July 14, 2026

The Rate-Hike Mirage: Why Conventional Finance Keeps Getting Gold Wrong

Every generation of investors inherits a set of market axioms that feel immutable until they suddenly are not. One of the most persistent of these inherited assumptions is the idea that rising interest rates are structurally bearish for gold. Financial media repeats this framework so reliably that it has achieved the status of received wisdom, rarely interrogated and almost never stress-tested against historical evidence. The debate between gold bugs versus mainstream narrators captures this tension precisely. Yet the empirical record tells a far more complicated story, and understanding that gap between the dominant narrative and observable market reality is precisely what separates effective gold investors from reactive ones.

When big ASX news breaks, our subscribers know first

The Ideological Fault Line Separating Gold Bugs from Mainstream Thinking

The disagreement between gold advocates and conventional financial commentators is not simply a dispute about price direction. It reflects two fundamentally incompatible theories of money itself.

Two Competing Monetary Worldviews

Gold advocates, often labelled gold bugs by critics, operate from the premise that sound money must exist independently of political institutions. In their framework, gold's value derives from its finite supply, its inability to be created through policy decisions, and its freedom from counterparty risk. Fiat currency, by contrast, is viewed as a political instrument whose purchasing power is structurally vulnerable to the preferences of whoever controls the printing mechanism at any given moment.

Mainstream financial thinking inverts this logic. Within the orthodox framework, gold is a non-productive relic that generates no cash flow, pays no dividend, and offers no yield. Central banks are viewed as stabilising institutions, fiat flexibility is considered a feature rather than a defect, and gold's role in a portfolio is treated as an emotional preference rather than a rational allocation decision.

The conflict between gold advocates and conventional financial media is not merely a disagreement about asset prices. It is a fundamental clash over monetary sovereignty, the legitimacy of central banking, and what constitutes real money in an era of unprecedented sovereign debt.

Why the Debate Has Never Been Resolved

This ideological fault line has persisted for over a century because both frameworks contain partial truths. Fiat systems have demonstrated genuine capacity to manage short-term economic crises. Gold has demonstrated genuine capacity to preserve purchasing power across multi-decade horizons. The debate intensifies precisely during periods when sovereign debt levels, inflation dynamics, and geopolitical instability make each side's core claims simultaneously more and less defensible.

Why the Mainstream Rate-Hike Narrative Fails to Explain Gold's Behaviour

The conventional rate-gold inverse relationship rests on a simple opportunity cost argument: when risk-free yields rise, holding a non-yielding asset like gold becomes relatively less attractive. This logic is internally coherent but historically unreliable. Furthermore, the gold price forecast for the current cycle challenges these assumptions further.

The Empirical Record Across Three Key Cycles

| Period | Fed Funds Rate Movement | Gold Price Movement | Inflation Rate |

|---|---|---|---|

| 1971 to 1980 | Rose from approximately 4% to approximately 20% | Rose from approximately $35/oz to approximately $850/oz | Peaked above 14% |

| 2015 to 2018 | Rose from 0.25% to 2.5% | Broadly range-bound, then rallied | Moderate and contained |

| 2022 to 2024 | Rose from near 0% to approximately 5.25% | Gold roughly doubled from $2,000 toward $4,000 | Multi-decade highs |

The table above illustrates a pattern that challenges the mainstream framework at its foundation. During each of these three distinct monetary tightening cycles, gold either held its value or appreciated substantially. The 1971 to 1980 period is the most instructive: gold delivered a gain exceeding 2,300% while the Federal Reserve raised rates to historically extreme levels to combat runaway inflation. Rather than suppressing gold, rising rates coincided with one of the metal's most spectacular bull markets.

The Real Interest Rate Variable That Gets Ignored

The critical variable that mainstream commentary consistently underweights is the distinction between nominal and real interest rates. What matters to gold is not the absolute level of the policy rate but whether that rate exceeds the prevailing inflation rate once adjusted for the true cost of living. The gold and bonds dynamics at play here are often overlooked entirely by conventional analysts.

When inflation runs above the nominal rate, real rates remain negative, and the opportunity cost argument for holding gold evaporates. Holding cash or short-duration bonds in a negative real rate environment involves an ongoing, guaranteed loss of purchasing power. Gold, which carries no such guaranteed erosion, becomes comparatively attractive.

How Sovereign Debt Changes the Entire Calculus

There is a further dimension that the mainstream rate framework ignores entirely: the impact of rate hikes on the government itself. When sovereign debt levels are modest, higher rates primarily affect borrowers in the private sector. However, when government debt reaches the scale now observable across major Western economies, a rate increase functions as a fiscal shock to the state rather than a monetary restraint on gold.

Analysis from Stewart Thomson of Graceland Investment Management, published on Gold-Eagle.com, highlights this asymmetry clearly. If US rates normalised to the levels considered standard during the 1970s, in the range of 8%, the US government's interest payment obligations would likely approach or exceed the point of fiscal unsustainability given current debt outstanding. In that environment, a rate hike hurts the issuer of the fiat currency far more severely than it hurts the holder of gold.

What Is Actually Driving the Gold Price in 2026

Understanding the current gold market requires moving beyond the rate narrative entirely and examining the actual supply and demand variables operating in real time.

The Indian Demand Shock

One of the most significant and underreported forces currently weighing on gold prices is a structural demand collapse from India. New Indian government tariff measures combined with a government-directed consumer moratorium have removed an estimated 40 to 70 tonnes of monthly gold demand from global markets. India has historically ranked among the world's largest gold-consuming nations, and this policy-driven withdrawal represents a material headwind to short-term gold pricing that is entirely separate from monetary policy dynamics.

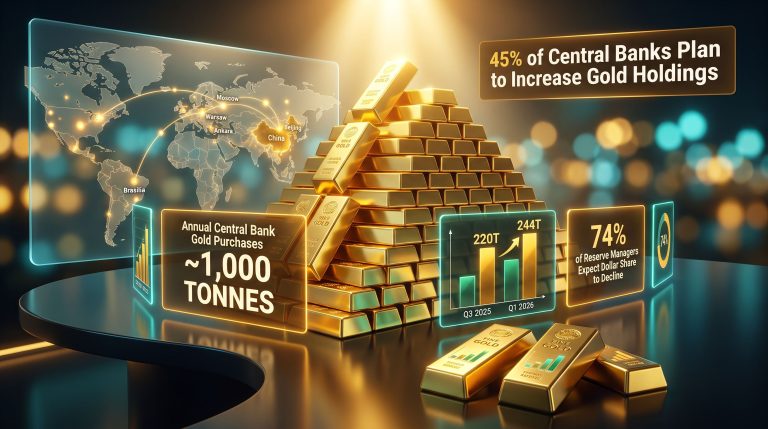

Central Bank Behaviour: From Buyers to Sellers

The central bank gold demand picture has also shifted considerably. Institutions that were consistent net purchasers of gold over the preceding several years have paused or reversed their accumulation. A significant driver behind this reversal is the escalating geopolitical contest for control of the Strait of Hormuz between the United States and Iranian governments.

Central banks facing economic disruption from this conflict require liquid fiat reserves to manage domestic financial stress, and gold liquidation provides that liquidity. This creates tactical selling pressure that sophisticated investors can treat as an entry opportunity rather than a directional signal.

Strategic Petroleum Reserve Depletion and the Inflation Feedback Loop

America's Strategic Petroleum Reserve has been drawn down to historically depleted levels. The process of rebuilding those reserves, which must eventually occur at scale, will inject sustained upward pressure on global crude oil prices and, through the energy cost transmission mechanism, into broader consumer price inflation. This dynamic is structurally bullish for gold over the medium term regardless of what the Federal Reserve does with its policy rate in any given quarter.

The depletion of government oil reserves across major economies creates a structural imperative to repurchase crude at scale, a process that injects significant upward pressure into energy costs and, by extension, broader consumer price inflation. This dynamic is historically bullish for gold over the medium term.

The Shipflation Signal: An Inflation Indicator the Market Is Underpricing

One of the most revealing cross-asset signals in the current environment is the extraordinary performance of shipping-related investment vehicles. The Breakwave shipping ETF, which tracks dry bulk freight rates and functions as a proxy for global supply chain stress, has delivered gains exceeding 100% over a twelve-month period. Freight costs are a leading indicator for consumer price inflation because they represent the cost of moving physical goods from production to consumption. When shipping costs rise sharply, consumer prices follow with a lag of several months.

The AI Bubble Versus Hard Asset Divergence

| Asset Category | Narrative Driver | Recent Performance Signal |

|---|---|---|

| AI and Technology Equities | Earnings growth optimism | Elevated valuations, momentum-driven |

| Shipping and Freight ETFs | Supply chain disruption, war premium | Over 100% gains reported over 12 months |

| Gold | Monetary debasement, inflation hedge | Approximately doubled from $2,000 toward $4,000 |

| Fiat Currency (USD) | Fed policy, reserve currency status | Purchasing power erosion under structural inflation |

While speculative capital concentrates in technology equities trading at stretched valuations, inflation-sensitive real assets are quietly compounding returns. This divergence tends to self-correct over time as inflation persistently erodes the real earnings assumptions embedded in growth stock valuations.

Navigating Buy Zones During Narrative-Driven Selloffs

One of the most actionable insights for gold investors during periods of bearish narrative dominance is the identification of technically significant price zones where risk-reward tilts in the buyer's favour. Understanding gold's safe-haven role becomes particularly important when navigating these emotionally charged selloff periods.

The $3,900 Zone in Context

The $3,900 price level in gold established itself as a meaningful reference point following the late October 2025 low. As gold subsequently pulled back toward this region in mid-2026, the zone offered a technically relevant accumulation opportunity. However, it is important to calibrate expectations correctly. Not every support zone carries equal analytical weight, and the $3,900 level, while a legitimate buying reference, does not represent the highest-conviction entry point on longer-term chart structures.

A Tiered Approach to Position Building

Effective accumulation during narrative-driven selloffs involves several principles:

- Higher-conviction buy zones are those where multiple prior price reactions converge with significant volume clusters, providing multiple layers of technical support

- Lower-conviction zones like $3,900 remain valid entry opportunities but warrant appropriately sized, conservative position increments

- Deploying capital progressively across a price zone rather than committing to a single transaction reduces timing risk considerably

- CPI and PPI data releases create short-term volatility events that may briefly breach support levels, generating more attractive entry prices for prepared investors

Gold Mining Equities: Leverage and Historical Context

For investors seeking leveraged exposure to a gold recovery, gold mining equity leverage has historically delivered outsized returns during sharp gold price reversals. Prior buy zone entries, including levels corresponding to gold at $4,400 and $4,100, subsequently rewarded investors with rapid rallies exceeding 20% in senior producers, with junior miners in some instances delivering substantially larger percentage moves over shorter timeframes.

These outcomes are not guaranteed and timing precision remains inherently uncertain. The strategic imperative is accumulation across a zone rather than attempting to identify a single price floor with precision.

The next major ASX story will hit our subscribers first

The 1970s Parallel and What It Means for the Current Cycle

The 1970s represent the most instructive historical precedent for the current macro environment because the structural conditions align across multiple dimensions: persistent inflation, sovereign fiscal stress, geopolitical disruption to energy supply, and a financial media consensus that consistently underestimated gold.

When the Anti-Gold Consensus Collapsed

Throughout the early 1970s, mainstream financial commentary treated gold with the same dismissiveness visible today. The conventional wisdom held that gold had been rendered obsolete by modern monetary management. From the Nixon shock of 1971 through to 1980, gold appreciated from approximately $35 per ounce to over $850 per ounce, a gain exceeding 2,300%, even as interest rates rose aggressively and economists repeatedly predicted gold's imminent correction.

Why Today's Version Could Be More Extreme

The critical structural difference between the 1970s cycle and the present is the absolute level of sovereign debt. In the 1970s, government debt-to-GDP ratios in major Western economies were a fraction of current levels. The Federal Reserve had meaningful capacity to raise rates aggressively without triggering a sovereign debt crisis. Today that capacity is far more constrained. Consequently, if the same inflationary dynamics that forced 1970s-era rate normalisation were to repeat at current debt levels, the fiscal consequences for governments would be far more severe, and the structural case for gold relative to fiat would be correspondingly more powerful.

Gold Bugs Versus Mainstream Narrators: A Framework Comparison

| Analytical Dimension | Gold Advocate Perspective | Mainstream Perspective |

|---|---|---|

| Nature of Gold | Sovereign-free store of value with no counterparty risk | Non-yielding relic with no cash flow generation |

| Fiat Currency | Structurally depreciating through political money creation | Flexible monetary tool enabling economic management |

| Central Banks | Institutions that erode purchasing power systematically | Stabilising forces that prevent deflationary collapse |

| Rate Hikes | Hurt over-indebted governments more than hard assets | Negative for gold due to opportunity cost of holding |

| Inflation | Structural and persistent, driven by debt monetisation | Transitory or manageable through policy intervention |

| Debt Levels | Existential fiscal risk; potential trigger for currency crisis | Manageable within modern monetary frameworks |

Frequently Asked Questions

What does the term gold bug actually mean?

A gold bug is an investor who maintains a strong philosophical conviction that gold represents superior long-term money relative to fiat currency. The term carries a mildly pejorative connotation in mainstream financial media but is often embraced as a badge of conviction by advocates of hard asset investing.

Has gold ever performed well when interest rates were rising?

Yes, consistently. The 1971 to 1980 period saw gold rise over 2,300% as the Fed funds rate climbed from approximately 4% to approximately 20%. The 2022 to 2024 cycle saw gold roughly double even as rates rose from near zero to over 5%. The rate-gold inverse relationship breaks down reliably during periods of negative real rates and elevated sovereign debt.

How do central bank gold sales affect the global gold price?

Central bank gold liquidation introduces short-term selling pressure that can suppress gold prices below levels justified by longer-term fundamentals. However, this selling is typically driven by emergency liquidity requirements rather than a structural reassessment of gold's value, and it historically creates tactical accumulation opportunities for patient investors.

What role does geopolitical conflict play in gold pricing?

Geopolitical disruption affects gold through two competing channels. It increases safe-haven demand from private investors while simultaneously forcing some central banks to liquidate gold holdings to raise emergency fiat liquidity, as is currently observable in the context of the Strait of Hormuz conflict. These opposing forces can create short-term price weakness during acute geopolitical stress even as the medium-term inflationary consequences of that stress remain bullish for gold.

Building a Psychologically Resilient Investment Posture

Perhaps the most underrated dimension of successful gold investing is psychological rather than analytical. The mainstream financial media narrative generates significant emotional noise, and investors who lack a robust analytical framework tend to react to that noise rather than to the underlying structural drivers.

The four structural forces most relevant to gold's long-term trajectory in 2026 and beyond include:

- Persistent inflationary pressure arising from energy supply disruption and the imperative to rebuild depleted strategic petroleum reserves across major economies

- Unsustainable sovereign debt trajectories that constrain the effectiveness of rate hikes as inflation management tools and place fiscal stress primarily on governments rather than on hard asset holders

- Geopolitical fragmentation driving emergency central bank liquidity events that generate tactical entry points for prepared accumulation

- Currency debasement dynamics that accelerate when governments face the choice between inflation and default and consistently choose the former

The most durable advantage available to gold-oriented investors is not a superior price forecast. It is a superior analytical framework that correctly identifies which macro variables are structurally driving gold, rather than reacting to short-term narrative cycles manufactured by financial media.

The gold bugs versus mainstream narrators debate ultimately resolves not through rhetorical victory but through price discovery over time. History suggests that when sovereign fiscal constraints collide with persistent inflation, the analytical framework that correctly weights monetary debasement risk tends to outperform the one that anchors to nominal rate comparisons. The current macro environment, characterised by depleted energy reserves, geopolitical disruption, historically elevated debt, and a shipping cost surge that functions as a leading inflation indicator, presents a compelling case for stress-testing every inherited assumption about how gold responds to rising rates.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. All investment decisions should be made in consultation with qualified financial advisors. Past performance of any asset class, including gold and gold mining equities, is not indicative of future results. All investments carry risk, including the potential loss of capital.

Want To Catch The Next Major ASX Mineral Discovery Before The Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through market noise to surface actionable opportunities the moment they're announced — explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.