July 7, 2026

The Invisible Metal Powering Modern Defence and Why Western Nations Are Racing to Secure It

Most people have never heard of germanium. Fewer still could identify its applications. Yet this obscure metalloid sits at the intersection of some of the most consequential technology systems of the 21st century: infrared optics for military targeting systems, fibre optic networks carrying global internet traffic, and the semiconductor substrates underpinning next-generation chip architectures. Its invisibility to the general public is inversely proportional to its strategic importance, and that contradiction is exactly why governments across the Western world are now scrambling to secure domestic supply.

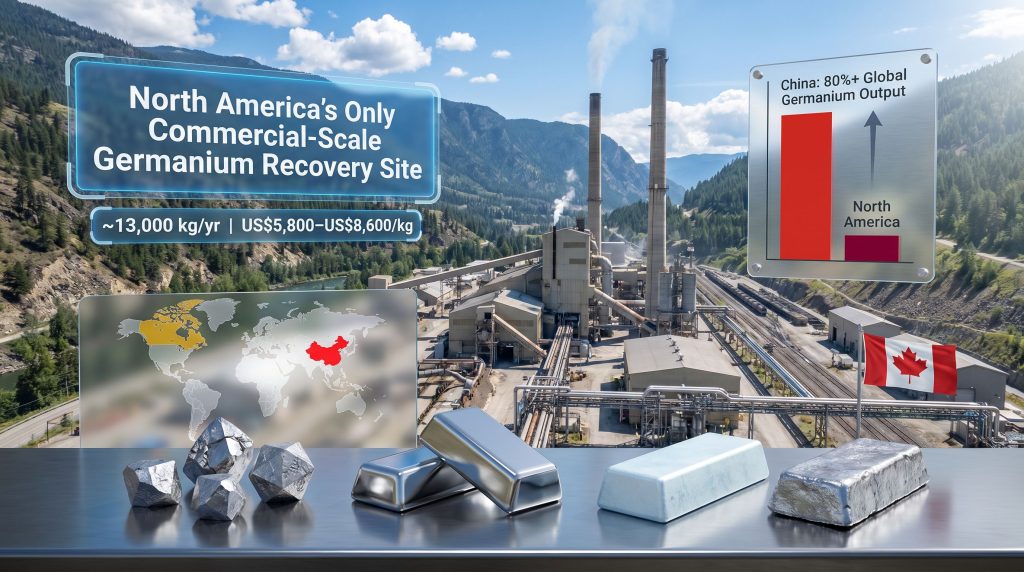

The structural problem is stark. A single country controls more than 80% of global germanium output, and that country has already demonstrated a willingness to restrict exports when geopolitical conditions shift in its favour. For industries and defence establishments that depend on a consistent, predictable germanium supply, that concentration of production represents a vulnerability that no amount of diplomatic goodwill can fully neutralise.

When big ASX news breaks, our subscribers know first

Why Germanium Is Not a Typical Critical Mineral

Understanding the urgency behind Teck Trail germanium output funding requires grasping something that distinguishes germanium from other critical minerals: it is almost never mined directly. Germanium exists in the Earth's crust at an average concentration of roughly 1.6 parts per million, making standalone mining economically unviable in most circumstances. Instead, it is recovered as a byproduct from zinc smelting operations, where it concentrates in the residues and flue dusts generated during the refining process.

This byproduct dependency creates a supply chain that is fundamentally different from primary metal markets. Germanium production is constrained not just by its own market dynamics but by the economics of zinc mining itself. If zinc prices fall and zinc operations curtail output, germanium supply contracts regardless of germanium demand or pricing. This structural coupling means that building resilient germanium supply chains requires investing in integrated zinc processing infrastructure, not simply developing dedicated germanium projects.

The recovery process involves extracting germanium-bearing residues from zinc smelter operations, followed by hydrometallurgical processing steps including leaching, solvent extraction, and distillation to produce germanium dioxide (GeO2), which is then reduced to produce refined germanium metal or converted into specialty compounds. The technical complexity of this process is significant, and very few facilities in the world have the scale and expertise to execute it commercially.

The Applications That Make Germanium Irreplaceable

Germanium's unique physical properties, including its high refractive index and transparency to infrared radiation, make it extraordinarily difficult to substitute in several critical applications:

- Infrared optics: Germanium lenses and windows are standard in thermal imaging systems used in military targeting, night vision equipment, and border surveillance technology

- Fibre optic cables: Germanium tetrachloride is used to modify the refractive index of glass in optical fibre manufacturing, with demand growing alongside global internet infrastructure buildout

- Semiconductor substrates: Germanium-on-insulator wafers are used in high-efficiency multi-junction solar cells for space applications and in certain advanced transistor architectures

- Polymerisation catalysts: Germanium dioxide serves as a catalyst in the production of polyethylene terephthalate (PET), with applications in food packaging and textiles

The defence and telecommunications applications in particular carry strategic weight that purely commercial assessments often understate. A country that cannot reliably procure germanium faces potential gaps in its military optical systems and its ability to maintain and expand fibre optic infrastructure. Furthermore, the critical minerals demand surge across Western economies is intensifying competition for exactly these kinds of materials.

Teck's Trail Operations: North America's Only Commercial-Scale Recovery Facility

Located in Trail, British Columbia along the Columbia River, Teck Resources' Trail Operations complex holds a unique position in North American metals processing. The facility functions as one of the world's largest integrated zinc and lead smelters, processing zinc concentrate sourced from multiple mines including Teck's Red Dog operation in Alaska.

What makes Trail strategically irreplaceable is not just its scale but its specialty metals recovery capability. The smelter has developed, over many decades, the infrastructure and metallurgical expertise to extract and refine germanium, indium, and antimony as byproducts of its primary zinc and lead operations. No other North American facility combines this breadth of specialty metal recovery at commercial scale.

| Specialty Metal | Primary Use Case | Trail's Role |

|---|---|---|

| Germanium | Semiconductors, defence optics, fibre optics | North America's only commercial-scale primary recovery site |

| Indium | Flat panel displays, thin-film solar cells | Co-produced at Trail |

| Antimony | Flame retardants, ammunition, batteries | Co-produced at Trail |

| Refined Zinc | Industrial galvanising, alloys | Core output of Trail smelter |

| Refined Lead | Batteries, construction materials | Core output of Trail smelter |

Teck is not only North America's largest germanium producer but also Canada's sole supplier of germanium dioxide to the United States. That bilateral supply relationship gives Trail an economic and diplomatic significance that extends well beyond its British Columbia footprint. In addition, the antimony supply risks associated with Trail's co-produced metals compound the strategic case for sustained federal investment.

The $230 Million Capital Requirement and the Path to $100 Million in Annual Specialty Metal Revenue

Trail's existing specialty metals operations are productive but require substantial capital investment to expand throughput and modernise processing infrastructure. Reports indicate an internal capital requirement of approximately $230 million to sustain current operations while scaling germanium recovery capacity meaningfully.

The longer-term commercial target is ambitious: Teck has indicated aspirations to build Trail's specialty metals portfolio toward generating approximately $100 million per year in revenue from germanium, indium, antimony, and related products. Achieving that target requires both infrastructure investment at Trail and the development of new germanium feedstock sources, which is where the Titan Mining partnership becomes significant.

The Federal Funding Architecture: Three Channels, One Strategic Objective

Reports indicate that the Canadian federal government is preparing to commit hundreds of millions of dollars to the Trail expansion through a blended capital structure drawing on three distinct federal financing mechanisms. While the formal announcement was scheduled for July 2026, the multi-agency structure itself reflects a deliberate policy design rather than administrative convenience.

- Natural Resources Canada (NRCan): The federal department responsible for Canada's minerals and energy policy, providing grant or contribution funding aligned with the Critical Minerals Strategy

- Canada Growth Fund (CGF): A federal investment vehicle established to deploy patient capital into projects that advance Canada's clean economy and supply chain resilience objectives

- Export Development Canada (EDC): Canada's export credit agency, which provides debt financing and risk mitigation tools for Canadian companies expanding export-oriented production capacity

The simultaneous deployment of grant, equity-oriented, and debt financing instruments represents a sophisticated co-investment model. Each mechanism serves a distinct risk-mitigation function: NRCan funding reduces upfront capital costs, CGF capital tolerates longer return timelines, and EDC financing provides commercial debt on terms that reflect the project's strategic importance to Canadian export competitiveness.

This multi-agency approach signals that Ottawa views Trail not as a single company's infrastructure problem but as a national industrial asset requiring coordinated public investment to reach its strategic potential.

For context, the scale of ambition is consistent with other recent federal critical mineral commitments. Canada's critical minerals strategy has evolved considerably, and in March 2026, EDC and the Canada Infrastructure Bank jointly committed C$459 million in senior debt financing to support Nouveau Monde Graphite's Matawinie graphite project in Quebec. The Trail investment, if confirmed at a comparable scale, would represent one of the largest federal commitments to an already-operational processing facility in Canadian mining history.

| Investment Example | Reported Amount | Federal Mechanisms | Status |

|---|---|---|---|

| Nouveau Monde Graphite, Matawinie QC | C$459M (approx. US$335M) | EDC + Canada Infrastructure Bank | Committed, March 2026 |

| Teck Trail Germanium Expansion | Hundreds of millions CAD | NRCan + CGF + EDC | Announcement pending, July 2026 |

A Policy Shift Worth Noting: From Explorers to Operators

Historically, federal critical mineral programmes in Canada have concentrated resources on exploration-stage companies and early-development projects, where the financing gap is largest relative to private capital availability. Directing comparable investment toward an operational, revenue-generating facility like Trail represents a meaningful evolution in federal industrial policy.

The logic is defensible. Trail already has the infrastructure, the expertise, and the proven metallurgical processes. What it lacks is the capital to scale those processes to a level commensurate with Western demand. From a policy efficiency standpoint, investing in an operational facility with demonstrated recovery capability may generate faster supply chain impact than funding greenfield development, which typically requires years of permitting and construction before producing a single kilogram of germanium.

The Titan Mining Partnership: Extracting Strategic Value From Waste

One of the more technically interesting dimensions of Teck's germanium expansion strategy is the cooperation agreement signed with Titan Mining on May 14, 2026. Rather than developing new mines or processing facilities, the partnership targets germanium recovery from existing zinc tailings at Titan's Empire State Mine in New York State.

Tailings are the finely ground waste rock left after valuable minerals have been extracted from ore. In zinc mining operations, tailings can retain measurable concentrations of germanium that were not economically recoverable using older processing technologies. Advances in hydrometallurgical extraction now make it possible to re-process these historical waste streams as germanium feedstock, without the permitting timelines, environmental footprint, or capital intensity of new mine development.

| Metric | Detail |

|---|---|

| Projected Annual Recovery | ~13,000 kg of germanium |

| Market Price Range | US$5,800 to US$8,600 per kg |

| Estimated Annual Revenue Potential | US$75M to US$112M |

| Source Material | Zinc mine tailings (waste streams) |

| Partnership Agreement Date | May 14, 2026 |

| Location | Empire State Mine, New York State |

At US$5,800 to US$8,600 per kilogram, the implied annual revenue from 13,000 kilograms of recovered germanium ranges from approximately US$75 million to US$112 million. That figure alone would go a substantial way toward Trail's $100 million annual specialty metals revenue target.

The cross-border dimension of this partnership also carries strategic resonance. A Canadian smelter processing germanium recovered from American zinc mine waste and supplying refined germanium dioxide back to US customers represents exactly the kind of integrated North American supply chain that both governments have been advocating. Consequently, this arrangement aligns closely with the broader minerals security partnership frameworks that have gained prominence since trade tensions with China intensified following the 2024 export restriction episode.

Understanding China's Germanium Restrictions and Why Lifting Them Changed Nothing Structurally

In 2024, China's export controls on germanium and antimony destined for the United States cited national security concerns in language that mirrored the justifications Western governments had used to restrict Chinese access to advanced semiconductor technology. The restrictions sent an immediate signal to Western defence and technology industries that supply chain exposure to Chinese-controlled critical minerals was not a theoretical risk but an operational one.

China suspended those restrictions in late 2025, but the episode's legacy endured. Western governments and industrial procurement managers drew a clear lesson: Chinese export policy can change rapidly, and reliance on a single dominant supplier creates fragility that cannot be managed through commercial hedging alone. Even with restrictions lifted, the underlying structural vulnerability, that the United States has essentially no domestic germanium production capacity, remained completely unaddressed.

The suspension of China's germanium export restrictions removed an immediate constraint but did nothing to alter the fundamental supply concentration risk. For Western governments, the relevant question shifted from whether China would restrict exports again to when.

This calculus has driven urgency into federal investment decisions that might otherwise have proceeded at a more measured pace. The Teck Trail germanium output funding is therefore not just a commercial infrastructure project but a hedge against a supply disruption scenario that has already been demonstrated as plausible.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Teck Trail Germanium Output Funding

What Does Trail Operations Actually Produce?

Trail is an integrated zinc and lead smelter that also recovers specialty metals including germanium, indium, and antimony as byproducts. It is North America's largest facility of its kind and the continent's only commercial-scale primary germanium recovery operation.

Why Is Germanium Classified as a Critical Mineral?

Germanium has no viable substitute in several high-value applications, including infrared military optics and fibre optic manufacturing, and its supply is heavily concentrated in a single geopolitical jurisdiction. These characteristics place it on critical mineral lists maintained by Canada, the United States, the European Union, and Australia.

Which Federal Agencies Are Expected to Participate in the Trail Funding?

Reports identify Natural Resources Canada, the Canada Growth Fund, and Export Development Canada as the three expected federal financing channels. Each provides a distinct form of capital suited to different aspects of the investment structure.

How Does the Teck-Titan Partnership Expand Germanium Supply Without New Mines?

The partnership targets germanium recovery from existing zinc tailings at the Empire State Mine in New York. Re-processing historical waste streams avoids the permitting timelines and capital intensity of new mine development while adding meaningful germanium feedstock to Trail's processing pipeline.

What Is the Current State of US Domestic Germanium Production?

The United States currently has no meaningful domestic germanium production capacity. All commercially usable germanium consumed in the US is either imported or sourced from Canada, making Trail's output directly relevant to American supply security.

What Investors and Industry Observers Should Watch

Several variables will determine whether the Trail investment delivers on its strategic promise:

- Formal announcement confirmation: The ministerial announcement scheduled for Trail in July 2026 will clarify actual commitment sizes, funding structures, and attached conditions

- Capital deployment timelines: Federal co-investment commitments do not always translate immediately into construction activity; the pace of actual capital deployment will determine when expanded germanium output materialises

- Germanium price trajectory: At current prices of US$5,800 to US$8,600 per kilogram, the commercial case is compelling, but price volatility in specialty metals markets can shift project economics materially

- China's export policy evolution: Any re-imposition of germanium export restrictions would dramatically increase the strategic premium placed on Western supply capacity and potentially accelerate investment timelines

- Tailings processing technology performance: The Titan partnership's 13,000 kg/year target depends on hydrometallurgical processing achieving recovery rates from zinc tailings that, while technically feasible, have not yet been demonstrated at full commercial scale at this specific site

The combination of federal co-investment, an operational processing anchor in Trail, and a capital-efficient tailings recovery partnership with Titan Mining gives Teck a multi-pronged germanium strategy that few other companies in the world can replicate. Whether that strategy delivers on its full potential will depend on execution, market conditions, and the continued willingness of Western governments to treat processing infrastructure as strategic national assets worthy of sustained public investment.

This article contains forward-looking information regarding potential investment commitments, production targets, and revenue projections. Such statements involve known and unknown risks and uncertainties. Readers should not place undue reliance on forward-looking information, and independent financial advice should be sought before making investment decisions based on the content of this article.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex data across 30-plus commodities to surface actionable opportunities in critical minerals like germanium and beyond. Start your 14-day free trial today and explore historic discoveries that generated extraordinary returns for investors who positioned early.