June 22, 2026

Global Lithium Markets Face Paradigm Shift as Supply Concentration Intensifies

The lithium sector stands at a crossroads where geopolitical strategy intersects with industrial necessity. As governments worldwide grapple with critical mineral security, Chile's recently approved Codelco–SQM lithium deal represents more than a corporate partnership—it signals a fundamental restructuring of how nations control resources essential to the energy transition. While electric vehicle adoption accelerates and battery demand surges, the concentration of lithium production in fewer hands raises profound questions about market stability and strategic autonomy.

Traditional mining partnerships typically focus on operational efficiency and cost reduction. However, the Codelco–SQM alliance operates within a different framework entirely, where state involvement aims to maximize national value capture while maintaining international supply commitments. This hybrid governance model emerges as countries recognize that lithium extraction transcends commercial considerations to become a matter of national security.

When big ASX news breaks, our subscribers know first

Strategic Architecture of the Codelco–SQM Partnership

State-Private Hybrid Control Mechanisms

The Codelco–SQM lithium deal establishes a governance structure that balances state control with operational expertise. Under this arrangement, SQM maintains operational control through 2030, leveraging its established Atacama infrastructure and technical capabilities, while Codelco assumes strategic oversight and eventual full management.

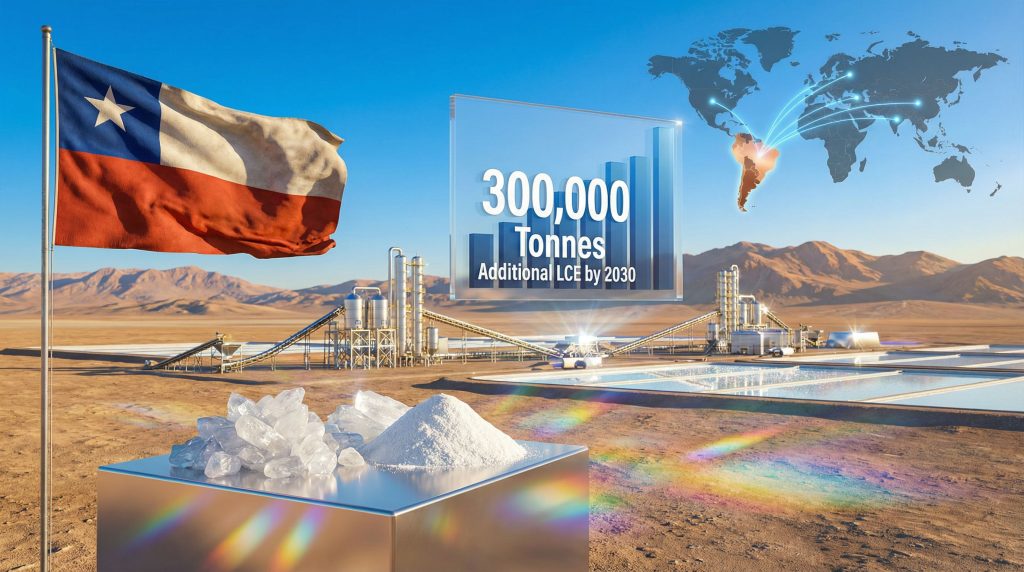

This phased transition model differs significantly from purely privatised operations seen in Australian lithium innovations or fully state-controlled enterprises dominating Chinese lithium processing. The partnership targets 300,000 tonnes of lithium carbonate equivalent annually by 2030, representing approximately 18-21% of projected global supply deficits under accelerated electrification scenarios.

Chile's approach emphasises maximising domestic value capture while ensuring environmental compliance and indigenous consultation, contrasting with Argentina lithium insights showing more aggressive lithium acceleration strategies across multiple operators like Livent and POSCO subsidiaries.

Geopolitical Positioning Within Global Supply Networks

The partnership positions Chile strategically within evolving supply chain networks. Currently accounting for 28-30% of global lithium production, Chile's dominant position in the Atacama Salt Flat creates both opportunities and vulnerabilities for international battery manufacturers.

Key strategic advantages include:

• Geographic diversification for Asian battery manufacturers seeking alternatives to Australian spodumene sources

• High-purity lithium carbonate from brine extraction, achieving 99.5-99.7% purity levels ideal for battery applications

• Established infrastructure reducing development timelines compared to greenfield projects in Argentina or Bolivia

• Political stability relative to other lithium-rich regions experiencing regulatory volatility

The Codelco–SQM structure provides international buyers with supply security while ensuring Chilean strategic control over pricing and allocation decisions. This balance becomes crucial as global lithium demand is projected to reach 1.4-1.7 million tonnes LCE by 2030 under various electrification scenarios.

Regulatory Scrutiny and Market Concentration Analysis

Multi-Jurisdictional Competition Authority Review Process

The partnership underwent intensive scrutiny from competition authorities across multiple jurisdictions, including China, the European Union, Brazil, Japan, and South Korea. This broad regulatory review reflected concerns about market concentration in critical mineral supply chains.

Competition authorities focused on several key areas:

• Market concentration risks where the combined entity would control approximately 40-45% of global lithium production capacity post-2030

• Strategic supply manipulation potential, given Chile's dominant position and increasing state control

• Downstream processing bottlenecks, as Chinese companies control 60-65% of global lithium conversion capacity

• Price coordination possibilities between state-controlled entities and private operators

Regulatory approval came with conditions including transparency requirements on pricing mechanisms, commitments to supply stability, and restrictions on production curtailment. Furthermore, these remedies mirror approaches used in other critical mineral cases, such as the EU's rare earth element market reviews conducted between 2020-2023.

Implications for Future Industry Consolidation

The conditional approval framework established precedents for future lithium sector consolidation. Regulators prioritised ensuring enhanced production capacity would not enable supply restrictions or artificial price inflation, particularly given lithium's critical importance for energy transition technologies.

| Regulatory Jurisdiction | Primary Concerns | Approval Timeline |

|---|---|---|

| European Union | Market concentration, supply security | Q4 2024 |

| China | Technology transfer, processing capacity | Q1 2025 |

| Japan | Battery supply chain stability | Q3 2024 |

| South Korea | Long-term contract availability | Q4 2024 |

| Brazil | Regional competition effects | Q2 2025 |

The regulatory framework suggests future lithium partnerships will face similar scrutiny, particularly those involving state entities or creating substantial market concentration.

Production Capacity Analysis and Global Supply Impact

Quantifying Supply Contribution Against Demand Projections

The Atacama partnership's 300,000 tonnes annual LCE output by 2030 addresses a significant portion of projected supply shortfalls. Current global production of approximately 1.2 million tonnes annually falls short of International Energy Agency projections suggesting demand will reach 1.4-1.7 million tonnes by 2030.

| Year | Global Demand (tonnes LCE) | Atacama JV Output | % of Total Supply |

|---|---|---|---|

| 2025 | 1,100,000 | 50,000 | 4.5% |

| 2027 | 1,300,000 | 150,000 | 11.5% |

| 2030 | 1,500,000 | 300,000 | 20% |

| 2035 | 2,100,000 | 300,000+ | 14.3% |

Regional demand distribution by 2030 shows concentrated requirements:

• Asia (China, South Korea, Japan): 50-55% of global demand

• Europe: 20-25% of demand

• North America: 15-20% of demand

• Other regions: 5-10% of demand

Technology and Processing Advantages

The Atacama operation leverages evaporation pond technology where naturally concentrated brine undergoes solar evaporation. This process produces higher-purity lithium carbonate compared to spodumene-based extraction used in Australian operations like Pilbara Minerals' Pilgangoora project.

Technical advantages include:

• Lower processing costs compared to hard rock spodumene extraction

• Higher margins due to natural concentration in Atacama brines

• Established infrastructure reducing capital expenditure requirements

• Solar-powered evaporation lowering energy costs

Modern improvements incorporate direct lithium extraction techniques, which accelerate processing timelines and reduce water consumption by approximately 90%. However, large-scale commercial DLE deployment remains in pilot phases, creating technology risk for rapid scaling.

Risk Assessment and Implementation Challenges

Environmental and Water Resource Constraints

The Atacama Desert receives less than 1mm annual precipitation, making water management critical for sustainable operations. Traditional brine processing requires approximately 500,000 gallons per tonne of lithium extracted, placing significant stress on local freshwater aquifers.

Water resource challenges include:

• Competing demands from agriculture and municipal usage

• Regulatory bottlenecks for new water extraction licences

• Environmental permitting delays for expanded operations

• Community opposition to increased water consumption

The partnership must navigate these constraints while scaling from current SQM production of approximately 70,000 tonnes LCE annually to the targeted 300,000 tonnes, requiring 4x expansion of evaporation ponds and processing capacity.

Political and Regulatory Uncertainty Factors

Chile's political environment shows volatility regarding mining policy, with shifting administrations affecting taxation, environmental standards, and indigenous consultation requirements. The partnership's success depends on policy continuity around export protocols, tax regimes, and environmental permitting.

Critical risk factors include:

• Chilean comptroller audit outcomes regarding compliance and indigenous consultation adequacy

• Electoral cycles potentially introducing new mining sector constraints

• Indigenous community relations requiring ongoing consultation under ILO Convention 169

• Environmental regulatory changes affecting permitting timelines

Important Notice: The Chilean comptroller's audit of the partnership structure could result in 12-24 month delays if inadequate indigenous consultation or environmental shortcomings are identified.

Management Transition and Operational Continuity

The planned 2030 transition from SQM operational control to Codelco management introduces execution risk. Codelco has faced historical operational challenges, including labour disputes and infrastructure underinvestment at other mining operations.

Key transition risks include:

• Technology transfer adequacy from SQM to Codelco technical teams

• Workforce retention during organisational culture shifts

• Operational efficiency maintenance post-transition

• International contract continuity under state management

Successful technology transfer requires seamless knowledge transfer across brine processing, chemical refining, and quality control systems. Inadequate preparation could reduce production efficiency and compromise international supply commitments.

Global Market Dynamics and Competitive Responses

Impact on Alternative Lithium Production Regions

The Codelco–SQM lithium deal's scale creates competitive pressures across other major lithium-producing regions. Australian spodumene producers, including Pilbara Minerals and others, face increased competition from low-cost South American brine operations.

Competitive dynamics include:

• Cost pressure on higher-cost Australian hard rock operations

• Quality differentiation between brine-derived and spodumene-based lithium compounds

• Supply chain diversification benefits for battery manufacturers

• Investment reallocation toward proven brine operations

Argentine lithium projects must demonstrate superior economics or strategic advantages to compete with the Atacama partnership's established infrastructure and political backing, whilst addressing lithium mining challenges inherent in brine-based extraction.

Strategic Responses from Chinese Lithium Processors

Chinese companies controlling 60-65% of global lithium conversion capacity face strategic decisions regarding South American supply integration. The Codelco–SQM partnership provides both opportunities and challenges for Chinese battery supply chains.

Strategic considerations include:

• Vertical integration versus reliance on Chilean state-controlled supply

• Processing capacity expansion to handle increased South American output

• Technology partnerships with Chilean entities for domestic processing development

• Alternative supply source development to reduce dependence risks

Chinese lithium processors like Ganfeng Lithium and Tianqi Lithium may pursue joint venture opportunities within Chile to secure long-term supply access while maintaining processing control.

The next major ASX story will hit our subscribers first

Investment Implications and Capital Allocation Strategies

Direct Investment Metrics and Timeline Considerations

The partnership requires substantial capital expenditure for infrastructure scaling to achieve 300,000 tonnes annual capacity. Investment considerations include:

| Investment Category | Estimated Range (USD) | Timeline |

|---|---|---|

| Evaporation pond expansion | $800M – $1.2B | 2025-2028 |

| Processing facility upgrades | $400M – $600M | 2026-2029 |

| Water management systems | $200M – $300M | 2025-2027 |

| Transportation infrastructure | $150M – $250M | 2026-2030 |

Revenue sharing between Codelco and SQM follows a structured model through the partnership phases, with Codelco's ownership percentage increasing toward the 2030 transition date.

Downstream Industry Investment Opportunities

The partnership creates investment opportunities across the lithium value chain:

• Chilean processing facilities for lithium hydroxide and specialty compounds

• Port infrastructure development for increased export capacity

• Regional economic development projects in northern Chile

• Technology partnerships for advanced extraction and processing methods

Battery manufacturers benefit from supply chain diversification away from concentrated Asian processing, potentially justifying premium pricing for secure supply contracts. In addition, the establishment of a battery-grade lithium refinery infrastructure provides critical downstream integration opportunities.

Critical Minerals Security and Strategic Frameworks

Comparison with Global Resource Nationalism Trends

Chile's state-private hybrid model parallels similar approaches across critical mineral sectors. Indonesia's nickel strategy combines state-owned PT Antam with private operators to control nickel concentrate exports while promoting domestic processing.

Key strategic parallels include:

• Export restriction policies encouraging domestic value-added processing

• Foreign investment controls in strategic mineral sectors

• State enterprise partnerships with international technology providers

• Community consultation requirements for social licence maintenance

The Codelco–SQM framework provides a template for other Latin American countries developing lithium resources, particularly Bolivia and Argentina, where state involvement varies significantly.

Long-term Geopolitical Implications for Energy Security

The partnership influences global energy security frameworks as countries seek supply chain resilience. European Union critical raw materials objectives emphasise diversification away from Chinese processing dominance, making Chilean supply strategically valuable.

Strategic implications include:

• US-China technology competition effects on lithium supply access

• Regional integration opportunities within Latin American mining frameworks

• Strategic stockpiling considerations for major consuming nations

• Technology transfer requirements for sustained competitive advantage

Countries implementing national battery manufacturing strategies must balance supply security with cost competitiveness, making the Codelco–SQM lithium deal a critical component of global supply planning.

Environmental and Social Governance Framework

Sustainable Operations in Extreme Environments

The Atacama Desert's extreme conditions require specialised environmental management protocols. Water resource management becomes paramount given competing demands from local communities and agricultural operations.

Sustainability requirements include:

• Water consumption minimisation through advanced extraction technologies

• Brine management to prevent aquifer contamination

• Solar energy utilisation for processing operations

• Waste heat recovery systems for energy efficiency

Climate change adaptation measures must address increasing temperatures and altered precipitation patterns affecting desert operations. Extreme weather events could disrupt production timelines and require infrastructure hardening investments.

Indigenous Consultation and Community Relations

Chilean law mandates prior consultation and consent for projects affecting indigenous territories under ILO Convention 169. The Atacama region hosts Lickanantay (Atacameño) communities with traditional water and land rights.

Community engagement frameworks require:

• Ongoing consultation processes throughout operational phases

• Benefit-sharing mechanisms for local economic development

• Employment creation prioritising indigenous community members

• Cultural preservation measures for traditional practices

Inadequate consultation frameworks or unresolved community grievances could trigger legal injunctions halting operations or requiring costly modifications. Successful projects demonstrate genuine partnership approaches rather than mere compliance with minimum legal requirements.

Frequently Asked Questions

When will the joint venture achieve full-scale production capacity?

The partnership targets 300,000 tonnes annual LCE capacity by 2030, with production ramp-up beginning around 2027. Timeline achievement depends on environmental permitting, infrastructure development, and community consultation completion.

What specific commitments were required by international regulators?

Competition authorities imposed conditions including transparency requirements on pricing mechanisms, commitments to supply stability, restrictions on production curtailment, and independent compliance monitoring. Specific terms vary by jurisdiction but focus on preventing anti-competitive practices.

How will the partnership affect global lithium pricing dynamics?

The additional 300,000 tonnes capacity could moderate price volatility by addressing supply shortfalls projected for 2030. However, pricing effects depend on demand growth rates, alternative supply development, and Chinese processing capacity expansion.

What happens if the Chilean comptroller audit identifies compliance issues?

Audit findings could result in 12-24 month operational delays for remediation if significant compliance shortcomings are identified. Potential issues include inadequate indigenous consultation or environmental permit violations requiring corrective action.

How does this partnership compare to other major global lithium alliances?

The Codelco–SQM structure represents the largest state-private lithium partnership by production capacity. Other significant alliances include Chinese companies' Australian operations and various Argentine public-private ventures, but none match the scale and state involvement of the Chilean model.

Strategic Scenarios for Global Energy Transition

The Codelco–SQM lithium deal fundamentally reshapes global battery supply chains by establishing a state-controlled alternative to purely private mining operations. This partnership provides supply security for battery manufacturers while demonstrating how resource-rich countries can maximise value capture from critical mineral extraction.

Success scenarios depend on successful environmental management, community relations maintenance, and seamless operational transitions. The partnership's 300,000 tonnes annual capacity addresses approximately one-fifth of projected supply deficits, making it strategically critical for global electrification goals.

Consequently, investment monitoring should focus on infrastructure development milestones, regulatory compliance outcomes, and community consultation progress through 2030. The partnership's performance will influence similar state-private models across Latin America and other critical mineral sectors globally.

"The approval of this partnership represents a fundamental shift in how Chile approaches strategic resource management, balancing international market demands with national sovereignty objectives."

The global energy transition requires diverse, resilient supply chains spanning multiple regions and governance models. The Codelco–SQM partnership represents one critical component of this complex system, demonstrating how strategic partnerships can balance national interests with international supply security requirements.

Disclaimer: This analysis is based on publicly available information as of December 2025. Production targets, regulatory conditions, and investment requirements may change based on operational developments, policy modifications, or market conditions. Readers should verify current information before making investment or strategic decisions.

Interested in Strategic Lithium Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including critical battery metals like lithium, empowering subscribers to identify actionable opportunities ahead of the broader market. With major mining partnerships reshaping global supply chains, staying ahead of discovery announcements becomes crucial for capturing both short-term trading gains and transformative long-term investments through real-time market intelligence.