August 1, 2026

The Global Energy Crisis Reshaping Industrial Competitiveness

The intersection of energy policy and industrial survival has become one of the most critical challenges facing resource-dependent economies worldwide. As global supply chains adapt to volatile energy costs and geopolitical pressures, traditional mining jurisdictions find themselves confronting unprecedented competitive disadvantages. The transformation of once-dominant industrial sectors reveals how quickly comparative advantages can erode when underlying cost structures deteriorate beyond sustainable thresholds.

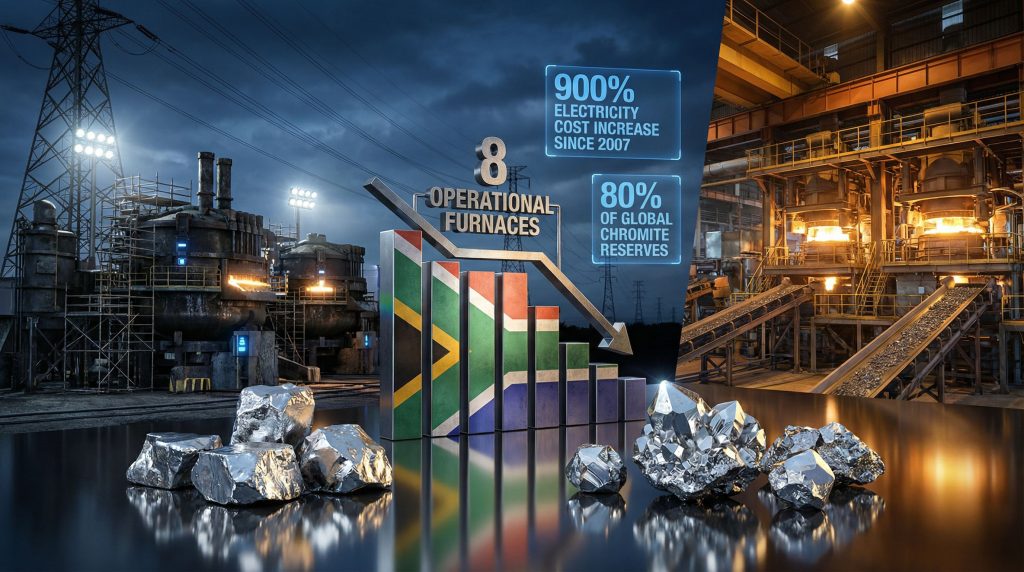

The South Africa ferrochrome industry crisis represents a particularly striking example of this phenomenon, where a nation controlling approximately 80% of global chromite reserves has witnessed systematic industrial collapse due to energy cost inflation and policy misalignment. Furthermore, this situation highlights broader challenges affecting energy transition strategies across resource-dependent economies.

When big ASX news breaks, our subscribers know first

Understanding the Scale of Industrial Shutdown

The magnitude of South Africa's ferrochrome sector contraction defies typical cyclical patterns observed in commodity markets. From an industrial base comprising 67 operational furnaces across multiple production facilities, only 8 units remained active by December 2025. This represents an 88% reduction in operational capacity within a concentrated timeframe.

The parallel shutdown of smelting infrastructure reveals even more dramatic compression. Of 48 ferrochrome smelters historically operating across the country, merely 4 facilities continued production, indicating a 92% operational contraction. These figures represent industrial decline rates rarely witnessed outside of wartime scenarios or systematic economic collapse.

Key Operational Metrics:

- Total ferrochrome production capacity utilisation: 12%

- Remaining active smelters: 8.3% of total facilities

- Production facilities in care-and-maintenance status: Majority of installations

- Geographic concentration of remaining operations: Limited to 4 locations

The terminology "care-and-maintenance" status indicates facilities are preserved in non-operational but theoretically recoverable condition, involving minimal staffing for facility preservation, equipment protection, and regulatory compliance despite production cessation.

What Makes This Crisis Unprecedented in Mining History?

The simultaneity of multiple industrial pressures creates conditions rarely observed in modern mining economics. Unlike typical commodity price cycles that affect profitability margins, the South African situation demonstrates how utility cost inflation can systematically eliminate entire industrial sectors regardless of underlying resource endowments.

The 27% production contraction experienced in the first half of 2025 occurred despite global demand remaining relatively stable, indicating supply-side rather than demand-side pressures driving industrial shutdown. This pattern contrasts sharply with historical mining downturns typically triggered by commodity price collapses or global recession. In addition, this crisis reflects broader challenges affecting mining industry innovation worldwide.

Policy-Market Collision Dynamics

South Africa's mineral beneficiation policy mandates domestic value-added processing rather than raw ore exports. However, this strategic objective has encountered insurmountable implementation barriers due to electricity cost structures that render domestic processing economically unviable.

The policy framework assumes industrial competitiveness can be maintained through regulatory requirements, but market dynamics demonstrate that competitive disadvantages ultimately override policy intentions. This creates a paradoxical situation where resource ownership provides no guarantee of processing capability or market access.

The Electricity Cost Explosion Framework

The transformation of electricity from a competitive advantage to an existential threat illustrates how utility pricing can fundamentally alter industrial economics. Since 2007, South African electricity tariffs have increased by approximately 900%, converting what was historically a 15-20% production cost component into 40-60% of total operating expenses.

Electricity Cost Evolution Analysis:

| Period | Electricity Share | Labour Share | Raw Materials Share | Cost Impact |

|---|---|---|---|---|

| 2007 | 15-20% | 25-30% | 40-45% | Competitive advantage |

| 2015 | 25-35% | 20-25% | 35-40% | Margin pressure |

| 2025 | 40-60% | 15-20% | 25-30% | Operational crisis |

This cost structure transformation creates mathematical impossibility for sustained operations under current tariff regimes. The 900% price increase over 18 years represents compound annual growth rates exceeding most commodity price appreciations, making electricity cost the dominant variable in production economics.

Arc Furnace Technology Constraints

Ferrochrome smelting utilises electric arc furnace technology requiring continuous, uninterrupted power supply. Unlike some industrial processes that can accommodate intermittent energy delivery, arc furnace operations cannot function under load-shedding conditions characteristic of South Africa's power grid management.

The technical impossibility of intermittent operation creates binary outcomes: facilities either operate continuously or shut down entirely. This technological constraint eliminates partial production strategies available to other industries during power supply disruptions.

Current Tariff Relief Measures and Industry Response

Government intervention through emergency tariff adjustments reveals the scale of subsidy required to maintain industrial viability. The interim 87c/kWh electricity rate represents a 35% discount from standard negotiated pricing agreements of 135c/kWh.

Despite substantial fiscal intervention, industry analysis indicates current relief remains insufficient for sustained operations. Producer requirements for 62c/kWh pricing establish a 25c/kWh gap between government relief measures and competitive necessity thresholds. For instance, this highlights the broader decarbonisation benefits that require careful cost-benefit analysis.

Tariff Structure Comparison:

- Standard negotiated rate: 135c/kWh

- Interim relief rate: 87c/kWh (35% discount)

- Industry viability threshold: 62c/kWh

- Required additional relief: 28.7% below interim rate

The persistence of uneconomic operations despite substantial government intervention demonstrates how competitive disadvantages can exceed politically sustainable subsidy levels.

How China Has Restructured Global Processing Networks

China's strategic approach to ferrochrome processing demonstrates how nations can capture value-added manufacturing despite lacking primary resource endowments. Chinese smelters now process approximately 70% of South African chromite ore exports, utilising lower domestic electricity costs and coal-based power generation to undercut South African producers.

This supply chain restructuring creates a paradoxical competitive dynamic where resource owners lose market access to processors importing their raw materials. Chinese ferrochrome production benefits from subsidised energy policies and geographic proximity to Asian stainless steel markets, enabling systematic displacement of South African smelters. However, recent tariff impact analysis suggests these competitive dynamics may shift under changing trade policies.

Market Share Transformation Metrics

The global ferrochrome market experienced a 10% price decline in Q2 2025, coinciding with South Africa's 27% production contraction. This inverse relationship suggests Chinese supply increases more than compensated for South African production losses, indicating substantial excess capacity development.

Competitive Displacement Analysis:

- Chinese processing of South African ore: 70% of chromite exports

- Global price impact: 10% decline (Q2 2025)

- South African production response: 27% contraction (H1 2025)

- Market share migration: Permanent structural change likely

The migration of processing activities from resource owners to distant processors represents a fundamental reversal of traditional mining economics, where transportation costs typically favour proximate processing.

The next major ASX story will hit our subscribers first

Strategic Industry Preservation Policy Options

Government consideration of multiple intervention mechanisms reflects the complexity of addressing systematic competitive disadvantage. Beyond electricity tariff relief, policy tools under evaluation include export restrictions, carbon tax suspension, and renewable energy procurement facilitation.

Policy Intervention Assessment:

| Intervention Type | Implementation Status | Industry Response | Sustainability Risk |

|---|---|---|---|

| Electricity subsidies | Interim approval | Insufficient relief | High fiscal burden |

| Chromite export restrictions | Under consideration | Mixed industry support | WTO compliance risk |

| Carbon tax suspension | Proposed | Strong industry support | Environmental policy pressure |

| Renewable energy wheeling | Regulatory development | Cautious industry optimism | Technology transition complexity |

Export restriction considerations reveal government willingness to prioritise domestic processing over export revenue, though such measures risk international trade retaliation and may conflict with World Trade Organisation obligations.

Economic Multiplier Effects and Regional Impact

The ferrochrome crisis extends beyond direct smelter employment, affecting chromite mining operations, transportation networks, and supporting service industries. Regional economic impact concentrates in traditional ferrochrome production areas, where facility closures eliminate anchor employers. Nevertheless, understanding the broader global mining landscape provides context for these regional challenges.

Beneficiation Policy Failure Implications

South Africa's mineral beneficiation strategy, designed to capture value-added processing revenues rather than exporting raw materials, faces systematic undermining as producers revert to ore exports to maintain cash flow. This policy reversal represents fundamental retreat from industrial development objectives established over multiple political administrations.

The failure of beneficiation policy implementation demonstrates how underlying competitive factors can override regulatory mandates, particularly when alternative markets remain available for raw material exports.

Global Supply Chain Security Implications

International stainless steel producers increasingly question South African ferrochrome supply reliability, driving diversification strategies that may permanently reduce market share even if operations resume. Supply chain disruption concerns extend beyond current production shortfalls to encompass future reliability expectations.

The concentration of global chromite reserves in a single jurisdiction facing systematic industrial decline raises strategic mineral security concerns for stainless steel producers worldwide. This vulnerability may accelerate development of alternative supply sources or substitute technologies.

Investment Flow Redirection Patterns

International ferrochrome investment may increasingly focus on jurisdictions with stable energy costs and reliable supply infrastructure, potentially excluding South Africa from future capacity expansion cycles. This capital allocation shift could entrench competitive disadvantages beyond current operational challenges.

Advanced Technology Solutions for Competitiveness Recovery

Emerging smelting technologies offer potential pathways to restore competitive viability despite high electricity costs. SmeltDirect and similar advanced processes promise up to 70% energy consumption reductions compared to conventional arc furnace technology.

However, implementation requires substantial capital investment during crisis periods when financing access remains constrained. The paradox of requiring investment to restore competitiveness while lacking cash flow for investment creates implementation barriers.

Renewable Energy Integration Pathways

Direct renewable energy procurement through wheeling arrangements could bypass Eskom's pricing structure, though regulatory frameworks remain underdeveloped. Wind and solar power costs have declined substantially, potentially offering long-term solutions to electricity cost disadvantages.

The technical challenges of matching intermittent renewable generation with continuous arc furnace requirements necessitate energy storage or backup power arrangements, adding complexity and cost to renewable integration strategies.

Emergency Bailout Framework Considerations

Industry calls for comprehensive financial support reflect the scale of intervention required to maintain operational viability during transition periods. Bailout mechanisms under consideration include direct subsidies, loan guarantees, and equity participation through state-owned development institutions.

The fiscal implications of sectoral bailouts raise questions about sustainable intervention capacity and priority allocation among competing industrial requirements. Government resources face competing demands from multiple struggling sectors.

Regulatory Reform Acceleration Requirements

Fast-tracking renewable energy wheeling regulations and carbon tax suspension could provide immediate relief while longer-term solutions develop. However, regulatory acceleration requires coordination across multiple government departments with potentially conflicting objectives.

Environmental policy alignment with industrial competitiveness creates tension between climate objectives and employment preservation, particularly in coal-dependent regions where ferrochrome facilities operate.

Lessons for Industrial Policy Design and Implementation

The South Africa ferrochrome industry crisis demonstrates how utility cost inflation, policy misalignment, and international competition can rapidly dismantle established industrial sectors. The experience highlights critical requirements for integrated policy frameworks addressing energy, environmental, and industrial objectives simultaneously.

The situation serves as a cautionary example for other resource-dependent economies, illustrating how domestic policy failures can compromise global supply chains for strategic materials. According to South Africa's ferrochrome industry outlook, the outcome will significantly influence international stainless steel markets while establishing precedents for managing tensions between environmental objectives and industrial competitiveness. Furthermore, the ongoing electricity crisis impact continues to shape industry discussions about sustainable operations.

Key Policy Integration Requirements:

- Coordinated industrial and energy policy development

- Recognition of technology constraints in renewable transitions

- Consideration of international competitiveness in domestic pricing

- Balancing beneficiation objectives with operational viability

The resolution of this crisis will determine whether resource endowments can sustain domestic processing industries or whether global supply chains will permanently restructure around processing locations with competitive advantages rather than resource proximity.

Disclaimer: This analysis involves forecasts and speculation about future market developments and policy outcomes. Industrial policy decisions carry significant economic and social implications that may differ from projections discussed. Readers should consider multiple perspectives and seek additional sources when making investment or policy decisions related to the South African ferrochrome sector.

Looking to Capitalise on Industrial Disruptions and Supply Chain Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial market returns, and begin your 14-day free trial today to position yourself ahead of industrial transformation trends.