June 14, 2026

The Geopolitics of Scarcity: Why India's Industrial Future Runs Through the Andes

Every major industrial revolution in history has been anchored by access to specific raw materials. Britain's dominance in the nineteenth century was inseparable from its coal reserves. America's twentieth-century ascendancy was underwritten by domestic oil and steel. Today, the architecture of economic power is being rebuilt around a new set of elements: copper, lithium, cobalt, and rare earth metals. For India, the world's most populous nation and one of its fastest-growing economies, this reconfiguration presents both an enormous opportunity and a structural vulnerability that is impossible to ignore.

India's industrial trajectory, encompassing mass EV adoption, grid-scale renewable energy, and advanced electronics manufacturing, requires vast quantities of minerals that its own geology cannot supply in adequate volume. This mismatch between what India needs and what it possesses domestically is the foundational driver behind one of the most consequential resource diplomacy campaigns currently unfolding in the developing world: India's strategic pivot toward the mining heartland of Latin America, and specifically toward India mining in Chile and Peru.

When big ASX news breaks, our subscribers know first

Understanding India's Copper Crisis Before the Crisis Arrives

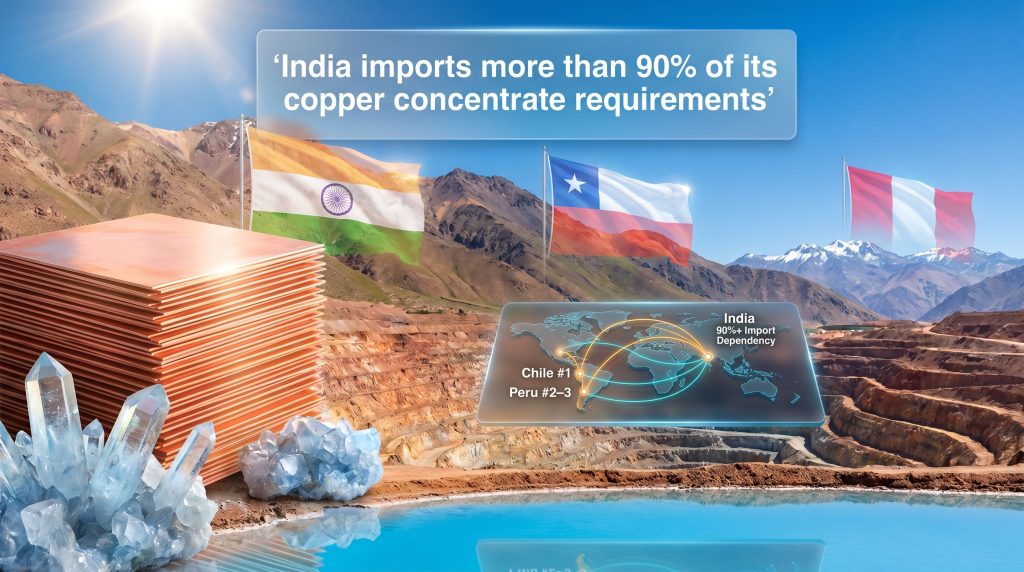

To appreciate why the Andean corridor has become a focal point of Indian foreign economic policy, it is necessary to understand the depth of the country's copper dependency. India currently imports more than 90% of its copper concentrate requirements, placing it among the most structurally exposed major economies on Earth for this single commodity (USGS, Mineral Commodity Summaries). Domestic copper mining contributes only a marginal fraction of what Indian smelters, led primarily by Hindalco and Vedanta, need to operate at capacity.

This dependency is not static. The International Energy Agency's India Energy Outlook 2021 projected that India's electricity demand would nearly double between 2020 and 2040, driven by rising incomes, accelerating urbanisation, and the electrification of transport and industry. Every additional unit of electricity generation, transmission, and distribution capacity requires copper, as does every electric vehicle, every solar panel inverter, and every industrial motor.

The World Bank's Minerals for Climate Action report estimated that meeting global climate targets could push demand for key transition metals up by more than 450% by 2050, with copper forming a foundational layer beneath virtually every clean technology pathway. Furthermore, the global copper supply crunch already unfolding makes early strategic positioning all the more critical for India.

What makes India's position particularly precarious is the secondary risk layer embedded within its existing copper supply chain. Even when India secures copper concentrate from overseas sources, a disproportionate share of global smelting and refining capacity is controlled by Chinese entities. This means India's industrial competitiveness is currently hostage not once but twice: first to foreign raw material suppliers, and then to Chinese-dominated midstream processing infrastructure. Addressing both vulnerabilities simultaneously is what gives India's Andean engagement its strategic urgency.

What Makes Chile and Peru Irreplaceable in India's Mineral Strategy

Chile's Dual Role as Copper Superpower and Lithium Frontier

Chile's mineral endowment is genuinely exceptional by global standards. The country holds the largest copper reserves on Earth and has historically ranked as the world's top copper-producing nation, accounting for roughly 27% of global mine output in recent years according to USGS data. Its established regulatory frameworks, relative institutional stability, and existing trade architecture make it a comparatively lower-risk destination for Indian capital and state-backed partnerships compared to many other resource-rich emerging markets.

Crucially, Chile's relevance to India extends beyond copper. The Atacama Desert's brine systems contain the most lithium-dense deposits on the planet. Chile's lithium strategy is, consequently, of enormous interest to Indian policymakers seeking to diversify feedstock supply for battery manufacturing.

One underappreciated technical point is that Atacama brine lithium is produced through solar evaporation rather than hard-rock mining, giving it among the lowest production costs of any lithium source globally. Understanding lithium brine extraction is therefore essential context for any investor or policymaker assessing the commercial viability of India's Andean ambitions. However, the same deposits face tightening environmental constraints around water use, and Chile's evolving policy environment introduces real timeline uncertainty for any prospective foreign investor.

Peru's Copper Corridor and Its Relevance to Indian Supply Chains

Peru consistently ranks among the top three global copper producers, with major mining regions concentrated in the Andean provinces of Apurímac, Moquegua, and Arequipa. The country's copper concentrate output feeds global smelting pipelines at scale, making it directly relevant to India's feedstock security needs. Peru also hosts significant zinc, gold, and silver endowments, offering potential for diversified mineral engagement beyond copper alone.

The investment climate in Peru is more complex than Chile's. Recurring episodes of political instability at the national level, combined with persistent community-level opposition to large-scale mining projects, have created a pattern of permitting delays and operational disruptions. Despite these risks, Peru's ongoing trade negotiations with India and the sheer scale of its copper resource base keep it firmly within India's strategic calculus.

Comparative Mineral Endowment: Chile vs. Peru

| Metric | Chile | Peru |

|---|---|---|

| Global Copper Rank (Production) | #1 | #2-3 |

| Lithium Reserves | World's largest (Atacama brines) | Limited |

| Key Minerals | Copper, Lithium, Molybdenum | Copper, Zinc, Gold, Silver |

| Trade Agreement Status with India | Under active negotiation | Under active negotiation |

| Primary State Mining Entity | Codelco (copper), SQM/Codelco (lithium) | Mixed private and state-linked operators |

| Key Risk Factors | Lithium nationalisation trajectory | Political instability, community opposition |

How India Is Building the Institutional Infrastructure for Mineral Access

KABIL: The State Vehicle for Overseas Mineral Acquisition

India's response to its mineral vulnerability is not purely diplomatic, it is also institutional. Khanij Bidesh India Limited (KABIL), established as a joint venture between three Indian state-owned mining companies (National Aluminium Company, Hindustan Copper Limited, and MECL), was created specifically to identify, acquire, and develop critical mineral assets outside Indian borders.

KABIL's operational mandate is deliberately broad, covering exploration rights, equity stakes, and offtake agreements across a geographic range that encompasses Latin America. The agency has already demonstrated that its activities extend beyond strategy documents: it concluded an agreement in Argentina covering lithium exploration blocks, providing concrete evidence that India's mineral diplomacy has moved from intent to execution. Latin America, including the copper and lithium belts of Chile and Peru, sits squarely within KABIL's declared priority geographies.

Trade Architecture With a Minerals Mandate

India's bilateral trade negotiations with Chile and Peru represent a structural evolution in how the country approaches commercial diplomacy. Traditionally, Indian trade agreements have prioritised market access for goods and services. The current negotiating framework explicitly incorporates critical mineral supply security as a core objective, reflecting a recognition that resource access has become a first-order strategic priority.

The specific instruments being developed include long-term supply agreements, preferential offtake rights for Indian entities, and frameworks enabling direct upstream investment participation. In addition, public-private partnership models are under active consideration, combining Indian state capital with private sector operational expertise to bridge the capability gaps that inevitably arise when a relatively new overseas investor enters a competitive sector.

India vs. China: A Comparison of Mineral Engagement Models

Understanding India's approach requires situating it against the model established by China over the preceding two decades. China's mineral strategy has been characterised by vertical integration from mine to refinery, infrastructure-for-minerals financing under the Belt and Road Initiative, and early-mover equity acquisition in resource-rich jurisdictions ranging from the Democratic Republic of Congo to Indonesia to Africa's lithium belt.

India's emerging model is structurally different, at least in its current phase. For instance, whereas China deployed state-owned enterprise capital aggressively and early, India is working through trade agreements and institutional vehicles like KABIL. India's copper strategy offers a useful parallel, demonstrating how the country is applying similar frameworks across multiple continents simultaneously.

| Dimension | China's Established Approach | India's Emerging Approach |

|---|---|---|

| Entry Strategy | Equity acquisition, infrastructure financing | Trade agreements, KABIL joint ventures, offtake frameworks |

| Processing Integration | Vertical, mine to refinery | Primarily upstream; midstream capacity being developed |

| Diplomatic Tools | BRI infrastructure deals | Bilateral trade pacts, state-to-state mineral agreements |

| Timeline | Decades of established presence | Active expansion from approximately 2023 onward |

| Key Latin American Targets | Chile, Peru (limited presence) | Chile, Peru, Argentina (copper and lithium) |

| Institutional Vehicle | SOE-led (Minmetals, CITIC, etc.) | KABIL plus private sector participants |

The critical insight here is that India is entering a competitive landscape already shaped by established players, and must offer differentiated value to host-country governments. Trade concessions, technology transfer proposals, and development cooperation arrangements are all tools under consideration as India works to establish a distinct value proposition relative to Chinese, Japanese, South Korean, and Western mining interests.

The Commodities India Needs Most: A Technical Breakdown

Copper: Why Concentrate Quality and Processing Routes Matter

A fact rarely discussed outside specialist circles is that not all copper concentrate is equal. The grade, penalty element profile, and mineralogy of concentrate batches determine which smelters can process them and at what cost. High-arsenic concentrates, for example, require specialised smelting infrastructure and can attract financial penalties from buyers.

India's domestic smelters have specific tolerance parameters, and any long-term offtake agreement with Chilean or Peruvian producers must be structured around concentrate specifications compatible with Indian processing facilities. Consequently, securing access to a mine is only the first step; ensuring that the concentrate produced is processable within India's existing or planned smelting infrastructure is a parallel engineering and commercial challenge.

Lithium: Brine Chemistry and Battery Grade Specifications

Chile's Atacama lithium is produced as lithium carbonate from brine, which must then be converted to lithium hydroxide for use in high-energy-density battery chemistries such as NMC (nickel-manganese-cobalt) and NCA (nickel-cobalt-aluminium). This conversion step is technically demanding and currently dominated by Chinese processing facilities.

For India to capture genuine value from Atacama lithium, it would need to develop or access lithium hydroxide conversion capacity, either domestically or through partnerships closer to the source. Furthermore, Codelco's copper strategy in Chile illustrates how state-controlled entities are increasingly shaping the terms under which foreign partners can participate in Chilean mineral value chains.

Cobalt, Nickel, and Rare Earth Elements

While copper and lithium dominate India's immediate mineral agenda, cobalt, nickel, and rare earth elements (REEs) are increasingly tracked as secondary priorities. These materials are essential for advanced battery chemistries, permanent magnets in EV motors and wind turbines, and defence electronics. The broader strategic logic of building diversified mineral supply relationships in the region extends naturally to these commodities as India's industrial base matures.

The next major ASX story will hit our subscribers first

Barriers, Risks, and the Latecomer Problem

Host-Country Political and Regulatory Complexity

Chile's ongoing lithium policy evolution, moving toward greater state participation in the sector through Codelco and revised licensing terms, introduces genuine uncertainty for foreign entities seeking upstream equity positions. The timeline and final form of Chile's lithium governance framework remain contested, and any foreign investor must factor regulatory evolution into project economics.

Peru's risk profile is different but equally real. The country has experienced multiple changes of government in recent years, each accompanied by shifts in mining policy signals. Community consultation requirements under Peruvian law, including free, prior, and informed consent processes with indigenous communities in mining regions, have extended project timelines significantly across the industry.

The Latecomer Disadvantage

Perhaps the most underappreciated challenge facing Indian mineral diplomacy in the Andes is simply the competitive weight of incumbency. Chinese entities have operated in Chilean and Peruvian mining for years. Japanese trading houses have established offtake relationships spanning decades. Western majors such as BHP, Rio Tinto, Freeport-McMoRan, and Glencore have operational footprints, relationship networks, and reputational capital that no new entrant can replicate quickly.

India must therefore compete not by matching established players on their own terms, but by identifying opportunities where its specific combination of trade leverage, market size, and state financing capacity can create a differentiated offer. According to recent critical minerals analysis, India is actively strengthening ties across Latin America to address precisely these competitive pressures.

Scenario Pathways: How India's Andean Engagement Could Unfold

The trajectory of India mining in Chile and Peru is genuinely uncertain, and investors, policymakers, and industry participants would be well-served by thinking across multiple scenarios rather than anchoring to a single forecast.

Scenario 1: Accelerated Integration

Trade agreements with Chile and Peru conclude within three to five years, KABIL secures equity positions in copper concentrate projects, and Indian smelting capacity expands to absorb Andean feedstock volumes. Lithium hydroxide conversion capacity develops through joint ventures, and India's Chinese processing dependency declines materially within a decade.

Scenario 2: Incremental Progress

Negotiations advance slowly but yield offtake agreements rather than equity positions. India's import dependency stabilises rather than declines, but supply diversification reduces concentration risk. KABIL builds operational experience in Argentina that transfers to Chile and Peru over time.

Scenario 3: Structural Stall

Chilean lithium nationalisation forecloses foreign equity participation, Peruvian political instability disrupts project timelines, and competitive exclusion by established players limits India's upstream access. Copper import dependency continues to rise unaddressed through the late 2020s.

The window for India to establish meaningful upstream positions in Andean mining is narrowing, not because the resources are running out, but because the terms of access are tightening as host-country governments recognise the strategic leverage their endowments provide and as competing nations accelerate their own agreement frameworks.

Key Takeaways: India's Mining Engagement With Chile and Peru

| Theme | Core Finding |

|---|---|

| Import Dependency | India imports 90%+ of copper concentrate, creating structural supply vulnerability |

| Primary Targets | Chile (copper and lithium), Peru (copper and zinc) |

| State Mechanism | KABIL, already operationally active in Latin America via Argentina |

| Geopolitical Driver | Reducing exposure to Chinese-dominated midstream processing |

| Trade Architecture | Bilateral agreements with minerals mandates under active negotiation |

| Technical Nuance | Concentrate quality and lithium hydroxide conversion are underappreciated bottlenecks |

| Key Risks | Chilean nationalisation trajectory, Peruvian political instability, latecomer dynamics |

| Long-Term Outlook | Early-stage but strategically consequential; execution capability will determine outcomes |

This article contains forward-looking analysis and scenario projections. These represent analytical frameworks based on publicly available information and should not be construed as investment advice or guarantees of future outcomes. Mineral markets, host-country regulatory environments, and geopolitical conditions are subject to rapid change.

Want to Track the Next Major Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex commodity data across copper, lithium, and more than 30 other commodities into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the market.