May 21, 2026

Understanding Global Commodity Market Structural Transformation

The global commodity landscape has undergone significant structural realignment over the past two decades, driven by technological advancement, monetary policy shifts, and evolving geopolitical dynamics. Resource-rich nations have benefited from these transformative forces, with export earnings fluctuating based on complex interactions between supply constraints, demand evolution, and macroeconomic conditions. This gold bonanza in australia reflects broader patterns requiring analysis of both cyclical price movements and fundamental structural changes affecting commodity consumption patterns across major economies.

Central bank monetary policies have particularly influenced precious metals markets, as quantitative easing programs and low interest rate environments have driven institutional capital toward tangible assets. This portfolio rebalancing has created sustained demand for gold prices record highs, silver, and other store-of-value commodities, while simultaneously supporting base metals through infrastructure spending programs. The convergence of these factors has created unique opportunities for diversified resource exporters positioned across multiple commodity categories.

When big ASX news breaks, our subscribers know first

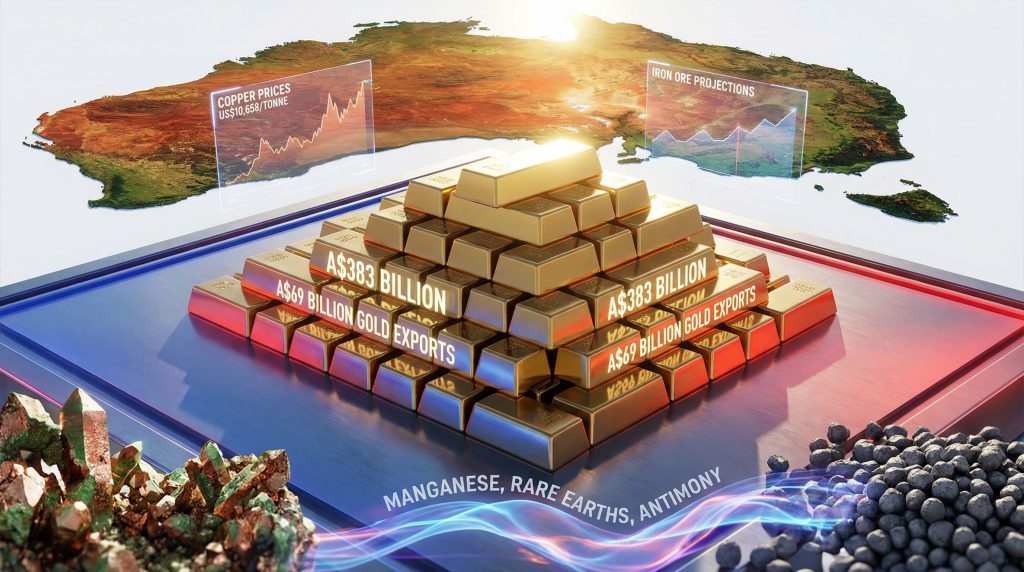

How Australia Achieves Record A$383 Billion Export Performance

Australia's resource sector has demonstrated remarkable resilience, with export earnings climbing to A$383 billion for the current financial year, representing a substantial 4% increase from previous forecasts. This upward revision of A$14 billion reflects the convergence of multiple favorable market dynamics, including sustained precious metals strength, resilient base metals pricing, and currency conditions that have enhanced export competitiveness.

The Australian Department of Industry attributed this performance to several key macroeconomic catalysts. According to their December 2025 report, the revision stems from easier monetary and fiscal policy across major economies, investment driven by rising artificial intelligence usage, and energy transition requirements maintaining robust commodity demand. These factors have created a supportive environment for Australian resource exports across multiple commodity categories.

Primary Revenue Drivers Behind Export Growth

The export surge reflects several interconnected market forces:

• Monetary policy accommodation across G7 economies creating favorable conditions for commodity demand

• Infrastructure investment acceleration in emerging markets maintaining steel and base metals consumption

• Energy transition requirements driving critical minerals energy transition and copper demand for renewable infrastructure

• Geopolitical uncertainty redirecting investment flows toward safe-haven assets and stable supply sources

• Currency stability preventing typical appreciation patterns that often accompany commodity booms

The combination of these factors has created an environment where Australian resource exports benefit from both volume growth and enhanced pricing power, particularly in precious metals markets where institutional demand has intensified significantly.

Why Gold Emerges as Australia's Second-Largest Export Earner

Gold has experienced unprecedented momentum in Australia's export portfolio, with values projected to reach A$69 billion in 2025-26, marking a substantial 15% increase from the September forecast of A$60 billion. This trajectory positions gold to surpass liquefied natural gas as Australia's second-largest export commodity, fundamentally reshaping the nation's resource export hierarchy.

The precious metal's ascension reflects both volume expansion and exceptional price appreciation. Furthermore, gold prices reached record highs exceeding US$4,350 per troy ounce in October 2024, driven by institutional portfolio diversification and safe-haven demand amid global uncertainty. The Australian Department of Industry projects pricing to remain robust around US$4,000 through 2026, providing sustained support for export values.

Market Positioning and Price Trajectory Analysis

Gold's market performance demonstrates several critical dynamics:

| Metric | 2025-26 Forecast | 2026-27 Projection | Growth Rate |

|---|---|---|---|

| Export Value | A$69 billion | A$74 billion | 7.2% |

| Price Range | ~US$4,000/oz | Declining trend | Post-2026 |

| Market Position | #2 Export Earner | Sustained dominance | Structural shift |

The Department of Industry noted that concerns about geopolitical instability have fueled demand for the safe-haven metal, creating sustained institutional interest beyond traditional jewellery and industrial applications. In addition, this demand pattern reflects broader portfolio rebalancing strategies among pension funds, sovereign wealth funds, and central banks seeking tangible asset exposure.

Institutional Demand Patterns and Investment Flows

Gold's export value growth represents more than cyclical price appreciation. The metal has attracted sustained institutional capital as central banks globally have increased reserve allocations and investment funds have enhanced commodity exposure. However, this institutional demand provides underlying support for pricing that extends beyond traditional retail or industrial consumption patterns.

The magnitude of gold's export value increase highlights Australia's competitive position in global markets, benefiting from high-grade deposits, established mining industry evolution infrastructure, and political stability that appeals to international buyers seeking secure supply sources.

How Iron Ore Maintains Market Leadership Despite Pricing Pressures

Iron ore continues to dominate Australia's resource export portfolio, maintaining approximately 25% of total resource earnings across both 2025-26 and 2026-27 forecast periods. Despite facing headwinds from abundant global supply and moderating steel demand, iron ore's structural importance to Australia's export base remains intact, with pricing forecasts showing resilience relative to earlier concerns about oversupply.

The Australian Department of Industry projects iron ore pricing at US$87 per tonne for the current financial year, declining to US$83 per tonne for 2026-27. Notably, the December forecast represented a US$1 per tonne upward revision from September projections, suggesting marginally improved confidence in iron ore demand insights despite acknowledged supply abundance.

Supply-Demand Equilibrium and Pricing Dynamics

Iron ore markets face complex balancing acts between expanding global production capacity and evolving steel consumption patterns:

• Chinese demand moderation as infrastructure investment cycles mature and real estate sector adjustments continue

• Emerging market infrastructure development providing offsetting demand from India, Southeast Asia, and Africa

• Energy transition steel requirements for wind turbines, transmission infrastructure, and renewable energy projects

• Supply expansion from Australia, Brazil, and other major producers increasing available capacity

The Department of Industry assessment that prices are expected to decline slightly because of abundant supply and moderating steel demand reflects industry consensus around global steel production forecasts. However, the maintenance of iron ore's 25% export share demonstrates the commodity's structural resilience and Australia's competitive advantages in quality and logistics.

Quality Advantages and Market Positioning

Australian iron ore benefits from several competitive factors that support pricing premium relative to alternative suppliers. High-grade deposits, established port infrastructure, and proximity to Asian steel markets provide structural advantages that help maintain market share even during periods of pricing pressure.

Consequently, the stability of iron ore's export share across forecast periods suggests that demand fundamentals remain supportive despite near-term pricing moderation, reflecting the commodity's essential role in global steel production and infrastructure development.

What Copper's 12% Price Revision Signals for Technology Infrastructure

Copper has emerged as a standout performer in Australia's commodity portfolio, with price forecasts revised upward by 12% for 2025-26 to US$10,658 per tonne, compared to the September projection of US$9,694. This substantial revision of US$964 per tonne reflects accelerating demand from data center construction and artificial intelligence infrastructure deployment.

The Department of Industry specifically identified data centers as a key demand catalyst, highlighting how technological advancement is creating new consumption patterns for traditional industrial metals. For instance, the 2026-27 forecast also received a significant 10% upward revision to US$10,896 per tonne, indicating sustained confidence in technology-driven demand growth.

Technology Infrastructure Driving Consumption Patterns

The copper prices record highs revision reflects several transformative demand drivers:

• Hyperscale data center expansion requiring extensive electrical infrastructure and cooling systems

• Artificial intelligence processing requirements creating unprecedented power density and connectivity demands

• Cloud computing infrastructure necessitating massive facility buildouts by technology companies

• Edge computing deployment distributing processing capability closer to end users

The magnitude of copper's upward revision suggests that technology infrastructure investment is accelerating beyond previous forecasts, creating structural demand that extends beyond traditional construction and manufacturing applications.

Investment Implications and Market Psychology

Copper's price trajectory indicates that investors and industry analysts are increasingly recognising the metal's role as an enabler of technological transformation. The consecutive annual upward revisions (10-12%) demonstrate growing confidence that structural demand from technology infrastructure will continue strengthening rather than moderating.

This demand pattern differs from cyclical copper consumption tied to construction activity or manufacturing cycles. Furthermore, technology infrastructure copper demand tends to be more sustained and less sensitive to economic downturns, providing underlying support for pricing that may persist beyond typical commodity cycles.

How Critical Minerals Transform Australia's Export Portfolio

Critical minerals represent Australia's fastest-growing export category, with values projected to increase from approximately A$11 billion in 2024-25 to A$14 billion by 2026-27. This 27% growth trajectory over two years reflects strategic positioning in global supply chains increasingly focused on technology sovereignty and energy transition requirements.

The Department of Industry identified several specific drivers behind critical minerals growth, including a recovery in manganese exports, rising exports of rare earths, and increased antimony demand. This diversification demonstrates Australia's geological advantages across multiple mineral categories essential for modern technology applications.

Mineral-Specific Growth Drivers and Market Dynamics

Critical minerals growth reflects distinct demand patterns for individual commodities:

• Manganese recovery as industrial demand normalises following pandemic-related disruptions in stainless steel and battery markets

• Rare earths expansion driven by permanent magnet applications in renewable energy turbines and electric vehicle motors

• Antimony emergence following strategic mineral classifications by major economies seeking supply chain diversification

• Supply chain diversification as nations reduce dependence on geopolitically concentrated sources

The 27% growth rate across the critical minerals portfolio indicates that Australia's geological diversity provides competitive advantages in multiple strategic mineral categories simultaneously.

Geopolitical Supply Chain Considerations

Critical minerals demand increasingly reflects geopolitical considerations beyond traditional market fundamentals. Governments and corporations are actively seeking to diversify supply sources away from geographically concentrated production, particularly for minerals essential to technology applications and energy transition infrastructure.

Australia's political stability, established mining expertise, and geological diversity position the nation favourably in this supply chain diversification trend. In addition, the critical minerals export growth reflects both market demand and strategic policy considerations by international buyers seeking secure, reliable supply sources.

The next major ASX story will hit our subscribers first

What Currency Dynamics Reveal About Export Competitiveness

The Australian dollar's performance relative to the US dollar has provided unexpected support for resource export earnings, with currency stability preventing the typical appreciation that often accompanies commodity booms. This dynamic has enhanced the competitive positioning of Australian exports in international markets while amplifying the domestic value of commodity price gains.

The Department of Industry noted that the failure of Australia's currency to rise against the US dollar as expected contributed significantly to the upward revision in export earnings. However, this currency performance reflects several macroeconomic factors, including relative interest rate differentials, capital flow patterns, and investor sentiment toward commodity-dependent economies.

Exchange Rate Impact on Export Valuations

Currency dynamics affect resource export competitiveness through multiple channels:

• Pricing competitiveness relative to alternative suppliers with stronger currencies

• Revenue optimisation as commodity prices denominated in USD translate to higher AUD values

• Investment attractiveness for international capital seeking resource sector exposure

• Production cost advantages as domestic operational expenses remain stable while export revenues increase

The maintenance of AUD weakness despite strong commodity performance suggests that global capital flows and monetary policy differentials are overriding traditional commodity currency appreciation patterns.

Implications for Resource Sector Investment

Currency stability during commodity price strength creates favourable conditions for resource sector investment. Mining companies benefit from enhanced margins as export revenues increase while domestic operational costs remain relatively stable, improving project economics and capital allocation decisions.

This dynamic supports exploration activity, capacity expansion projects, and technological upgrades across Australia's resource sector, potentially extending the current favourable market conditions through improved productivity and resource development.

How Geopolitical Factors Reshape Global Commodity Demand

Geopolitical uncertainty has fundamentally altered commodity demand structures, extending beyond traditional economic fundamentals to encompass strategic considerations around supply chain security and resource sovereignty. This shift has particularly benefited safe-haven assets and strategic minerals essential for technological infrastructure and national security applications.

The Department of Industry explicitly identified geopolitical instability as a driver of safe-haven metal demand, highlighting how political and economic uncertainty translates into tangible asset allocation strategies. This gold bonanza in australia demand pattern creates sustained support for precious metals that extends beyond traditional monetary and inflation hedge applications.

Strategic Resource Allocation and National Security Considerations

Geopolitical factors influence commodity demand through several mechanisms:

• Strategic stockpiling by governments seeking to reduce supply chain vulnerabilities

• Diversification initiatives aimed at reducing dependence on geopolitically concentrated sources

• Technology sovereignty efforts requiring secure access to critical mineral inputs

• Financial system diversification through increased central bank reserve allocations to tangible assets

These factors create demand patterns that differ substantially from traditional industrial or investment commodity consumption, providing underlying support for pricing that may persist regardless of cyclical economic conditions.

Investment Portfolio Implications

Geopolitical commodity demand affects investment strategies across institutional and retail portfolios. Asset managers are increasingly incorporating supply chain security considerations into commodity allocation decisions, recognising that geopolitical factors can override traditional economic analysis in determining long-term demand patterns.

This shift toward strategic commodity allocation supports Australia's resource sector positioning, as the nation's political stability and established mining expertise align with international buyers' security-focused sourcing strategies.

Where Market Structure Evolution Creates Investment Opportunities

Australia's export performance provides insights into broader structural changes within global commodity markets, as technological advancement, energy transition requirements, and geopolitical realignment create new demand hierarchies favouring diversified resource producers. These structural shifts extend beyond cyclical price movements to reflect fundamental changes in how commodities are valued and consumed.

The convergence of multiple growth drivers across Australia's resource portfolio suggests that the nation's geological advantages, political stability, and mining expertise are increasingly valued by international markets. For instance, this bonanza gold discovery positioning creates potential for sustained export growth beyond current forecast periods as structural demand factors strengthen.

Structural Demand Transformation

Market structure evolution reflects several transformative trends:

• Technology infrastructure expansion creating new consumption categories for traditional metals

• Energy transition acceleration driving demand for specialised minerals and materials

• Supply chain localisation efforts favouring politically stable, high-quality producers

• Financial system evolution incorporating tangible assets into portfolio strategies

These trends suggest that commodity demand patterns are becoming more complex and diversified, potentially supporting sustained pricing for producers positioned across multiple categories.

Investment Strategy Considerations

The structural transformation of commodity markets creates opportunities for investors seeking exposure to resource sector themes extending beyond traditional cyclical patterns. Australia's diversified resource base provides exposure to multiple structural demand drivers simultaneously, potentially reducing single-commodity risk while capturing growth across several categories.

Resource sector investment strategies may benefit from recognising these structural changes rather than focusing solely on cyclical price movements, as technological and geopolitical factors create demand patterns with different characteristics than traditional commodity cycles.

Future Outlook for Australia's Resource Sector Evolution

Looking beyond immediate price cycles, Australia's resource sector appears positioned for sustained growth driven by structural demand shifts rather than cyclical factors. The combination of geological advantages, political stability, technological capability, and established infrastructure creates compelling fundamentals for continued export expansion across multiple commodity categories.

The Department of Industry's upward revisions across gold, copper, and critical minerals suggest that structural demand factors are strengthening rather than moderating, potentially supporting sustained export performance through 2026-27 and beyond. This outlook reflects both market fundamentals and strategic considerations that favour Australia's competitive positioning in the ongoing gold bonanza in australia.

Long-Term Structural Drivers

Future resource sector performance may benefit from several persistent trends:

• Energy transition acceleration requiring massive mineral inputs for renewable infrastructure and grid modernisation

• Technology advancement creating new consumption patterns for both traditional and specialised materials

• Urbanisation and infrastructure development in emerging markets maintaining base metals demand

• Climate policy implementation affecting global supply chains and production patterns

These factors suggest that Australia's resource sector may experience sustained demand across multiple commodity categories, supporting continued investment and development activity.

Investment and Development Implications

The robust export outlook is attracting renewed investment interest across Australia's resource sector, with particular focus on operations capable of scaling production to meet projected demand growth. This investment cycle may support exploration acceleration, technology integration, and infrastructure development across the industry.

Future resource sector evolution may increasingly focus on sustainability, technology integration, and supply chain efficiency as competitive differentiators, building on Australia's existing advantages in quality, scale, and operational expertise to maintain market leadership across diverse commodity markets throughout the current gold bonanza in australia.

Ready to Profit From Australia's A$383 Billion Resource Export Boom?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications when significant ASX mineral discoveries are announced, helping investors capitalise on market-moving opportunities across gold, copper, and critical minerals before the broader market reacts. Explore how major mineral discoveries can generate substantial returns by examining historical examples, then begin your 30-day free trial today to position yourself ahead of Australia's continuing resource sector expansion.