June 21, 2026

The Mechanics Behind Gold's Rate Sensitivity: Why Monetary Policy Moves Markets

Few relationships in financial markets are as consistently misunderstood as the one between interest rates and gold prices. Most investors know the headline rule: rising rates hurt gold, falling rates help it. However, the underlying mechanics are more nuanced than that simple formula suggests, and understanding those mechanics is essential for anyone navigating precious metals markets. This is precisely why gold plunges as fed keeps rates unchanged — a pattern worth dissecting in detail.

Gold is a non-yielding asset. It pays no interest, no dividend, and no coupon. When interest rates rise or remain elevated, investors holding gold are effectively forgoing the returns available from Treasury bonds, money market funds, and other yield-bearing instruments. This is the opportunity cost principle at work, and it is the single most powerful short-term force acting on gold prices when central bank policy shifts.

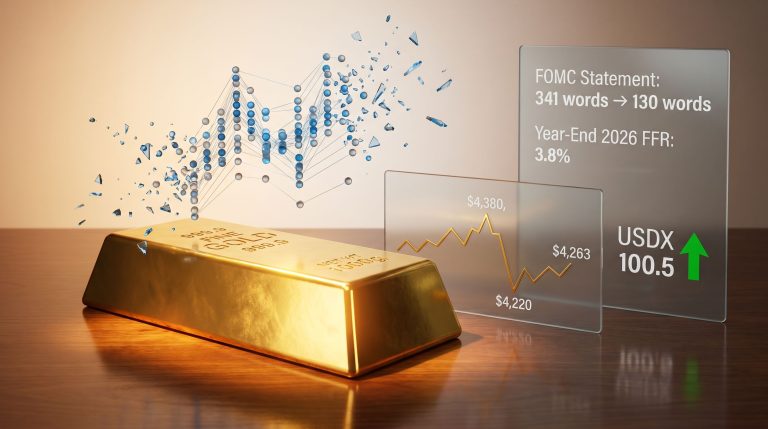

When the Federal Reserve held the federal funds rate steady in June 2026, the market reaction was swift and unambiguous. Spot gold fell 1.03% to $4,285.52 per ounce, while August gold futures declined 0.84% to $4,317.80. That immediate repricing reflects a recalibration of opportunity cost across thousands of portfolios simultaneously, as reported by CNBC's live market coverage.

When big ASX news breaks, our subscribers know first

Kevin Warsh's First FOMC Decision Sets a Hawkish Tone

The June 2026 Federal Open Market Committee meeting carried symbolic weight beyond just the rate decision itself. It marked the first policy outcome under newly installed Fed Chair Kevin Warsh, and markets were watching closely for signals about the direction of the institution under his leadership.

The FOMC held the federal funds rate at 3.50% to 3.75%, citing ongoing inflationary pressures that remain above the committee's 2% target. Critically, the statement specifically identified energy sector price increases driven by supply shocks as a contributing factor. This is an important distinction: supply-driven inflation is harder for monetary policy to address than demand-pull inflation, creating a genuine policy dilemma.

When a central bank acknowledges that inflation is partly the result of supply disruptions rather than excess demand, it signals that tighter monetary policy alone cannot fully resolve the problem. Yet rates must remain elevated to prevent inflation expectations from becoming unanchored.

That tension is precisely what makes the current environment so challenging for gold investors. The Fed is not raising rates aggressively, but it is also signalling clearly that cuts are not imminent. That higher-for-longer posture is arguably more damaging to gold over time than a sharp rate spike, because it removes the expectation of near-term relief. Furthermore, understanding gold and bond dynamics helps illuminate why this environment creates such persistent headwinds.

Breaking Down the Price Data: Spot Gold vs. Futures

Understanding why different data sources reported different gold price levels on the same day requires a brief explanation of market structure.

| Metric | Spot Gold (XAU/USD) | August Gold Futures (@GC.1) |

|---|---|---|

| Price Change | -1.03% | -0.84% |

| Price Level | $4,285.52/oz | $4,317.80/oz |

| Market Type | Physical/OTC | Exchange-traded contract |

| Primary Driver | Immediate supply/demand | Forward-looking sentiment |

Spot gold represents the current market price for immediate delivery, while futures contracts reflect expectations about where prices will be at a future settlement date. The slight divergence between the two is normal and reflects the cost of carry, storage expectations, and speculative positioning in the futures market.

Reuters and CNBC reported slightly different intraday figures because commodity prices fluctuate continuously. Snapshots taken at different timestamps during active trading sessions will naturally differ, and neither figure is incorrect. This multi-source variance is a standard feature of real-time commodity reporting, not an inconsistency in the underlying data.

The broader significance is that both the spot and futures markets moved in the same direction with meaningful magnitude, confirming that the post-FOMC selloff was not a brief algorithmic glitch but a genuine repricing event.

The Higher-for-Longer Rate Framework and Its Structural Impact on Gold

The phrase higher-for-longer has become the defining macroeconomic narrative of the current monetary cycle, and its implications for precious metals deserve careful examination.

When markets price in rate cuts that never materialise, gold tends to give back gains accumulated in anticipation of those cuts. This dynamic has played out repeatedly across rate cycles. Real yields, which adjust nominal Treasury yields for inflation expectations, are arguably more important than nominal rates alone when assessing gold's fair value at any given moment.

Why Do Real Yields Matter So Much?

Here is why real yields matter so much:

- When real yields are negative, gold effectively outperforms cash, making it an attractive store of value even without yield.

- When real yields are positive and rising, the opportunity cost of holding gold becomes increasingly painful for portfolio managers.

- When real yields are positive but stable, gold can trade range-bound, with direction determined by geopolitical risk and dollar strength.

The current environment sits in the second category. With nominal rates held at 3.50% to 3.75% and inflation still above target, real yields remain in positive territory, creating persistent headwinds for gold.

Supply Shock Inflation vs. Demand-Pull Inflation: Why the Distinction Matters for Gold

Not all inflation is the same from gold's perspective, and this is one of the most underappreciated dynamics in precious metals analysis.

Demand-pull inflation, which occurs when consumer spending and economic growth outpace supply, historically benefits gold because it reflects a broad erosion of purchasing power across the economy. Central banks respond by raising rates, but gold often moves higher in anticipation before policy tightens fully.

Supply shock inflation, by contrast, is more targeted. When energy prices surge because of geopolitical disruptions, production constraints, or logistical bottlenecks, the inflationary impulse is concentrated rather than broad-based. This creates a more complicated environment for gold:

- The gold safe-haven appeal that supply shocks generate can support prices.

- Simultaneously, the central bank's response of holding rates elevated suppresses gold through the opportunity cost mechanism.

- The net result is often sideways or mildly declining gold prices, with elevated volatility.

This explains why gold, despite sitting near historically elevated price levels above $4,000 per ounce, remains vulnerable to sharp intraday declines whenever the Fed reinforces a restrictive posture.

Precious Metals Compared: How Silver and Platinum Respond Differently

Not every precious metal reacts to Fed decisions in the same way, largely because their demand structures differ significantly.

| Metal | Primary Demand Driver | Rate Sensitivity | Typical Post-Hold Reaction |

|---|---|---|---|

| Gold | Monetary / Safe Haven | Very High | Negative |

| Silver | Industrial + Monetary | High | Moderately Negative |

| Platinum | Industrial (Auto/Hydrogen) | Moderate | Mixed |

Silver occupies an interesting middle ground. Roughly half of annual silver demand comes from industrial applications including solar panels, electronics, and medical devices. This industrial demand provides a partial buffer against rate-driven selling pressure. However, silver's monetary characteristics still expose it to significant downside when the Fed turns hawkish. In addition, the gold-silver ratio analysis provides further context on how these two metals diverge during restrictive monetary cycles.

Platinum is even more insulated from rate sensitivity in the short term, because its primary demand comes from automotive catalytic converters and, increasingly, from hydrogen fuel cell technology. Rate decisions matter less to platinum's price than trends in electric vehicle adoption, emissions regulations, and industrial production levels.

For investors constructing a precious metals allocation, this divergence in rate sensitivity is a useful portfolio construction tool. Overweighting platinum relative to gold during periods of sustained rate elevation is a strategy worth examining, though it introduces its own set of industrial and geopolitical risks.

The next major ASX story will hit our subscribers first

What Could Reverse the Gold Selloff: Key Catalysts to Monitor

A single FOMC decision does not permanently define gold's trajectory. Several catalysts have the potential to reverse the current bearish pressure, and understanding them is essential for positioning.

1. A pivot in Fed rate expectations. If inflation data surprises to the downside in coming months, market participants will rapidly reprice the probability of rate cuts. Gold tends to rally aggressively in anticipation of easing cycles, often before the first cut actually occurs.

2. Geopolitical risk escalation. Gold's safe-haven premium can override rate logic during periods of acute geopolitical stress. When uncertainty spikes across equity and credit markets simultaneously, capital flows into gold regardless of the interest rate environment.

3. U.S. dollar weakness. Gold is priced in U.S. dollars globally, meaning dollar depreciation mechanically lifts gold prices for international buyers and creates reflexive demand. A weakening dollar index has historically been one of gold's most reliable positive catalysts.

4. Central bank accumulation. Central bank gold demand from emerging markets, particularly those in Asia and the Middle East, has been significant over recent years. This structural demand creates a price floor that purely rate-driven analysis may underestimate. Central bank buying is largely insensitive to short-term rate movements, making it a powerful long-term support mechanism.

Practical Implications for Gold Investors

The June 2026 rate hold reinforces a set of portfolio considerations that precious metals investors should actively revisit.

For short-term traders, the post-FOMC environment favours caution on long gold positions until either rate cut expectations firm up or a geopolitical catalyst emerges. Technical traders will be watching whether gold can hold above its 30-day low, as a failure to do so could trigger further algorithmic selling. According to Reuters, investor positioning ahead of Fed decisions has consistently proved to be a key determinant of post-announcement price swings.

For long-term holders, the picture is more nuanced. Gold above $4,000 per ounce represents a historically elevated price level, and the structural reasons that drove that rally — including central bank diversification away from the U.S. dollar, persistent geopolitical fragmentation, and sovereign debt concerns — have not disappeared. The rate hold creates a tactical headwind, not a structural reversal. Consequently, monitoring the broader gold price outlook remains essential for assessing longer-term positioning.

Hedging strategies worth considering in this environment include:

- Allocating a portion of precious metals exposure to platinum or palladium, which carry different rate sensitivities.

- Using options strategies to limit downside on gold positions while maintaining upside participation if rate cut expectations emerge.

- Monitoring real yield movements via the 10-year Treasury Inflation-Protected Securities (TIPS) yield as the most direct signal for gold's near-term direction.

Frequently Asked Questions

Why Does Gold Fall When the Fed Keeps Rates Unchanged?

When rates remain elevated, yield-bearing assets like Treasury bonds become more attractive relative to gold, which generates no return. This opportunity cost dynamic reduces demand for gold and pushes prices lower, particularly when a hold signals that rate cuts are not imminent. It is precisely this mechanism that explains why gold plunges as fed keeps rates unchanged.

What Is the Relationship Between Treasury Yields and Gold Prices?

The two have an inverse relationship. When Treasury yields rise or remain high, the cost of holding gold increases because investors forgo that yield. When yields fall, gold becomes relatively more attractive. Real yields, which subtract inflation from nominal yields, are the more precise indicator of this relationship.

Who Is Kevin Warsh and Why Does His Leadership Matter for Monetary Policy?

Kevin Warsh is an economist and former Federal Reserve Governor who was appointed as Fed Chair ahead of the June 2026 FOMC decision. His tenure began with a rate hold that markets interpreted as consistent with a restrictive monetary stance, though it is too early to characterise a long-term policy direction from a single meeting.

Does Gold Always Decline After a Fed Hold Decision?

No. The market's reaction depends on how the hold is communicated and what expectations were priced in beforehand. If markets expected a rate cut and received a hold, the reaction tends to be sharply negative for gold. If a hold was widely anticipated, the price impact may be minimal or even positive if the accompanying statement is interpreted as more dovish than feared.

How Does Inflation Affect Gold Prices When Rates Are Also Elevated?

This is one of the most complex dynamics in precious metals analysis. In theory, inflation should support gold as a store of value. In practice, if the central bank responds to inflation by keeping rates high, the opportunity cost effect often dominates the inflation-hedge benefit in the short term. Over longer horizons, sustained inflation that erodes real purchasing power tends to reassert gold's value.

Key Takeaways from the June 2026 Fed Decision

- The FOMC held the federal funds rate at 3.50% to 3.75%, reinforcing a higher-for-longer monetary posture.

- Spot gold fell 1.03% to $4,285.52 per ounce in the immediate aftermath, confirming once again that gold plunges as fed keeps rates unchanged in a restrictive environment.

- The Fed explicitly cited above-target inflation and supply-driven energy price increases as justification for the hold, signalling limited appetite for near-term cuts.

- Gold's sensitivity to opportunity cost dynamics means sustained elevated real yields will continue to cap upside potential in the near term.

- Central bank accumulation, dollar weakness, and geopolitical risk escalation remain the primary catalysts capable of reversing the current bearish pressure.

- Investors should track real TIPS yields, the U.S. dollar index (DXY), and incoming inflation data as the most reliable forward indicators for gold's next directional move.

This article is intended for informational purposes only and does not constitute financial advice. Precious metals prices are subject to significant volatility, and past performance is not indicative of future results. Investors should conduct their own research and consult a qualified financial adviser before making investment decisions.

Want to Stay Ahead of Major Mineral Discoveries Before the Broader Market Reacts?

While gold's sensitivity to monetary policy creates short-term volatility, significant wealth in the resources sector is often built through identifying transformative mineral discoveries at the earliest possible moment — and that's precisely what Discovery Alert delivers, using its proprietary Discovery IQ model to provide real-time ASX discovery alerts that turn complex mineral data into actionable opportunities. Explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.