June 9, 2026

The Monetary Architecture Beneath Gold's Historic Ascent

Few asset classes reveal the fault lines in the global monetary system as clearly as gold. When sovereign wealth managers, retail investors, and central banks simultaneously accelerate their accumulation of a single asset, it rarely reflects a passing trend. It reflects a structural reassessment of trust, and in 2025, that reassessment produced the most powerful gold rally in over four decades.

Understanding where the gold bull market still has legs today requires looking beyond the noise of short-term price swings and examining the foundational forces that catalysed the move higher in the first place. The question for 2026 is not whether those forces existed, but whether they remain potent enough to drive the next leg of the rally once near-term headwinds subside.

When big ASX news breaks, our subscribers know first

What the 2025 Numbers Actually Tell Us

A 44% Annual Gain: Separating Signal From Noise

Gold delivered a 44% price gain in calendar year 2025, its strongest annual performance since 1979. The yellow metal crossed above $4,500 for the first time in history before the year closed. Numbers of this magnitude invite scepticism, and rightly so. However, the composition of demand behind that move tells a more nuanced story than a simple speculative surge.

A rally of this scale driven primarily by speculative futures positioning would be identifiable by thin physical demand, declining central bank interest, and a reversal in ETF flows. The 2025 data shows something structurally different. Three distinct demand categories, each operating with its own independent motivation, converged simultaneously to reprice gold upward.

The Three Demand Pillars That Powered the Rally

1. Investment Demand

Physical gold investment climbed 16% to a 12-year high in 2025. The primary catalysts were bullish price expectations combined with elevated economic and geopolitical uncertainty. Geographically, the growth was led by Asia's two largest economies:

- China recorded a +28% increase in physical gold investment

- India followed with a +17% increase

- Both countries have deep cultural and financial motivations for gold accumulation that extend well beyond short-term price speculation

This was not retail momentum chasing. The scale of physical investment growth in China and India reflects long-term savings behaviour and a deliberate shift in how households in these economies store wealth.

2. Central Bank Accumulation

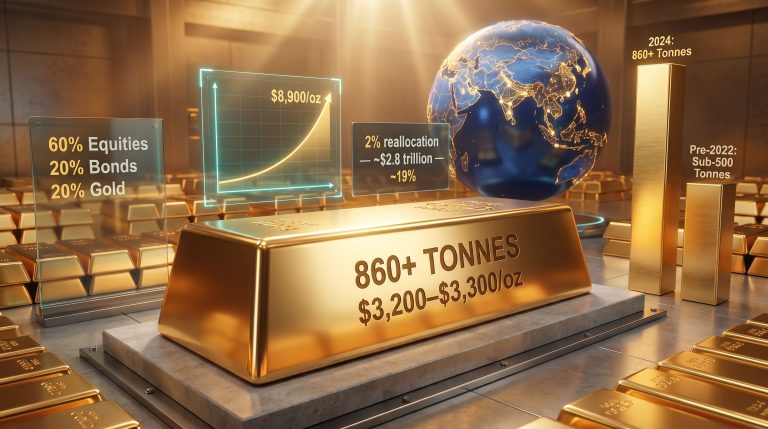

Official sector net purchases reached 863.3 tonnes in 2025. While this represented a 21% year-on-year decline and the lowest level since 2021, the historical context transforms this figure entirely. Furthermore, central bank gold buying has fundamentally reshaped price dynamics in ways that were not anticipated by traditional market models.

Between 2010 and 2021, central banks added an average of just 473 tonnes per year to global gold reserves. The 2025 figure is therefore running at nearly double the pre-2022 historical average, despite the annual decline.

| Metric | 2025 Figure | 2010-2021 Annual Average |

|---|---|---|

| Central Bank Net Purchases | 863.3 tonnes | 473 tonnes |

| Physical Investment Growth | +16% (12-year high) | – |

| China Physical Investment | +28% | – |

| India Physical Investment | +17% | – |

| Jewelry Demand | 1,542 tonnes | – |

| Mine Production Growth | +2% (record level) | – |

| Recycling Growth | +2.8% | – |

The acceleration in central bank gold reserves since 2022 is directly linked to a watershed moment in reserve asset management: the freezing of Russian sovereign reserves following the Ukraine invasion. That single geopolitical decision demonstrated to reserve managers globally that U.S. dollar holdings could be immobilised by policy action. Nations holding significant dollar reserves now face a credible precedent that those assets carry a form of political risk that was previously theoretical.

3. Dollar Credibility Concerns

Growing anxiety about trust in the US dollar as the world's primary reserve currency represents perhaps the most structurally significant driver of the current gold bull market still has legs narrative. This concern operates across multiple levels simultaneously:

- Fiscal deterioration in the United States, with federal debt at historically elevated levels, raises questions about the sustainability of dollar-denominated obligations

- U.S. policy divergence across trade, domestic, and foreign policy domains has introduced unpredictability that unnerves sovereign holders of dollar assets

- A modest but persistent de-dollarisation trend among emerging market central banks is reshaping how nations approach reserve diversification

Why Falling Jewelry Demand Actually Reinforces the Bull Case

Jewelry consumption fell 18% to 1,542 tonnes in 2025, a five-year low. At first glance, this appears concerning. In practice, it confirms the opposite. Jewelry demand is price-sensitive and consumer-driven. When gold prices rise substantially, discretionary jewelry purchases contract. This is entirely expected behaviour.

What matters analytically is the demand rotation occurring beneath the surface. The categories that declined in 2025 were precisely those most sensitive to price levels. The categories that surged were institutional, sovereign, and long-horizon in nature. This shift from consumer to institutional demand is a hallmark of a maturing bull market, not a signal of exhaustion.

Supply Constraints: The Invisible Amplifier

Mine Production Cannot Match Institutional Appetite

Mine output grew by just 2% in 2025, driven by project ramp-ups, capacity expansions, and increased artisanal and small-scale mining activity. Despite the modest percentage gain, this figure represented a new all-time record for global gold mine production. The structural challenge is straightforward: even record output is insufficient to absorb the pace of institutional demand growth.

Recycling volumes increased by approximately 2.8% in 2025 but remain well below the 2012 peak. This is a behavioural signal worth examining carefully. In theory, rising gold prices should incentivise holders of physical gold to sell scrap material back into the market. The fact that recycling remains historically subdued despite record prices suggests that physical gold holders are choosing to retain their metal rather than liquidate. This preference for accumulation over profit-taking provides a structural floor under prices.

The combination of record mine production growing at just 2% annually against investment demand rising 16% and central bank buying running at nearly double historical averages creates a supply-demand dynamic with only one natural price resolution.

Reading the 2026 Correction Without Losing the Thread

From $5,500 to a Consolidation Range

Gold extended its extraordinary run into early 2026, breaking above $5,000 and approaching $5,500 before a sharp correction materialised in late January. Subsequently, military action by the U.S. and Israel against Iran introduced a new layer of complexity. The yellow metal entered a consolidation range between approximately $4,300 and $4,800, with sustained downward pressure driven by a specific market narrative.

The dominant mainstream interpretation holds that elevated oil prices resulting from the Iran conflict will sustain or worsen inflation, forcing the Federal Reserve to keep interest rates higher for longer, or potentially raise them further. Since gold carries no yield, higher rates theoretically increase the opportunity cost of holding it, creating selling pressure even in a risk-elevated environment. This is the apparent paradox: gold declining during a geopolitical shock.

The resolution of this paradox lies in understanding that safe-haven demand and interest rate expectations operate as competing forces simultaneously. When a geopolitical event raises inflation expectations more than it raises fear-driven buying, the rate-expectation effect can temporarily dominate. According to TD Securities' analysis of the gold bull run, however, this temporary pressure is unlikely to derail the broader structural uptrend.

Bull Case vs. Bear Case: Mapping the Scenarios

| Factor | Bull Case | Bear Case |

|---|---|---|

| Federal Reserve Policy | Fed tolerates higher inflation to avoid economic contraction | Fed hikes rates to combat oil-driven inflation |

| Geopolitical Resolution | Iran conflict resolves relatively quickly | Prolonged conflict sustains oil price shock |

| Dollar Trajectory | Continued erosion of confidence supports gold | Dollar strengthens as safe-haven demand shifts |

| Central Bank Demand | Official buying remains above historical averages | Sovereign buyers pause amid budget pressures |

| Equity Valuations | Reallocation from stretched equities to gold | Equity resilience reduces safe-haven urgency |

| Physical Investment | Asian demand remains structurally robust | Price fatigue dampens discretionary buying |

Research from Metals Focus, published in its Gold Focus 2026 report, maintains a bullish outlook for the second half of 2026. The analytical framework assumes the economic and political costs of a prolonged conflict are likely to drive toward a relatively swift resolution, limiting both the duration of the oil price shock and its downstream monetary policy implications.

Critically, Metals Focus analysts challenge the prevailing consensus that U.S. rate hikes are the likely outcome over the next 12 months. Their view is that policymakers may ultimately choose to tolerate above-target inflation rather than impose rate increases on an economy carrying record levels of debt. This is a minority position in current market discourse, but it has historical precedent.

The Federal Reserve's Structural Dilemma

A Policy Catch-22 That Favours Gold in Both Directions

The Federal Reserve faces what may be the most structurally constrained policy environment in modern U.S. monetary history. The dilemma is binary and irreconcilable in the short term:

- Option A: Tighten monetary policy to suppress inflation. Risk: imposing additional strain on an economy and financial system saturated with debt, potentially triggering credit stress, corporate distress, and recession.

- Option B: Hold rates steady or ease to protect economic growth. Risk: entrenching inflation above target while eroding dollar purchasing power and credibility.

The analytically significant insight here is that gold benefits materially from both outcomes. If the Fed tightens and damages the economy, recession fears accelerate safe-haven demand. If the Fed eases or simply fails to tighten sufficiently, the opportunity cost of holding gold falls and real interest rates remain suppressed, directly supporting gold prices.

U.S. federal debt dynamics create a structural incentive for policymakers to tolerate above-target inflation rather than risk a debt-servicing crisis. Historical episodes of fiscal dominance over monetary policy, where governments constrain central bank tightening to manage sovereign debt loads, have consistently been associated with elevated real gold prices. The post-2020 U.S. fiscal trajectory shares several characteristics with these historical episodes.

The mainstream rate-hike consensus may be structurally weaker than markets currently believe, precisely because the debt burden constraining Fed policy options is larger than in any prior tightening cycle.

The Four Macro Pillars Keeping the Gold Bull Market Intact

Analysts at Metals Focus identify four structural drivers from 2025 that remain firmly in place heading into the second half of 2026. These are not transient catalysts but multi-year forces reshaping how institutions and sovereigns approach capital allocation. In addition, the ways in which central banks influencing gold prices continue to evolve represent a critical variable in the outlook for H2 2026.

1. U.S. Policy Uncertainty

Ongoing divergence from established norms across trade, fiscal, and foreign policy domains creates persistent demand for assets that exist outside the dollar system. Unpredictability in U.S. policy is itself a source of risk premium for dollar-denominated assets, making gold's politically neutral status increasingly attractive.

2. Dollar Reserve Status Erosion

The long-term concerns about the U.S. dollar's role as the world's primary reserve currency are not resolving. Incremental de-dollarisation among emerging market central banks continues, supported by the precedent set by the freezing of Russian reserves. Each new instance of dollar weaponisation reinforces the case for reserve diversification.

3. Elevated Geopolitical Risk Premium

Multiple active conflict zones and intensifying great-power competition have established a structural risk premium in gold that extends well beyond any single geopolitical event. The Iran conflict is a layer added to an already elevated baseline, not the sole driver of gold's geopolitical value.

4. Stretched Equity Valuations

Historically elevated equity price-to-earnings ratios increase the appeal of gold as a portfolio diversifier. When equity markets are priced for near-perfection, the marginal utility of adding gold to institutional portfolios rises. Furthermore, as noted by EPC Advisors in their long-term outlook, this dynamic supports sustained investment demand independent of any crisis narrative.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

Is the gold bull market still has legs in 2026, or is the rally finished?

The current price consolidation in the $4,300 to $4,800 range is characterised by institutional analysts as a mid-cycle correction rather than a trend reversal. The four structural drivers that powered the 2025 rally remain intact. The correction reflects a confluence of geopolitical shock and rate-expectation repricing, not a collapse in the underlying demand thesis.

What would definitively end the gold bull market?

A genuine trend reversal would likely require several simultaneous developments: sustained real interest rate increases that make yield-bearing assets significantly more attractive than gold, a credible restoration of U.S. fiscal discipline that rebuilds long-term dollar confidence, a meaningful reduction in geopolitical tensions across multiple regions, and a sustained decline in central bank gold buying back below the 473-tonne historical average. None of these conditions are currently present.

Why does gold sometimes fall during geopolitical crises?

Safe-haven demand and interest rate expectations operate as competing forces simultaneously. When a geopolitical event raises inflation expectations more sharply than it drives fear-based buying, the rate-expectation effect can temporarily dominate, creating selling pressure even in risk-elevated environments. The Iran conflict falls into this category: its primary market impact was to raise oil prices and therefore inflation expectations, rather than to trigger a pure flight-to-safety response.

What price levels matter technically for gold in H2 2026?

The $5,000 level represents a key psychological and technical reference point established during early 2026. The $4,300 level marks the lower boundary of the current consolidation range. Institutional research points to a resumption of the uptrend in the second half of 2026 as geopolitical clarity improves and the Fed's constrained policy options become more apparent to markets.

Key Data Summary

- Gold posted a 44% gain in 2025, its best calendar year performance since 1979

- Physical investment reached a 12-year high, up 16% year-on-year

- Central bank purchases of 863.3 tonnes remain 83% above the 2010-2021 annual average

- Mine production set a record but grew by only 2%, insufficient to offset institutional demand

- Recycling volumes grew 2.8% but remain well below 2012 peaks, indicating holders prefer accumulation

- Gold approached $5,500 in early 2026 before correcting into the $4,300-$4,800 range

- Institutional research maintains a bullish H2 2026 forecast contingent on geopolitical resolution

This article is intended for informational purposes only and does not constitute financial advice. Gold markets involve significant price risk and forecasts referenced herein represent the analytical views of independent research firms, not guaranteed outcomes. Investors should conduct their own due diligence before making any investment decisions.

Want to Identify the Next Major ASX Mineral Discovery Before the Market Does?

While gold's structural bull case continues to unfold across global markets, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly notifying subscribers of significant mineral discoveries — from gold to over 30 other commodities — so both traders and long-term investors can act decisively ahead of the crowd. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to secure a market-leading edge.