July 12, 2026

The Commodity Control Revolution Reshaping Critical Mineral Markets

When governments decide that market forces are no longer working in their favour, they reach for the one lever that cannot be ignored: the export tap. Across multiple critical mineral categories in 2025 and 2026, sovereign producers have moved decisively toward supply management, replacing passive price-taking with active price-making. Cobalt, produced overwhelmingly within the Democratic Republic of Congo, has become one of the most dramatic examples of this shift, with consequences rippling through battery supply chains, electric vehicle procurement strategies, and global commodity trading desks.

Understanding the mechanics, scale, and strategic logic behind the Glencore DRC cobalt export quotas is no longer optional for anyone with exposure to energy transition materials, critical mineral markets, or major diversified mining companies.

When big ASX news breaks, our subscribers know first

Why the DRC Chose Supply Control Over Market Reliance

The DRC's decision to intervene in cobalt markets was not impulsive. It followed a prolonged and severe price collapse that pushed cobalt spot prices to nine-year lows by early 2025, according to Mining.com. For a nation where cobalt royalties and production taxes represent a significant portion of government revenue, the price deterioration represented an existential fiscal challenge rather than a routine commodity cycle.

In February 2025, the DRC government initiated a full export suspension, cutting off cobalt shipments to arrest the price decline. This cobalt export suspension functioned as a supply shock, immediately reducing available inventory in global markets and signalling to downstream buyers that the period of cheap, freely flowing Congolese cobalt was over.

By October 2025, approximately eight months after the suspension began, the DRC cobalt export ban transitioned from a blunt export ban to a more sophisticated quota architecture. This evolution reflects an important distinction in resource policy thinking: a permanent ban destroys relationships and triggers substitution, while a managed quota system maintains market influence while preserving producer revenues and customer relationships. The quota framework has been confirmed to remain operational through at least the end of 2027.

The DRC's cobalt policy shift mirrors resource nationalism strategies seen in oil, rare earths, and nickel markets, where dominant producers have learned that supply control and price influence are more durable economic tools than volume maximisation at low prices.

How the DRC Cobalt Quota System Actually Works

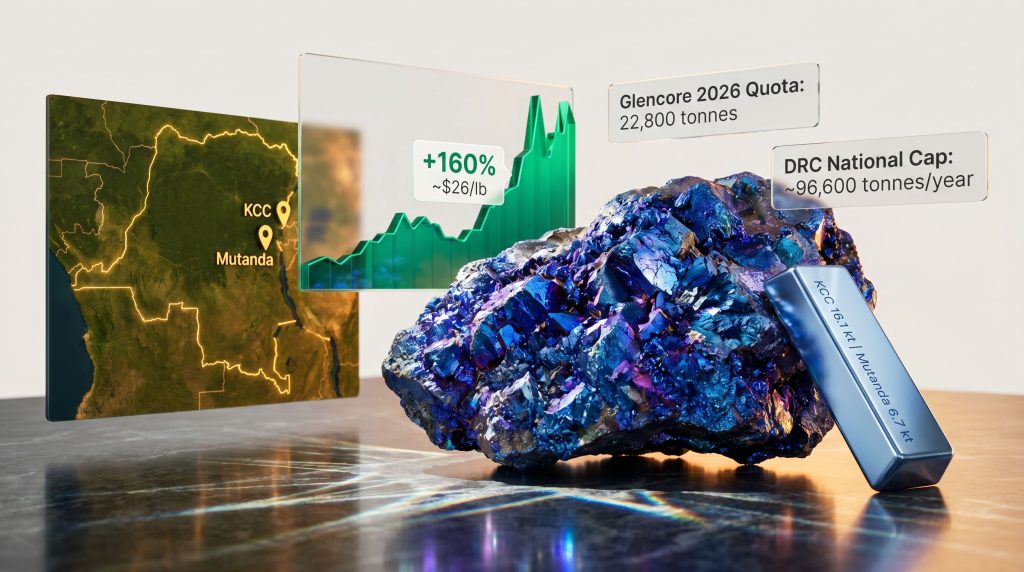

The quota architecture is built around a national annual cap of approximately 96,600 tonnes for both 2026 and 2027. This cap is not simply distributed in full to operating producers. ARECOMS, the DRC's mining supply chain regulatory authority, retains a 10% strategic reserve, meaning the allocable quota available to licensed producers totals approximately 86,940 tonnes annually. The remaining 9,660 tonnes sits under direct government discretion, available for release, reallocation, or retention depending on market conditions.

Key Compliance Requirements Under the Export Rules

Participation in the quota system is subject to several non-negotiable operational requirements:

- Prepayment of 10% royalties within a 48-hour window prior to each shipment

- Mandatory compliance certificates issued by regulatory authorities before physical export

- Joint sampling and on-site inspection protocols involving both government representatives and company personnel

- Domestic storage obligations for any cobalt produced above allocated quota thresholds

The joint inspection requirement is particularly significant from a market transparency perspective. By mandating physical co-verification of quantity and quality, the DRC government has built a dual-accountability mechanism that limits the risk of under-declaration or quota circumvention.

How Carryover Provisions Work in Practice

One of the lesser-understood features of the quota system is its carryover functionality. Producers who do not fully utilise their annual allocation within the calendar year may carry forward unused volumes into subsequent periods under defined conditions. The DRC government extended the validity of producers' 2025 export quotas through April 2026, granting additional time to implement new export processes. Unused first-quarter 2026 quotas remain valid through June 30, 2026, establishing a rolling six-month validity window that allows producers to align shipments with logistics, pricing windows, and customer requirements.

Glencore's Quota Position: Operation-by-Operation Breakdown

As one of the two largest quota holders within the DRC system alongside CMOC, Glencore's allocation reflects both its operational scale and its strategic importance to the DRC's cobalt export economy. Furthermore, understanding how these allocations are distributed across individual operations is essential for assessing Glencore's near-term revenue potential.

Glencore Total DRC Cobalt Export Quota (2026 and 2027)

| Operation | 2026 Quota (incl. 2025 carryover) | 2027 Quota |

|---|---|---|

| Kamoto Copper Company (KCC) | 16,100 tonnes | 13,300 tonnes |

| Mutanda | 6,700 tonnes | 5,500 tonnes |

| Glencore Total | 22,800 tonnes | 18,800 tonnes |

Glencore's combined 2026 allocation of 22,800 tonnes represents approximately 23.6% of the DRC's total national cap, making it one of the two dominant players within the quota system. The 2027 allocation of 18,800 tonnes represents a 17.5% reduction from 2026 levels, which may reflect either a reduction in the national cap itself or a rebalancing of quota shares among licensed producers. According to Glencore's export strategy under Congo's quota system, the company shipped its first cobalt cargo under the new regime in December 2025.

KCC: The Anchor Operation

Kamoto Copper Company is Glencore's primary cobalt-producing asset in the DRC and holds the largest single-operation allocation within Glencore's portfolio at 16,100 tonnes for 2026. KCC carries the bulk of Glencore's in-country stockpiles accumulated during the suspension period, and its inventory position is sufficient to fully utilise near-term quota windows, according to Glencore's Q1 2026 production report.

Mutanda: Cobalt as a Joint Product

Mutanda operates as a copper-cobalt mine, meaning cobalt extraction occurs alongside primary copper production rather than as the sole operational focus. Its 6,700-tonne 2026 quota reflects this secondary cobalt production profile. Glencore has confirmed that Mutanda also holds sufficient inventory to draw down near-term quota allocations as export windows become available.

An important operational nuance at both KCC and Mutanda is that Glencore has deliberately deferred final cobalt processing stages to avoid incurring processing costs on material that cannot yet be exported. Where export limits cap sales volumes, committing full processing expenditure on material destined for domestic storage creates margin dilution without corresponding revenue. This cost management strategy reflects sophisticated operational planning under quota constraints. Consequently, cobalt price impacts from this approach have been considerable across global supply chains.

Cobalt Price Performance: Anatomy of a 160% Rally

The price response to the DRC's supply intervention has been one of the most dramatic commodity recoveries in recent years, driven by a fundamental supply shock rather than demand acceleration.

Key Price Metrics

| Data Point | Figure |

|---|---|

| Export Suspension Initiated | February 2025 |

| Price Condition at Suspension | Nine-year lows |

| Cobalt Price as of Q1 2026 | |

| Price Increase Since Suspension | +160% |

| Quota System Duration | Confirmed through end-2027 |

The 160% price increase since February 2025 is a supply-side phenomenon, not a demand-driven rally. Global cobalt demand has not increased by 160% in the intervening period. What changed was the available supply entering the seaborne market. The DRC accounts for the substantial majority of global cobalt production, meaning its unilateral export controls function as a systemic variable for the entire global supply chain, not merely a regional pricing event.

Supply Shock vs. Structural Demand: What Is Driving the Rally?

It is worth separating two distinct forces operating simultaneously in the cobalt market:

- The supply shock component: The DRC's suspension and quota system directly reduced available cobalt reaching downstream processors and battery manufacturers, creating physical shortages in spot and contract markets.

- The strategic stockpiling response: Downstream buyers, aware that the quota regime is confirmed through 2027 at minimum, have moved to secure forward supply through longer-term offtake agreements and inventory building, adding procurement-side demand pressure to the supply-side constraint.

- Speculative positioning: As prices accelerated, financial participants entered cobalt-linked instruments, amplifying near-term price momentum beyond what physical supply-demand fundamentals alone would justify.

Whether the $26/lb level represents a sustainable equilibrium or an overshoot will depend critically on whether quota-constrained export volumes normalise through 2026 at a pace that satisfies downstream inventory needs without triggering further hoarding behaviour.

Glencore's Operational Response to Quota Constraints

Glencore's Q1 2026 cobalt production results reveal a deliberate strategic pivot rather than an involuntary production decline. However, understanding why output has fallen so sharply requires examining the specific quota mechanics driving Glencore's decisions.

Q1 2026 Production Metrics

| Metric | Q1 2026 | Year-on-Year Change |

|---|---|---|

| Cobalt Output (Q1 2026) | 5,800 tonnes | -39% vs. Q1 2025 |

| Full-Year 2025 Cobalt Output | 36,100 tonnes | -5% vs. 2024 |

The 39% year-on-year decline in Q1 2026 cobalt production is not a reflection of reduced mining capacity or geological constraints at KCC or Mutanda. It reflects Glencore's deliberate decision to defer final processing stages on cobalt material where quota limitations prevent near-term export. Running full processing circuits on material that must then be stored domestically adds cost without generating revenue, making partial deferral the economically rational response under quota constraints. Furthermore, this approach aligns directly with how cobalt export quotas push Glencore to prioritise copper production across its DRC operations.

The Stockpile Equation

During the full export suspension from February to October 2025, neither KCC nor Mutanda exported any cobalt. This created a substantial volume of in-country inventory accumulating as either work-in-process intermediate material or finished product. This stockpile is now the key variable in Glencore's 2026 cobalt revenue outlook.

As quota allocations are drawn down through the year, accumulated inventory will be progressively converted to revenue at prices that are dramatically higher than the nine-year lows that triggered the suspension in the first place. The timing dynamic is notable. Glencore exported most of its 2025 carryover quota during Q1 2026, with remaining 2025 volumes shipped in April 2026. This means that a meaningful portion of early 2026 cobalt revenue is being recognised at current elevated prices on material that was produced at lower cost in prior periods, providing a margin profile that is unusually favourable relative to operational expenditure.

The next major ASX story will hit our subscribers first

How Long Will the Quota System Remain in Place?

The DRC government has confirmed the quota framework through at least the end of 2027, providing a two-year policy horizon that allows producers and downstream buyers to plan accordingly. Beyond 2027, three broad scenarios are plausible:

Scenario 1: Quota Extension as Permanent Architecture. The DRC maintains managed export controls indefinitely, treating cobalt supply management as a permanent feature of its resource sovereignty strategy. This would position the DRC's cobalt policy as functionally similar to OPEC's oil production management framework, where dominant producers use supply discipline as a long-term pricing mechanism rather than a temporary intervention.

Scenario 2: Gradual Liberalisation as Demand Grows. Accelerating cobalt demand from battery supply chains, particularly if high-nickel cathode chemistries maintain market share against lithium iron phosphate alternatives, could reduce the need for supply restriction to maintain prices. Under this scenario, quotas would be progressively relaxed as global demand growth absorbs additional supply without price deterioration.

Scenario 3: System Erosion Through Non-Compliance or Geopolitical Pressure. If major producers circumvent quota obligations or if geopolitical pressure from cobalt-consuming nations leads to diplomatic negotiations that weaken the DRC's regulatory enforcement capacity, the system could unravel, returning the market to pre-2025 oversupply dynamics and price vulnerability.

The most underappreciated risk in the cobalt market is not a demand collapse but a compliance failure within the DRC quota system itself. If enforcement weakens and unreported exports increase, the supply shock premium embedded in current prices could reverse rapidly.

Global Implications: Battery Supply Chains and Downstream Strategy

The DRC's dominant position in global cobalt mine supply means its export policy functions as a systemic variable for battery manufacturers, electric vehicle producers, and energy storage developers worldwide. In addition, the broader battery metals landscape has been reshaped considerably as a result, with investors and procurement teams reassessing exposure to DRC supply risk across the battery metals landscape.

Comparing DRC Cobalt Controls to Other Resource Export Regimes

| Country and Commodity | Control Mechanism | Duration | Market Impact |

|---|---|---|---|

| DRC / Cobalt | Export quotas and royalty prepayment | 2025 to 2027+ | +160% price rally |

| China / Rare Earths | Export licensing and production caps | Ongoing | Persistent supply risk |

| China / Tungsten | Export restrictions | 2025 onwards | +200% price surge YTD 2026 |

| Indonesia / Nickel | Export ban on raw ore | Since 2020 | Processing shifted onshore |

The pattern is consistent across each case: dominant producers of critical materials are increasingly using export control mechanisms as a tool to extract higher value from their resource endowments, shift processing activities onshore, and reduce dependency on market pricing that reflects buyer leverage rather than producer leverage.

How Battery Manufacturers Are Responding

Downstream buyers have not been passive in the face of DRC supply constraint. Three primary strategic responses have emerged:

- Accelerated qualification and adoption of cobalt-free cathode chemistries, particularly lithium iron phosphate formulations, to reduce structural exposure to DRC supply risk

- Negotiation of longer-term offtake agreements tied to quota-backed supply, providing volume certainty at the cost of price flexibility

- Geographic diversification of cobalt sourcing, including increased focus on Zambian production, Australian laterite deposits, and recycled cobalt streams from battery recovery operations

The tension between these responses creates a long-term structural uncertainty for cobalt demand. If cobalt-free cathodes succeed in capturing a larger share of the battery market, demand growth may not be sufficient to absorb DRC supply even at quota-constrained volumes, potentially undermining the pricing rationale for the quota system itself.

Key Data Summary: Glencore DRC Cobalt Quota at a Glance

| Data Point | Figure |

|---|---|

| DRC National Cobalt Export Cap (2026 and 2027) | ~96,600 tonnes per year |

| ARECOMS Strategic Reserve | ~9,660 tonnes (10% of cap) |

| Glencore Total 2026 Quota (incl. carryover) | 22,800 tonnes |

| KCC 2026 Quota | 16,100 tonnes |

| Mutanda 2026 Quota | 6,700 tonnes |

| Glencore 2027 Quota | 18,800 tonnes |

| Cobalt Price Increase Since Feb 2025 | +160% |

| Cobalt Price Q1 2026 | |

| Glencore Q1 2026 Cobalt Output | 5,800 tonnes (-39% YoY) |

| Full-Year 2025 Cobalt Output | 36,100 tonnes (-5% vs. 2024) |

| Quota System Confirmed Duration | Through at least end-2027 |

What Investors and Supply Chain Participants Should Watch

For those monitoring the Glencore DRC cobalt export quotas and broader cobalt market dynamics, the critical variables going forward include:

- Quarterly quota utilisation rates from Glencore, CMOC, and other major DRC producers, which will signal whether the physical supply gap is closing faster or slower than expected

- Any ARECOMS announcements regarding strategic reserve mobilisation, quota reallocation, or system extension beyond 2027

- Battery cathode chemistry adoption trends, particularly the rate at which LFP captures market share from higher-cobalt nickel manganese cobalt formulations in key EV markets

- Cobalt price trajectory through H2 2026, as deferred 2025 inventory enters the market and the first full year of quota-governed exports is completed

- Compliance and enforcement data, including any evidence of quota circumvention that could undermine the supply restriction premium currently embedded in cobalt prices

This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity price forecasts and scenario analysis involve inherent uncertainty. Past price performance is not indicative of future results. Readers should conduct independent research before making investment decisions.

Want to Capitalise on the Next Major Commodity Supply Shock Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity developments into actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market shift.