June 7, 2026

Understanding Global Supply Chain Vulnerabilities in the Critical Minerals Sector

The modern economy's dependence on a narrow range of materials has created unprecedented vulnerability patterns that threaten industrial stability across multiple sectors. Critical minerals, essential for everything from defense systems to consumer electronics, represent potential chokepoints in global supply chains that could disrupt entire industries. The recent US-UK critical minerals agreement demonstrates how nations are addressing these dependencies through strategic partnerships. These dependencies have evolved beyond simple commodity trading relationships into complex webs of geopolitical leverage and strategic control.

Current supply chain architectures concentrate production in limited geographic regions, creating systemic risks that extend far beyond typical market volatility. When examining mineral extraction patterns globally, the concentration becomes apparent: certain countries control not just primary production but also processing capabilities, creating multiple dependency layers that compound vulnerability. This concentration effect means disruptions at any single point can cascade through entire industrial ecosystems.

The challenge extends beyond mere availability to encompass pricing control, quality standards, and technological access. Nations controlling critical mineral supplies possess leverage over importing countries that transcends traditional economic relationships, entering the realm of strategic influence and national security considerations.

When big ASX news breaks, our subscribers know first

Economic Vulnerability Assessment Through Risk Diversification Models

Strategic planners increasingly recognise that single-source dependencies represent unacceptable risk profiles for national economies. The 60% diversification threshold emerging in policy frameworks represents a calculated approach to risk mitigation, where no single external source controls more than three-fifths of any critical mineral supply. This threshold balances economic efficiency with security considerations, acknowledging that complete autarky remains economically unfeasible for most minerals.

Recent analysis indicates that achieving this diversification target requires systematic investment in alternative supply sources, including domestic extraction capabilities and processing infrastructure. Furthermore, the challenge involves creating viable economic alternatives to existing supply relationships while maintaining cost competitiveness in global markets.

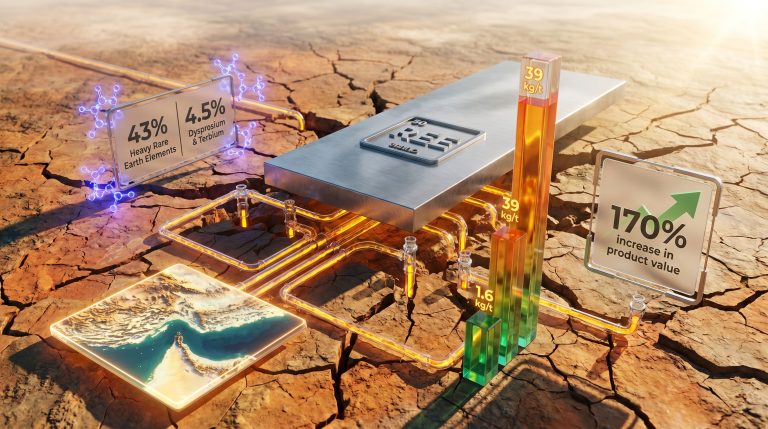

Defence industry implications demonstrate the most acute vulnerabilities, as advanced weapons systems require specific mineral compositions that often depend on single-source suppliers. Semiconductor manufacturing, aerospace applications, and precision guidance systems all rely on materials with limited geographic distribution, creating potential national security risks during geopolitical tensions. These vulnerabilities highlight growing energy security trends that influence global supply chain planning.

Investment Flows Responding to Supply Chain Security Concerns

Capital allocation patterns in mining and mineral processing sectors reflect growing awareness of supply chain vulnerabilities. Traditional investment criteria focused primarily on geological potential, operational costs, and commodity price projections. Contemporary investment frameworks increasingly incorporate geopolitical risk assessments, supply chain security premiums, and strategic value considerations that extend beyond pure financial returns.

Government backing mechanisms now influence private capital decisions through risk reduction strategies. When authorities provide regulatory streamlining, permitting acceleration, or investment guarantees, they effectively reduce the risk-adjusted returns required by private investors. This government involvement transforms project economics by lowering capital costs and reducing development timelines.

The UK mining sector, currently contributing £1.79 billion to the economy and supporting over 50,000 jobs, represents the scale of economic activity that strategic mineral policies can influence. With more than 50 active projects focused on extracting and refining vital materials, the sector demonstrates significant domestic capacity potential that policy coordination can unlock. These developments showcase lithium industry innovations that support strategic objectives.

Permitting streamlining represents a critical mechanism for accelerating project development timelines. Traditional mining project development cycles often extend 7-10 years from initial exploration to production, with regulatory approval processes consuming substantial portions of this timeline. Coordinated policy approaches can potentially reduce these development periods to 3-5 years, fundamentally altering project economics and investment attractiveness. Understanding the mining permitting process becomes crucial for investors navigating this landscape.

Market Concentration Dynamics and Alternative Supply Development

China's position in critical mineral markets extends beyond primary production to encompass processing and refining capabilities that create multiple dependency layers. Even minerals extracted elsewhere often require Chinese processing facilities, meaning supply diversification requires developing both mining and processing capabilities in alternative locations.

This processing dominance creates pricing power that extends beyond simple supply and demand fundamentals. Control over refining and separation technologies enables manipulation of global pricing through capacity utilization decisions, export restrictions, or quality standards that favour certain end users over others.

Strategic stockpiling policies further complicate market dynamics by allowing dominant suppliers to influence timing of supply releases. Consequently, these practices create artificial scarcity or flood markets to discourage investment in alternative sources. These practices represent non-market behaviours that traditional economic models struggle to predict or counter.

Understanding these dynamics requires recognition that critical mineral markets often function more like strategic resources than traditional commodities. Price discovery mechanisms become distorted when state actors prioritise geopolitical objectives over pure economic optimisation, creating market conditions that challenge conventional investment analysis. These factors demonstrate broader investment market impacts affecting global supply chains.

Industry-Specific Supply Chain Requirements and Vulnerabilities

Automotive Sector Battery Metal Dependencies

Electric vehicle production scaling creates unprecedented demand patterns for specific minerals essential to battery manufacturing. A typical EV lithium-ion battery with 60 kWh capacity requires approximately 8-10 kg of lithium, 8-10 kg of cobalt, and 15-20 kg of nickel. These quantities, multiplied across millions of projected annual EV production units, create demand volumes that dwarf historical consumption patterns.

Lithium demand projections suggest 15-fold increases by 2035 under clean energy transition scenarios, rising from approximately 1.4 million tonnes lithium carbonate equivalent in 2023. Cobalt requirements could triple from 200,000 tonnes to 600,000+ tonnes by 2030, while nickel faces similar upward pressure from battery applications competing with traditional stainless steel demand.

Manufacturing reshoring considerations for automotive applications involve complex cost-benefit calculations. Domestic battery production provides supply security benefits but typically involves higher labour and regulatory costs compared to existing Asian manufacturing hubs. OEMs must balance these security premiums against competitive pricing requirements in consumer markets.

Supply chain mapping from mine to battery pack assembly reveals multiple vulnerability points where disruption can halt production. Beyond raw material extraction, intermediate processing, chemical conversion, and component manufacturing all represent potential chokepoints that require geographic diversification to ensure reliability.

Clean Energy Infrastructure Mineral Requirements

Wind turbine manufacturing demands specific rare earth elements for permanent magnet generators, particularly neodymium and dysprosium. A typical 3 MW wind turbine requires approximately 600 kg of rare earth materials, with larger offshore installations requiring proportionally more. Solar panel production, while less rare earth intensive, depends on silver, tellurium, and other materials with concentrated supply chains.

Grid storage technology mineral intensity varies significantly by technology type. Lithium-ion storage systems require the same materials as EV batteries, while alternative technologies like vanadium redox flow batteries create demand for different mineral sets. Energy storage deployment targets suggest material requirements that could compete directly with automotive applications for limited supplies.

Energy transition timeline alignment with supply security goals presents coordination challenges. In addition, renewable energy deployment schedules often assume material availability without accounting for supply development lead times or potential bottlenecks. This misalignment creates risks that energy transition goals could be delayed by mineral supply constraints.

Implementation Frameworks and Policy Coordination Mechanisms

International mineral agreements require sophisticated coordination mechanisms that extend beyond diplomatic signatures to operational implementation. The US-UK critical minerals agreement represents a framework where economic policy tool alignment between different national systems involves harmonising investment review processes, regulatory standards, and strategic objective definitions while respecting sovereignty principles. The British government's announcement highlights the partnership's comprehensive approach to supply chain security.

Investment review processes for national security considerations typically evaluate proposed foreign investments in strategically significant assets. Coordinated approaches enable allied nations to share information about potential buyers and coordinate responses to acquisition attempts that might compromise mineral supply security.

Asset sale oversight represents another critical coordination area, where nations can jointly protect strategic mineral assets from acquisition by potentially hostile actors. This involves creating frameworks for evaluating proposed transactions based on cumulative strategic impact rather than individual deal assessments. These mechanisms help address trade war impacts on strategic supply chains.

| Implementation Phase | Timeframe | Key Activities |

|---|---|---|

| Immediate Coordination | Q1-Q2 2026 | Investment review process alignment |

| Regulatory Harmonisation | 12-18 months | Permitting streamlining implementation |

| Capacity Development | 3-4 years | Domestic refining infrastructure expansion |

| Strategic Independence | 5-9 years | 60% single-country dependency cap achievement |

Timeline analysis reveals the extended nature of mineral supply chain transformation. Unlike financial markets that can adjust rapidly to new conditions, mining and processing infrastructure development requires sustained commitment over multiple economic cycles to achieve strategic objectives.

Comparative Analysis of International Critical Mineral Partnerships

The expanding network of bilateral and multilateral critical mineral agreements reflects growing recognition that supply chain security requires coordinated action among like-minded nations. Australia and Canada represent particularly valuable partners due to their significant mineral endowments and established mining industries, creating resource complementarity that strengthens collective supply security.

Trade bloc formation potential emerges when multiple resource-rich allied nations coordinate policies to create preferential access arrangements. These frameworks can include preferential pricing mechanisms, priority allocation during supply shortages, or coordinated export policies that favour alliance members over non-allied purchasers. The Politico report on the UK-US deal emphasises the strategic timing of this partnership.

Competitive positioning against alternative supply networks becomes crucial when multiple blocs compete for market influence. China's Belt and Road Initiative mineral investments create alternative supply relationships that compete directly with Western alliance frameworks, requiring strategic responses that combine economic attractiveness with security benefits.

Success metrics for partnership effectiveness require measurable indicators that track progress toward strategic objectives. Supply chain resilience indicators might include response time to supply disruptions, alternative source activation capabilities, and price stability measurements across different market stress scenarios.

However, price stability measurements become particularly important when evaluating whether diversification efforts successfully reduce volatility. Traditional commodity markets exhibit cyclical price patterns, but strategic mineral markets may experience additional volatility from geopolitical events that pure economic analysis cannot predict.

The next major ASX story will hit our subscribers first

Challenge Assessment and Risk Factor Analysis

Implementation Obstacles and Regulatory Complexities

Regulatory harmonisation between different national systems presents significant technical challenges that extend beyond political agreements. Legal frameworks, environmental standards, and administrative procedures evolved independently in different countries, creating compatibility issues that require substantial coordination efforts to resolve.

Industry resistance to higher-cost domestic alternatives represents a predictable market response that policy makers must anticipate and address. Companies optimising for cost efficiency may resist supply chain changes that increase input costs, requiring policy incentives or requirements to overcome pure market-driven decision making.

Timeline pressures between 2035 diversification targets and realistic project development schedules create potential policy-implementation gaps. Mining projects typically require 7-10 years from exploration to production, meaning projects initiated today may not contribute to supply diversification until the early 2030s, creating a narrow window for achieving stated objectives.

Market Response Scenarios and Unintended Consequences

Price inflation risks from supply chain restructuring represent significant concerns for end-user industries and consumers. Diversification efforts may increase costs if alternative suppliers operate at higher cost structures than incumbent sources, creating inflationary pressure that policy makers must balance against security objectives.

Retaliation concerns arise when dominant suppliers perceive diversification efforts as threats to their market positions. Export restrictions, quality standard changes, or pricing manipulation represent potential responses that could accelerate supply chain disruptions rather than preventing them.

Technology transfer implications require careful balance between cooperation benefits and competitive advantage protection. Sharing technological knowledge to develop alternative supply sources creates capabilities that eventually compete with original technology providers, requiring frameworks that reward innovation while enabling strategic objectives.

Future Trajectory Analysis and Strategic Implications

Global Supply Chain Reconfiguration Trends

Friend-shoring versus near-shoring considerations represent different approaches to supply chain risk reduction. Geographic proximity provides logistics advantages and cultural familiarity, while alliance-based sourcing prioritises political alignment over pure geographic factors. Optimal strategies likely combine both approaches based on specific mineral characteristics and strategic importance.

Technology innovation acceleration offers potential pathways to reduce mineral intensity requirements across multiple applications. Advanced battery chemistry development, recycling technology improvements, and alternative material substitution research could fundamentally alter demand patterns and reduce supply chain vulnerabilities.

Recycling and circular economy integration represents crucial long-term supply security strategies that reduce primary extraction dependence. Furthermore, urban mining of electronic waste, battery recycling, and component remanufacturing can provide substantial material volumes while reducing environmental impacts compared to primary extraction.

Investment Strategy Evolution for Mining Sector

ESG compliance alignment with national security priorities creates new investment evaluation frameworks that incorporate governance factors alongside traditional financial metrics. Projects that contribute to strategic supply security may receive preferential treatment or regulatory support that enhances their investment attractiveness.

Joint venture structuring enables risk sharing between private investors and government entities while leveraging complementary capabilities. Public-private partnerships can combine government strategic objectives with private sector operational efficiency, creating hybrid models that achieve both security and economic objectives.

Vertical integration opportunities from extraction to processing provide companies with greater supply chain control while reducing dependency on external processing capabilities. This integration requires substantial capital investment but offers long-term strategic positioning advantages in secure supply markets.

Strategic Framework Assessment for Stakeholders

Investment Community Implications: The US-UK critical minerals agreement signals a fundamental shift toward security-premium valuations in strategic mineral assets, particularly those located within allied nations featuring streamlined regulatory frameworks and government support mechanisms.

Mining Industry Strategic Positioning: Domestic extraction and processing projects within US and UK jurisdictions now carry enhanced strategic value through government backing that reduces financing costs and accelerates permitting timelines for qualifying projects.

End-User Industry Planning: Supply chain diversification requirements will increase input costs during transition periods but provide long-term price stability and supply security for automotive, defence, and clean energy sectors dependent on critical mineral inputs.

The transformation of critical mineral supply chains represents a fundamental shift from purely economic optimisation toward strategic security considerations that balance cost efficiency with supply reliability. This evolution requires sustained commitment from both government and industry stakeholders to develop alternative supply sources while managing transition costs and implementation challenges.

Understanding these dynamics provides essential context for stakeholders navigating an increasingly complex mineral supply environment where geopolitical factors play growing roles in traditional commodity markets. Success in this environment requires comprehensive strategies that integrate economic analysis with strategic risk assessment and policy coordination capabilities.

Looking to Capitalise on Critical Minerals Market Shifts?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications about significant ASX mineral discoveries in critical materials sectors, transforming complex geological data into actionable investment insights for both short-term traders and strategic investors. With supply chain vulnerabilities creating unprecedented opportunities in domestic mineral projects, explore Discovery Alert's track record of identifying major discoveries and begin your 14-day free trial to position yourself ahead of these transformative market developments.