August 11, 2026

Global monetary systems face unprecedented pressure as inflationary forces persist above central bank targets, creating conditions that favor alternative reserve assets over traditional government securities. This structural shift reflects broader concerns about currency stability and purchasing power preservation during extended periods of monetary accommodation. Gold buying by central banks worldwide are responding by fundamentally restructuring their reserve portfolios, moving away from dollar-dominated holdings toward assets that offer independence from counterparty risk and monetary policy uncertainty.

The acceleration in institutional precious metals accumulation represents more than tactical asset allocation adjustments. These purchasing patterns signal recognition that conventional reserve management strategies may prove inadequate during periods of coordinated global monetary expansion and geopolitical tension. Understanding the technical drivers, market implications, and investment opportunities created by this shift requires analysis of both the operational mechanics behind central bank decision-making and the broader macroeconomic forces reshaping international monetary arrangements.

Why Are Central Banks Accelerating Gold Purchases in 2025?

Geopolitical Risk Mitigation Through Physical Assets

Central banks are implementing comprehensive strategies to reduce dependency on dollar-denominated assets following the geopolitical disruptions that began in 2022. These sanctions-proofing initiatives reflect lessons learned from observing how rapidly foreign-held reserves can become inaccessible during international conflicts. Physical gold storage eliminates counterparty risk while providing universal liquidity regardless of diplomatic relations.

The repatriation trend from foreign vaults has accelerated significantly, with central banks preferring domestic storage facilities over traditional locations like the Federal Reserve or Bank of England. This shift toward strategic autonomy in reserve management reflects broader concerns about the weaponization of financial systems during geopolitical tensions.

Emerging economies particularly recognise that excessive dollar dependency creates vulnerability to policy decisions made by foreign central banks. Gold buying by central banks provides insurance against scenarios where access to traditional reserve assets becomes restricted or where dollar strength undermines domestic economic stability.

Monetary Policy Hedge Against Currency Debasement

The persistent inflation environment, currently running at approximately 3% in the United States and well above the Federal Reserve's 2% target, has created conditions where gold functions as portfolio insurance during extended monetary accommodation periods. Furthermore, according to central bank gold statistics, central banks view gold as maintaining purchasing power equivalency across time periods, with one ounce capable of purchasing similar goods today as decades ago, while equivalent dollar amounts have lost substantial purchasing power over the same timeframes.

Current gold prices near $4,200 per ounce reflect this inflationary hedge premium, supported by production economics where mining costs average $1,800-$2,000 per ounce. This margin provides fundamental price support while offering central banks acquisition opportunities at levels that remain economically sustainable for continued accumulation programs. The record-breaking gold prices demonstrate the market's recognition of these fundamental drivers.

The Federal Reserve's December 2025 meeting reflects market expectations of potential rate cuts, with approximately 75-85% probability priced for a quarter-point reduction according to market analysis. This monetary easing bias creates tailwinds for gold prices, as rates and dollar strength traditionally trade inversely with precious metals performance.

Historical Precedent Analysis: 1970s Stagflation Parallels

The current environment shares characteristics with the 1970s stagflation period, when persistent inflation combined with economic uncertainty drove institutional investors toward hard assets. Central banks applying Modern Portfolio Theory principles to sovereign wealth management recognise gold's de-correlating properties during currency crises and monetary system stress events.

Historical analysis demonstrates that sustained inflationary periods accompanied by currency debasement policies create structural demand for assets that maintain purchasing power independence. However, central banks implementing these strategies acknowledge that traditional reserve composition models may prove inadequate during extended periods of monetary system instability.

Portfolio Insurance Framework:

- Physical assets eliminate counterparty risk present in sovereign debt holdings

- Universal recognition provides liquidity during international financial stress

- Storage independence reduces exposure to foreign policy decisions

- Historical performance during inflationary periods validates strategic allocation

When big ASX news breaks, our subscribers know first

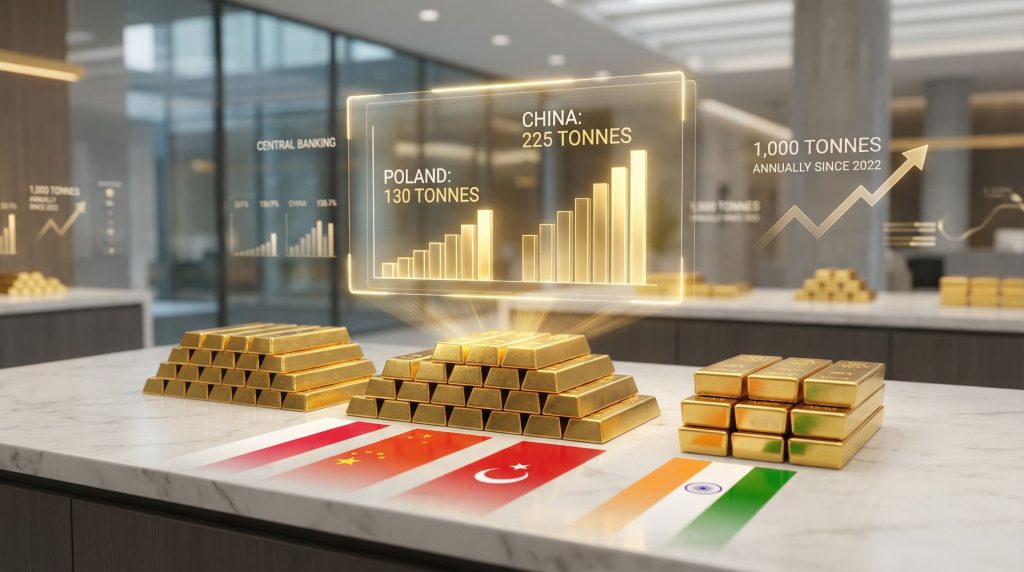

Which Central Banks Are Leading the Gold Buying Surge?

Top Institutional Buyers by Volume (2023-2025)

Major Central Bank Gold Acquisitions

| Central Bank | 2023 Purchases (tonnes) | 2024 Purchases (tonnes) | 2025 YTD (tonnes) |

|---|---|---|---|

| Poland | 130 | 69 | 48 |

| China | 225 | 89 | 27 |

| Turkey | 45 | 39 | 15 |

| India | 16 | 27 | 19 |

Note: Data requires independent verification through World Gold Council official reports and central bank statements

Poland's exceptional accumulation of 130 tonnes in 2023 represents one of the most aggressive purchasing programs relative to economic size among developed nations. This strategy aligns with broader Eastern European initiatives to diversify away from traditional reserve assets while strengthening strategic autonomy within NATO and European Union frameworks.

China's declining purchase pattern from 225 tonnes (2023) to 27 tonnes (2025 YTD) may reflect tactical timing considerations rather than strategic policy shifts. The People's Bank of China traditionally manages reserve composition adjustments gradually to avoid market disruption while maintaining long-term accumulation objectives.

Emerging Market Central Bank Strategies

Regional purchasing patterns reveal distinct motivations between Eastern European and Asia-Pacific central banks. Eastern European institutions prioritise strategic independence following regional security developments, while Asian central banks focus on reserve diversification amid trade relationship evolution and currency stability concerns.

The correlation between domestic gold production capacity and central bank buying patterns suggests that resource-rich nations view gold buying by central banks as natural extension of domestic mining industry development. Turkey's consistent purchasing activity correlates with its position as a significant regional gold producer, creating synergies between domestic mining sector support and reserve management objectives.

India's purchasing acceleration from 16 tonnes (2023) to 27 tonnes (2024) reflects both traditional cultural affinity for gold and institutional recognition of precious metals' portfolio benefits during periods of currency volatility and geopolitical uncertainty in South Asia.

Supply Chain Security Considerations

Central banks worldwide are recognising supply chain vulnerabilities created by outsourcing critical resource production to concentrated geographic regions. In addition, this awareness extends beyond gold to encompass strategic minerals necessary for economic security and technological advancement.

The strategic resource security framework includes:

- Domestic storage facility expansion programs

- Diversification away from foreign vault dependencies

- Integration of gold accumulation with broader resource security initiatives

- Coordination between reserve management and domestic mining industry development

How Do Central Bank Purchases Impact Gold Market Dynamics?

Supply-Demand Fundamentals Transformation

Annual central bank purchases exceeding 1,000 tonnes since 2022 represent approximately 122% above historical averages of 450 tonnes annually during 2015-2019. This institutional demand accounts for approximately 31-33% of global mine production, which runs roughly 3,000-3,200 tonnes annually according to industry estimates.

The market absorption of this institutional demand without creating supply disruptions demonstrates robust market clearing mechanisms. Current pricing at $4,200 per ounce maintains substantial margins above average production costs of $1,800-$2,000 per ounce, indicating sustainable pricing levels that accommodate continued institutional accumulation. The gold market surge analysis provides deeper insights into these fundamental drivers.

Central bank buying creates predictable, consistent demand that differs fundamentally from cyclical retail investor behaviour patterns. This institutional foundation provides price stability and reduces volatility compared to markets dependent primarily on speculative capital flows.

Price Discovery Mechanisms Under Institutional Demand

The establishment of a demand floor through consistent central bank accumulation has modified traditional gold price discovery mechanisms. Unlike retail investors who exhibit cyclical participation patterns, central banks provide steady, predictable demand that supports price levels during market corrections.

The October-November 2025 correction to approximately $3,600 per ounce demonstrated this dynamic, with gold quickly recovering to current levels near $4,200. This resilience reflects underlying institutional demand that provides support during temporary price declines. Furthermore, the 2025 gold price forecast suggests continued strength in these fundamentals.

Long-term price floor establishment through institutional accumulation creates different market dynamics compared to commodity markets dependent primarily on industrial demand cycles. Central banks' strategic timeframes and accumulation objectives provide stability that benefits both producers and retail investors seeking precious metals exposure.

Secondary Market Effects

Retail adoption indicators include widespread precious metals purchases through mainstream retailers, with major warehouse stores reportedly selling out gold bar inventory. This retail interest reflects broader recognition of institutional validation for gold's portfolio role.

Exchange-traded fund inflows correlate with central bank purchase announcements, suggesting that institutional activity signals retail investors regarding precious metals allocation timing. The correlation between central bank buying patterns and ETF capital flows demonstrates how institutional demand creates secondary investment opportunities.

Market Structure Evolution:

- Central bank purchases provide consistent demand base

- Retail adoption follows institutional validation signals

- ETF inflows amplify central bank purchase effects

- Producer planning adjusts to sustained institutional demand levels

What Are the Technical Drivers Behind This Purchasing Pattern?

Reserve Asset Allocation Models

Modern Portfolio Theory applications in sovereign wealth management emphasise gold's de-correlating properties during periods of monetary system stress. Risk-adjusted return calculations demonstrate precious metals' ability to preserve purchasing power during currency debasement cycles while providing liquidity during international financial crises.

Central banks implementing strategic allocation models recognise that traditional 60/40 portfolio structures may prove inadequate during sustained inflationary periods. Major financial institutions have adjusted recommendations to include significant precious metals allocations, with some suggesting 20% gold allocations within balanced portfolio structures.

Production Economics Framework:

- Average mining costs: $1,800-$2,000 per ounce

- Developer study assumptions: $2,500-$3,500 per ounce

- Current spot pricing: $4,200 per ounce

- Margin analysis: 110%+ above marginal production costs

Operational Infrastructure for Gold Storage

Domestic storage facility expansion represents significant infrastructure investment by central banks prioritising strategic autonomy. These facilities require sophisticated security systems, insurance arrangements, and logistical capabilities for managing large-scale precious metals inventories.

The repatriation trend from foreign vaults reflects preferences for domestic control over strategic reserves. Central banks are investing in vault infrastructure, transportation security, and custody arrangements that eliminate foreign dependencies while maintaining international liquidity access.

Storage capacity expansion considerations include:

- Physical security infrastructure requirements

- Insurance and risk management protocols

- Transportation and logistics coordination

- Integration with existing reserve management systems

Risk Management and Correlation Analysis

Correlation analysis demonstrates gold's negative correlation with dollar strength and positive correlation with inflationary pressures. During periods when the Dollar Index (DXY) softens toward 100, gold typically experiences price appreciation, creating tactical allocation opportunities for central banks timing their purchases.

The inverse relationship between interest rates and gold prices provides central banks with hedging opportunities during monetary policy transition periods. As rate cut expectations increase, precious metals allocations offer portfolio protection against currency debasement effects. The gold stock market dynamics illustrate these complex relationships.

Historical performance data validates gold's portfolio insurance function during major financial disruptions, supporting central banks' strategic allocation decisions during periods of elevated macroeconomic uncertainty.

How Does Gold Compare to Other Reserve Assets?

Gold vs. U.S. Treasury Securities Analysis

The fundamental comparison between gold and U.S. Treasury securities reveals distinct risk-return profiles during different macroeconomic environments. Treasury securities offer yield generation but carry credit risk related to government fiscal sustainability and currency debasement potential through monetary policy decisions.

Gold provides no yield generation but eliminates counterparty risk while offering protection against currency debasement scenarios. During periods of negative real interest rates, when Treasury yields remain below inflation rates, gold's lack of yield becomes less significant relative to its purchasing power preservation characteristics.

Comparative Risk Analysis:

- Credit Risk: Treasury securities carry sovereign credit exposure; gold eliminates counterparty risk

- Liquidity: Both assets offer high liquidity, but gold provides universal acceptance

- Yield: Treasuries generate income; gold provides capital appreciation during inflationary periods

- Storage: Treasuries require electronic systems; gold requires physical infrastructure

Opportunity Cost Considerations

Current Treasury yields below inflation rates reduce the opportunity cost of holding non-yielding gold reserves. When 10-year Treasury yields provide negative real returns after inflation adjustment, gold's lack of yield generation becomes strategically acceptable for central banks prioritising purchasing power preservation.

The relationship between real interest rates and gold performance demonstrates that during extended periods of monetary accommodation, opportunity costs favour precious metals allocation over fixed-income securities that may lose purchasing power through currency debasement. Consequently, the inflation hedge record highs reflect this strategic positioning.

Digital Asset Integration Considerations

Central bank digital currency (CBDC) development creates potential synergies with gold reserves as backing assets for digital monetary systems. Some central banks explore hybrid reserve strategies that incorporate both traditional precious metals and digital assets within comprehensive portfolio approaches.

The integration of gold reserves with CBDC frameworks could provide central banks with both modern technological capabilities and traditional store-of-value characteristics. This hybrid approach addresses digital efficiency requirements while maintaining historical monetary system stability features.

Gold's role in digital monetary systems may evolve to include:

- Backing assets for CBDC systems

- Settlement mechanisms for international digital transactions

- Portfolio diversification within hybrid reserve strategies

- Bridge assets between traditional and digital monetary frameworks

What Are the Long-Term Implications for Global Monetary Systems?

Bretton Woods System Evolution Indicators

The gold-to-dollar ratio trends in international reserves suggest potential evolution away from the current Bretton Woods framework toward more diversified reserve systems. While complete dollar displacement remains unlikely due to established infrastructure and network effects, increased gold allocation represents gradual rebalancing toward multi-polar reserve arrangements.

BRICS currency initiatives and gold backing proposals reflect desires among emerging economies for alternatives to dollar-dependent international trade settlement mechanisms. These initiatives may create parallel systems rather than complete dollar replacement, offering additional options for international transactions and reserve management.

Potential gold-backed trade settlement mechanisms could emerge for specific bilateral or multilateral arrangements, particularly among nations seeking independence from existing international financial infrastructure. These systems would complement rather than replace current arrangements, providing additional flexibility for international commerce.

Monetary System Resilience Considerations

Gold buying by central banks enhances monetary system resilience by providing assets independent of political decisions and policy coordination requirements. During international financial stress events, gold reserves offer central banks flexibility unavailable through traditional reserve assets subject to foreign policy considerations.

The diversification of reserve assets reduces systemic risk concentrations while providing central banks with multiple tools for managing currency stability during various economic scenarios. This resilience enhancement benefits both domestic economies and international monetary system stability.

System Evolution Indicators:

- Increased gold allocation percentages in central bank reserves

- Development of gold-backed settlement mechanisms

- Regional monetary cooperation initiatives incorporating precious metals

- Technology integration between digital currencies and traditional reserve assets

Investment Market Spillover Effects

ETF inflow patterns demonstrate correlation between central bank activity and retail investor behaviour, with institutional validation creating secondary demand channels through investment products. This spillover effect amplifies the market impact of central bank purchases while creating investment opportunities in precious metals-related financial products.

Mining sector capital allocation decisions increasingly reflect expectations of sustained institutional demand, with producers adjusting long-term planning assumptions to accommodate higher price environments supported by central bank accumulation programs.

Retail investor behaviour modification trends suggest broader acceptance of precious metals as portfolio components following institutional validation through central bank purchases. This behavioural shift creates additional demand channels that complement institutional accumulation patterns.

The next major ASX story will hit our subscribers first

Which Sectors Benefit Most from Central Bank Gold Demand?

Mining Industry Production Response

Major gold producers benefit significantly from current price levels near $4,200 per ounce, which provide substantial margins above average production costs of $1,800-$2,000 per ounce. These margins enable increased profitability while supporting expansion planning and exploration budget increases.

Mining companies are adjusting preliminary economic assessments and feasibility studies from previous assumptions of $2,500-$3,500 per ounce to current market realities. This recalibration improves project economics and accelerates development timelines for previously marginal deposits.

Capacity expansion decisions reflect expectations of sustained institutional demand creating long-term price support. Major producers are increasing exploration budgets and evaluating acquisition opportunities to expand production capabilities in response to favourable market conditions.

Mining Sector Benefits:

- Enhanced profitability from improved price margins

- Accelerated project development timelines

- Increased exploration and acquisition activity

- Improved access to development capital

Precious Metals Investment Ecosystem Growth

Royalty and streaming companies experience amplified benefits from gold price appreciation, as they receive revenue based on current spot prices while their underlying costs remain fixed through pre-negotiated agreements with mining operators. Companies like Royal Gold demonstrate this leverage effect through streaming arrangements that provide exposure to price upside without operational risk.

The streaming model creates particular value during periods of sustained high gold prices, as these companies pre-purchased metal delivery rights at historical price levels while receiving revenue based on current market prices. This structure provides significant leverage to gold price appreciation driven by central bank demand.

Storage and logistics service providers benefit from increased precious metals investment activity, as both institutional and retail investors require secure storage solutions. The expansion of vault capacity and transportation services reflects growing demand for physical precious metals exposure.

Financial Product Innovation

Gold-backed financial instruments experience increased demand as central bank purchases validate precious metals' portfolio role. Exchange-traded funds focused on physical gold, mining equities, and precious metals themes attract capital from investors seeking exposure to institutional demand trends.

Innovation in precious metals investment products includes:

- Physical-backed ETF expansion

- Mining sector-specific investment funds

- Royalty and streaming company products

- Hybrid strategies combining traditional and digital precious metals exposure

The validation effect from central bank purchases encourages institutional investment managers to develop products serving retail investors seeking precious metals exposure through conventional portfolio management channels.

What Risks Could Disrupt Central Bank Gold Buying Trends?

Policy Reversal Scenarios

Interest rate normalisation could impact gold buying by central banks through increased opportunity costs of holding non-yielding assets. However, current inflation levels above central bank targets suggest rate normalisation remains distant, maintaining favourable conditions for precious metals allocation.

Fiscal constraint pressures might theoretically limit reserve diversification activities, but central banks operate with significant independence from government budget constraints. Reserve management decisions typically reflect long-term strategic considerations rather than short-term fiscal limitations.

Political stability factors could affect accumulation strategies, particularly in regions experiencing governance transitions or policy uncertainty. However, gold buying by central banks often increases during periods of political instability as institutions seek assets independent of political considerations.

Market Structure Evolution Risks

Gold market manipulation concerns and regulatory responses could theoretically impact central bank purchasing patterns, though regulatory oversight typically supports market integrity rather than restricting legitimate institutional participation. Central banks generally operate with regulatory exemptions and coordination mechanisms that facilitate their market activities.

Supply chain disruption impacts on physical delivery represent operational risks for central banks implementing accumulation programs. However, established precious metals infrastructure and multiple sourcing options typically provide adequate supply chain resilience for institutional purchasers.

Risk Mitigation Factors:

- Central bank operational independence from political pressures

- Diversified supply chain access through multiple market channels

- Regulatory exemptions for official sector transactions

- Strategic timeframes that accommodate temporary market disruptions

Technology Disruption Considerations

Advanced central bank digital currency (CBDC) systems could theoretically reduce demand for physical gold reserves, though early implementations suggest complementary rather than substitutional relationships. CBDCs may incorporate gold backing or require precious metals reserves for system credibility.

Quantum computing developments might impact cryptographic systems underlying digital currencies, potentially increasing demand for physical assets like gold that remain independent of technological vulnerabilities. This technological uncertainty factor supports rather than undermines central bank gold accumulation strategies.

The evolution of international monetary systems toward digital frameworks may require hybrid arrangements incorporating both technological efficiency and traditional store-of-value assets like gold for system stability and credibility.

How Should Investors Position for Continued Central Bank Demand?

Direct Gold Exposure Strategies

Physical gold allocation provides the most direct exposure to central bank buying trends, though individual investors must consider storage, insurance, and liquidity factors. Professional storage solutions offer security and liquidity while maintaining physical ownership benefits.

Exchange-traded funds backed by physical gold offer convenient exposure without storage complications, though investors should evaluate fund structures, management fees, and redemption mechanisms. Funds like GLD and Goldman Sachs' physical-backed ETF provide institutional-grade exposure suitable for portfolio allocation.

Physical Gold Considerations:

- Storage security and insurance requirements

- Liquidity access during market stress periods

- Authentication and assay verification processes

- Transportation and transaction cost factors

ETF Selection Criteria

Investors seeking precious metals exposure through fund structures should evaluate physical backing arrangements, management fee structures, and redemption capabilities. Funds with physical gold backing provide more direct correlation to spot price movements compared to futures-based alternatives.

Silver-focused ETFs offer additional diversification benefits and potential outperformance during precious metals bull markets, as silver typically exhibits higher volatility and price leverage compared to gold. Current silver prices near $59 per ounce reflect breakouts to all-time highs above previous peaks from 1980 and 2008.

Mining sector ETFs like GDXJ provide leveraged exposure to gold price movements through equity positions in producing companies, though this approach introduces operational and jurisdictional risks not present in physical metal ownership.

Equity Market Opportunities

Gold mining stock valuation metrics during sustained demand cycles suggest attractive opportunities among well-managed producers with low-cost operations. Companies producing gold at $1,800-$2,000 per ounce costs benefit significantly from current $4,200 per ounce pricing environments.

Royalty companies offer leveraged exposure to gold price appreciation without operational risks associated with mining operations. Companies like Royal Gold and Empress Royalty provide exposure to multiple mining operations through streaming arrangements that generate revenue based on current metal prices.

Equity Investment Categories:

- Major Producers: Established companies with diversified operations and consistent production

- Development Companies: Projects transitioning from exploration to production phases

- Royalty/Streaming: Financial exposure without operational risk

- Exploration: Early-stage companies with discovery potential

Geographic Diversification Considerations

Mining jurisdiction selection requires evaluation of political stability, regulatory frameworks, and infrastructure availability. Developed mining jurisdictions offer regulatory certainty but may have higher operational costs, while emerging markets provide cost advantages with increased political risks.

Portfolio diversification across multiple geographic regions reduces concentration risk while providing exposure to different cost structures and development timelines. Companies operating in mining-friendly jurisdictions like Canada, Australia, and certain U.S. states typically offer more predictable operating environments.

Regional considerations include:

- Regulatory Environment: Permitting efficiency and policy stability

- Infrastructure: Transportation, power, and skilled labour availability

- Political Risk: Government stability and mining industry support

- Cost Structure: Labour, energy, and regulatory compliance expenses

Risk Management and Position Sizing

Position sizing relative to central bank buying sustainability requires consideration of institutional timeframes and accumulation objectives. Central banks typically implement strategic allocation decisions over multi-year periods, providing sustained demand support for precious metals markets.

Correlation monitoring with broader commodity cycles helps investors understand when precious metals may outperform or underperform relative to other asset classes. During periods of dollar weakness and monetary accommodation, precious metals typically demonstrate strong relative performance.

Risk Management Framework:

- Allocation Limits: Appropriate position sizes within diversified portfolios

- Correlation Analysis: Understanding relationships with other asset classes

- Rebalancing Triggers: Predetermined adjustment points based on performance

- Exit Strategy Development: Planning for potential demand normalisation scenarios

Speculative Investment Opportunities

Early-stage exploration companies offer potential for significant returns during precious metals bull markets, though these investments carry substantial risks requiring careful due diligence and position sizing. Companies with experienced management teams, favourable jurisdictions, and brownfields projects offer better risk-adjusted return profiles.

Prospect generator models provide risk diversification through portfolio approaches where companies develop multiple projects simultaneously while partnering with larger operators for development capital. This structure reduces single-project dependency while maintaining upside exposure to successful discoveries.

The current environment of sustained institutional demand creates favourable conditions for precious metals exploration and development companies, though investors should maintain appropriate risk management discipline and diversification strategies when participating in speculative opportunities. For instance, why central banks are buying gold provides additional context for these strategic decisions.

Disclaimer: This analysis is for educational purposes and does not constitute investment advice. Precious metals investments carry risks including price volatility, storage costs, and potential liquidity constraints. Central bank policies and market conditions can change rapidly, affecting investment performance. Investors should conduct independent research and consider consulting qualified financial advisors before making investment decisions.

Seeking exposure to precious metals opportunities from institutional demand?

Discovery Alert's proprietary Discovery IQ model provides real-time notifications on significant ASX mineral discoveries, including gold and precious metals announcements that institutional investors are actively seeking. With central banks driving unprecedented demand for precious metals assets, subscribers gain immediate access to actionable trading and investment opportunities in the Australian mining sector. Explore why major mineral discoveries can generate substantial returns and begin your 30-day free trial today to position yourself ahead of the institutional demand surge.