August 5, 2026

Understanding the Critical Dynamics of Global Iron Ore Markets

The global commodity landscape operates through intricate supply chains where disruptions can reverberate across continents within days. Iron ore, as the fundamental raw material for steel production, represents one of the most strategically sensitive trade relationships in modern industrial economics. When major producers and consumers experience friction, the ripple effects extend far beyond bilateral negotiations into currency markets, shipping rates, and industrial planning cycles worldwide.

The complexity of modern commodity relationships stems from their dual nature as both industrial inputs and geopolitical instruments. Supply security, pricing mechanisms, and settlement currencies have evolved into tools of economic statecraft, particularly as nations seek to reduce dependencies on traditional market structures. This strategic dimension transforms what might appear as commercial disagreements into broader tests of supply chain resilience and market power distribution.

Recent developments between major Australian producers and Chinese purchasing entities illustrate these evolving dynamics in real time. The interaction between commercial negotiations and policy frameworks creates multi-layered challenges that require sophisticated BHP-China iron ore dispute resolution mechanisms balancing immediate operational needs with long-term strategic positioning.

When big ASX news breaks, our subscribers know first

Examining the Commercial and Strategic Tensions

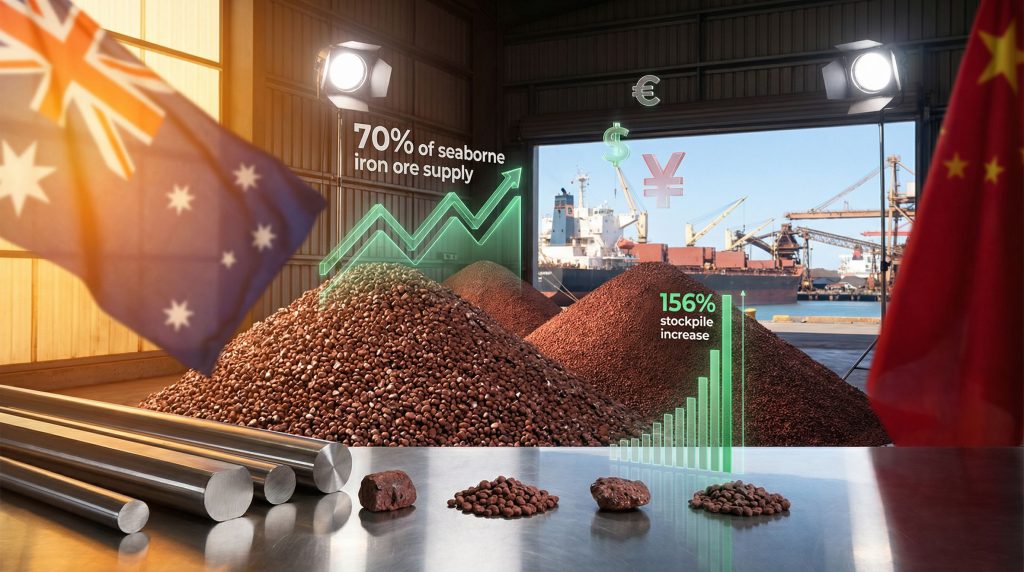

The fundamental structure of iron ore trade relationships reflects decades of established patterns built around USD-denominated pricing and standardised quality specifications. China's emergence as the dominant consumer of seaborne iron ore supply has created unprecedented concentration risk for producers whilst simultaneously providing Chinese entities with significant negotiating leverage through volume control.

Currency settlement mechanisms have become increasingly contentious as China advances broader financial strategies aimed at internationalising the yuan across commodity markets. The technical challenge lies not merely in price conversion but in establishing banking infrastructure, hedging mechanisms, and risk management protocols that accommodate multi-currency transactions without disrupting existing supply chain financing arrangements.

Quality specifications present another layer of complexity, particularly regarding technical standards for iron ore grades. Products such as Jimblebar Blend Fines and Newman Fines carry specific metallurgical characteristics that affect steel production efficiency. Disputes over these specifications can quickly escalate from technical disagreements into broader commercial restrictions, as purchasing entities leverage quality concerns to influence negotiating positions.

Long-term contract negotiations have evolved beyond traditional volume and pricing arrangements to incorporate sophisticated flexibility mechanisms. Modern agreements must address currency volatility, force majeure scenarios, and quality assurance protocols whilst maintaining sufficient operational flexibility for both parties to adapt to changing market conditions. Furthermore, these arrangements must consider iron ore price trends that affect long-term viability.

Tracing the Evolution of Trade Restrictions and Accommodations

Initial Disruption Phase

The September 2025 period marked a significant escalation when China Mineral Resources Group directed steelmakers to pause purchases of specific product categories. This action represented a shift from individual company negotiations to centralised purchasing coordination, demonstrating China's strategic approach to commodity market leverage.

Import restrictions expanded systematically from Jimblebar fines to include Newman fines, indicating a calculated approach rather than isolated quality concerns. The resulting port stockpile accumulation of approximately 156% between mid-September and November 2025 created visible evidence of supply chain disruption whilst maintaining plausible technical justifications for the restrictions.

Partial Resolution Efforts

Early 2026 brought tentative accommodation measures as both parties recognised the costs of prolonged disruption. The agreement for 30% of spot sales to be settled in yuan currency represented a significant compromise from traditional USD-exclusive arrangements, though it maintained majority dollar exposure for the producer whilst providing China with meaningful yuan internationalisation progress.

Enhanced customs inspections implemented during this phase served dual purposes of maintaining pressure whilst creating operational pathways for resumed trade. Limited cargo discharges at select Chinese ports allowed for gradual normalisation whilst preserving negotiating leverage for both sides. Additionally, iron ore demand insights revealed how these restrictions affected broader market expectations.

Current Normalisation Trajectory

Recent diplomatic engagement, including high-level executive visits to Beijing in April 2026, suggests movement toward comprehensive resolution. However, the absence of formal confirmations regarding meetings with China Mineral Resources Group indicates ongoing sensitivity around the negotiation process.

Market reactions to these diplomatic signals demonstrate the broader industry's attention to resolution progress. Iron ore slides after new SA-born BHP boss sighted in Beijing, with prices dropping to $102.10 per ton following reports of executive engagement, reflecting trader expectations about supply normalisation and its impact on market dynamics.

Analysing Market Forces and Resolution Incentives

| Market Factor | Resolution Impact | Timeline Sensitivity |

|---|---|---|

| Chinese Steel Demand | Creates urgency for stable supply access | Q2-Q3 2026 seasonal patterns |

| Capesize Freight Markets | Influences alternative sourcing economics | Real-time rate fluctuations |

| Brazilian Production Capacity | Affects China's negotiating alternatives | 6-12 month expansion cycles |

| Spot vs Contract Pricing | Determines settlement mechanism flexibility | Ongoing market conditions |

Chinese steel demand patterns drive fundamental resolution incentives as industrial production cycles require predictable raw material access. Seasonal construction activity typically peaks during Q2-Q3 periods, creating natural deadlines for supply arrangement finalisation. Disruptions during high-demand periods carry disproportionate economic costs for steel producers and their industrial customers.

Capesize vessel freight rates significantly influence the economics of alternative sourcing strategies. Higher freight costs from Brazilian suppliers can strengthen the negotiating position of Australian producers, whilst depressed shipping rates reduce the penalty for supply chain diversification. Current market participants monitor Baltic Dry Index movements as indicators of sourcing flexibility.

Brazilian iron ore production capacity represents China's primary alternative to Australian supply, though logistical and quality differences create imperfect substitution. Vale's production schedules and port infrastructure capacity directly influence China's willingness to accept extended negotiations versus pursuing alternative supply arrangements.

Consequently, the relationship between spot market pricing and long-term contract mechanisms affects both parties' flexibility in reaching accommodation. Furthermore, understanding iron ore price decline factors helps predict negotiation dynamics.

Evaluating Geopolitical Considerations and Strategic Objectives

Resource Security and Supply Chain Control

China's establishment of the China Mineral Resources Group in 2022 represented a fundamental shift toward centralised commodity purchasing coordination. This institutional development provides Chinese negotiators with enhanced leverage through coordinated demand management whilst reducing individual steelmaker autonomy in supplier relationships.

The strategic resource security dimension extends beyond immediate commercial considerations to encompass long-term industrial planning and crisis resilience. Chinese policymakers view diversified supply sources and favourable commercial terms as essential components of economic security, particularly given the concentration of high-quality iron ore production among the largest iron ore mines in Australia and Brazil.

Currency Sovereignty and Financial Infrastructure

Yuan settlement initiatives reflect China's broader objectives of reducing USD dependence in international trade whilst expanding yuan internationalisation. However, the technical complexity of implementing multi-currency commodity trading requires sophisticated financial infrastructure development and risk management capabilities.

Banking relationships, hedging instruments, and settlement mechanisms must accommodate currency flexibility without disrupting established financing arrangements that support global commodity trade flows. These infrastructure requirements often prove more challenging than the political commitments to currency diversification.

Strategic Relationship Management

Both parties recognise the importance of maintaining stable long-term relationships whilst preserving negotiating flexibility. The scale of China-Australia iron ore trade creates mutual dependencies that discourage extreme positions, though periodic tensions reflect underlying strategic competition and policy divergences.

The resolution framework emerging from current negotiations will likely establish precedents for other major commodity relationships, particularly in sectors where geographic concentration creates similar strategic dependencies.

In addition, broader economic factors such as US‑China trade war impacts continue to influence bilateral commodity relationships.

Assessing Broader Industry Implications and Competitive Dynamics

Precedent Setting for Future Commodity Negotiations

The commercial and technical mechanisms developed through this BHP-China iron ore dispute resolution process will influence negotiations across multiple commodity sectors. Currency settlement arrangements, quality specification protocols, and dispute resolution mechanisms established here may become templates for other major trading relationships.

Other major producers monitor these developments closely as indicators of acceptable commercial terms and negotiating strategies. The balance achieved between commercial flexibility and strategic positioning will inform future contract negotiations across the global commodity complex.

Competitor Positioning and Market Share Dynamics

Rio Tinto, Fortescue Metals Group, and Vale face strategic decisions regarding their own Chinese market approaches based on the precedents established through these negotiations. Competitive advantages may emerge for producers willing to accept currency diversification or enhanced quality assurance requirements.

Market share redistribution remains possible if resolution terms create competitive disadvantages for major producers relative to smaller or more flexible competitors. However, the scale advantages and infrastructure investments of major producers typically provide resilience against short-term market disruptions.

Transportation and Logistics Reconfiguration

Shipping market dynamics may experience permanent alterations based on new trade flow patterns established through resolution arrangements. Capesize vessel deployment, port infrastructure utilisation, and freight rate structures could shift to accommodate modified trading relationships.

Long-term charter arrangements and shipping capacity investments respond to sustained changes in trade patterns rather than temporary disruptions. However, the scale of China-Australia iron ore trade means significant alterations in shipping arrangements could influence global dry bulk market structure.

The next major ASX story will hit our subscribers first

Analysing Price Volatility and Market Structure Evolution

Short-term Price Movement Patterns

Immediate market reactions to resolution progress demonstrate the sensitivity of iron ore pricing to supply security perceptions. Price movements following diplomatic engagement, such as the 3.5% decline to $102.10 per ton after reports of executive meetings, indicate trader positioning around normalisation expectations.

Port inventory levels in Chinese facilities provide tangible indicators of supply flow restoration. Inventory accumulation during restriction periods and subsequent drawdowns following resolution progress offer measurable metrics for assessing trade normalisation pace.

Medium-term Market Structure Implications

Hybrid pricing mechanisms incorporating multiple currencies may reduce traditional benchmark volatility whilst creating new arbitrage opportunities for sophisticated market participants. Currency basis differentials could emerge as additional trading factors alongside traditional supply and demand fundamentals.

Quality premium structures may become more standardised as resolution processes clarify technical specifications and testing protocols. Enhanced quality assurance requirements could benefit producers with superior product consistency whilst penalising those with variable quality control.

Identifying Risk Factors and Resolution Vulnerabilities

Regulatory and Policy Implementation Risks

Complex resolution arrangements face implementation challenges related to customs procedures, banking regulations, and quality control protocols. Technical failures in operational execution could undermine negotiated agreements despite good-faith political commitments from both parties.

Changes in broader trade policies or diplomatic relationships could affect commodity-specific agreements, particularly given the integration of economic and strategic considerations in modern international relations. Resolution sustainability requires isolation from unrelated bilateral tensions.

Market Disruption Scenarios

Global steel demand fluctuations could alter the fundamental economics underlying negotiated arrangements. Significant demand reductions might reduce Chinese interest in maintaining complex accommodation mechanisms, whilst demand surges could increase pressure for supply access regardless of commercial terms.

Third-party supply disruptions, such as Brazilian production interruptions or shipping market disruptions, could modify the strategic calculations underlying current negotiations. External market forces may either strengthen resolution incentives or provide alternatives that reduce accommodation pressures.

Furthermore, Reuters reported that China has relaxed restrictions on some BHP iron ore cargoes, indicating progress in the BHP-China iron ore dispute resolution.

Preparing for Multiple Resolution Scenarios

Comprehensive Resolution Pathway

A complete resolution scenario involves normalised trade flows, stable pricing mechanisms, and reduced geopolitical risk premiums. This outcome would likely emerge through Q2 2026 as seasonal steel demand increases create natural deadlines for supply arrangement finalisation.

Market participants should prepare for:

- Stabilised iron ore pricing around fundamental supply-demand balances

- Reduced volatility premium in derivative markets

- Normalised shipping patterns and freight rate relationships

- Enhanced commercial relationship stability for similar trade partnerships

Partial Accommodation Scenario

Ongoing restrictions on specific product categories could create segmented market conditions where certain grades trade at discounts whilst others maintain premium pricing. This scenario might persist through extended negotiation periods whilst technical implementation challenges are resolved.

- Product-specific pricing differentials reflecting quality or commercial restrictions

- Continued elevated freight costs for alternative sourcing arrangements

- Selective supplier relationship development by Chinese purchasers

- Enhanced focus on quality assurance and technical specification compliance

Extended Standoff Outcomes

Prolonged negotiation stalemates could force significant supply chain restructuring with lasting implications for global iron ore trade patterns. Whilst this represents the lowest probability scenario, the potential impacts would be substantial enough to warrant contingency planning.

- Permanent market share redistribution among major producers

- Infrastructure investments in alternative supply chains

- Development of parallel trade and financing mechanisms

- Increased strategic inventory holdings by major consumers

Strategic Implications for Market Participants

The evolution of the BHP-China iron ore dispute resolution offers critical insights into the changing nature of commodity trade relationships. The integration of commercial negotiations with currency policy, technical standards, and strategic positioning reflects broader trends in international economic relationships.

Supply chain resilience emerges as a fundamental requirement for major commodity market participants. The ability to maintain operational flexibility whilst accommodating evolving political and commercial requirements will differentiate successful companies from those unable to adapt to changing market structures.

Currency risk management capabilities become increasingly important as multi-currency commodity trading expands beyond traditional USD-denominated arrangements. Companies must develop sophisticated financial management systems capable of handling complex currency exposure whilst maintaining commercial competitiveness.

Quality assurance and technical specification compliance will likely receive enhanced attention as purchasing entities leverage technical requirements for strategic positioning. Investment in quality control systems and product standardisation may become competitive advantages rather than merely operational requirements.

Investment Consideration: Market participants should develop scenario-based planning frameworks that account for the evolving nature of commodity trade relationships, recognising that commercial agreements increasingly reflect broader strategic and political considerations rather than purely economic factors.

The resolution of this trade dispute will establish important precedents for future commodity market negotiations whilst providing insights into the resilience and adaptability of global supply chain relationships under strategic pressure. Understanding these dynamics becomes essential for effective risk management and strategic positioning in evolving commodity markets.

Ready to Capitalise on the Next Major Mining Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring major mineral finds that have delivered exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.