July 9, 2026

The Global Manufacturing Paradigm Shift Accelerating Supply Chain Security

Manufacturing resilience has evolved from an operational efficiency metric to a fundamental national security priority. As technological competition intensifies between major economic powers, the control mechanisms governing critical material flows increasingly determine industrial competitiveness across entire economic blocs. This transformation reflects a broader shift from market-based resource allocation toward strategically-motivated supply management, where geopolitical considerations override traditional cost-optimization frameworks.

The rare earth elements sector exemplifies this paradigm shift most clearly. These seventeen metallic elements enable virtually all advanced manufacturing processes, from permanent magnets in electric vehicles to precision-guided munitions in defence systems. Unlike conventional commodities where multiple suppliers compete globally, rare earth supply chains concentrate both geographically and technologically in ways that create systemic vulnerabilities for importing economies.

Recent policy developments demonstrate how China tightens rare earth export controls to achieve broader strategic objectives. The January 2026 implementation of enhanced dual-use export restrictions targeting Japan illustrates this evolution from economic tool to diplomatic leverage. Chinese authorities characterise these measures as legitimate responses to security concerns, while affected economies confront immediate production continuity risks that transcend typical supply chain management capabilities.

When big ASX news breaks, our subscribers know first

Understanding China's Strategic Export Control Framework

China's export control architecture operates through a sophisticated dual-use classification system that distinguishes between civilian and military applications for identical materials. This regulatory approach creates significant compliance challenges for manufacturers operating across multiple sectors, particularly in industries where civilian and military supply chains increasingly converge.

The Dual-Use Technology Classification System

The Ministry of Commerce maintains comprehensive catalogues defining which rare earth materials, processing technologies, and finished products require export licensing. These classifications extend beyond raw materials to encompass processing equipment, technical documentation, and even software applications used in rare earth refining operations.

Current regulations establish multi-tier review processes involving coordination between the Ministry of Commerce, national security agencies, and industry-specific regulatory bodies. Applicants must demonstrate end-use compliance through detailed documentation including purchase contracts, facility inspections, and ongoing monitoring agreements.

Key Classification Categories:

- Raw rare earth concentrates and separated oxides

- Processing equipment and separation technologies

- Permanent magnet alloys and finished magnetic assemblies

- Electronic components containing rare earth elements

- Technical documentation and manufacturing processes

The system's complexity creates inherent uncertainty for international buyers. Furthermore, identical materials may receive different classification depending on stated end-use, purchasing entity, and destination country. This regulatory ambiguity serves strategic purposes by maintaining flexibility for Chinese authorities while imposing compliance costs on foreign manufacturers.

Extraterritorial Reach of Chinese Regulations

Chinese export controls extend jurisdiction beyond territorial boundaries through technology transfer restrictions and overseas subsidiary compliance requirements. Foreign companies utilising Chinese-origin rare earth materials must implement monitoring systems tracking material flows, processing applications, and final product destinations throughout their global operations.

These extraterritorial provisions affect joint ventures, licensing agreements, and technology partnerships involving Chinese rare earth suppliers. Additionally, international manufacturers often face requirements to segregate Chinese-origin materials from other supply sources, implement separate inventory tracking systems, and provide periodic compliance audits to Chinese regulatory authorities.

The enforcement mechanisms include contract termination provisions, financial penalties, and exclusion from future supply allocations. Chinese suppliers increasingly incorporate regulatory compliance clauses in commercial agreements that extend Chinese legal jurisdiction to overseas manufacturing operations.

What Industries Face the Greatest Supply Chain Vulnerability?

Industrial vulnerability to Chinese rare earth export controls varies significantly based on material requirements, inventory management practices, and alternative sourcing capabilities. Analysis of current dependencies reveals that strategic exposure extends far beyond traditional heavy industrial applications into consumer electronics, clean energy infrastructure, and advanced manufacturing systems.

Defence and Aerospace Manufacturing Exposure

Military applications consume relatively small volumes of rare earth materials but require extremely high-purity specifications that limit sourcing alternatives. Defence contractors typically maintain extended supply contracts with qualified suppliers, creating inflexibility when export restrictions emerge suddenly.

Critical Defence Applications:

- Radar and electronic warfare systems requiring high-purity yttrium compounds

- Precision-guided munition components utilising samarium-cobalt magnets

- Aircraft engine components incorporating rare earth superalloy additions

- Advanced optics and laser systems dependent on specialised rare earth crystals

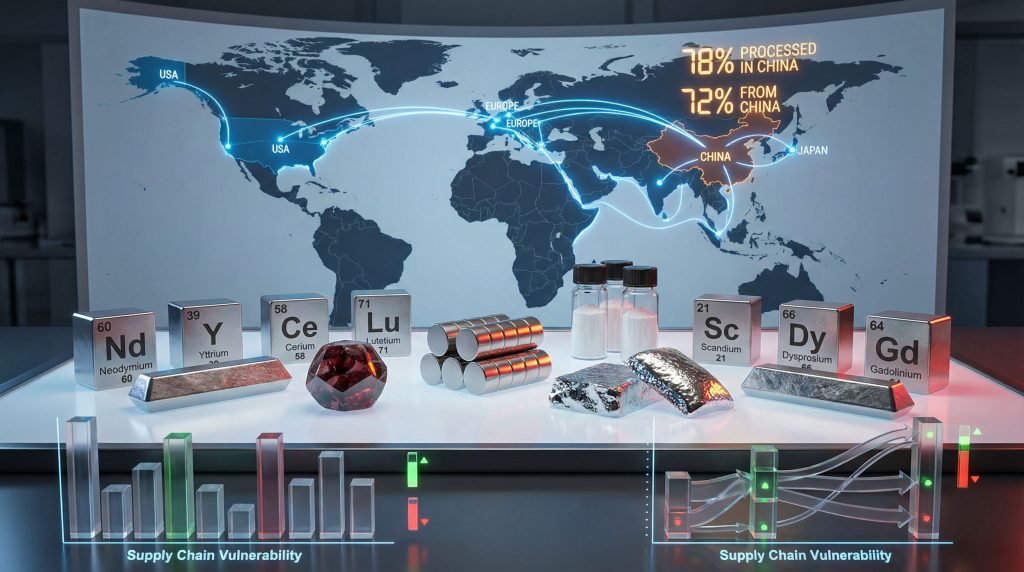

Japanese defence manufacturers exemplify these vulnerabilities. Despite sourcing 72% of rare earth imports from China as of 2024, alternative suppliers cannot immediately replace Chinese processing capacity for defence-grade materials. Moreover, lead times for qualifying new suppliers typically range from 18 to 36 months, creating extended exposure periods during which production continuity depends entirely on existing inventory levels.

Major Japanese magnet producers report operational sustainability of approximately two months if Chinese raw material supplies face interruption. This timeline reflects typical working inventory levels optimised for cost efficiency rather than supply security, demonstrating how manufacturing economics conflict with strategic resilience requirements.

Automotive and Electric Vehicle Production Risks

Electric vehicle manufacturing represents the fastest-growing consumer of rare earth permanent magnets, with each vehicle requiring approximately 1-3 kilograms of neodymium-iron-boron magnetic materials. Consequently, this consumption pattern creates concentrated demand among automotive manufacturers who previously had minimal rare earth exposure.

EV Supply Chain Dependencies:

- Traction motor assemblies requiring high-performance neodymium magnets

- Power electronics utilising rare earth-enhanced semiconductor materials

- Battery thermal management systems incorporating rare earth compounds

- Advanced driver assistance sensors dependent on rare earth-enabled components

Regional automotive manufacturing hubs face differentiated risk profiles based on local inventory practices and alternative sourcing infrastructure. Japanese automotive clusters maintain relatively low inventory levels due to just-in-time manufacturing philosophies, creating heightened vulnerability to supply interruptions. However, European automotive manufacturers typically maintain higher strategic inventory levels but lack comprehensive alternative sourcing arrangements outside Chinese supply chains.

The transition toward electric vehicles amplifies these dependencies rather than reducing them. Unlike internal combustion engines where rare earth applications remained limited to specialised components, electric drivetrains require rare earth materials as core functional elements that cannot be easily substituted without fundamental technology redesign.

Renewable Energy Infrastructure Dependencies

Wind turbine manufacturing consumes substantial quantities of heavy rare earth elements, particularly dysprosium and terbium, for permanent magnet generators operating in variable temperature and weather conditions. These applications require premium-grade materials that represent a small fraction of global rare earth production but command disproportionate strategic importance.

Wind Energy Vulnerabilities:

- Direct-drive generators utilising large permanent magnet assemblies

- Offshore installations requiring enhanced corrosion-resistant materials

- Grid-scale turbines incorporating advanced power electronics

- Energy storage systems dependent on rare earth-enhanced components

Solar panel manufacturing exhibits lower direct rare earth intensity but faces exposure through power electronics, inverter systems, and grid integration equipment. In addition, the renewable energy transition creates multiplicative demand growth across multiple rare earth applications simultaneously, compounding supply security challenges.

Grid-scale energy storage technologies increasingly utilise rare earth compounds for battery cathode materials, thermal management systems, and power conversion equipment. These applications typically require long-term supply contracts due to extended project development timelines, creating contractual exposure to supply disruptions spanning multiple years.

How Do Export Licensing Delays Create Market Disruption?

Administrative delays in export licensing create market disruption through uncertainty mechanisms that operate independently of actual supply constraints. The announcement of enhanced review procedures triggers precautionary behaviour among manufacturers, distributors, and financial markets that amplifies economic consequences beyond direct supply impacts.

The Economics of Supply Chain Uncertainty

Export licensing delays shift commercial relationships from predictable contract fulfilment toward contingent supply availability. This transformation requires manufacturers to restructure inventory management, financial planning, and production scheduling around uncertain material access rather than market-determined pricing and availability.

Uncertainty-Driven Market Behaviours:

- Precautionary inventory accumulation beyond optimal economic levels

- Premium pricing for confirmed near-term supply contracts

- Supply contract renegotiation to include force majeure provisions

- Alternative supplier qualification acceleration despite higher costs

Price volatility during licensing uncertainty periods typically exceeds volatility during confirmed supply restrictions. Markets respond to ambiguous regulatory signals by incorporating worst-case scenarios into pricing mechanisms, creating price appreciation that may reverse quickly if licensing approvals resume normal processing.

The psychological impact on procurement decision-making extends beyond immediate material requirements. Manufacturing executives report shifting strategic planning timelines from quarterly optimisation toward annual or multi-year supply security frameworks, fundamentally altering capital allocation and operational planning processes.

Processing Bottleneck Analysis

China's dominant position in rare earth processing creates concentrated bottlenecks that amplify export control effectiveness. Even when alternative mining sources exist, processing capabilities outside China remain insufficient to support global manufacturing demand without Chinese participation.

Global Processing Concentration:

- Separation and refining technologies concentrated in Chinese facilities

- Specialised processing equipment manufacturing controlled by Chinese suppliers

- Technical expertise and operational knowledge accumulated over decades

- Environmental and regulatory frameworks optimised for rare earth processing

Establishing alternative processing capabilities requires substantial capital investment, technological transfer, and regulatory development. Recent feasibility studies indicate capital requirements ranging from $200 million to $800 million for medium-scale integrated processing facilities, with construction timelines extending 3 to 7 years depending on environmental permitting and technology acquisition.

The technical barriers extend beyond financial investment to encompass specialised metallurgical knowledge, environmental management systems, and quality control capabilities that Chinese processors have refined through decades of operational experience. These knowledge-based advantages cannot be replicated quickly through capital investment alone.

Which Countries Are Most Exposed to Chinese Rare Earth Controls?

Import dependency analysis reveals significant variations in national vulnerability to Chinese rare earth export controls, based on industrial structure, strategic stockpiling, and alternative sourcing development. Advanced manufacturing economies generally exhibit higher exposure due to intensive rare earth utilisation across multiple industrial sectors.

| Country | Import Dependency | Key Vulnerable Industries | Strategic Response |

|---|---|---|---|

| Japan | 72% from China | Electronics, Automotive, Defence | Recycling expansion, ASEAN partnerships |

| Germany | 65% from China | Automotive, Industrial machinery | EU Critical Materials Act implementation |

| United States | 78% processed in China | Defence, Clean energy | Inflation Reduction Act incentives |

| South Korea | 85% from China | Electronics, Shipbuilding | Technology substitution research |

Regional Vulnerability Assessment

East Asian manufacturing economies face the highest immediate vulnerability due to geographic proximity, integrated supply chains, and limited strategic inventory maintenance. Japan's 72% import dependency persists despite more than a decade of diversification efforts initiated following the 2010 rare earth supply disruption.

South Korea exhibits even higher dependency levels, with an estimated 85% of rare earth imports originating from Chinese sources. The country's specialisation in electronics manufacturing, shipbuilding, and advanced materials creates concentrated exposure across multiple strategic industries simultaneously.

European Union economies face differentiated exposure based on industrial specialisation patterns. Germany's automotive and industrial machinery sectors create substantial rare earth demand, while EU-level strategic autonomy initiatives attempt to coordinate alternative sourcing development across member states.

Regional Response Strategies:

- East Asia: Bilateral partnerships with alternative suppliers, technology substitution research

- European Union: Coordinated strategic autonomy initiatives, Critical Raw Materials Act implementation

- North America: Friend-shoring partnerships, domestic processing capacity development

- Australia/Canada: Mining capacity expansion, processing infrastructure development

North American economies benefit from domestic mining potential and closer strategic coordination, but face significant processing bottlenecks that maintain dependency on Chinese refining capabilities. For instance, the United States sources approximately 78% of processed rare earths from Chinese facilities, even when mining occurs domestically or in allied countries.

What Alternative Supply Chain Strategies Are Emerging?

Manufacturing companies and governments are implementing diversified strategies to reduce Chinese rare earth dependency, though these approaches require substantial time, capital investment, and technological development to achieve meaningful supply security improvements.

Geographic Diversification Approaches

Alternative mining development focuses on deposits in allied or neutral countries that offer political stability and aligned strategic interests. Australian rare earth projects represent the most advanced alternative capacity, with several large-scale developments approaching commercial production phases.

Primary Alternative Sources:

- Australia: Multiple projects advancing toward commercial production with allied-country processing partnerships

- Africa: Nascent exploration programmes requiring substantial infrastructure and technology transfer

- Latin America: Early-stage exploration with limited near-term production potential

- North America: Domestic mining revival constrained by processing bottlenecks and environmental regulations

African rare earth deposits offer substantial long-term potential but require extensive infrastructure development, technology transfer, and institutional capacity building. However, Chinese companies maintain significant involvement in African rare earth exploration and development, complicating efforts to establish genuinely independent alternative supply chains.

Latin American countries possess identified rare earth deposits but lack processing infrastructure, technical expertise, and regulatory frameworks necessary for commercial development. These regions offer long-term diversification potential but require decades of sustained investment and institutional development.

Technology Substitution and Recycling Solutions

Permanent magnet recycling technologies offer near-term potential for reducing primary rare earth demand, particularly for neodymium and dysprosium applications in automotive and wind energy sectors. Current recycling operations remain economically marginal but benefit from policy incentives and supply security considerations.

Recycling Technology Development:

- Hydrogen-based magnet processing for rare earth element recovery

- Hydrometallurgical separation techniques adapted for recycled feedstocks

- Urban mining programmes targeting electronic waste and end-of-life products

- Closed-loop manufacturing systems reducing primary material requirements

Alternative material research focuses on developing rare earth-free technologies that maintain performance characteristics while eliminating supply chain vulnerabilities. These approaches typically require fundamental technology redesign rather than simple material substitution.

Substitution Research Areas:

- Ferrite-based motor technologies for lower-performance applications

- Advanced steel alloys for permanent magnet alternatives in specific uses

- Synthetic material development for electronics and catalytic applications

- Hybrid approaches combining reduced rare earth content with alternative materials

Strategic Stockpiling and Buffer Inventory Models

Government strategic reserves and private sector inventory optimisation represent immediate-term approaches to managing supply disruption risks. These strategies provide buffer capacity during supply interruptions but require substantial capital investment and ongoing management costs.

Strategic Reserve Frameworks:

- Government stockpiling: National emergency reserves for defence and critical infrastructure applications

- Private strategic inventory: Enhanced safety stock levels beyond normal operational requirements

- Cooperative reserves: Industry consortium stockpiling for shared supply security

- Allied coordination: International strategic reserve sharing agreements

The United States maintains strategic rare earth stockpiles through the Defense Logistics Agency, though current inventory levels remain insufficient for extended supply disruptions affecting civilian manufacturing. Industry estimates suggest optimal strategic minerals reserve would require 6 to 12 months of consumption coverage across critical applications.

Private sector inventory optimisation involves balancing carrying costs against supply security benefits. Companies report increasing safety stock levels from traditional 30-60 day coverage toward 90-180 day coverage for critical rare earth materials, despite significant working capital implications.

The next major ASX story will hit our subscribers first

How Do Geopolitical Tensions Amplify Supply Chain Risks?

Contemporary geopolitical competition transforms rare earth trade from commercial relationships into strategic leverage mechanisms. This evolution creates feedback loops where economic competition intensifies political tensions, which subsequently drive further economic decoupling and supply chain fragmentation.

Taiwan Strait Security Implications

Taiwan Strait tensions create multiplicative risks for rare earth supply chains due to geographic concentration, shipping route vulnerabilities, and potential conflict scenarios affecting both Chinese production and international logistics networks.

Conflict-Related Vulnerabilities:

- Shipping route disruptions affecting bulk rare earth transport

- Production facility damage or operational interruption in mainland China

- Financial system disruptions affecting trade finance and supply contracts

- Escalatory export controls targeting allied countries supporting Taiwan

Japanese Prime Minister Sanae Takaichi's statements regarding potential military intervention in Taiwan Strait conflicts triggered immediate Chinese export control responses in January 2026. This episode demonstrates how security rhetoric directly translates into supply chain actions, creating immediate economic consequences for diplomatic positions.

Cross-strait military tensions would likely disrupt rare earth logistics regardless of Chinese government policy choices. Major shipping routes between Chinese ports and East Asian manufacturing centres traverse areas that would face operational restrictions during military conflicts, creating supply interruptions independent of deliberate export controls.

Trade War Escalation Patterns

Historical analysis of the 2010 Japan-China rare earth dispute reveals escalation patterns that begin with administrative restrictions, progress through explicit export controls, and potentially culminate in comprehensive supply embargoes affecting entire economic sectors.

Escalation Timeline Patterns:

- Administrative delays: Extended licensing reviews and enhanced documentation requirements

- Selective restrictions: Targeting specific companies, applications, or end-uses

- Comprehensive controls: Industry-wide export limitations or quotas

- Complete embargoes: Total supply cutoffs affecting all commercial relationships

The 2010 precedent demonstrates that rare earth export controls can escalate rapidly from administrative inconvenience to existential threats for affected industries. Japanese manufacturers experienced production stoppages within weeks of initial export restrictions, despite maintaining inventory levels considered adequate for normal supply chain variability.

Furthermore, tit-for-tat restriction cycles create symmetric vulnerabilities where Chinese producers lose market share and revenue while importers face production disruptions and increased costs. These economic consequences often motivate negotiated settlements, though the underlying strategic competition typically remains unresolved.

What Investment Opportunities Emerge from Supply Chain Restructuring?

Supply chain diversification initiatives create substantial investment opportunities across mining development, processing infrastructure, recycling technologies, and alternative material development. These sectors benefit from both commercial demand growth and strategic policy support from governments seeking supply security.

Mining and Processing Infrastructure Development

Alternative rare earth mining projects require substantial capital investment but benefit from strategic partnerships, government incentives, and long-term supply contracts that reduce commercial risk compared to traditional mining investments.

Investment Categories and Capital Requirements:

- Mining development: $100-500 million per project depending on scale and complexity

- Processing facilities: $200-800 million for integrated separation and refining capabilities

- Infrastructure development: $50-200 million for transportation, power, and environmental systems

- Technology licensing: $10-50 million for processing technology and operational expertise

Australian rare earth projects attract international investment partnerships combining mining industry innovation, processing technology, and strategic market access. These ventures benefit from allied-country policy support, environmental and regulatory stability, and established mining industry infrastructure.

North American processing facility development faces higher regulatory and environmental compliance costs but benefits from substantial government incentive programmes. The U.S. Inflation Reduction Act provides significant tax credits and loan guarantees for critical mineral processing infrastructure development.

Recycling and Circular Economy Investments

Permanent magnet recycling technologies offer attractive investment returns due to material value recovery, policy incentives, and strategic supply security benefits. These ventures typically require lower capital investment than primary mining operations while providing faster development timelines.

Recycling Investment Opportunities:

- Technology development: Advanced separation and purification processes for recycled materials

- Collection networks: Electronic waste and end-of-life product gathering systems

- Processing facilities: Industrial-scale recycling plants for permanent magnet materials

- Urban mining: Comprehensive rare earth recovery from consumer electronics and industrial equipment

European recycling initiatives benefit from extended producer responsibility regulations, circular economy policy frameworks, and substantial research and development funding. These policy environments create favourable conditions for recycling technology commercialisation and market development.

Japanese recycling programmes focus on closed-loop manufacturing systems where electronic device manufacturers reclaim rare earth materials from their own products. These approaches reduce regulatory complexity while providing guaranteed feedstock sources for recycling operations.

Alternative Technology Development Funding

Rare earth-free technology development attracts venture capital, government research funding, and strategic corporate investment focused on eliminating supply chain vulnerabilities through fundamental technology innovation.

Technology Innovation Areas:

- Motor technologies: Advanced ferrite, switched reluctance, and hybrid magnetic systems

- Material sciences: Synthetic alternatives to rare earth compounds in electronics and catalysts

- Manufacturing processes: Reduced rare earth content through improved efficiency and design optimisation

- System redesign: Product architectures that minimise or eliminate rare earth requirements

Government research and development programmes provide substantial funding for alternative technology development, with the United States, European Union, and Japan allocating billions of dollars annually for critical material independence initiatives.

Corporate strategic investment focuses on technologies that provide competitive advantages while reducing supply chain vulnerabilities. Automotive manufacturers increasingly invest in rare earth-free motor technologies that offer both cost reduction and supply security benefits.

Frequently Asked Questions About Rare Earth Export Controls

Understanding the practical implications of export controls requires addressing common questions about licensing procedures, dependency reduction possibilities, and policy response options. These issues affect strategic planning for manufacturers, investors, and policymakers navigating rare earth supply security challenges.

How Long Do Chinese Export License Reviews Take?

Standard export licensing procedures for dual-use rare earth materials typically require 30 to 90 days for initial review, though complex applications involving sensitive end-uses or technologies may extend beyond six months. Expedited review procedures exist for established commercial relationships and routine applications, reducing timelines to 10 to 30 days under normal circumstances.

Factors Influencing Approval Timelines:

- End-use application classification and sensitivity assessment

- Purchasing entity qualifications and previous compliance history

- Destination country relationships and bilateral trade status

- Material specifications and potential dual-use applications

During periods of heightened scrutiny or geopolitical tensions, review timelines extend significantly as additional security assessments and inter-agency coordination requirements activate. The January 2026 enhanced controls affecting Japan demonstrate how administrative processes can create supply uncertainty even before formal restrictions take effect.

Appeal processes for denied applications typically require 90 to 180 days and involve senior Ministry of Commerce officials with discretionary approval authority. These procedures rarely result in approval reversals unless underlying security concerns change substantially.

Can Countries Completely Eliminate Chinese Rare Earth Dependence?

Complete elimination of Chinese rare earth dependency appears technically feasible but economically prohibitive and operationally complex for most importing economies. Alternative sourcing requires simultaneous development of mining capacity, processing infrastructure, technology transfer, and regulatory frameworks across multiple countries and industrial sectors.

Independence Requirements:

- Alternative mining development: 5 to 15 years for commercial production

- Processing infrastructure: 3 to 7 years for facility construction and commissioning

- Technology transfer: 2 to 5 years for operational expertise development

- Strategic reserves: 1 to 3 years for adequate stockpiling coverage

Total capital requirements for achieving supply independence likely exceed $50 to 100 billion globally across mining, processing, and technology development. These investments require sustained government support, international coordination, and private sector participation over extended timeframes.

Partial dependency reduction represents a more realistic near-term objective, reducing Chinese supply reliance from current levels of 70-85% for most countries toward 40-50% dependency within 10 to 15 years through diversified sourcing strategies.

What Happens During Temporary Control Suspensions?

Temporary suspension of export controls typically triggers accelerated procurement activity as manufacturers attempt to rebuild inventory levels and secure longer-term supply contracts. These periods create market volatility as accumulated demand meets restored supply availability.

Market Behaviour Patterns:

- Procurement surge: Accelerated ordering to rebuild depleted inventory levels

- Price volatility: Temporary price spikes from concentrated demand followed by normalisation

- Contract renegotiation: Updated supply agreements incorporating force majeure and alternative sourcing provisions

- Strategic planning revision: Enhanced contingency planning and alternative sourcing development

Historical precedent from the resolution of the 2010 Japan-China dispute demonstrates that temporary suspensions create false confidence if underlying strategic tensions remain unresolved. Manufacturers who failed to diversify supply chains during suspension periods faced renewed vulnerability when export controls resumed.

Long-term planning implications emphasise supply chain resilience over cost optimisation during suspension periods. Companies report using temporary control suspensions to accelerate alternative sourcing qualification, increase strategic inventory levels, and develop technological substitution capabilities.

Long-Term Implications for Global Manufacturing Competitiveness

The integration of rare earth supply chains with geopolitical competition fundamentally alters global manufacturing location decisions, technology development priorities, and industrial policy frameworks. This transformation extends beyond immediate supply security concerns to reshape comparative advantages across economic regions and industrial sectors.

Reshoring and Friend-Shoring Acceleration

Manufacturing location decisions increasingly incorporate supply chain resilience factors alongside traditional cost optimisation criteria. The integration of strategic supply security considerations into location analysis modifies the competitive landscape for industrial development across different regions and policy environments.

Location Decision Factors:

- Supply chain proximity: Reduced transportation costs and supply interruption risks

- Allied-country sourcing: Political stability and aligned strategic interests

- Strategic stockpiling: Government reserve access and emergency supply protocols

- Technology autonomy: Domestic or allied processing capabilities and technical expertise

Regional manufacturing hub development benefits from coordinated industrial policies that address supply chain vulnerabilities through targeted incentives, infrastructure development, and strategic partnerships. The European Union's Critical Raw Materials Act and United States Inflation Reduction Act exemplify policy frameworks designed to attract manufacturing investment through supply security enhancement.

Trade-offs between efficiency and resilience create permanent increases in manufacturing costs as companies maintain higher inventory levels, develop alternative sourcing relationships, and invest in backup production capabilities. Industry estimates suggest resilience-focused supply chains require 10 to 30% higher operating costs compared to efficiency-optimised alternatives.

Technology Innovation Drivers

Strategic competition in critical materials accelerates research and development investment in alternative technologies, recycling processes, and substitution materials. This innovation pressure creates opportunities for breakthrough technologies while driving systematic improvements in resource efficiency and material utilisation.

Innovation Investment Areas:

- Alternative materials research: Development of rare earth-free technologies with comparable performance

- Recycling technology advancement: Enhanced recovery rates and reduced processing costs for recycled materials

- Efficiency optimisation: Reduced rare earth content through improved design and manufacturing processes

- Substitution technologies: Fundamental technology redesign eliminating rare earth dependencies

Patent landscape analysis reveals accelerating investment in rare earth alternatives across multiple technology domains. United States, European, and Japanese companies significantly increased patent filings for rare earth-free technologies following supply disruptions and export control implementations.

Collaborative research initiatives between allied nations pool resources and expertise to accelerate technology development while sharing costs and risks. International research partnerships increasingly focus on critical minerals energy security as a shared strategic objective rather than competitive advantage.

The comprehensive approach to addressing supply chain vulnerabilities requires coordination across multiple policy domains, from critical minerals strategy development to international cooperation frameworks. This reflects broader recognition that resource security determines technological competitiveness in an increasingly competitive global environment.

Furthermore, the evolution of China tightens rare earth export controls demonstrates how export restrictions become integrated with broader geopolitical strategies. Understanding this relationship enables better policy responses that balance short-term supply security with long-term competitive positioning.

The complexity of these challenges extends beyond individual company strategies to encompass international cooperation mechanisms that address shared vulnerabilities. Recent developments in China export control strategy illustrate how these policies continue evolving in response to changing geopolitical dynamics.

Strategic Consideration: China's approach to rare earth export controls represents a fundamental transformation from market-driven supply allocation toward strategically motivated resource distribution. This evolution forces global manufacturers to integrate supply security considerations into every major business decision, fundamentally altering the relationship between cost optimisation and operational continuity in strategic planning processes.

The long-term implications extend beyond immediate supply chain management to encompass technology development priorities, manufacturing location decisions, and international economic relationships. As geopolitical competition intensifies, rare earth supply chains serve as both economic assets and strategic weapons, requiring manufacturers to balance market efficiency against supply security in an increasingly uncertain global environment.

The need for coordinated responses across allied nations has been highlighted by recent developments, as reported by Reuters on Japan's rare earth mining initiatives, while the International Energy Agency emphasises how supply concentration risks become reality through export controls. These developments underscore the importance of developing comprehensive strategies that address both immediate vulnerabilities and long-term technological autonomy.

Disclaimer: This analysis incorporates publicly available information and industry observations current as of early 2026. Rare earth market conditions, export control policies, and geopolitical relationships evolve rapidly. Readers should verify specific claims through current government sources, industry publications, and specialised consulting reports when making strategic decisions. Investment and supply chain strategies should incorporate professional consultation and due diligence appropriate to specific circumstances and risk tolerance.

Ready to Navigate Critical Minerals Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications when significant ASX mineral discoveries emerge, helping investors identify opportunities in alternative supply chain companies ahead of broader market awareness. Explore why major mineral discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, then start your 30-day free trial to position yourself ahead of supply chain disruption trends shaping global markets.