July 8, 2026

When One Waterway Controls the World's Gas Supply

Energy markets rarely fail catastrophically from many directions at once. More often, they fracture along a single point of concentrated dependency that nobody adequately stress-tested. The global liquefied natural gas system has long carried an underappreciated structural vulnerability: roughly one-fifth of all LNG export volumes move through a single maritime corridor just 33 kilometres wide at its narrowest point. The global gas demand decline IEA Strait of Hormuz LNG supply analysis makes this vulnerability impossible to ignore. When that corridor becomes contested, the consequences ripple into power grids, industrial facilities, fertiliser plants, and ultimately food systems across the world's most economically fragile regions.

That is precisely what 2026 has demonstrated. The conflict that erupted across the Middle East at the end of February 2026 has transformed the Strait of Hormuz from an operational constant into an active risk variable. Consequently, the global gas market is now recalibrating across every dimension: supply volumes, pricing architecture, procurement strategy, and long-term infrastructure investment.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is the Most Consequential Bottleneck in Global Energy

The Anatomy of a Chokepoint: What Makes Hormuz Irreplaceable?

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman and, from there, to international shipping lanes serving Asia, Europe, and beyond. For oil tankers, it is well understood as a critical corridor. For LNG carriers, its significance is even more concentrated because the producing infrastructure on its western shore is uniquely large and difficult to replicate.

Qatar's Ras Laffan industrial complex sits at the centre of this dependency. As the single largest LNG liquefaction site on the planet, Ras Laffan processes gas from the North Field, which Qatar shares with Iran and which represents one of the world's largest natural gas reserves. Every cargo that leaves Ras Laffan must transit the Strait. The UAE's Das Island and Ruwais facilities share the same routing constraint.

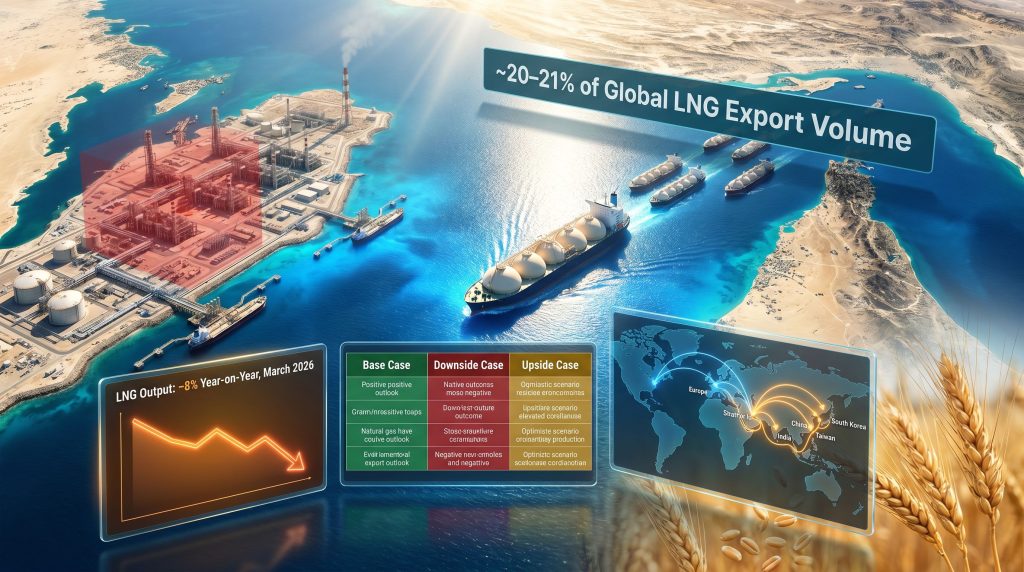

Approximately 20 to 21% of global LNG export volumes move through this single passage under normal operating conditions, according to data referenced in the IEA's Q3 2026 Gas Market Report. For Asian importing nations specifically, the dependency is even more pronounced, with the Strait accounting for roughly 25% of total LNG import volumes flowing into Northeast and South Asian markets.

Alternative routing options for LNG carriers are not practically equivalent. Unlike crude oil, where Saudi Arabia maintains the East-West Pipeline as a partial bypass, no comparable LNG pipeline infrastructure exists to redirect gas exports away from the Strait. Rerouting LNG carriers via the Cape of Good Hope adds weeks to transit times, dramatically increasing shipping costs and reducing effective delivery capacity. This is the architectural reality that makes Hormuz irreplaceable.

Mapping the Exposure: Which Regions Bear the Greatest Supply Risk?

The hierarchy of vulnerability among importing nations follows directly from their sourcing geography. Furthermore, the LNG supply outlook heading into 2025 had already highlighted the fragility of Hormuz-dependent trade flows:

- China, South Korea, Japan, and Taiwan hold long-term supply contracts heavily weighted toward Qatari LNG, making their exposure structurally embedded rather than merely spot-market-driven. Indeed, Asian LNG import pressures were already intensifying before the conflict emerged.

- India has diversified its LNG import portfolio more aggressively in recent years but still draws significant volumes from Hormuz-dependent suppliers.

- European buyers face elevated spot market prices but carry less direct structural dependency due to pipeline diversity, higher storage buffer capacity, and a broader geographic spread of contracted supply sources.

- South and Southeast Asian economies, including Bangladesh and Pakistan, lack the demand flexibility of wealthier importers and face acute exposure when spot prices spike.

The asymmetry between short-term spot exposure and long-term contracted supply creates a bifurcated risk landscape. Buyers holding fixed-price, long-term contracts with Qatari suppliers face force majeure uncertainty and volume shortfalls. Spot market participants, however, face price spikes but retain sourcing flexibility across alternative origins.

What Does a 0.5% Global Gas Demand Decline Actually Mean?

Decoding the IEA's Q3 2026 Gas Market Assessment

The International Energy Agency projects that global natural gas consumption will contract by approximately 0.5% across the full year. Taken in isolation, this figure appears modest. Placed in historical context, it is striking: this would mark the third annual demand decline within a seven-year period, a pattern without precedent in the modern gas market era.

Demand contractions at the global level are unusual because gas consumption has generally grown alongside industrialisation and population expansion in emerging markets. The emergence of three contraction years within a single seven-year window signals something more structural than a cyclical correction. This global gas demand decline IEA Strait of Hormuz LNG supply dynamic is reshaping the entire energy procurement landscape.

Demand Destruction by Sector: Power Generation vs. Industrial Consumption

The mechanisms driving the 2026 contraction are not uniform across sectors or geographies. The following table maps the primary drivers:

| Demand Sector | Driver of Decline | Regional Concentration | Structural or Cyclical? |

|---|---|---|---|

| Power Generation | Fuel switching to coal amid elevated gas prices | Asia, particularly China and India | Cyclical with structural risk |

| Industrial Activity | Supply tightening and feedstock cost inflation | Middle East, Europe | Structural, driven by infrastructure damage |

| Fertiliser Production | Natural gas as primary feedstock disrupted | Global, food-vulnerable regions most exposed | Structural |

| Residential and Commercial | Price-driven conservation and efficiency responses | Europe and Asia | Cyclical |

Analytical note: The coal re-entry dynamic in Asian power sectors deserves particular attention. When gas prices spike, grid operators in China and India face a straightforward economic calculation: coal is cheaper and domestically available. The policy implications of this substitution extend well beyond energy markets into emissions trajectories and climate commitments.

The Middle East Demand Collapse: A Supply-Side Shock Feeding Back Into Consumption

One of the less-discussed dimensions of the current disruption is that the Middle East is simultaneously a major producing and consuming region. Conflict-related damage to gas-intensive industrial facilities within the producing zone has suppressed regional demand from the inside out. Gas-fired power plants, desalination facilities, and petrochemical complexes across the affected area have reduced throughput, creating a feedback loop where supply destruction and demand destruction are occurring in the same geography.

This paradox complicates market modelling. Standard supply-disruption frameworks assume that demand remains intact while supply contracts. In this case, both sides of the equation are contracting simultaneously in the most affected region, which partially explains why the global demand decline figure of 0.5% does not fully capture the severity of the underlying disruption.

How Has the Global LNG Supply System Responded?

The Compensatory Supply Architecture: North America, Africa, and Australia

The global LNG system has not simply absorbed the Hormuz disruption passively. New liquefaction capacity coming online across alternative producing regions in 2025 and 2026 has partially offset Middle Eastern volume losses. Export terminals in the United States, Mozambique, and Australia have ramped incremental output to capture market share vacated by disrupted Qatari and UAE volumes.

This compensatory response has a ceiling, however. Replacement volumes from these alternative origins cannot fully substitute for disrupted Qatari output in the near term for three reasons:

- Contract rigidity: Many Asian buyers hold take-or-pay contracts with Qatari suppliers rather than alternative producers, limiting their ability to freely redirect procurement.

- Shipping economics: Australian and US Gulf Coast cargoes destined for Northeast Asian buyers travel longer distances, compressing effective delivered volume relative to equivalent Qatari shipments.

- Infrastructure constraints: The pace of new liquefaction capacity additions is finite and was already reflected in pre-conflict market balance projections.

The Critical Threshold: What a Delayed Strait Reopening Triggers

At peak disruption intensity in March 2026, LNG output dropped approximately 8% year-on-year, according to the IEA's assessment. The supply gap at peak disruption removed approximately 7 million tonnes per month from global LNG availability, with weekly throughput losses estimated at roughly 1.5 million tonnes per week, equivalent to approximately 2.2 billion cubic metres of gas.

Scenario Alert: The IEA has indicated that if full Strait reopening is delayed beyond the beginning of Q4 2026, the market could face the first annual decline in global LNG supply volumes since 2012. This would represent a landmark deterioration in a trade system that has grown continuously for over a decade.

LNG Supply Scenario Modelling: Three Pathways for the Remainder of 2026

| Scenario | Strait Status by Q4 2026 | Annual LNG Supply Outcome | Price Trajectory |

|---|---|---|---|

| Base Case | Partial reopening, gradual volume recovery | Flat to marginally negative versus 2025 | Moderating but elevated above 2025 levels |

| Downside Case | Reopening delayed beyond Q4 | First annual LNG supply decline since 2012 | Sustained elevation; renewed Asia-Europe competition for cargoes |

| Upside Case | Full reopening by September 2026 | Near-flat supply with recovery momentum | Rapid moderation toward pre-conflict price levels |

The Qatar Capacity Expansion Setback: A Multi-Year Consequence

Why Ras Laffan Infrastructure Damage Has Long-Horizon Implications

The disruption to Ras Laffan carries consequences that extend well beyond 2026. Qatar had been executing one of the most ambitious LNG capacity expansion programmes in history, targeting a significant increase in annual export capacity from the North Field. Conflict-related damage to infrastructure at the facility has disrupted not just current output but the construction and commissioning timeline for these expansion trains.

The IEA's Q3 2026 report indicates that the impacts on projected supply growth are expected to be concentrated primarily in 2026 and 2027, creating a two-year window during which global gas markets will remain tighter than pre-conflict projections had indicated. This is a critical distinction for utilities, governments, and industrial buyers who had incorporated Qatar's expansion volumes into their medium-term supply planning assumptions.

Before the Conflict: What Did the Market Balance Look Like in Late 2025?

The current tightness is particularly jarring because the market had been moving in the opposite direction. From the second half of 2025 onward, a genuine easing trajectory was underway as new global LNG supply facilities came online across multiple producing regions. Spot prices were declining, long-term contract negotiations were shifting in buyers' favour, and analyst consensus pointed toward a more balanced market through 2026 and 2027.

The conflict reversed this trajectory with speed and severity that most market participants had not adequately scenario-planned for. The energy price shock has been especially acute for nations with limited procurement flexibility. The gap between pre-conflict supply growth projections and post-conflict revised forecasts now defines the supply shortfall that importing nations must navigate.

How Are Asian and European Gas Markets Adapting?

Asia's Policy Response: Fuel Switching, Demand Management, and Procurement Diversification

Across major Asian importing economies, government and utility responses to the supply shock have followed several parallel tracks:

- Power sector coal substitution has been the most immediate and visible response, with grid operators in China and India increasing coal burn as a direct price hedge against elevated LNG costs.

- Demand management programmes have been activated in several Northeast Asian economies, including industrial curtailment guidelines and residential conservation incentive schemes.

- Procurement diversification is accelerating, with buyers pursuing spot and short-term contracts with US, Australian, and African suppliers to reduce Hormuz-concentrated exposure in future supply portfolios.

- Long-term contract renegotiation is underway in several cases, with buyers seeking geographic diversification clauses and force majeure protections tied to specific chokepoint scenarios.

Europe's Position: Elevated Prices Without the Same Structural Dependency

European gas prices have experienced material elevation relative to 2025 baselines, though they have moderated from the extreme levels recorded in March 2026. The structural exposure is meaningfully different from Asia's, however, for several reasons.

Europe's LNG import portfolio has diversified rapidly since 2022, with US LNG now representing a substantial share of import volumes. Pipeline supply from Norway and Azerbaijan provides a partial buffer unavailable to island or peninsular economies in Asia. Storage infrastructure across Northwest Europe provides seasonal demand flexibility, and demand response mechanisms established during the 2022 energy crisis remain partially embedded in industrial and commercial consumption patterns.

The US-Iran Interim Agreement: What Changed and What Remains Uncertain?

The interim agreement reached between the United States and Iran in mid-June 2026 to end hostilities and reopen the Strait has provided a partial reset. LNG carrier traffic through the Strait has resumed and is trending upward from post-conflict lows. However, throughput volumes remain materially below pre-conflict levels, and market participants are pricing in a meaningful uncertainty premium reflecting unresolved questions about the agreement's durability and the pace of infrastructure rehabilitation.

The next major ASX story will hit our subscribers first

Beyond Energy: How the Gas Disruption Is Reshaping Food Security

Natural Gas as a Fertiliser Feedstock: The Hidden Agricultural Exposure

The relationship between natural gas and food production is one of the most systemically important and least publicly understood linkages in the global economy. Natural gas, specifically methane, is the primary feedstock for the Haber-Bosch process that produces ammonia, the foundation of nitrogen-based fertilisers. Without affordable natural gas, ammonia production becomes economically unviable at scale, and without ammonia, global crop yields collapse.

The Hormuz disruption has cascaded directly into global fertiliser availability and pricing through this channel. Producing nations in the Middle East that export both LNG and ammonia-based fertilisers have seen simultaneous disruptions to both output streams.

Critical Linkage: The transmission mechanism from gas market disruption to food security risk operates through fertiliser supply chains, and it disproportionately affects economies that cannot absorb higher agricultural input costs. Sub-Saharan Africa, South Asia, and parts of the Middle East represent the highest-risk concentration of food import dependency coinciding with fertiliser supply vulnerability.

Historical precedent supports treating this linkage seriously. The European gas crisis of 2022 prompted several major European fertiliser producers, including CF Industries and Yara, to curtail ammonia production as gas prices made operations uneconomic. The resulting fertiliser price spike contributed directly to food price inflation in import-dependent economies across Africa and South Asia. The 2026 Hormuz disruption has activated a similar transmission pathway, but from a producing region that directly supplies both gas and fertiliser to some of the world's most food-vulnerable markets.

What Are the Strategic Implications for LNG Investment?

Reassessing LNG Project Economics in a Post-Disruption Environment

The Hormuz crisis is altering the risk calculus for long-term LNG infrastructure investment in ways that will outlast the immediate disruption. Project finance teams, insurers, and offtake contract negotiators are incorporating chokepoint concentration risk into their analytical frameworks with a rigour that was previously absent.

Interest in non-Hormuz-dependent export route development is accelerating. Potential pipeline bypass infrastructure, expanded capacity at alternative terminals, and floating liquefaction solutions in non-constrained geographies are all attracting elevated investor attention. The broader trade and geopolitics analysis surrounding energy infrastructure investment has shifted fundamentally as a result.

The Geopolitical Diversification Imperative for Importing Nations

The lessons being drawn by energy security planners across Asia and Europe converge on a common conclusion: supply portfolios anchored to a single maritime chokepoint represent an unacceptable concentration of strategic risk. The strategic value of long-term supply agreements with producers in the United States, Australia, and East Africa has been materially re-rated upward by this event.

Sovereign wealth funds and national energy companies across Northeast Asia are actively repositioning procurement strategies. Furthermore, the willingness to pay a modest premium for non-Hormuz-dependent supply diversity is now embedded in procurement decision-making in ways that will reshape LNG trade flows for years ahead.

Infrastructure Resilience as a Policy Priority

Several governments across Asia and Europe are advancing policy frameworks to mandate higher strategic gas reserves, accelerate floating storage and regasification unit deployment as rapid-response tools, and expand onshore LNG storage capacity. Floating storage and regasification units are particularly valued in this context because they can be deployed quickly and repositioned as circumstances change, providing supply flexibility that fixed onshore infrastructure cannot match.

Frequently Asked Questions

What Is the IEA's Forecast for Global Gas Demand in 2026?

The International Energy Agency projects that global natural gas consumption will contract by approximately 0.5% across 2026, driven primarily by reduced demand in power generation and industrial sectors. This would represent the third annual decline in global gas demand decline IEA Strait of Hormuz LNG supply conditions within a seven-year period.

How Much of Global LNG Supply Passes Through the Strait of Hormuz?

Approximately 20 to 21% of global LNG export volumes transit the Strait of Hormuz under normal conditions, with the majority originating from Qatar and the UAE. For Asian importing nations, the Strait accounts for roughly 25% of total LNG import volumes.

What Would Happen if the Strait of Hormuz Remained Closed Through Q4 2026?

A sustained closure through the fourth quarter of 2026 would likely produce the first annual decline in global LNG supply volumes since 2012. The market would face a structural shortfall of approximately 7 million tonnes per month at peak disruption, intensifying competition for non-Hormuz cargoes between Asian and European buyers and sustaining elevated price levels.

Why Has Qatar's LNG Expansion Been Delayed?

Conflict-related damage to infrastructure at Ras Laffan, the world's largest LNG liquefaction complex, has disrupted the operational and construction timeline for Qatar's planned capacity expansion. Supply growth impacts are expected to be concentrated primarily in 2026 and 2027.

How Does the Gas Supply Disruption Affect Food Security?

Natural gas is a critical feedstock for ammonia-based fertiliser production through the Haber-Bosch process. Disruptions to gas supply chains reduce fertiliser availability and increase agricultural input costs globally, with the most acute impacts concentrated in food-import-dependent economies across Sub-Saharan Africa, South Asia, and parts of the Middle East.

What Is the Current Status of LNG Shipping Through the Strait of Hormuz?

Following the interim agreement reached between the United States and Iran in mid-June 2026, LNG carrier traffic has resumed and is trending upward. However, throughput volumes remain materially below pre-conflict levels, and significant uncertainty persists regarding the long-term stability of the agreement and the timeline for full market normalisation.

Key Takeaways: The Structural Shift in Global Gas Market Architecture

- The Hormuz disruption has exposed the concentration risk embedded in a global LNG trade system where a single maritime chokepoint controls approximately one-fifth of all export volumes.

- A 0.5% demand contraction in 2026 masks deeper sectoral and regional divergences, with Middle Eastern and Asian markets bearing disproportionate adjustment burdens.

- The delay to Qatar's capacity expansion creates a two-year window of tighter-than-expected supply conditions that will persist regardless of when the Strait fully reopens.

- The cascading effects into fertiliser markets and food security represent the most underappreciated systemic risk emanating from the gas market disruption.

- Strategic responses including supply diversification, storage expansion, and long-term contracting with non-Hormuz producers are likely to permanently reshape LNG procurement strategies across major importing economies.

- The coal re-entry dynamic in Asian power sectors carries long-term implications for emissions trajectories that extend well beyond the immediate energy security response.

This article contains forward-looking analysis and scenario modelling based on IEA projections and publicly available market data as of early July 2026. Energy market conditions remain subject to rapid change based on geopolitical developments, and readers should not interpret any scenario projections as investment advice or assured market outcomes. For ongoing coverage of Middle East energy developments and IEA market assessments, Zawya's Energy section at zawya.com provides continuous regional reporting.

Want to Track the ASX Opportunities Emerging From Global Energy Disruptions?

When geopolitical shocks reshape commodity markets at this scale, significant mineral discovery opportunities often follow — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment major ASX mineral discoveries are announced, turning complex market signals into actionable investment insights. Explore Discovery Alert's discoveries page to see how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.