past decade illustrate the potential impact on project economics.

Price Risk Management Strategies:

- Long-term supply agreements with European steel producers to provide revenue stability

- Operational flexibility to adjust production volumes during price downturns

- Cost structure optimisation to maintain profitability at lower price levels

- Quality premiums development to reduce exposure to benchmark pricing volatility

The project's estimated cost structure suggests breakeven pricing around $50-60 per tonne, providing reasonable margins during normal market conditions while creating vulnerability during severe commodity downturns.

Infrastructure and Operational Risks

The 950-kilometer railway represents a critical single point of failure for the entire operation. Rail line disruptions from equipment failures, maintenance requirements, or external factors could significantly impact production and revenue generation.

Infrastructure Risk Mitigation:

- Comprehensive maintenance programmes and equipment redundancy

- Alternative transportation route development for partial capacity during disruptions

- Insurance coverage for infrastructure damage and business interruption

- Strategic stockpile management at both mine and port facilities

The remote location in Tindouf province also creates challenges for workforce management, equipment maintenance, and supply chain reliability that require specialised operational approaches.

Regulatory and Political Risk Factors

Mining operations with 15-20 year development timelines face exposure to changing regulatory environments, taxation policies, and political conditions. Algeria's economic pressures and need for mining revenue provide incentives for stable mining policies, but political changes could affect operational conditions.

Regulatory Risk Considerations:

- Mining law stability and foreign investment protection frameworks

- Taxation policy consistency and revenue-sharing arrangements

- Environmental regulation compliance and permitting requirements

- Export licensing procedures and trade policy consistency

The August 2025 mining law reforms demonstrate government commitment to sector development, but ongoing monitoring of regulatory evolution remains essential for long-term planning.

Future Market Scenarios and Strategic Positioning

The development trajectory of Gâra Djebilet iron ore mine production will unfold within evolving global steel and iron ore markets influenced by decarbonisation trends, technological innovations, and shifting demand patterns. Understanding potential future scenarios enables better strategic positioning and investment decision-making.

How Will Decarbonisation Affect Iron Ore Demand?

The global steel industry's transition toward lower-carbon production methods creates both challenges and opportunities for iron ore suppliers. Direct reduction processes using hydrogen or natural gas require different ore specifications than traditional blast furnace operations. Additionally, Algeria's strategic positioning as a raw resource exporter could transform into industrial value creation.

Technology Transition Implications:

- Direct Reduction Iron (DRI) requirements: Higher Fe content (67%+), lower impurities, specific size distributions

- Electric Arc Furnace growth: Increased scrap steel utilisation reducing primary iron ore demand

- Hydrogen-based steel production: Premium quality ore requirements for emerging technologies

- Carbon pricing impact: Transportation cost advantages for regionally positioned suppliers

Gâra Djebilet's processing capabilities position it to potentially serve emerging DRI markets in Europe and the Middle East, where natural gas availability and hydrogen development programmes support steel industry decarbonisation initiatives.

Regional Steel Production Growth Scenarios

Middle Eastern steel production expansion, driven by economic diversification programmes in Saudi Arabia, UAE, and other countries, creates potential demand growth for regional iron ore suppliers. This market development could provide Algeria with strategic alternatives to traditional European export markets.

Regional Demand Growth Drivers:

- Infrastructure development programmes across the Middle East

- Manufacturing sector expansion and economic diversification initiatives

- Regional steel production capacity additions and modernisation projects

- Import substitution strategies reducing dependence on external steel suppliers

The proximity advantages for serving Middle Eastern markets could become increasingly valuable as regional steel production capacity expands and quality requirements evolve.

Strategic Positioning for Market Evolution

The successful positioning of Gâra Djebilet iron ore mine production requires adaptation to changing market conditions while leveraging inherent competitive advantages. This strategic flexibility enables value capture across different market scenarios and demand patterns.

Strategic Positioning Elements:

- Quality optimisation: Continuous improvement in phosphorus reduction and Fe content enhancement

- Logistics efficiency: Transportation cost reduction through operational improvements and scale economies

- Market diversification: Balanced exposure across European and Middle Eastern steel markets

- Technology adaptation: Processing capability evolution to serve changing steel industry requirements

The project's scale and infrastructure investments create the foundation for long-term market participation, while operational flexibility and technical capabilities enable adaptation to evolving industry conditions.

Disclaimer: This analysis is based on publicly available information and industry estimates. Actual production costs, technical specifications, and market performance may vary significantly from projections. Commodity investments involve substantial risk, and past performance does not guarantee future results. Readers should conduct independent research and consult qualified advisors before making investment decisions.

Looking to Capitalise on Major Mining Developments?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities in Australia's dynamic mining sector before the broader market reacts. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the next major breakthrough.