May 19, 2026

When Solar Giants Collide With the Storage Revolution

The energy transition has never moved in a straight line. For decades, the dominant assumption was that solar generation and battery storage would develop as parallel but separate industries, each with its own supply chains, manufacturers, and market dynamics. That assumption is now unravelling at speed. Across China's industrial heartland, the companies that built their empires on silicon wafers and polysilicon ingots are making calculated moves into battery materials — and the GCL Technology energy storage business represents one of the most significant examples of this structural shift.

Understanding why this is happening, and what it means for the global LFP cathode supply chain, requires looking past the headline announcements and into the deeper mechanics of how clean energy businesses actually generate durable returns.

When big ASX news breaks, our subscribers know first

The Structural Forces Reshaping China's Solar Supply Chain

Polysilicon oversupply has become one of the defining industrial themes of the mid-2020s. Massive capacity expansions between 2021 and 2024 created a situation where global polysilicon production capacity significantly outpaced module demand growth, sending average selling prices into sustained decline. Solar module prices followed a similar trajectory, compressing margins all the way up the upstream supply chain.

For manufacturers whose revenue base is concentrated in these commoditised segments, the financial logic of diversification is straightforward. However, the direction of diversification matters enormously. Companies with deep materials science expertise, established large-scale chemical manufacturing infrastructure, and existing energy service relationships are uniquely positioned to enter adjacent battery materials markets — particularly LFP cathode production — without starting from zero.

Several dynamics are converging to make LFP cathode materials an attractive destination for this capital. Furthermore, the battery raw materials market is itself undergoing rapid structural change, adding further momentum to this transition:

- Global battery energy storage system (BESS) installations have been growing at compound annual rates exceeding 30%, with stationary storage demand accelerating across Asia-Pacific, Europe, and North America.

- LFP has firmly displaced nickel manganese cobalt (NMC) chemistry as the dominant technology for grid-scale and commercial storage applications, driven by its superior safety profile and cycle life economics.

- China's large and rapidly expanding domestic BESS market provides a captive demand base for new cathode material producers before they need to compete in export markets.

- Cathode material supply agreements with downstream cell manufacturers can be structured as long-term offtake contracts, offering more revenue stability than spot-priced polysilicon sales.

Why LFP Chemistry Dominates Stationary Storage Applications

The chemistry itself deserves closer examination, because it explains why LFP has become so entrenched in the stationary storage segment and why new entrants are focusing here rather than on NMC or other chemistries.

| Characteristic | LFP Performance | NMC Comparison |

|---|---|---|

| Thermal Stability | Excellent, low thermal runaway risk | Higher risk, as evidenced by multiple BESS fire incidents |

| Cycle Life | 3,000 to 6,000+ full cycles | Typically 1,000 to 2,000 cycles |

| Cobalt Dependency | Zero | Significant |

| Cost Per kWh | Among lowest of all lithium-ion chemistries | Higher, driven by cobalt pricing |

| Energy Density | Lower than NMC | Higher volumetric density |

| Grid Storage Suitability | Excellent | Less optimal for long-duration cycling |

A notable recent data point underscores LFP's market momentum. China's CEEC (China Energy Engineering Corporation) completed a 7 GWh battery storage cell procurement in May 2026 where the lowest-end prices for large-format LFP cells reached approximately $47 per kWh, according to ESS News reporting. This pricing level signals how far LFP cell costs have fallen and illustrates the competitive intensity new cathode producers will face.

The fire safety dimension has also become increasingly material. A confirmed NMC battery short circuit caused a fire at a UK grid-scale BESS project in early May 2026, reinforcing the industry-wide preference for LFP in new deployments. As ESS News reported, the incident involved one of the UK's oldest operational BESS sites and occurred at a project using early-generation NMC technology — the chemistry type that has now been largely superseded by LFP in new projects globally. In addition, the broader shift towards battery storage expansion continues to accelerate demand for safer, longer-lasting chemistries like LFP.

GCL Technology's Energy Storage Business: Architecture and Ambition

From Polysilicon Producer to Materials Platform

GCL Technology occupies a significant position in China's solar supply chain. Its manufacturing ecosystem spans polysilicon and granular silicon production, solar modules through GCL System Integration (GCL-SI), and perovskite solar technology development through GCL Optoelectronics. The company's fiscal year 2025 results, however, laid bare the financial pressure that has accelerated its strategic transformation.

For FY2025, GCL Technology reported:

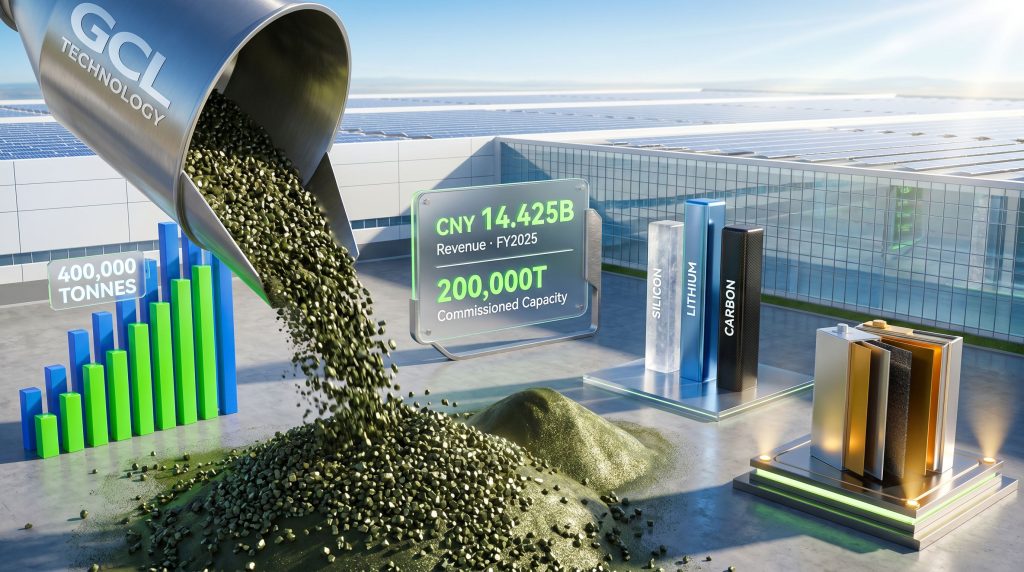

- Total revenue: CNY 14.425 billion (approximately USD 2.12 billion), down 4.5% year-on-year

- Net loss attributable to shareholders: CNY 2.868 billion, concentrated in the polysilicon segment

- Granular silicon remained the company's largest single revenue-generating segment despite the losses, indicating the transition away from polysilicon will be gradual

The financial reality of FY2025 is not merely a poor earnings cycle. It reflects a structural compression that is unlikely to reverse quickly given the volume of new polysilicon capacity still coming online across China's industrial provinces.

The Silicon, Lithium, and Carbon Platform Framework

GCL Technology has articulated its transformation around three material pillars: silicon (existing polysilicon and solar materials), lithium (new LFP battery materials), and carbon (carbon-based energy products and emissions-related services). This framing is strategically significant because it positions the company not as a solar business adding a storage division, but as a diversified materials science platform serving the clean energy economy across multiple vectors simultaneously.

The distinction matters for how investors and industrial customers perceive the business. A solar company diversifying into storage is still fundamentally dependent on solar market conditions. A materials platform serving silicon, lithium, and carbon markets can, in theory, rebalance revenue exposure as each segment moves through its own demand cycle.

Existing Energy Services Infrastructure as a Commercial Foundation

Before the LFP cathode expansion, GCL's energy arm had already established operational presence across a range of storage-adjacent businesses. Consequently, this existing infrastructure creates a strategically important internal demand channel:

- Virtual power plants (VPPs): Aggregating distributed generation and storage assets for grid balancing services

- Solar-storage-charging-swapping systems: Integrated infrastructure combining photovoltaic generation with EV charging and battery swapping

- Energy trading and microgrid operations: Grid flexibility services generating recurring revenue

- Carbon asset services: Monetising verified emissions reductions for compliance and voluntary markets

- Energy efficiency management: Industrial and commercial optimisation contracts

GCL's LFP cathode material does not need to compete exclusively in the open market from day one. GCL-SI's integrated solar-plus-storage products represent a natural internal customer, and the VPP and microgrid operations provide additional pull-through demand as those businesses scale.

The Xinneng LFP Cathode Facility: Technical Specifications and Production Status

Scale and Current Commissioning Status

GCL Technology's LFP cathode material project is located in Xinneng, China, and is operated by subsidiary Leshan Xinneng New Material Technology Co., Ltd. The project's total planned annual capacity is 400,000 tonnes of LFP cathode material. As of mid-2026, the facility had reached an initial commissioned capacity of 200,000 tonnes per year and entered the commissioning stage.

For context, a 400,000-tonne nameplate capacity for LFP cathode material would represent a substantial addition to global supply. The phased approach, beginning at half the total planned capacity, reflects standard practice in large-scale chemical manufacturing: quality validation, process stabilisation, and customer qualification all need to be completed before full-scale production ramp is commercially viable.

GCL's Iron Oxide Red-Based LFP Process: What Makes It Different?

GCL Technology has specified that its LFP product is based on a physically synthesised iron oxide red-based lithium iron phosphate production process. This distinguishes the company's approach from conventional LFP synthesis routes, which typically use either iron phosphate (FePO4) or ferrous oxalate as the iron source.

The iron oxide red-based route is less commonly used at industrial scale, and GCL's claimed advantages for this approach include:

- Higher compacted density, meaning more active material can be packed into a given cell volume, improving volumetric energy density at the cell level

- Greater capacity, measured in milliampere-hours per gram of cathode material

- Improved voltage stability across charge-discharge cycles

- A more energy-efficient production process with a lower manufacturing carbon footprint

- A cost structure that GCL claims is competitive relative to conventional LFP cathode manufacturing

Important caveat: These performance claims are company-disclosed and have not been independently verified through publicly available third-party testing or peer-reviewed technical publications as of the date of this article. Buyers and investors should treat them as indicative until external validation is available.

The absence of independent verification is not unusual at the commissioning stage of a new chemical manufacturing facility. However, it does mean the differentiation narrative remains a commercial claim rather than an established technical fact, and competitive response from established LFP cathode producers should be expected once GCL begins approaching cell manufacturer customers at scale.

Risk Factors and Strategic Vulnerabilities

The Oversupply Paradox

One of the most significant risks in GCL's LFP cathode strategy is the one most familiar from its existing business: the potential for capacity additions to outpace demand growth and compress margins before scale is achieved. China's LFP cathode industry has been expanding rapidly, with multiple producers accelerating capacity plans in response to global storage demand growth.

GCL entering at 200,000 to 400,000 tonnes per year joins a market where established producers have multi-year head starts on process optimisation, customer relationships, and quality track records. If the LFP cathode market follows the trajectory of polysilicon, the window for new entrants to capture premium pricing may be limited. For further context on how Chinese producers are managing material cycles, China's battery recycling outlook offers a useful parallel on how the broader ecosystem is evolving.

Lithium Carbonate Price Volatility

LFP cathode material economics are directly tied to lithium carbonate spot prices, which have been among the most volatile commodity prices globally over the 2021 to 2025 period. Understanding lithium carbonate dynamics is therefore essential for any assessment of GCL's cathode business viability. Prices swung from below $10,000 per tonne in early 2021 to over $80,000 per tonne in late 2022 before collapsing back toward the $10,000 range through 2024. This volatility directly affects LFP cathode production costs and the economics of long-term supply contracts.

Export Market Trade Barriers

GCL's Chinese production base creates competitive advantages for domestic supply but faces growing headwinds in export markets:

- The European Union extended its funding restrictions on high-risk Chinese-supplied energy components to battery power conversion systems (PCS) in May 2026, according to ESS News reporting. This policy applies to billions in European Investment Bank funding for renewable and storage projects, signalling a broader pattern of European supply chain scrutiny.

- US Inflation Reduction Act provisions around domestic content requirements create structural barriers for direct Chinese materials entering the US battery supply chain.

- Southeast Asian and Middle Eastern markets currently offer more accessible near-term export pathways, though competition from other Chinese producers in these regions is also intensifying.

The next major ASX story will hit our subscribers first

Competitive Positioning Within the LFP Supply Chain

Where GCL Sits in the Value Chain

GCL's entry at the cathode materials level, rather than at the cell or full system integration level, is a deliberate strategic choice with meaningful implications. Furthermore, the Chinese battery recycling breakthrough occurring in parallel signals that the entire Chinese battery materials ecosystem is rapidly maturing across multiple fronts simultaneously.

| Entry Point | Capital Requirement | Customer Base | Margin Profile | GCL's Position |

|---|---|---|---|---|

| Cathode materials | High, but lower than cell manufacturing | Cell manufacturers, battery producers | Subject to commodity pricing | Current focus |

| Cell manufacturing | Very high, requires cell fab | BESS integrators, OEMs | Better, if differentiated | Not announced |

| System integration | Moderate | Project developers, utilities | Service-based, recurring | Via GCL-SI |

By entering at the materials layer, GCL can potentially supply multiple competing cell manufacturers simultaneously, avoiding the channel conflict that would arise from full cell manufacturing. GCL-SI's existing solar-plus-storage product line provides a parallel integration pathway that does not require the GCL Technology energy storage business to build cell manufacturing capabilities immediately.

The broader trend this represents — where large Chinese solar and materials manufacturers pivot into battery materials rather than cells — reflects a rational division of labour within China's clean energy industrial ecosystem. As PV Magazine recently reported, companies like GCL bring manufacturing scale, chemical process expertise, and supply chain infrastructure. Cell manufacturers, in contrast, bring electrochemical engineering depth and customer qualification relationships. The two capabilities are consequently complementary rather than competitive at the current stage of the market's development.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and company-disclosed performance claims referenced in this article involve inherent uncertainty. Readers should conduct independent research before making any investment decisions.

Want to Track the Next Big Battery Materials Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across lithium, iron ore, and the full spectrum of battery materials driving the clean energy transition — explore historic examples of major discovery returns to understand the opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.