June 20, 2026

Global Technology Infrastructure Revolution: How AI Infrastructure Demands Are Reshaping Materials Markets

The convergence of artificial intelligence acceleration and digital infrastructure expansion represents one of the most significant technological transitions since the advent of the internet. AI and the growth of data centre infrastructure creates unprecedented demands for materials, power, and cooling systems that cascade across multiple industrial sectors simultaneously.

Modern AI workloads require specialised processing capabilities that traditional data centre architectures cannot efficiently support. Graphics processing units (GPUs) designed for parallel computation consume approximately 10-15 times more electrical power per computational unit compared to conventional central processing units (CPUs), fundamentally altering facility design requirements across power distribution, thermal management, and materials specifications.

This architectural transition creates investment opportunities extending far beyond technology companies into materials science, mining industry evolution, and industrial infrastructure. The Silver Institute research indicates that since 2000, total global information technology power capacity has expanded approximately 53 times, from 0.93 gigawatts to nearly 50 gigawatts, representing a 5,252 percent increase over two decades.

When big ASX news breaks, our subscribers know first

Exponential Infrastructure Capacity Requirements Through 2030

Unprecedented Power Consumption Growth Trajectories

Current data centre power consumption represents approximately 4.4% of total United States electricity generation, with projections suggesting global data centre consumption could reach 15-21% of worldwide electrical demand by 2030. This growth trajectory exceeds historical technology adoption curves and positions data centres among the largest single electricity consumers globally.

The JLL 2026 Global Data Centre Outlook projects nearly 100 gigawatts of new data centre capacity coming online between 2026 and 2030, effectively doubling global capacity at a 14% compound annual growth rate. Furthermore, Gartner forecasts indicate that global electricity consumption from data centres will double from 448 terawatt hours in 2025 to 980 terawatt hours by 2030.

| Infrastructure Component | 2025 Baseline | 2030 Projection | Growth Multiple |

|---|---|---|---|

| Global Power Capacity | 50 GW | 150 GW | 3.0x |

| Annual Electricity Consumption | 448 TWh | 980 TWh | 2.2x |

| Capital Investment (Cumulative) | $1.2 trillion | $7.0 trillion | 5.8x |

Regional Infrastructure Distribution Patterns

Geographic expansion patterns reveal sophisticated optimisation across competing variables including renewable energy availability, regulatory frameworks, and natural cooling characteristics. Northern European facilities leverage cold climate conditions and abundant renewable energy sources, while Texas and Arizona deployments capitalise on solar power availability and deregulated electricity markets.

Singapore and Hong Kong continue expanding despite higher operational costs due to strategic positioning for Asian market access, whilst Canadian facilities increasingly utilise hydroelectric power combined with natural cooling advantages. This geographic diversification reflects risk management strategies addressing regulatory uncertainty, energy security, and operational resilience requirements.

Critical Infrastructure Bottlenecks and Solutions

Electrical Grid Connection Constraints

Grid connection delays currently average 2-4 years for major data centre deployments, with potential expansion to 5-7 years by 2030 due to transmission infrastructure limitations. These delays represent the primary constraint limiting rapid capacity expansion, even when construction timelines and equipment availability permit faster deployment.

Hyperscale operators including Microsoft, Amazon, and Google increasingly develop dedicated power generation facilities rather than relying exclusively on utility grid connections. This strategic shift toward vertical energy integration reflects recognition that traditional utility infrastructure cannot accommodate projected growth trajectories without substantial modernisation investments.

Advanced Thermal Management Technologies

Traditional air cooling systems prove inadequate for AI workloads generating heat densities exceeding 50 kilowatts per rack, compared to conventional data centre densities of approximately 5-10 kW/rack. This five-to-ten-fold increase in thermal intensity necessitates fundamental cooling system redesigns.

Advanced cooling methodologies include:

• Liquid immersion cooling: Complete server submersion in dielectric fluids engineered for electrical neutrality and superior heat transfer

• Direct-to-chip cooling: Closed-loop coolant circulation through processor heat exchangers, bypassing intermediate thermal interfaces

• Hybrid air-liquid systems: Segmented cooling strategies combining air cooling for periphery equipment with liquid cooling for GPU-intensive cluster arrays

These technologies can reduce overall facility energy consumption by 20-40% compared to traditional air cooling whilst enabling higher computational densities essential for AI and the growth of data centre infrastructure.

Critical Materials Supply Chain Analysis

Silver's Strategic Role in High-Performance Computing

Silver's unique material properties make it irreplaceable in high-performance computing environments where marginal efficiency improvements compound across thousands of interconnection points. The metal's 108% IACS conductivity rating represents the industry standard for minimising electrical resistance losses in mission-critical applications requiring 99.999% uptime specifications.

Oxford Economics analysis identifies silver's thermal conductivity advantage at 429 W/m·K versus copper's approximately 385 W/m·K, providing roughly 11% superior heat transfer capability. This differential becomes critical when aggregate cooling demands create facility-wide constraints affecting operational reliability and energy consumption.

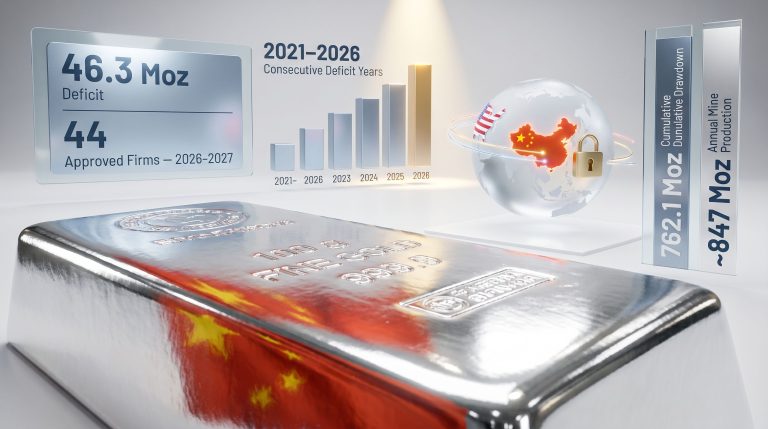

Global Supply-Demand Imbalance Dynamics

Current global silver production of approximately 844 million ounces annually faces a structural deficit of 150 million ounces, representing approximately 15% undersupply relative to industrial demand according to Silver Institute research. Consequently, this deficit occurs during the fourth consecutive year of structural supply shortages, suggesting fundamental market imbalance rather than cyclical fluctuation.

Additionally, silver supply deficits create compelling investment opportunities across the materials value chain.

Primary supply source breakdown:

• Lead/zinc byproduct mining: 29.4% of global supply

• Primary silver mines: 27.8% of global supply

• Copper byproduct mining: 18.6% of global supply

• Recycling operations: 24.2% of global supply

Industrial demand drivers show accelerating consumption patterns:

• Solar photovoltaic sector: Silver demand increased from 11% of global supply in 2020 to 29% by 2024

• Electric vehicle manufacturing: Projected 3.4% compound annual growth rate through 2031, with EVs consuming approximately twice the silver per vehicle compared to internal combustion engines

• Advanced electronics: Record-high demand across consumer devices, industrial automation, and telecommunications infrastructure

Hyperscaler Infrastructure Investment Strategies

Capital Allocation Transformation

McKinsey analysis indicates hyperscale operators are committing approximately $7 trillion through 2030 across infrastructure development, representing unprecedented capital allocation toward physical assets rather than software and services development. This investment prioritisation reflects recognition that infrastructure constraints represent the primary limitation on AI and the growth of data centre infrastructure capability expansion.

Strategic investment allocation breakdown:

| Priority Category | Capital Allocation | Investment Focus |

|---|---|---|

| Power Generation & Distribution | 35% ($2.45 trillion) | On-site renewable generation, grid modernisation |

| Cooling & Thermal Management | 25% ($1.75 trillion) | Advanced cooling systems, energy efficiency |

| Computing Hardware | 20% ($1.4 trillion) | GPU accelerators, specialised AI chips |

| Network & Connectivity | 15% ($1.05 trillion) | High-speed interconnects, edge infrastructure |

| Physical Facilities & Security | 5% ($350 billion) | Construction, environmental systems |

This allocation reveals that non-computing infrastructure represents 65% of total capital expenditure, fundamentally reframing data centre investment priorities compared to historical patterns where computing hardware dominated budgets.

Geographic Risk Diversification

Hyperscale operators increasingly prioritise geographic diversification to mitigate regulatory, environmental, and geopolitical risks. Northern European expansion leverages renewable energy abundance and favourable regulatory frameworks, whilst Texas and Arizona growth capitalises on deregulated electricity markets and solar power availability.

Moreover, Canada emerges as a strategic location combining hydroelectric power abundance, natural cooling advantages, and political stability. In addition, Canada's energy transition supports sustainable data centre development. Asian market expansion continues despite higher operational costs due to proximity to manufacturing centres and growing regional demand for AI services.

Materials Investment Opportunities and Market Dynamics

Mining Sector Value Creation Mechanisms

The structural silver deficit creates compelling investment scenarios across the mining value chain, particularly for operations with low all-in sustaining costs below $15 per ounce and expandable production capacity. Polymetallic operations generating silver as byproduct from lead/zinc, copper, or gold mining offer diversified revenue streams whilst benefiting from silver price appreciation.

Investment criteria for silver-exposed mining operations:

• Geographically diversified asset portfolios reducing regulatory and operational risk concentration

• Low-cost production profiles maintaining profitability across commodity price cycles

• Expandable reserves and resources supporting production growth without additional exploration risk

• Byproduct credit optimisation from lead, zinc, copper, or gold co-production reducing silver production costs

Silver's price performance demonstrates strong fundamentals, with 21% intra-year price increases in 2024 and a 59% trough-to-peak rally supporting mining sector margins. Values exceeded $100 per ounce in late 2025, whilst production costs remain relatively stable, creating favourable operational leverage for established producers.

Technology Infrastructure Investment Themes

Power generation and management solutions targeting data centre markets offer exposure to infrastructure expansion without direct commodity price sensitivity. Companies developing renewable energy solutions specifically designed for data centre applications benefit from long-term purchase agreements and predictable demand growth.

Energy storage and grid stability technologies address intermittent renewable energy integration challenges whilst enabling data centres to operate independently from utility grid constraints. Smart grid technologies facilitating demand response capabilities allow facilities to optimise energy consumption and reduce peak demand charges.

Advanced cooling system manufacturers developing liquid cooling, thermal interface materials, and energy-efficient HVAC systems specifically for high-density computing environments capture value from the fundamental architectural transition toward AI and the growth of data centre infrastructure.

The next major ASX story will hit our subscribers first

Regulatory Framework Evolution and Policy Implications

Environmental and Energy Efficiency Standards

Government regulatory frameworks increasingly address data centre environmental impact through specific performance requirements rather than general industrial standards. Power Usage Effectiveness (PUE) requirements below 1.3 become standard across major jurisdictions, driving adoption of advanced cooling technologies and renewable energy integration.

Renewable energy procurement mandates require data centre operators to source specified percentages of electricity from renewable sources, creating dedicated markets for solar, wind, and battery storage systems. Carbon neutrality timelines established for major technology companies accelerate investment in renewable energy and energy efficiency technologies.

Demand response programme participation requirements enable utility companies to manage grid stability during peak consumption periods whilst providing data centres with favourable electricity rates for flexible consumption patterns.

Critical Materials Security Initiatives

National security considerations drive policy support for domestic mining and processing capacity, particularly for materials essential to digital infrastructure. Strategic material stockpiling programmes create government demand for silver and other critical metals whilst supporting price stability during supply disruptions.

Furthermore, critical minerals recycling initiatives aim to reduce dependence on primary mining operations. Mining project expedited permitting processes reduce development timelines for domestic production capacity, whilst research and development funding for recycling technologies aims to increase secondary supply from electronic waste and industrial scrap recovery.

Trade policy measures supporting supply chain resilience include tariffs on processed materials from specific countries combined with incentives for domestic processing capacity development.

Long-Term Structural Transformation Implications

Industry Consolidation and Market Concentration

The capital intensity required for AI-optimised data centre development favours larger operators with access to substantial financial resources and technical expertise. This trend potentially accelerates consolidation among smaller cloud service providers whilst creating barriers to entry for new competitors.

Vertical integration strategies become increasingly common as hyperscale operators develop capabilities across power generation, thermal management, and even materials processing to ensure supply chain security and operational control.

Supply Chain Restructuring and Investment Opportunities

Critical materials supply chains will likely undergo fundamental restructuring emphasising increased emphasis on vertical integration by technology companies seeking supply security. Long-term supply agreements with mining operations provide producers with revenue certainty whilst ensuring technology companies access to essential materials.

Investment in recycling and circular economy initiatives addresses both environmental concerns and supply security, particularly for silver recovery from electronic waste streams. Development of alternative materials and manufacturing processes creates opportunities for companies developing substitutes or efficiency improvements.

The intersection of AI infrastructure expansion and critical materials demand represents a multi-decade investment theme spanning technology, mining, energy, and industrial sectors. Understanding these interconnected dynamics provides investors with framework for identifying opportunities across the entire value chain supporting digital infrastructure transformation.

Disclaimer: This analysis is for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult with qualified financial professionals before making investment decisions. Commodity markets and mining investments carry substantial risks including price volatility, operational challenges, and regulatory changes.

Looking to Capitalise on AI Infrastructure's Materials Demand?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including silver and critical materials essential for AI data centre infrastructure development. Begin your 14-day free trial today and position yourself ahead of the market as technology infrastructure demand creates unprecedented opportunities for materials sector investors.