July 20, 2026

The Ownership Vacuum at the Top of the Diamond World

Every generation or so, the diamond industry undergoes a structural reset so significant that its effects ripple through the entire supply chain for decades. The dissolution of De Beers' single-channel marketing monopoly in the early 2000s was the last such moment. The current contest for ownership of the world's largest diamond miner may prove to be the next one. The outcome will be determined not just by who writes the largest cheque, but by who can navigate the most complex web of sovereign politics, geopolitical disruption, and structural market decline that the industry has faced in living memory.

The Gareth Penny De Beers bid sits at the centre of this convergence. Understanding what it means requires going well beyond the transaction itself.

When big ASX news breaks, our subscribers know first

What the Gareth Penny De Beers Bid Actually Represents

At its core, the Gareth Penny De Beers bid is not simply a change of corporate ownership. It is a proposed philosophical reimagination of how the world's most iconic diamond business should be positioned, governed, and operated as it enters one of the most turbulent chapters in its history.

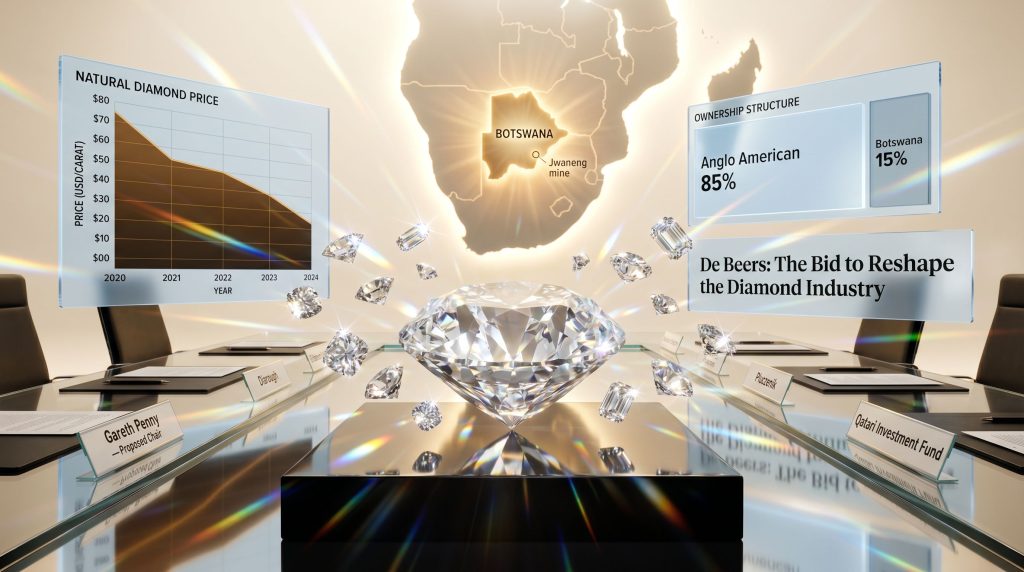

Anglo American holds an 85% ownership stake in De Beers, with the Government of Botswana holding the remaining 15%. The divestiture process was initiated as part of a sweeping portfolio restructuring triggered by BHP's hostile takeover approach in 2024, which forced Anglo's management to publicly commit to concentrating capital on copper and transition metals. De Beers, for all its brand power, does not fit that narrower strategic identity.

What makes this more than a routine corporate sale is the identity of the frontrunner. Penny served as De Beers Chief Executive for approximately five years before departing in 2010. His proposed role in the incoming structure is as Chair rather than operational CEO, signalling that the bid has been designed as an investor-led governance model with deep industry expertise embedded at the board level rather than in day-to-day management.

Who Is in the Consortium?

The consortium Penny leads is notable for its composition:

| Consortium Participant | Role / Background |

|---|---|

| Gareth Penny | Former De Beers CEO; proposed Chair of new entity |

| Qatari Investment Fund | Reported financial backer |

| Diarough | Belgian diamond trading firm |

| Pluczenik | Belgian diamond company |

| Rosy Blue | Major international diamond trading house |

The presence of multiple major rough diamond trading houses within the shareholder base is strategically significant and not widely appreciated. It suggests the new ownership model would embed distribution expertise directly into the capital structure, effectively internalising relationships that De Beers has historically managed at arm's length through its sightholder system.

Furthermore, Antwerp sightholders have reportedly backed the Penny bid, adding further weight to its industry credibility. As a result, the sightholder system — through which De Beers allocates rough diamond parcels to a select group of approved buyers at fixed prices roughly ten times per year — has historically been one of the most powerful pricing mechanisms in any commodity market. Embedding the trading houses directly into the ownership structure could fundamentally alter how that system operates in practice.

The Competitive Landscape: Three Bids, One Immovable Obstacle

As of mid-2026, at least three private consortiums remain active in pursuing the De Beers asset, with the original binding offer deadline of mid-April having been extended as negotiations continue.

| Bidder | Background | Reported Status | Key Risk Factor |

|---|---|---|---|

| Gareth Penny Consortium | Former De Beers CEO; backed by diamond traders and Qatari capital | Frontrunner | Botswana approval and deal structure |

| Bruce Cleaver Consortium | Former De Beers CEO; separate independent bid | Active competitor | Financing differentiation |

| Michael O'Keeffe Group | Australian mining veteran | Currently an outsider | Limited diamond sector depth |

| Nir Livnat / Diacore | Israeli diamond trader | Financing difficulties reported | Middle Eastern capital disruption |

How Geopolitics Is Reshaping the Bidding Field

The geopolitical dimension shaping this competition is underappreciated by most market observers. The escalation of the Iran conflict has created severe disruption to Middle Eastern capital markets, with direct consequences for bidders who structured their financing around Gulf-region investors. This broader geopolitical mining landscape has consequently reshaped the competitive dynamics in ways that few anticipated at the outset of the sale process.

Nir Livnat's Diacore consortium, which had reportedly sought backing from Qatari and other Middle Eastern sources, has encountered material difficulties finalising its capital commitments as a result. This dynamic has inadvertently strengthened the Penny consortium's relative position.

By appearing to have secured more diversified and stable financial commitments, the group has benefited from a competitive disadvantage imposed on rivals by circumstances entirely outside the transaction itself. It is a reminder that in large-scale M&A, macro-level instability does not merely affect deal valuations; it reshapes the competitive field entirely.

Botswana's Sovereignty Ambition: The Non-Negotiable Variable

No analysis of the Gareth Penny De Beers bid is complete without an honest accounting of Botswana's leverage in this process, and it is considerable.

Botswana is not a passive 15% minority stakeholder. It is the sovereign host of De Beers' most strategically valuable assets, most notably the Jwaneng mine, widely regarded by industry analysts as the world's highest-value diamond mine by revenue per tonne of ore processed. Jwaneng's ore grades and the gem-quality proportion of its production place it in a category of its own within the global kimberlite mining universe. Without Botswana's continued cooperation, De Beers' asset base is materially diminished.

President Duma Boko has publicly called for majority control of De Beers. However, while the government may ultimately accept a position short of outright majority, diplomatic activity — including a reported presidential visit to Oman to advance related discussions — signals that Botswana views this as a national economic priority, not a minor negotiating point.

The structural constraint this creates is stark: any acquirer must simultaneously satisfy Anglo American's valuation expectations, address Botswana's ownership ambitions, and present a credible operational plan. These three requirements may not be simultaneously satisfiable at any price.

Three scenarios emerge from this constellation of pressures:

-

Scenario A — Penny consortium acquires Anglo's 85% stake while Botswana negotiates an increase to approximately 25–30%, allowing the transaction to proceed with restructured sovereign participation.

-

Scenario B — No bidder can bridge the gap between Anglo's pricing expectations and Botswana's ownership demands simultaneously, forcing Anglo to retain De Beers or pivot to a partial IPO structure.

-

Scenario C — A competing consortium, potentially the Cleaver group, resolves its financing structure and submits a superior binding offer, displacing the Penny consortium despite its frontrunner status.

Why Penny's Track Record Is More Relevant Now Than It Was in 2010

There is a structural parallel between the conditions Penny navigated during his tenure and the environment any new De Beers owner will inherit that has not received sufficient analytical attention. Indeed, the global financial crisis parallels to the current environment are striking for those willing to examine them closely.

During the 2008–2009 financial crisis, Penny led De Beers through a period of acute demand destruction and financing pressure. The response involved idling mine production across multiple operations and executing a $1 billion rights offering to stabilise the company's capital position. These were operationally painful decisions that required overriding short-term commercial pressures in favour of long-term financial survival.

What Structural Pressures Does the New Owner Inherit?

The current diamond market exhibits structurally similar characteristics:

- Demand destruction driven by synthetic diamond penetration and weakening Chinese luxury consumption

- Inventory overhang across the mid-pipeline, inherited from an artificial demand spike during 2021–2022

- Financing pressure on downstream participants, including rough diamond dealers and polished manufacturers

- Price compression across rough diamond categories that has made new mine investment economically marginal

The institutional knowledge Penny carries from the prior crisis cycle is not simply biographical colour. It represents a genuine operational advantage in a business where understanding how to sequence mine curtailments, manage sightholder relationships through demand shocks, and maintain brand investment during downturns requires hard-won experience that cannot be acquired from a distance.

The Lab-Grown Diamond Challenge: What the New Owners Must Confront

Chinese manufacturers, increasingly leveraging AI-assisted production optimisation, have driven a dramatic acceleration in synthetic diamond output. The result has been a structural compression in the price premium that natural diamonds have historically commanded over their laboratory-produced equivalents, particularly in the bridal and fashion jewellery categories. Furthermore, China demand trends across luxury goods more broadly indicate that the recovery in high-end consumer spending remains uneven and fragile.

De Beers itself launched the Lightbox lab-grown diamond brand under prior management, a move that was designed to commoditise the synthetic segment and protect natural diamond pricing. That strategy has since been partially wound back, reflecting the difficulty of simultaneously defending a premium natural product while selling a commoditised synthetic alternative under the same corporate umbrella.

Any incoming ownership group will need to resolve this strategic contradiction. The most credible path involves a focused commitment to differentiating natural diamonds on provenance, rarity, and emotional value — areas where synthetic production cannot compete by definition.

A regulatory development in the United Kingdom provides a meaningful opening. In 2025, UK advertising standards authorities ruled against lab-grown diamond retailers who had made claims about value retention and investment characteristics that were deemed misleading. This ruling creates a legitimate marketing platform for natural diamond producers to reassert the unique attributes of mined stones without making comparative claims that regulators would scrutinise.

The next major ASX story will hit our subscribers first

The Structural Headwinds Are Real and Should Not Be Minimised

Disclaimer: The following section contains market observations and analytical perspectives. None of this constitutes investment advice. Readers should conduct independent research and consult qualified financial advisers before making any investment decisions.

The diamond sector's current downturn is not a standard cyclical correction. It reflects the convergence of multiple simultaneous pressures that compound one another:

| Market Indicator | Current Trend | Implication for De Beers |

|---|---|---|

| Natural rough diamond prices | Multi-year decline | Revenue and margin compression |

| Lab-grown market share | Accelerating penetration | Demand substitution in key categories |

| Chinese luxury jewellery demand | Subdued recovery | Volume shortfall in critical growth market |

| Mid-pipeline inventory levels | Elevated and persistent | Sustained pressure on new production pricing |

| Botswana production volumes | Stable but strategically uncertain | Continuity dependent on sovereign resolution |

The weakness in Chinese luxury demand deserves particular emphasis. China emerged as the decisive growth engine for diamond jewellery consumption throughout the 2010s, absorbing supply growth that would otherwise have tested natural price support levels far earlier. The sustained softening of Chinese consumer confidence, combined with shifting generational preferences toward experiential spending rather than jewellery acquisition, represents a structural demand revision that no ownership change can address in isolation.

What a Private Ownership Transition Means for the Broader Industry

A successful transfer of De Beers to private consortium ownership would represent the most consequential structural change in the global diamond industry since De Beers dismantled its historical single-channel marketing monopoly in the early 2000s. That earlier transition reshaped rough diamond pricing, market access, and the commercial relationships between miners, cutters, polishers, and retailers across the entire supply chain.

For junior diamond miners and mid-tier producers, the strategic direction adopted by a new De Beers ownership group carries downstream implications that extend well beyond the transaction itself. Broader mining industry consolidation trends suggest that these downstream effects could accelerate further as capital concentrates around fewer, larger players. De Beers' investment in consumer marketing, its positioning of natural diamonds against synthetic alternatives, and its management of the sightholder allocation system all influence the commercial environment in which every other natural diamond producer operates.

What Precedent Does This Set Beyond the Diamond Sector?

The outcome of the Botswana ownership negotiations will also set a precedent that extends far beyond this specific transaction. How African resource-producing nations engage with foreign capital in high-value extractive asset acquisitions will be shaped by the terms ultimately agreed between Anglo American, Botswana, and whichever consortium prevails. In that sense, this deal carries significance well beyond the world's largest open-pit mines and the extractive industries more broadly.

As of mid-2026, the Gareth Penny De Beers bid remains the frontrunner in an open and unresolved competitive process. No binding transaction has been confirmed, and the parallel negotiation tracks involving bidder selection, Botswana's ownership stake, and multi-jurisdictional regulatory approvals all remain active. The timeline for resolution is uncertain, and Anglo American, while described as patient, cannot absorb the operational and capital costs of indefinite uncertainty around an asset it has publicly committed to divesting.

The next phase of this process will reveal whether operational pedigree and crisis management credibility are sufficient to close one of the most complex mining transactions in recent memory.

Want to Track the Next Major Mining Sector Shift Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex sector data into actionable opportunities — explore historic discoveries and their extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.