July 18, 2026

Understanding Global Energy Market Shifts Through Strategic Pricing Adjustments

The modern crude oil market operates as an intricate network of supply chains, pricing mechanisms, and geopolitical considerations that extend far beyond traditional supply-demand dynamics. Understanding how major producers adjust their pricing strategies reveals deeper structural forces reshaping global energy flows. These pricing decisions reflect broader market psychology, competitive positioning, and long-term strategic planning that influences everything from refinery margins to national energy security policies.

Current market conditions demonstrate how established petroleum exporters must navigate an increasingly complex landscape of alternative energy sources, geopolitical tensions, and evolving consumer demand patterns. The mechanisms behind official selling price adjustments provide insight into how energy markets adapt to changing global conditions while maintaining operational stability across international supply chains.

When big ASX news breaks, our subscribers know first

Market Fundamentals Behind February 2026 Pricing Adjustments

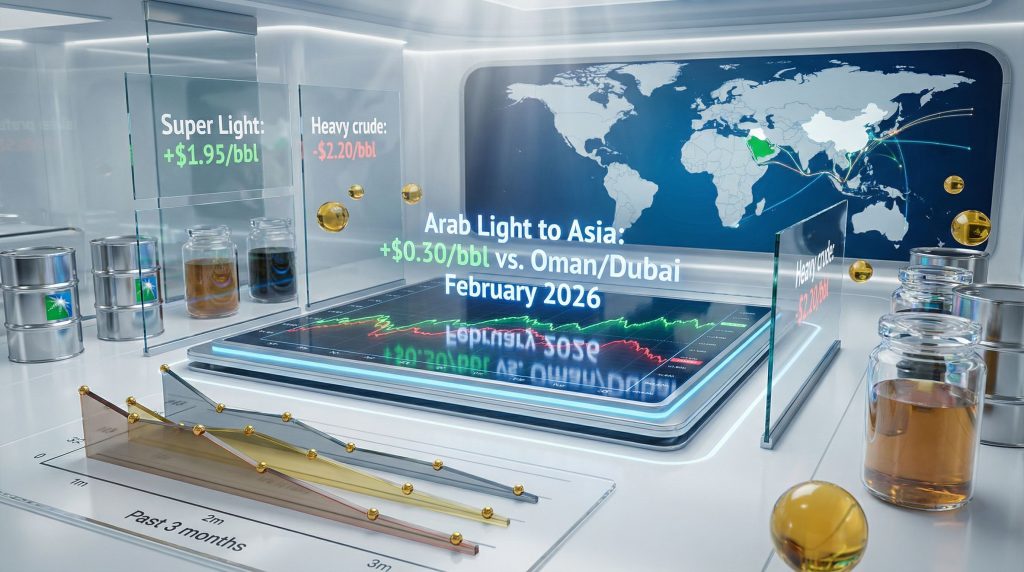

Saudi Arabia cuts oil prices to Asia for the third consecutive month, establishing Arab Light crude at $0.30 per barrel above the Oman/Dubai benchmark in February 2026. This represents a $0.30 reduction from January's $0.60 premium, continuing a systematic downward pricing trend that began in December 2025.

The comprehensive nature of these adjustments affects multiple crude grades simultaneously. Super Light crude declined $0.20 to $1.95 per barrel premium, while Extra Light decreased $0.30 to $0.80 per barrel. Medium grade crude shifted $0.30 lower to -$0.85 per barrel discount, and Heavy crude dropped $0.30 to -$2.20 per barrel discount relative to the regional benchmark.

These coordinated reductions across all quality specifications suggest market-wide pressures rather than grade-specific competitive challenges. The consistency of the $0.30 adjustment for most crude types indicates a strategic recalibration designed to maintain market share while adapting to current demand conditions across Asian refining centers.

Technical Pricing Structure Analysis

The official selling price system employs distinct benchmark references depending on destination markets, creating a sophisticated framework for regional optimization. Asian deliveries use the Oman/Dubai average as the reference point, while North American shipments reference ASCI (American Sour Crude Index), and European markets utilise ICE Brent crude futures.

This multi-benchmark approach allows producers to optimise competitiveness across different regional refining configurations and local market dynamics. The systematic nature of recent adjustments suggests coordination designed to maintain relative positioning across all major consuming regions rather than favouring specific markets.

Quality differentials remain consistent with historical patterns, where lighter, sweeter crudes command premiums while heavier, more sulfurous grades trade at discounts. However, the magnitude of these differentials adjusts based on refining capacity, seasonal demand patterns, and alternative crude availability in each region.

Regional Market Dynamics and Competitive Positioning

North American Market Adaptations

Pricing adjustments to North American refineries show strategic recalibration amid domestic production dynamics. Arab Light crude pricing decreased $0.30 to a $2.20 premium versus ASCI, maintaining substantial premiums despite competitive pressure from regional suppliers.

Extra Light crude declined $0.40 to $4.05 per barrel premium, while Medium grade fell $0.40 to $1.70 per barrel and Heavy crude decreased $0.40 to $0.95 per barrel premium. The consistency of these reductions suggests systematic competitive response rather than market-specific tactical adjustments.

North American refining capacity continues expanding, with complex refineries capable of processing various crude specifications. The maintained premium structure indicates that Saudi crude grades retain value propositions for refiners despite abundant domestic unconventional production and pipeline-delivered Canadian bitumen.

The $0.30 to $0.40 reduction range across grades reflects efforts to maintain competitiveness while preserving margin structures. This approach suggests confidence in long-term market positioning despite near-term pricing pressure from regional alternatives.

European Market Dynamics

European pricing demonstrates more aggressive competitive positioning compared to other regions. Mediterranean pricing for Arab Light crude moved to a $0.55 discount against ICE Brent, widening from January's $0.15 discount—representing a 40-cent deterioration.

Northwest European pricing shifted even more dramatically, with Arab Light moving to a $0.35 discount versus ICE Brent from a previous $0.05 premium—also a 40-cent adjustment. This transition from premium to discount pricing indicates intensified competitive dynamics in European markets.

The uniform 40-cent reduction across all crude grades for European destinations contrasts with more modest 30-cent adjustments to Asian markets, suggesting region-specific competitive pressures. European refiners benefit from multiple supply options including North Sea production, Russian crude (subject to sanctions), and North African suppliers.

Mediterranean markets experience even wider discounts than Northwest Europe, reflecting proximity to alternative suppliers and regional refining configuration differences. The competitive intensity in these markets requires more aggressive pricing to maintain market share and supply relationships.

Production Strategy and Market Share Considerations

OPEC+ Output Decisions

OPEC+ maintained unchanged production levels during their January 5, 2026 meeting, despite ongoing geopolitical developments affecting member nations. Furthermore, the OPEC production impact on global supply chains reflects complex considerations balancing market stability against individual member revenue requirements.

The production group avoided addressing political crises affecting several members, focusing instead on market fundamentals and supply-demand balance assessments. Maintaining current output levels while prices adjust downward suggests confidence in market absorption capacity and long-term demand outlook.

Production discipline remains critical for market stability, though individual members may prioritise revenue optimisation over collective price support. In addition, the balance between market share preservation and price stability continues challenging traditional OPEC+ coordination mechanisms.

Current production allocations reflect historical negotiations and capacity considerations, though market conditions may require future adjustments as demand patterns evolve and new supply sources develop globally.

Supply Chain Resilience Factors

Global crude oil supply chains demonstrate remarkable adaptability despite ongoing geopolitical tensions and logistical challenges. Alternative sourcing capabilities reduce dependency on single suppliers while maintaining operational flexibility for refiners worldwide.

Tanker availability, storage capacity, and transportation infrastructure enable supply chain adjustments when traditional routes face disruption. Strategic petroleum reserves provide additional stability buffers for major consuming nations during market volatility periods.

The development of multiple benchmark pricing systems reflects supply chain diversification efforts, allowing market participants to optimise sourcing decisions based on quality specifications, transportation costs, and regional demand conditions.

Refinery configuration flexibility enables processors to adapt feedstock selections based on economic optimisation rather than exclusive supplier relationships, increasing competition among crude producers while improving supply security.

Investment Implications and Market Psychology

Refinery Margin Dynamics

Lower crude acquisition costs improve refinery crack spreads, particularly benefiting complex refineries with heavy crude processing capabilities. These facilities can maximise value extraction from discounted feedstocks while producing full petroleum product slates.

Asian refiners gain competitive advantages through improved input cost structures, especially those with flexible crude processing configurations. The ability to process various crude grades at attractive pricing enhances profitability during periods of abundant supply.

However, recent oil price movements indicate that refining margins depend on product demand strength relative to crude costs, creating opportunities during periods of favourable crack spreads. Petrol and diesel margins remain critical profitability drivers for most refining operations globally.

Inventory management strategies become crucial during volatile pricing periods, as refiners balance feedstock costs against product pricing cycles and storage capacity constraints.

Long-term Strategic Positioning

Consecutive price reductions signal potential long-term market share strategy prioritising volume maintenance over short-term revenue optimisation. This approach may influence marginal oil project investment decisions globally as developers reassess economic viability.

Upstream investment patterns typically respond to sustained price signals rather than short-term volatility, though extended periods of competitive pricing pressure may defer high-cost project developments. Consequently, the potential for oil price stagnation creates additional uncertainty for long-term investment planning.

Energy transition considerations add complexity to long-term investment planning, as traditional petroleum demand faces potential challenges from alternative energy adoption and efficiency improvements.

Market share preservation strategies reflect recognition of changing global energy dynamics, where maintaining customer relationships and supply chain positions becomes increasingly valuable amid industry transformation.

Commodity Trading and Market Structure Evolution

Benchmark Pricing Systems

The Oman/Dubai benchmark system continues serving as the primary Asian crude pricing reference, with approximately 9 million barrels per day of crude oil transactions utilising these official selling prices as reference points for commercial negotiations.

Price discovery mechanisms rely on spot market activity, futures trading, and official pricing announcements to establish fair value relationships between different crude grades and regional markets.

Derivative instruments based on these benchmarks provide risk management tools for market participants, enabling hedging strategies that protect against adverse price movements while maintaining operational flexibility.

Trading house operations adapt strategies based on expected pricing trends and regional arbitrage opportunities, influencing physical crude flows and storage utilisation patterns worldwide.

Forward Market Implications

Forward purchase strategies among refiners and trading companies increasingly reflect expectations of continued pricing flexibility from major suppliers, influencing global crude oil futures market sentiment and volatility patterns.

For instance, the tariff market impact demonstrates how contract structures evolve to accommodate changing market dynamics, with buyers seeking pricing optionality and suppliers maintaining volume commitments across different market conditions.

Risk management approaches become more sophisticated as market participants navigate increased price volatility and geopolitical uncertainty while maintaining operational efficiency.

| Crude Grade | February 2026 ($/bbl) | January 2026 ($/bbl) | Monthly Change |

|---|---|---|---|

| Super Light | +$1.95 | +$2.15 | -$0.20 |

| Extra Light | +$0.80 | +$1.10 | -$0.30 |

| Arab Light | +$0.30 | +$0.60 | -$0.30 |

| Medium | -$0.85 | -$0.55 | -$0.30 |

| Heavy | -$2.20 | -$1.90 | -$0.30 |

All prices relative to Oman/Dubai benchmark for Asian deliveries

The next major ASX story will hit our subscribers first

Energy Security and Strategic Reserve Management

Supply Chain Diversification Benefits

Saudi Arabia cuts oil prices to Asia while maintaining competitive positioning, encouraging supply chain diversification among major importing nations. This approach reduces single-supplier dependency while maintaining attractive crude acquisition costs for strategic buyers.

Multiple sourcing strategies enhance energy security by creating alternative supply options during geopolitical tensions or operational disruptions affecting traditional suppliers or transportation routes.

Regional supplier networks develop to provide backup capacity and competitive alternatives, improving negotiating leverage for importing nations while ensuring supply continuity during market stress periods.

Infrastructure investments in storage, transportation, and processing facilities support diversified sourcing strategies by accommodating different crude specifications and delivery logistics requirements.

Strategic Petroleum Reserve Considerations

Current pricing conditions create strategic petroleum reserve accumulation opportunities for major importing nations seeking to enhance energy security buffers at attractive acquisition costs.

Government stockpiling programmes may accelerate during favourable pricing environments, building strategic inventories that provide supply security during future market disruptions or geopolitical tensions.

Commercial inventory strategies also respond to attractive pricing opportunities, with companies building stocks when economics support storage investments relative to forward price expectations.

Release mechanisms for strategic reserves require careful planning to avoid market disruption while providing intended supply security benefits during crisis situations.

Market Outlook and Strategic Considerations

Near-term Price Trajectory Analysis

Current pricing trends suggest continued pressure on crude oil valuations through Q1 2026, with major suppliers maintaining flexible pricing approaches to preserve market position amid abundant global supply conditions. Furthermore, the broader oil price rally faces significant headwinds from these competitive dynamics.

Demand recovery patterns in major consuming regions will influence pricing dynamics, particularly in China where industrial activity levels affect regional crude consumption patterns significantly.

Seasonal factors typically influence crude demand through refinery maintenance schedules and product consumption patterns, though 2026 seasonal effects may differ from historical norms due to changing market structures.

Geopolitical developments continue creating potential supply disruption risks, though markets demonstrate increasing resilience through diversified sourcing and improved supply chain flexibility.

Long-term Strategic Implications

Energy market participants must evaluate investment strategies considering apparent willingness to compete on price rather than restrict supply, potentially establishing new equilibrium pricing levels for global crude markets.

Market share competition among major suppliers suggests sustained competitive pressure that may influence long-term industry consolidation patterns and investment allocation decisions.

Energy transition considerations add complexity to traditional petroleum market analysis, as alternative energy adoption rates influence long-term demand projections and investment planning horizons.

Infrastructure development requirements for changing energy systems create both challenges and opportunities for traditional petroleum industry participants adapting to evolving market conditions.

Investment Consideration: Energy market participants should carefully evaluate the implications of sustained competitive pricing on project economics, supply chain strategies, and long-term market positioning decisions during this period of structural industry change.

The evolving dynamics in global crude oil markets reflect broader transformations affecting energy systems worldwide. Consequently, understanding these pricing mechanisms and market forces provides valuable insight into future industry direction and investment considerations for market participants navigating an increasingly complex energy landscape.

In addition, recent developments in Saudi Arabia's strategic pricing decisions and broader Asian oil market dynamics continue to shape the competitive landscape for regional crude oil pricing strategies.

Ready to Capitalise on Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including opportunities in energy-related resources that could benefit from current market dynamics. Begin your 30-day free trial today to gain actionable insights and position yourself ahead of the market when energy commodities present exceptional investment opportunities.