May 14, 2026

The Infrastructure Paradox at the Heart of Australia's Gas Supply Crisis

When energy infrastructure outlives the resource base it was built to serve, the result is a peculiar kind of economic irony: pipelines with capacity to carry hundreds of terajoules per day sitting largely idle, processing facilities mothballed mid-decade, and a state government scrambling to reverse a legislative decision made just seven years earlier. This is the situation confronting South Australia in 2026, and it reveals something important about how energy policy cycles actually work in practice.

The infrastructure already exists. The market pathway already exists. What has been missing is a sufficient volume of gas to fill it, and the regulatory framework to allow the kind of exploration that might produce that gas. Understanding why South Australia plans to lift gas fracking ban legislation is being introduced now, rather than simply waiting for the 2018 moratorium to expire naturally in November 2028, requires looking at the lead times involved in bringing new gas supply to market, not the politics of the moment.

When big ASX news breaks, our subscribers know first

Why Waiting Until 2028 Is Not a Viable Supply Strategy

The Australian Energy Market Operator has flagged material risks to southern Australia's gas supply emerging as early as 2029, with further shortfalls projected beyond that point. This timeline creates a structural problem for policymakers: even if the moratorium were allowed to expire on schedule, the sequence of exploration application, environmental assessment, public consultation, regulatory approval, drilling, appraisal, and final investment decision would consume the better part of a decade before new production could reach commercial volumes.

This is not a hypothetical concern. It reflects the well-documented lead times of the upstream gas industry, where the gap between a positive policy signal and first molecules flowing through a pipeline routinely spans five to ten years. Ending the moratorium two years early is therefore less about unlocking immediate supply and more about compressing that lead time window so that any new production has a realistic chance of contributing to the market before the supply crunch deepens.

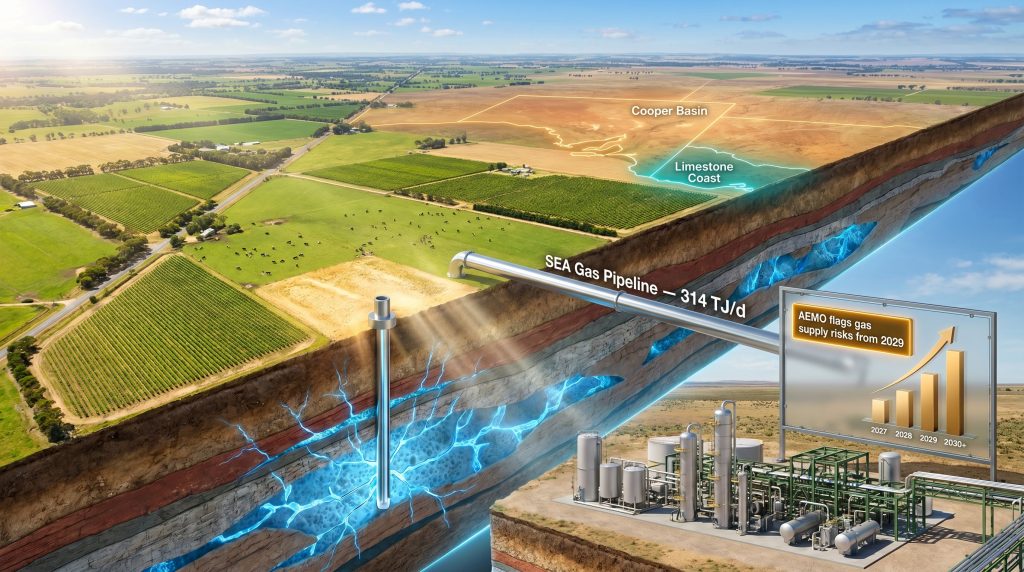

Furthermore, natural gas price trends across the region underscore the urgency of securing new domestic supply sources. South Australia's declining domestic production profile compounds this urgency. The state's gas supply mix has historically drawn on Bass Strait reserves feeding through the SEA Gas pipeline, Cooper Basin output from Santos's Moomba operations, and modest local production from the Otway basin fields in the South East.

The moratorium reversal sits within a broader package of measures the state government has assembled in response to this trajectory, including a South Australian Strategic Gas Reserve, a Firm Energy Reliability Mechanism, and the South Australian Gas Initiative. These instruments address different dimensions of the supply security problem, but none of them can manufacture new molecules. Only upstream investment can do that.

The 2018 Moratorium: What It Actually Prohibited and What It Didn't

One of the most persistent misunderstandings about South Australia's fracking policy is the assumption that it represented a statewide prohibition. It did not. The 10-year moratorium, enacted in November 2018 by the then-Marshall Liberal Government, applied exclusively to the South East region, also known as the Limestone Coast, which sits within the onshore Otway basin straddling the South Australian and Victorian border.

Hydraulic fracturing has continued without restriction throughout the Cooper Basin, where Santos operates the 250 TJ/d Moomba gas plant and where more than 1,300 wells have been hydraulically fractured since 1969. The South Australian government has stated that this decades-long history of Cooper Basin fracking has produced no documented impacts on aquifer systems, a claim central to its argument that the technology, applied appropriately and subject to rigorous oversight, can coexist with groundwater protection objectives.

The moratorium was a geographically targeted precautionary measure, not a blanket rejection of hydraulic fracturing as a technology. The distinction matters enormously when evaluating what the proposed legislation actually changes.

The South East received this targeted protection because its environmental and economic character differs fundamentally from the remote arid Cooper Basin. The Limestone Coast is underlain by a network of interconnected aquifer systems that supply water to premium wine, dairy, and livestock operations. Its shallow water table and porous limestone geology present a risk profile that justified a precautionary approach in 2018, and the current government maintains that groundwater protection remains a non-negotiable condition of any future approvals.

The Energy Resources Amendment Bill: Legislative Mechanics and Political Arithmetic

The Energy Resources (Regulated Activities) Amendment Bill proposes to terminate the moratorium approximately two years ahead of its scheduled November 2028 expiry. Critically, the bill does not constitute approval for any specific fracking operation. It removes the legislative prohibition, after which all individual proposals would still need to navigate the full regulatory approval pathway, encompassing environmental impact assessments, public consultation, and formal permitting.

What the bill does do is change the investment calculus for companies with acreage in the South East. Regulatory uncertainty is among the most powerful deterrents to upstream capital commitment. Removing the statutory barrier signals that the state is open to applications, which is the precondition for any exploration program to commence. In addition, government intervention in resources policy of this nature often reshapes how operators approach long-term investment planning across the sector.

The bill's passage is far from guaranteed. To become law, it must clear the South Australian Legislative Council, where Labor does not hold a majority in the 22-member chamber. The political arithmetic is complex:

| Party | Legislative Position | Notes |

|---|---|---|

| Labor (Government) | Supports passage | Does not hold upper house majority |

| Liberal Party (Opposition) | Conditional support | Calls for community consultation; distinguishes South East from Cooper Basin context |

| South Australian Greens | Opposed | Consistent with broader anti-fracking platform |

| One Nation | Pro-drilling platform | Holds pivotal seats including MacKillop in the South East |

Labor almost certainly requires One Nation's support to pass the bill in its current form. This dependency is politically delicate for reasons that go beyond simple party alignment. One Nation won a historic three seats in the 22-member chamber at the March 2026 election, including the state seat of MacKillop, which is centred on the agricultural towns of Naracoorte, Millicent, and Bordertown.

These communities sit within the very region where the moratorium would be lifted, and where grassroots sentiment toward gas fracking has historically been resistant. According to reporting from InDaily, the announcement has already drawn sharp criticism from local community members and environmental advocates.

One Nation now faces a genuine internal tension: its national policy platform advocates for pro-drilling policies, but its newest South East constituency holds views that may pull in the opposite direction. How the party resolves this conflict will likely determine whether the bill passes the upper house.

A Tale of Two Gas Provinces: Cooper Basin vs. South East Otway

The contrast between the Cooper Basin and the South East is instructive for understanding both the risk calculus and the potential opportunity at stake.

| Factor | Cooper Basin | South East (SA Otway Basin) |

|---|---|---|

| Fracking Status | Permitted and active | Prohibited under moratorium |

| Wells Fracked Since 1969 | 1,300+ | None under moratorium |

| Primary Land Use | Remote arid zone | Premium agricultural land |

| Key Processing Facility | Moomba gas plant (250 TJ/d) | Katnook gas plant (10 TJ/d) |

| Pipeline Connection | Moomba to Sydney Pipeline | SEA Gas pipeline (314 TJ/d capacity) |

| Dominant Operator | Santos | Beach Energy |

| Aquifer Risk Profile | Deep formations, arid geology | Shallow water table, porous limestone |

The scale difference between Moomba and Katnook is striking. Moomba's 250 TJ/d throughput dwarfs Katnook's 10 TJ/d nameplate capacity, reflecting the vastly different reserve scales underpinning each region. However, it is the relationship between Katnook and the SEA Gas pipeline that reveals the latent opportunity. The SEA Gas pipeline carries a throughput capacity of 314 TJ/d, which is more than 31 times Katnook's current output ceiling.

The Katnook Gas Plant: A Stranded Asset Awaiting a Decision

Katnook's recent operational history illustrates the reserve adequacy problem that underlies the entire policy debate. Beach Energy, which has owned the facility since 2011, was forced to mothball the plant between July and September 2022 when available reserves proved insufficient to sustain operations at commercial rates. A gas processing plant sitting idle because it has run out of gas to process is perhaps the clearest possible demonstration of what declining production without new exploration looks like in practice.

Beach Energy has indicated that restarting Katnook would not require fracking to source initial feedstock, as some conventional reserves remain available. However, the company's longer-term position is that an early end to the moratorium would meaningfully improve investment confidence in the broader South East exploration program needed to sustain production over the medium term. This distinction between short-term restart capability and long-term development confidence is important: it explains why the industry welcomes the policy change even though the immediate operational impact may be limited.

Environmental Stakes in the Limestone Coast: Why the Risk Profile Is Different

Accepting the government's position that hydraulic fracturing can be conducted safely does not mean ignoring the genuine environmental differences between the South East and the Cooper Basin. Those differences are real and technically significant.

The Limestone Coast's aquifer systems supply water to one of Australia's most productive and economically distinctive agricultural zones. Unlike the deep, confined formations typical of the Cooper Basin's arid geology, the South East's shallow water table and porous limestone composition create a fundamentally different subsurface environment for industrial activity.

Effective regulatory governance of any future South East fracking program would need to address several technical dimensions that have no direct precedent from Cooper Basin operations:

- Wellbore integrity standards calibrated specifically to Otway basin geology and formation pressures

- Comprehensive baseline aquifer monitoring established before any drilling commences, to create a defensible pre-activity reference point

- Full chemical disclosure requirements for fracturing fluid composition

- Ongoing post-activity groundwater testing protocols with defined trigger levels for intervention

- Induced seismicity monitoring, particularly relevant given the UK's experience with tremor events linked to fracking operations that led to its own moratorium in 2019

South Australia's government has described groundwater protection as a non-negotiable condition of any approvals. Translating that political commitment into specific technical standards will be among the most consequential regulatory tasks that follows any legislative passage.

The next major ASX story will hit our subscribers first

How Other Jurisdictions Have Navigated Similar Decisions

South Australia's proposed policy shift takes on additional significance when viewed against the approaches adopted in comparable jurisdictions. Furthermore, the broader LNG supply outlook for the Asia-Pacific region adds further context to why domestic supply decisions carry such weight.

Victoria has maintained a permanent ban on onshore unconventional gas extraction, making South Australia's proposed reversal a notable divergence between two states sharing the same geological basin. If South Australian exploration in the Otway ultimately produces commercially significant results, it may reopen the policy debate on the Victorian side of the border, where similar formations extend.

Queensland and Western Australia permit hydraulic fracturing under state-specific regulatory frameworks that impose environmental conditions without prohibiting the practice outright. Both states have built substantial unconventional gas industries under these frameworks, providing regulatory models that South Australia could adapt.

Internationally, the United Kingdom's 2019 moratorium following induced seismicity concerns offers a cautionary example of what can go wrong when regulatory frameworks are insufficiently tailored to local geological conditions. The UK experience underscores the importance of pre-activity seismic baseline surveys and operational protocols designed to detect and respond to early warning signs before material damage occurs.

From Policy Change to Pipe Pressure: The Nine-Step Supply Pathway

Even in an optimistic scenario, the journey from legislative passage to commercial gas production in the South East involves a lengthy and non-compressible sequence of steps:

- Legislative passage of the amendment bill through the Legislative Council

- Regulatory framework update by state agencies to reflect the new operating environment for South East applications

- Exploration permit applications lodged by companies, primarily Beach Energy as the dominant acreage holder

- Environmental baseline studies including aquifer surveys, seismic profiling, and land use assessments

- Public consultation processes engaging agricultural communities, local government, and environmental stakeholders

- Regulatory decision on individual permit applications, which may be granted, conditioned, or refused

- Drilling and appraisal of exploration wells to assess whether commercially viable reserves exist

- Final investment decision by the operator, contingent on reserve confirmation and economic modelling

- Production ramp-up and pipeline injection connecting new gas into the SEA Gas network and the broader east coast market

Each step carries its own timeline and its own potential for delay. Environmental assessments for projects in sensitive agricultural regions routinely take two to three years. Community consultation in areas with established opposition can extend that further. Exploration drilling and appraisal add additional years before a development decision can be made.

Even under an optimistic scenario, commercial volumes of new South East gas production from fracked wells are unlikely before the early 2030s. The 2029 supply risks identified by AEMO may not be fully addressed by this single policy measure, reinforcing the case for the multi-instrument approach the state government has adopted.

The Renewable Energy Paradox: Why Gas Demand Persists in a Decarbonising Grid

South Australia presents an apparent contradiction: it is simultaneously one of Australia's most advanced states in renewable energy penetration and one of the most vocal advocates for domestic gas supply security. Understanding why these positions are not incompatible requires understanding the technical role gas plays in a high-renewables electricity system.

Wind and solar generation are inherently variable. When wind drops or cloud cover reduces solar output, the grid requires dispatchable generation capacity that can respond quickly to fill the gap. Gas-fired generation currently performs this firming function more flexibly than most alternatives. Consequently, the renewable energy transition does not eliminate gas demand in the short term but rather reshapes its role within the broader energy mix.

This dynamic means that domestic gas supply security is a genuine policy concern for South Australia, not a cover for fossil fuel advocacy. Sourcing that gas domestically from the South East, rather than relying on increasingly constrained interstate supply from depleting Bass Strait fields, has legitimate energy security logic. Moreover, when considering Australia's resource exports and their contribution to national revenue, the case for developing proven domestic reserves becomes even more compelling regardless of one's views on the long-term trajectory of natural gas.

Key Milestones to Track as the Policy Develops

| Milestone | Why It Matters | Expected Timing |

|---|---|---|

| Bill introduction to parliament | Formal start of the legislative process | Imminent as of May 2026 |

| Legislative Council vote | Determines whether the moratorium ends early | Weeks to months from introduction |

| One Nation's voting decision | Likely decisive given parliamentary arithmetic | Concurrent with upper house debate |

| Beach Energy exploration applications | First commercial signal post-passage | Months after legislative passage |

| Baseline environmental assessments | Determines whether projects can proceed to drilling | Multi-year process |

| AEMO annual gas supply outlooks | Benchmark for whether the policy is tracking toward its supply security objectives | Annual reviews |

Frequently Asked Questions

Does lifting the moratorium mean fracking will automatically begin in the South East?

No. Removing the legislative prohibition is the enabling step, not the approval step. Any company wishing to conduct hydraulic fracturing in the South East would still need to obtain individual project approvals through a full regulatory process involving environmental assessment, baseline monitoring, and public consultation before a single well could be drilled.

Why not simply wait for the moratorium to expire in November 2028?

The development lead times for upstream gas projects mean that waiting until 2028 would effectively push any potential new production into the mid-2030s at the earliest. Given that AEMO has flagged supply risks beginning from 2029, the two-year window created by early termination is intended to allow exploration programs to begin earlier, compressing the gap between policy change and market impact.

How does this affect the east coast gas market more broadly?

New South East production would connect directly to the SEA Gas pipeline, which feeds into the broader east coast gas network serving South Australia, Victoria, and New South Wales. The 314 TJ/d capacity of the SEA Gas pipeline significantly exceeds what current South East production could fill, meaning the transportation infrastructure already exists to carry substantially more gas than is currently being produced.

What is the significance of Beach Energy's role?

Beach Energy is the largest acreage holder in the South East region and owns the Katnook gas plant. It is the most likely near-term beneficiary of any moratorium removal, and the company's public support for the legislative change reflects its assessment that the policy shift improves the investment case for longer-term exploration in the SA Otway basin. As Argus Media reported on 14 May 2026, South Australia plans to lift gas fracking ban provisions in a move directly relevant to Beach Energy's operations.

How does South Australia's approach compare to Victoria's?

Victoria has enacted a permanent ban on onshore unconventional gas extraction, including hydraulic fracturing. South Australia's proposed reversal represents a divergence between two states that share the same Otway basin geology, and could have indirect implications for future policy debates on the Victorian side of the border. Indeed, the fact that South Australia plans to lift gas fracking ban restrictions well ahead of schedule marks a significant shift in the regional policy landscape.

Disclaimer: This article contains forward-looking statements, supply projections, and legislative timeline estimates that are subject to change based on parliamentary outcomes, regulatory decisions, and commercial factors beyond public visibility. Nothing in this article constitutes financial, investment, or legal advice. Readers should consult appropriate professional advisers before making decisions based on the information contained herein. Supply projections attributed to AEMO reflect publicly reported commentary and should be verified against AEMO's primary published outlook documents.

Want to Know Which ASX Energy and Resources Companies Are Making Significant Discoveries Right Now?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral and energy discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market — explore Discovery Alert's dedicated discoveries page to understand why major resource discoveries can generate substantial returns, or begin your 14-day free trial today to position yourself ahead of the market.