July 14, 2026

When Geography Becomes Strategy: The Logic Reshaping Australia's Gold Sector

In mining, proximity is not just a convenience, it is a competitive moat. The most defensible synergy cases in the history of gold M&A activity have almost always been built on one foundational principle: two operations sharing the same geological address. When processing infrastructure, haulage networks, and ore bodies sit within kilometres of each other, the arithmetic of consolidation shifts decisively in favour of the acquirer. This dynamic sits at the very heart of the Genesis Vault merger, a transaction that has redefined the scale ambitions of Australia's mid-tier gold sector and triggered one of the most closely watched corporate contests on the ASX in recent years.

When big ASX news breaks, our subscribers know first

Why Western Australia's Goldfields Have Become a Consolidation Battleground

The Eastern Goldfields and Leonora district of Western Australia have long been recognised as among the world's highest-grade, most infrastructure-rich gold-producing regions. What has changed in the current cycle is the intensity of corporate competition for the remaining independent mid-tier assets within this corridor.

Sustained record gold prices have fundamentally altered the dealmaking calculus for ASX-listed producers. When gold trades at multi-year highs, acquisition premiums that would previously have been considered financially unjustifiable become absorbable within a reasonable synergy payback window. This creates a permissive environment for aggressive bidding, and that is precisely what the events of mid-2026 demonstrated.

Before the Genesis Vault merger crystallised, Vault Minerals had already agreed to an all-stock combination with Regis Resources, a deal signed in May 2026. That agreement established Vault's value within the market's mind but also, inadvertently, signalled to competing producers that the asset was in play. The competitive bidding environment that followed is a textbook illustration of how a single announced transaction can catalyse a broader auction dynamic.

Furthermore, the displacement of an existing merger agreement by a superior competing bid is relatively uncommon in ASX gold M&A. When it occurs, it typically reflects both the quality of the underlying asset and the strategic desperation of acquirers who recognise that consolidation windows do not remain open indefinitely.

The Core Terms of the Genesis Vault Merger: What the Numbers Reveal

Understanding the financial architecture of this transaction is essential for evaluating both its strategic logic and its execution risk.

| Merger Component | Specific Terms |

|---|---|

| Consideration per Vault share | 0.7629 new Genesis shares + A$0.475 cash |

| Implied per-share value | A$5.274 per Vault share |

| Premium to last closing price | 15.7% |

| Premium over displaced Regis offer | 14.5% |

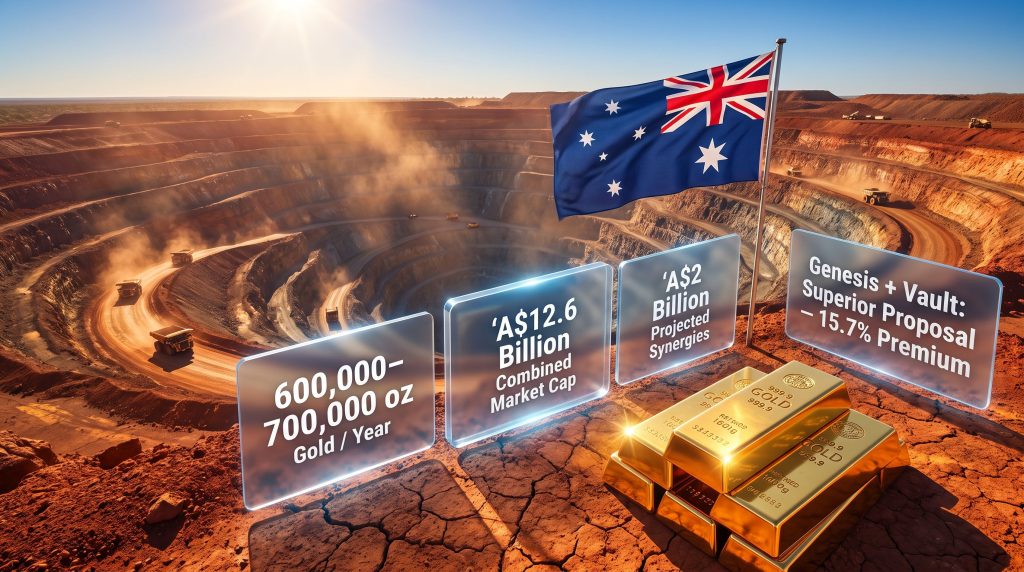

| Total Vault acquisition value | ~A$5.6 billion (approx. US$3.9 billion) |

| Combined entity market capitalisation | A$12.6 billion (approx. US$8.71 billion) |

The structure of the consideration is itself analytically meaningful. The rejected gold bid from Regis was an all-stock exchange, which transfers the full execution risk to target shareholders. Genesis, however, chose a cash-and-scrip approach, blending A$0.475 per share in cash with a fixed share exchange ratio. This design serves multiple purposes simultaneously.

Cash components reduce uncertainty for Vault shareholders by locking in a defined floor value, regardless of short-term Genesis share price volatility between announcement and completion. From a market psychology perspective, the presence of cash in an offer typically signals acquirer conviction and financial capacity, making the proposal more credible to institutional shareholders who must assess deal completion probability alongside headline valuation.

Ownership and Board Composition Post-Merger

The governance architecture of the combined entity reflects the relative scale differential between the two companies:

- Genesis shareholders will retain approximately 59.8% of the combined group

- Vault shareholders will hold approximately 40.2% of the merged entity

- The board will comprise 7 directors total: 4 nominated by Genesis and 3 nominated by Vault

- This split preserves meaningful Vault board representation while ensuring Genesis retains operational and strategic control

The 4:3 board ratio is an important detail. It prevents Vault's nominees from being reduced to a purely ceremonial presence while still ensuring the acquirer's strategic vision drives the combined entity's direction. In Australian corporate governance terms, this structure is consistent with how major scheme of arrangement transactions typically balance acquirer control against target stakeholder interests.

The Synergy Architecture: Why A$2 Billion Is Believable

Synergy projections in mining M&A are frequently met with scepticism, and not without reason. The history of large-scale mining combinations includes numerous examples where anticipated cost savings failed to materialise against the operational complexity of integrating distinct mining cultures, legacy systems, and geographically dispersed infrastructure.

The Genesis Vault merger synergy case is, however, structurally different from most, and this is where geological proximity becomes the analytical centrepiece.

How Geographic Clustering Creates Hard Cost Savings

Genesis's established operations in the Leonora district sit in direct proximity to Vault's core asset portfolio, which includes the Bardoc-Mt Monger operations and the King of the Hills mine. This clustering creates tangible cost reduction pathways that are not available to geographically dispersed acquirers:

- Processing consolidation: Ore from multiple sources can be directed to the most cost-effective processing facility, improving throughput utilisation rates and reducing per-ounce processing costs

- Haulage and logistics rationalisation: Shared haulage corridors eliminate duplicated trucking infrastructure and reduce fuel and labour costs per tonne of ore moved

- Camp and overhead consolidation: Remote mining operations carry significant fixed costs in accommodation, catering, and site services. Combining proximate operations onto shared camp infrastructure produces immediate overhead savings

- Technical services integration: Geology, engineering, and planning teams supporting adjacent operations can be merged without meaningful productivity loss, reducing duplicated corporate overhead

Of the total A$2 billion in projected post-tax synergies over 10 years, Genesis has identified A$1.5 billion as uniquely achievable through the Genesis-Vault pairing and not replicable under the Regis alternative. This is a critical distinction. Regis Resources, while a credible mid-tier producer, does not share the same operational footprint adjacency to Vault's core assets. The geographic fit argument, therefore, is not promotional language but a substantive differentiator that directly influenced Vault's board determination.

Comparing the Competing Offers

According to reporting on the competing bids, the contrast between the two proposals is stark across multiple evaluation dimensions:

| Evaluation Dimension | Genesis Offer | Regis Offer (Displaced) |

|---|---|---|

| Consideration structure | Cash + shares | All-stock only |

| Premium to market | 15.7% | Lower (basis for superior proposal finding) |

| Unique synergy value identified | A$1.5 billion | Not identified as equivalent |

| Geographic operational fit | High (Leonora proximity) | Lower adjacency |

| Board recommendation outcome | Unanimous superior proposal | Superseded |

The Approval Pathway: What Needs to Happen Before Completion

The Genesis Vault merger must navigate a multi-stage approval process before it becomes legally binding. Each stage carries its own execution risk, and investors monitoring this transaction should understand the precise sequence of required milestones.

- Regis Resources matching right expiry – Regis held a contractual right to match or improve its offer until 11:59pm AWST on July 10, 2026. The expiry of this window without a Regis counterbid cleared the path for Genesis to proceed

- Execution of binding merger implementation agreement – Formalisation of the legal agreement between Genesis and Vault

- Independent expert assessment – A qualified independent expert must opine that the scheme is in the best interests of Vault shareholders

- Vault shareholder vote – Requires a minimum of 75% of voting shareholders to approve the scheme

- Court approval – As a scheme of arrangement under Australian corporate law, the transaction requires judicial sanction

- Regulatory clearances – Standard FIRB (Foreign Investment Review Board) and competition review processes applicable to major ASX transactions

Under Australia's scheme of arrangement framework, the 75% shareholder approval threshold is materially higher than the simple majority required in many comparable jurisdictions. This structural feature of Australian corporate law provides stronger minority shareholder protection but also means that a concentrated bloc of dissenting Vault shareholders could theoretically block an otherwise broadly supported transaction.

If the 75% threshold is not achieved, the scheme lapses. Genesis could theoretically pursue an alternative off-market takeover offer structure, but this would likely require a higher premium to achieve the same result through individual shareholder acceptances, increasing the total cost of the acquisition.

Production Scale and Competitive Positioning

The combined entity's projected annual output of 600,000 to 700,000 ounces of gold per year is the metric that carries the most weight from a long-term investor valuation perspective.

In the global gold mining hierarchy, this production band places the merged Genesis-Vault group comfortably within the category of significant mid-tier producers, with a scale that attracts institutional index inclusion, analyst coverage depth, and, critically, the cost-per-ounce efficiencies that accompany higher throughput volumes.

At a combined market capitalisation of A$12.6 billion (approximately US$8.71 billion), the merged group also enters a size bracket where it becomes relevant to global precious metals funds and sector ETFs that apply minimum market cap screening thresholds. This re-rating potential from expanded institutional accessibility is frequently underappreciated by retail investors analysing the standalone economics of individual merger components.

The Broader Consolidation Pattern in ASX Gold

The Genesis Vault merger does not exist in isolation. It reflects a broader structural reorientation underway across gold mining equities on the ASX, where multiple mid-tier producers have been pursuing scale through acquisition rather than organic development. Several factors reinforce why this trend is likely to continue:

- Development capital inflation: The cost of building new mines from greenfield has increased substantially, making it financially rational to acquire existing production rather than fund new construction

- Permitting timelines: New mine development in Australia, while comparatively faster than Canada (where PwC data indicates timelines run approximately six years longer), still involves multi-year approval processes that favour acquisition of permitted, operating assets

- Investor preference for production certainty: In a high gold price environment, markets increasingly reward producers with confirmed output rather than developers with uncertain timelines

- Western Australia's infrastructure advantage: The Goldfields region's established power, water, and haulage networks lower the marginal cost of incremental production expansion compared to more remote Australian jurisdictions

Analysts tracking the transaction note that the Genesis Vault merger has effectively redrawn the competitive map of the Leonora and Eastern Goldfields corridor, concentrating significant geological and processing capacity under a single management team and making the remaining independent operators in the region simultaneously more valuable and more exposed to competitive pressure.

The next major ASX story will hit our subscribers first

Key Metrics Summary

| Metric | Value |

|---|---|

| Combined market capitalisation | A$12.6 billion (US$8.71 billion) |

| Vault acquisition value | A$5.6 billion (US$3.9 billion) |

| Premium to Vault's last close | 15.7% |

| Premium over Regis offer | 14.5% |

| Projected annual production | 600,000-700,000 oz gold |

| Genesis ownership post-merger | ~59.8% |

| Vault ownership post-merger | ~40.2% |

| 10-year post-tax synergies | A$2 billion |

| Genesis-specific unique synergies | A$1.5 billion |

| Minimum shareholder approval required | 75% of voting Vault shareholders |

Frequently Asked Questions: Genesis Vault Merger

What is the Genesis Vault merger?

Genesis Minerals (ASX: GMD) has agreed to acquire Vault Minerals (ASX: VAU) through a scheme of arrangement valued at approximately A$5.6 billion, forming a combined Australian gold producer with a market capitalisation of around A$12.6 billion.

How much are Vault shareholders receiving per share?

Each Vault share is valued at A$5.274 under the Genesis offer, structured as 0.7629 new Genesis shares plus A$0.475 in cash, representing a 15.7% premium to Vault's last closing price.

Why did Vault's board choose Genesis over Regis Resources?

Vault's board unanimously declared the Genesis proposal a superior offer because it provides a 14.5% premium over the all-stock Regis deal, incorporates a cash component that reduces execution risk, and is supported by an estimated A$1.5 billion in synergies uniquely achievable through the Genesis-Vault geographic combination.

What approvals are needed to complete the transaction?

The merger requires at least 75% approval from voting Vault shareholders, an independent expert's fairness opinion, court approval under Australia's scheme of arrangement process, and standard FIRB and competition regulatory clearances.

What annual gold production will the merged company achieve?

The combined Genesis-Vault entity is projected to produce between 600,000 and 700,000 ounces of gold per year, positioning it as a significant mid-to-major tier producer within the ASX gold sector.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Synergy projections, production forecasts, and transaction completion timelines involve inherent uncertainty. Investors should conduct independent due diligence and consult a licensed financial adviser before making investment decisions. All financial figures are sourced from publicly available company and market disclosures.

Want to Capitalise on the Next Major ASX Gold Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model instantly notifies subscribers of significant ASX mineral discoveries — turning complex geological data into clear, actionable opportunities the moment they are announced. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.