May 22, 2026

Understanding Global Sulphur Supply Dynamics in Modern Energy Markets

The global energy sector operates within increasingly complex commodity interdependencies where petroleum refining byproducts have evolved into critical industrial inputs. Sulphur, traditionally viewed as a waste product from natural gas processing and oil refining, now functions as a cornerstone material for agricultural fertilizer production, industrial chemical manufacturing, and metallurgical processes. This transformation reflects broader shifts in commodity trading trends where integrated energy companies leverage vertical supply chains to establish pricing power across multiple sectors.

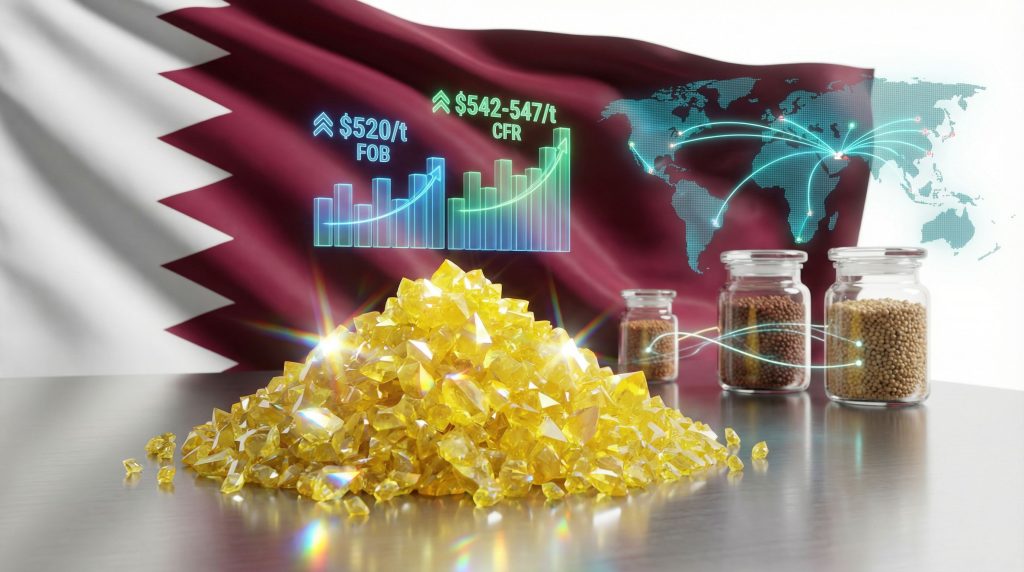

QatarEnergy's strategic positioning exemplifies this evolution, as the state-controlled entity utilizes its massive natural gas reserves and refining infrastructure to influence global sulphur pricing benchmarks. The company's February 2026 QatarEnergy sulphur price increase to $520 per tonne FOB represents sophisticated market management within volatile commodity cycles, affecting downstream industries from Chinese fertilizer manufacturers to European chemical processors.

When big ASX news breaks, our subscribers know first

Qatar's Strategic Position in Global Sulphur Markets

Qatar's emergence as a sulphur pricing benchmark reflects fundamental shifts in global energy production patterns. The country's vast natural gas reserves, primarily from the North Field development, generate substantial sulphur volumes as a byproduct of hydrogen sulfide removal during gas processing. This positioning creates unique market leverage, as QatarEnergy can coordinate sulphur sales with broader energy portfolio management strategies.

The Qatar Sulphur Price (QSP) mechanism operates as more than a simple commodity pricing tool. It functions as a strategic instrument for managing relationships with key importing regions, particularly Asia-Pacific markets where agricultural demand drives sulphur consumption patterns. Furthermore, the monthly pricing announcements incorporate sophisticated analysis of freight rate fluctuations, regional demand elasticity, and competitive positioning against other Gulf Cooperation Council (GCC) producers including Saudi Aramco and Kuwait Petroleum Corporation.

Regional Supply Chain Integration

QatarEnergy's sulphur operations benefit from integrated infrastructure connecting gas processing facilities at Ras Laffan and Mesaieed with specialized port terminals designed for bulk commodity handling. This integration enables flexible delivery scheduling that responds to seasonal agricultural cycles across major consuming regions.

Key infrastructure advantages include:

• Advanced storage facilities capable of handling 300,000+ tonnes of sulphur inventory

• Dedicated loading terminals optimized for 30,000-50,000 tonne bulk carriers

• Quality control systems ensuring consistent product specifications for industrial applications

• Logistics coordination with major shipping lines serving Asia-Pacific routes

The February pricing adjustment reflects current freight rate pressures, with shipping costs of $22-24 per tonne to South China ports creating delivered pricing of $542-547 per tonne CFR. These logistics costs represent approximately 4-5% of total delivered pricing, indicating the importance of transportation efficiency in global sulphur trade competitiveness.

Regional Economic Impact Assessment: Asia-Pacific Focus

China Market Dynamics

China's position as the world's largest fertilizer producer creates significant exposure to sulphur price volatility. The delivered pricing implications of the QatarEnergy sulphur price increase directly affect production economics across multiple fertilizer categories, with phosphate-based products experiencing the most immediate impact.

Fertilizer Production Cost Analysis:

| Product Category | Sulphur Content | Cost Impact per $10/t Sulphur Increase |

|---|---|---|

| Single Superphosphate (SSP) | 12-15% | $1.20-1.50/t |

| Diammonium Phosphate (DAP) | 8-10% | $0.80-1.00/t |

| Triple Superphosphate (TSP) | 6-8% | $0.60-0.80/t |

Chinese manufacturers face additional pressure from domestic environmental regulations limiting sulphur dioxide emissions from industrial processes. This regulatory framework increases reliance on imported sulphur for sulphuric acid production, consequently reducing flexibility to substitute lower-quality domestic sources during price spikes.

The concentration of China's fertilizer manufacturing in coastal provinces creates geographic vulnerability to shipping disruptions and freight rate volatility. Major production hubs in Shandong, Jiangsu, and Guangdong provinces depend on efficient port infrastructure to receive imported sulphur, making supply chain optimization critical for maintaining competitiveness.

Southeast Asian Agricultural Economics

Southeast Asian agricultural economies demonstrate particular sensitivity to sulphur pricing fluctuations due to intensive cultivation practices requiring substantial fertilizer inputs. Rice production across Vietnam, Thailand, and Indonesia relies heavily on phosphate-based fertilizers for maintaining soil nutrient balance in tropical growing conditions.

Regional Agricultural Impact Metrics:

• Vietnam: 8.2 million hectares of agricultural land requiring 450,000 tonnes annual sulphur equivalent

• Thailand: 6.8 million hectares with 380,000 tonnes sulphur demand from fertilizer applications

• Indonesia: 47.3 million hectares supporting 850,000 tonnes sulphur-based fertilizer consumption

The QatarEnergy sulphur price increase creates cascading effects through these agricultural systems, potentially influencing crop selection decisions and fertilizer application timing. Smallholder farmers, who comprise 60-70% of agricultural producers in these regions, possess limited financial flexibility to absorb input cost increases without affecting production levels.

Government subsidy programs in these countries face mounting pressure to offset fertilizer cost inflation. Indonesia's fertilizer subsidy program, budgeted at approximately $3.2 billion annually, requires constant adjustment to maintain farmer access to essential nutrients while managing fiscal constraints.

Industrial Sector Ramifications

European Chemical Industry Stress Points

The closure of Germany's Kelheim Fibres facility exemplifies broader structural challenges facing European industrial sulphur consumers. The company's annual consumption of 15,000-20,000 tonnes of sulphur for viscose fiber production became economically unviable due to accumulated cost pressures from multiple sources.

European Industrial Cost Structure Analysis:

| Cost Component | 2023 Baseline | 2026 Current Level | Percentage Increase |

|---|---|---|---|

| Electricity Costs | €85/MWh | €145/MWh | +71% |

| Natural Gas Prices | €28/MWh | €52/MWh | +86% |

| Sulphur Import Costs | $420/t CFR | $565/t CFR | +35% |

| Labor Costs | €38,500/year | €41,200/year | +7% |

These accumulated pressures create a cost competitiveness gap of 25-30% compared to Asian and Middle Eastern producers operating with lower energy costs and integrated supply chains. European manufacturers face strategic decisions regarding facility rationalisation, technology investment, or geographic relocation to maintain viability.

The Bayernoil Vohburg-Neustadt refinery, which supplied Kelheim Fibres with sulphur, exemplifies the interconnected nature of European industrial ecosystems. The refinery's 97,000 tonnes annual sulphur capacity must now seek alternative customers or consider export marketing to distant markets, potentially affecting regional pricing dynamics.

Chemical Process Integration Challenges

Industrial sulphur consumption extends beyond fertilizer applications into critical chemical processes including:

Sulphuric Acid Production for Metallurgy:

- Copper ore processing requiring 3-4 tonnes sulphuric acid per tonne refined copper

- Zinc processing utilising 2-3 tonnes sulphuric acid per tonne metal production

- Rare earth element extraction consuming 8-12 tonnes sulphuric acid per tonne concentrate

Pharmaceutical Intermediate Manufacturing:

- Active pharmaceutical ingredient synthesis requiring high-purity sulphuric acid

- Antibiotic production processes utilising sulphur-containing compounds

- Vaccine manufacturing employing sulphur-based stabilising agents

The QatarEnergy sulphur price increase affects these sectors through cost transmission mechanisms that vary by industry structure and competitive positioning. However, pharmaceutical manufacturers typically possess greater pricing power to pass through input costs, while commodity chemical producers face more rigid price discovery mechanisms.

Investment Market Implications

Commodity Trading Strategy Evolution

Professional commodity traders must recalibrate portfolio strategies around evolving sulphur market dynamics, particularly given the increasing correlation between energy commodity cycles and agricultural input costs. The traditional approach of treating sulphur as a simple petroleum byproduct requires updating to reflect its strategic importance in food production systems.

Trading Strategy Adaptations:

• Enhanced hedging complexity requiring correlation analysis between crude oil, natural gas, and sulphur pricing

• Geographic arbitrage optimisation exploiting price differentials between Middle Eastern, North American, and European markets

• Seasonal positioning aligning inventory strategies with global agricultural planting cycles

• Quality spread management capturing premiums for high-purity industrial grades versus agricultural specifications

The contango structure in sulphur futures markets creates opportunities for storage-based trading strategies, particularly given the product's stability and relatively low storage costs. Professional traders increasingly utilise sulphur positions as portfolio diversification tools within broader agricultural commodity exposure.

Furthermore, understanding oil price movements becomes crucial as they directly influence refinery operations and sulphur production rates. Additionally, how tariffs impact markets affects international sulphur trading patterns and pricing mechanisms.

Equity Market Sector Analysis

Sustained elevation in sulphur pricing creates investment opportunities across multiple equity sectors, particularly companies developing input-efficient agricultural technologies and alternative fertilizer production methods.

Investment Theme Development:

-

Precision Agriculture Technology Companies

- Variable rate fertilizer application systems reducing input requirements by 15-25%

- Soil sensing technologies optimising nutrient timing and placement

- Drone-based crop monitoring enabling targeted fertilizer interventions

-

Alternative Fertilizer Producers

- Biological nitrogen fixation companies reducing synthetic fertilizer dependency

- Organic waste processing facilities converting municipal waste to fertilizer products

- Algae-based nutrient producers offering sustainable phosphorus alternatives

-

Supply Chain Optimisation Providers

- Logistics technology companies reducing fertilizer transportation costs

- Inventory management systems optimising fertilizer storage and distribution

- Blockchain platforms enhancing fertilizer supply chain transparency

Institutional investors increasingly recognise sulphur price volatility as a key variable affecting agricultural productivity and food security outcomes. In addition, ESG-focused investment strategies incorporate fertilizer input costs as material factors influencing sustainable agriculture transition pathways.

Forward-Looking Market Structure Analysis

Technology-Driven Supply Side Transformation

The current sulphur pricing environment accelerates investment in alternative production technologies and enhanced recovery methods at existing facilities. Moreover, refineries worldwide reassess sulphur recovery optimisation as the commodity transitions from waste management challenge to revenue opportunity.

Emerging Technology Applications:

• Advanced Claus process modifications increasing sulphur recovery rates from 95% to 98-99%

• Tailgas treatment upgrades capturing previously vented sulphur compounds

• Pyrite processing development utilising iron sulfide minerals as alternative sulphur sources

• Gypsum decomposition technologies converting calcium sulfate waste into elemental sulphur

Regional production capacity expansion focuses on areas with both energy infrastructure and proximity to agricultural markets. West Africa, particularly Nigeria and Angola, represents a growth frontier given substantial natural gas reserves and developing agricultural sectors requiring increased fertilizer application.

The Lobito Atlantic Railway project in Angola exemplifies infrastructure development supporting sulphur trade expansion. For instance, the recent delivery of 50,000 tonnes of bulk sulphur via the port of Lobito for copper belt applications demonstrates growing trade route development connecting Middle Eastern suppliers with African industrial consumers.

Demand Side Evolution Scenarios

Agricultural demand for sulphur-based fertilizers faces transformation pressure from multiple technological and regulatory developments. Climate change adaptation strategies increasingly emphasise soil health improvement and nutrient use efficiency rather than maximising application rates.

Precision Agriculture Impact Modelling:

| Technology Category | Adoption Timeline | Sulphur Demand Reduction Potential |

|---|---|---|

| Variable Rate Application | 2026-2030 | 12-18% efficiency gain |

| Enhanced Efficiency Fertilizers | 2027-2032 | 20-25% application reduction |

| Biological Nutrient Enhancement | 2029-2035 | 15-30% synthetic replacement |

Regulatory frameworks supporting sustainable agriculture practices create incentives for reduced synthetic fertilizer dependency. The European Union's Farm to Fork strategy targets 20% reduction in fertilizer use by 2030, whilst maintaining agricultural productivity through technology adoption and soil health improvement.

Carbon credit mechanisms increasingly recognise soil carbon sequestration benefits from optimised fertilizer management. This creates economic incentives for farmers to adopt precision application technologies that simultaneously reduce input costs and generate environmental credits.

The next major ASX story will hit our subscribers first

Risk Assessment Framework for Market Participants

Systematic Risk Identification

Market participants face multifaceted risk exposure from sulphur price volatility, requiring comprehensive assessment frameworks that account for interconnected commodity cycles and geopolitical factors affecting supply chain stability. Understanding mining industry evolution becomes particularly relevant as mining operations increasingly depend on sulphur-based acid for ore processing.

Primary Risk Categories:

-

Supply Disruption Risks

- Geopolitical tensions affecting Middle Eastern production facilities

- Natural gas price volatility influencing refinery sulphur output decisions

- Shipping disruptions impacting bulk commodity transportation routes

- Environmental regulations constraining sulphur recovery operations

-

Demand Destruction Scenarios

- Agricultural recession reducing fertilizer consumption

- Technology adoption accelerating beyond current projections

- Government subsidy programme reductions affecting farmer purchasing power

- Alternative crop varieties requiring reduced fertilizer inputs

-

Financial Market Integration Risks

- Correlation increases between energy and agricultural commodity cycles

- Currency volatility affecting international trade pricing mechanisms

- Interest rate changes influencing inventory financing costs

- Derivative market liquidity constraints during volatility periods

Mitigation Strategy Development

Effective risk management requires diversified approaches addressing both operational and financial exposure to sulphur price volatility. Companies develop multi-layered strategies combining physical supply security with financial hedging mechanisms.

Operational Risk Management:

• Supply source diversification reducing dependence on single geographic regions

• Inventory optimisation balancing carrying costs with price volatility protection

• Technology investment improving process efficiency and input utilisation rates

• Customer relationship development enabling collaborative demand planning and risk sharing

Financial Risk Management:

• Forward contract utilisation securing predictable input costs for production planning

• Option strategy implementation providing price protection while maintaining upside flexibility

• Cross-commodity hedging exploiting correlations between sulphur, energy, and agricultural prices

• Insurance product development covering supply disruption and price volatility scenarios

Consequently, proper investment risk management becomes essential for companies exposed to commodity price volatility. For additional insights into sulphur pricing mechanisms, Argus Media provides comprehensive market analysis on recent pricing developments. Furthermore, World Fertilizer magazine offers detailed coverage of global sulphur market trends affecting the fertilizer industry.

The evolution of sulphur markets from byproduct disposal to strategic commodity management reflects broader transformation in global commodity systems. QatarEnergy's pricing decisions serve as market signals influencing investment allocation, technology development, and policy formation across interconnected agricultural and industrial sectors.

Market participants who develop sophisticated understanding of these dynamics and implement comprehensive risk management frameworks position themselves to capture opportunities while navigating increasing volatility in global commodity markets.

Looking for Your Next Commodity Investment Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, transforming complex market data into actionable investment insights for both seasoned traders and emerging investors. Explore how major mineral discoveries can generate exceptional returns whilst securing your competitive advantage with a 14-day free trial today.