June 22, 2026

The Quiet Restructuring of Global Mineral Diplomacy

The world's most consequential industrial agreements are no longer signed in the boardrooms of multinational corporations. Increasingly, they are formalised between governments at dedicated mining forums, shaped by a single overriding imperative: securing access to the minerals that underpin the entire energy transition. Lithium, copper, cobalt, rare earths, uranium, chromium — these are the building blocks of electric vehicles, grid-scale storage, advanced semiconductors, and next-generation manufacturing systems. Nations that control them, or that can forge credible partnerships to access them, are positioning themselves at the centre of the next industrial era.

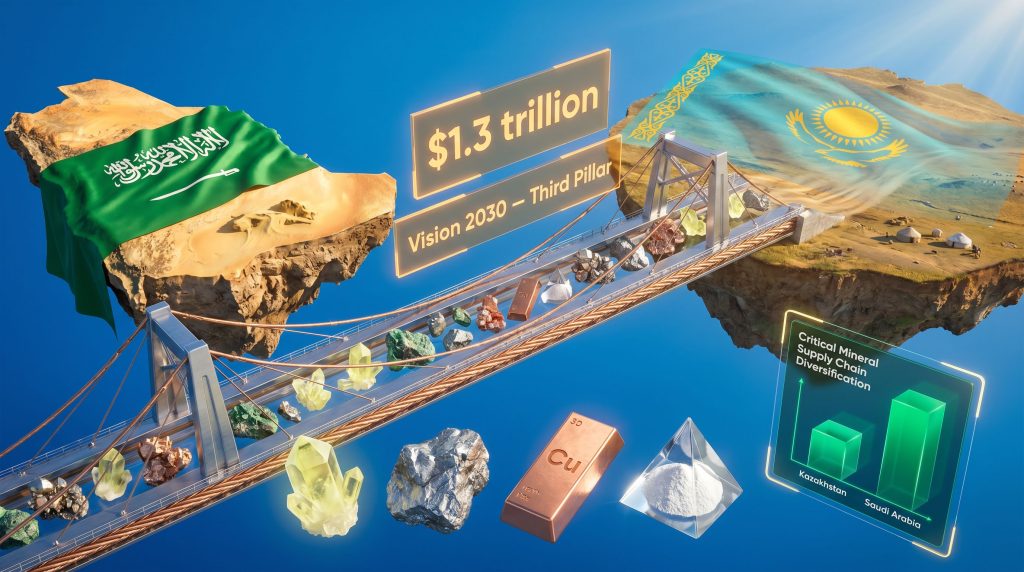

It is within this context that the Saudi Arabia Kazakhstan mining MoU, signed on June 11, 2026, carries significance well beyond the immediate diplomatic moment. This agreement reflects a structural shift in how resource-rich and capital-rich nations are choosing to engage with one another outside of the traditional Western-and-Chinese-dominated supply chain architecture. Furthermore, the broader Saudi licensing push signals that this MoU is part of a coordinated, long-term strategic posture rather than an isolated diplomatic gesture.

When big ASX news breaks, our subscribers know first

Two Economies, One Strategic Logic

Understanding why this particular bilateral partnership makes sense requires examining what each nation brings to the table and what each is trying to achieve.

Kazakhstan is, by almost any geological measure, one of the most mineral-endowed nations on earth. The country ranks among the top two globally for uranium production, consistently accounting for roughly 40 to 45 percent of global uranium output in recent years. Beyond uranium, Kazakhstan holds world-class deposits of chromium, copper, zinc, manganese, barite, and titanium. Crucially, it also contains resources directly relevant to critical minerals demand and the energy transition, including minerals used in battery cathode chemistry and grid infrastructure systems. Despite this extraordinary endowment, Kazakhstan's mineral sector has historically been underdeveloped relative to its full geological potential, creating a structural gap between resource wealth and economic realisation.

Saudi Arabia approaches this partnership from a fundamentally different position. The Kingdom is not a major mineral producer in the conventional sense, but it holds an estimated $1.3 trillion in untapped mineral wealth according to government assessments, with significant deposits of phosphate, gold, zinc, and bauxite identified across the Arabian Shield geological formation. More importantly, Saudi Arabia is capital-rich, logistics-capable, and strategically motivated to transform its economy under Vision 2030, which formally designates mining as the Kingdom's third major economic pillar alongside oil and petrochemicals.

These two nations represent a genuinely complementary pairing: one possessing the resource base, the other possessing the capital, infrastructure ambition, and geographic reach to unlock that resource base's full industrial value.

The Four Pillars of the Saudi Arabia Kazakhstan Mining MoU

The agreement signed by Saudi Industry and Mineral Resources Minister Bandar Alkhorayef and Kazakhstan's Industry and Construction Minister Yerlan Nagaspayev is structured around four interconnected cooperation areas that collectively span the entire mining value chain.

Knowledge Exchange and Exploration Technology

The first and perhaps most foundational pillar involves the systematic sharing of geological knowledge, survey methodologies, and exploration technologies. This is more technically significant than it might initially appear. Modern mineral exploration has undergone a profound technological evolution over the past decade. Where traditional exploration relied on physical sampling and geological mapping, contemporary approaches incorporate:

- Airborne geophysical surveys using magnetometry and electromagnetic methods to detect subsurface mineralisation without drilling

- Hyperspectral remote sensing from satellite and drone platforms to identify surface mineralogical signatures

- AI-assisted geological target generation, which uses machine learning models trained on historical discovery datasets to predict the locations of undiscovered deposits

- 3D subsurface modelling that integrates multiple data types into probabilistic resource models

Saudi Arabia is at an earlier stage of systematically cataloguing its mineral endowment compared to Kazakhstan. Consequently, the knowledge exchange pillar represents a genuine transfer of exploration capability that could accelerate Saudi Arabia's domestic mineral discovery pipeline.

Joint Investment Facilitation

The second pillar creates the structural conditions for private capital to move between the two jurisdictions. This is architecturally important: government-to-government MoUs of this type function primarily as enabling frameworks rather than direct investment commitments. They establish the regulatory clarity, mutual recognition, and institutional trust that allow private companies to engage in cross-border co-financing, joint ventures, and co-development arrangements with reduced friction.

The qualification of 24 firms for new Saudi exploration licences in June 2026 is directly relevant here. The domestic licensing pipeline is expanding precisely as the international partnership framework is being assembled, suggesting a coordinated strategy to attract both domestic and foreign capital simultaneously.

Mining Value Chain Integration

The third pillar addresses the most strategically complex dimension of the partnership: moving beyond raw extraction toward integrated industrial value chains. This concept, which Minister Alkhorayef has articulated consistently across multiple forums, reflects a sophisticated understanding of where commodity economics actually creates durable national wealth.

The conventional model of resource development involves extracting raw ore, exporting it to processing hubs (historically dominated by China in the critical minerals space), and receiving payment for a low-value commodity. The integrated value chain model instead seeks to capture value at every stage: mining, beneficiation, smelting and refining, precursor chemical production, and advanced manufacturing of battery materials or industrial inputs.

Kazakhstan already possesses meaningful metallurgical processing infrastructure built during the Soviet era and subsequently modernised. Saudi Arabia, however, is investing heavily in building downstream processing capacity. Together, the partnership creates a potential corridor where Kazakh ores could be processed through Saudi facilities en route to European and Asian markets, generating value at both ends.

Innovation and Emerging Technology Integration

The fourth pillar, while perhaps the most forward-looking, is increasingly central to competitive mining operations globally. The forum session at the Astana International Mining and Metals Forum, titled From the Depths of the Earth to the Horizons of Artificial Intelligence: Global Partnerships Shaping the Future of the Mining and Minerals Sector, framed AI and advanced technology not as peripheral tools but as core drivers of the sector's next phase.

Practically, this encompasses:

- Autonomous mining equipment reducing operational costs and safety risks in underground and open-pit operations

- Predictive maintenance systems using sensor data and machine learning to reduce unplanned equipment downtime

- AI-driven ore sorting and grade control to maximise recovery and reduce processing waste

- Digital twin modelling of entire mine operations for optimisation and scenario planning

Saudi Arabia's Hub Architecture: The Geographic Logic

One of the less-examined dimensions of the Saudi Arabia Kazakhstan mining MoU is how it fits within a broader geographic strategy. Minister Alkhorayef has repeatedly described Saudi Arabia's ambition to function as a global minerals hub connecting Africa, Europe, and Asia. This is not merely rhetorical positioning. The Kingdom is investing materially in the infrastructure that makes such a hub viable.

| Infrastructure Element | Strategic Function |

|---|---|

| Red Sea and Gulf port networks | Mineral import/export gateway |

| Railway corridor expansion | Inland logistics for ore and processed materials |

| Industrial zone development | Co-location of processing and manufacturing |

| Logistics free zones | Reduced friction for re-export flows |

| Financial sector deepening | Capital availability for large-scale mining investment |

Kazakhstan sits at the northern end of this hub's potential reach, connected via Central Asian transport corridors that are themselves undergoing significant infrastructure investment. The mineral flows envisaged under this partnership would, in theory, transit through multiple infrastructure nodes across both countries.

What Makes Kazakhstan's Mineral Profile Uniquely Relevant to the Energy Transition

A critical insight that is often overlooked in coverage of Kazakhstan's mineral sector is the specific nature of its energy transition relevance. Much attention focuses on Kazakhstan uranium dominance, but the energy transition mineral story is more nuanced.

Kazakhstan holds deposits of several minerals that sit at critical pinch points in battery supply chains:

- Copper: Essential for electrical wiring, EV motors, and charging infrastructure. Kazakhstan ranks in the top ten globally for copper reserves.

- Manganese: A key component of lithium-manganese-oxide (LMO) and lithium-nickel-manganese-cobalt-oxide (NMC) battery cathode chemistries, which are gaining commercial traction as battery manufacturers seek to reduce cobalt dependency.

- Titanium: Increasingly relevant to next-generation battery electrolyte formulations and aerospace applications.

- Chromium: Critical for stainless steel used in industrial equipment across the energy sector.

The combination of uranium for nuclear baseload power and transition minerals for storage and electrification positions Kazakhstan as arguably the most comprehensively energy-transition-relevant mineral jurisdiction in Central Asia.

The Supply Chain Diversification Imperative

The broader context for the Saudi Arabia Kazakhstan mining MoU cannot be separated from the accelerating global debate about critical mineral supply chain concentration. A significant proportion of global rare earth supply chains, lithium refining, and cobalt chemical production currently flows through a very small number of facilities in a limited number of countries. This concentration creates systemic vulnerability for industrial economies that depend on these materials.

Bilateral agreements like this MoU are one of the primary instruments through which nations are attempting to build alternative supply chain architecture. The key structural shifts this agreement reflects include:

-

Mining diplomacy elevation: Mineral cooperation agreements are now conducted at senior ministerial level, treated as strategic economic instruments equivalent in importance to energy or defence cooperation.

-

South-South and cross-regional framework building: Non-Western nations are constructing independent mineral supply chain networks that do not route through existing dominant processing corridors.

-

Value chain capture as a national objective: Both Kazakhstan and Saudi Arabia are explicitly pursuing strategies to retain more industrial value domestically rather than exporting low-value raw commodities.

-

Private sector enablement as government philosophy: Minister Alkhorayef's articulation of the government's role as facilitator rather than operator represents a deliberate policy model that prioritises creating conditions for private investment rather than direct state participation.

-

Technology as a structural partnership pillar: AI, automation, and data-driven exploration are no longer treated as sector-specific technical matters but as core elements of intergovernmental mining cooperation frameworks.

The next major ASX story will hit our subscribers first

Kazakhstan's Multi-Vector Diplomatic Advantage

One dimension of Kazakhstan's strategic position that adds complexity to this partnership is the country's carefully maintained relationships across multiple geopolitical blocs. Kazakhstan is a member of the Shanghai Cooperation Organisation (SCO) and maintains deep economic ties with Russia through the Eurasian Economic Union. Simultaneously, it has actively cultivated relationships with Western nations and multilateral institutions seeking alternatives to Chinese-dominated mineral supply chains.

This multi-vector positioning gives Kazakhstan a degree of diplomatic flexibility that few major mineral-producing nations can match. For Saudi Arabia, which is itself navigating complex relationships across Western, Asian, and regional geopolitical spheres, Kazakhstan represents a partner whose diplomatic posture is compatible with its own strategic ambiguity. Indeed, reporting from Economy Middle East confirms that both governments view the partnership as a long-term strategic alignment rather than a transactional arrangement.

It is worth noting that the full commercial realisation of the partnership's potential will depend on private sector appetite, regulatory alignment between the two jurisdictions, and the resolution of practical logistical challenges in cross-regional mineral transport. MoUs establish intent and framework; they do not guarantee investment outcomes.

Frequently Asked Questions: Saudi Arabia Kazakhstan Mining MoU

What was agreed between Saudi Arabia and Kazakhstan in June 2026?

Saudi Arabia and Kazakhstan signed a Memorandum of Understanding on June 11, 2026, establishing a cooperation framework across the mining and mineral resources sector. The agreement covers geological knowledge exchange, adoption of modern exploration technologies, facilitation of joint investments, and development of integrated mining value chains. It was formalised at the Astana International Mining and Metals Forum.

Who were the signatories of the agreement?

The MoU was signed by Bandar Alkhorayef, Saudi Arabia's Minister of Industry and Mineral Resources, and Yerlan Nagaspayev, Kazakhstan's Minister of Industry and Construction, during an official ministerial visit to Kazakhstan.

How does the MoU connect to Saudi Vision 2030?

The agreement directly advances Vision 2030's objective of establishing mining as a national economic pillar, supporting GDP diversification and reducing structural dependence on hydrocarbon revenues. It also advances Saudi Arabia's ambition to function as a global minerals hub connecting major continental markets through integrated value chains.

Which critical minerals are most relevant to this partnership?

Kazakhstan's mineral endowment includes uranium, copper, manganese, chromium, zinc, titanium, and barite. Several of these are directly relevant to battery technology, EV manufacturing, grid infrastructure, and advanced industrial systems that sit at the core of the global energy transition.

What is the Astana International Mining and Metals Forum?

The Astana International Mining and Metals Forum is a major Central Asian mining investment and policy event hosted in Kazakhstan's capital. The 2026 edition centred on the intersection of artificial intelligence and global mining partnerships, drawing senior government officials and sector leaders from across multiple regions. Furthermore, coverage from TIMES Central Asia highlights the forum's growing significance as a venue for high-level mineral diplomacy.

Does this MoU guarantee investment outcomes?

No. An MoU establishes a cooperative framework and signals political intent. Actual investment outcomes depend on subsequent commercial negotiations, regulatory alignment, private sector participation, and market conditions. This distinction is important for investors and analysts assessing the agreement's near-term economic impact.

Key Strategic Takeaways

| Dimension | Saudi Arabia | Kazakhstan |

|---|---|---|

| Primary Motivation | Critical mineral access + global hub positioning | Foreign investment, technology transfer, market access |

| Value Chain Priority | Processing, logistics, downstream manufacturing | Exploration, extraction, raw material supply |

| Vision 2030 Alignment | Direct: mining as third economic pillar | Indirect: economic diversification and FDI attraction |

| Energy Transition Role | Industrial transformation requires critical mineral inputs | Holds key deposits across multiple transition mineral categories |

| Technology Dimension | AI exploration, digital mining operations | Adoption of advanced exploration and operational platforms |

| Diplomatic Context | Global hub strategy across Africa, Europe, Asia | Multi-vector positioning across SCO, Western, and Gulf relationships |

The Saudi Arabia Kazakhstan mining MoU is best understood not as a single bilateral event but as one node in a rapidly expanding network of mineral diplomacy agreements reshaping global supply chain architecture. For analysts, investors, and policymakers tracking the critical minerals space, the Astana forum and the agreements signed there represent a leading indicator of where the next phase of industrial competition will be contested.

Want to Identify the Next Major Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the complexity of global commodity shifts to surface actionable opportunities for investors at every level. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.