May 16, 2026

The journey from laboratory breakthrough to industrial reality represents one of the most challenging phases in advanced materials development. While graphene's exceptional properties have been documented since 2004, when researchers at the University of Manchester first isolated this single-layer carbon structure, the path to commercial viability has proven far more complex than early optimists anticipated. Despite significant progress, graphene technology commercialisation continues to face unique challenges that distinguish it from traditional technology adoption cycles.

Why Has Graphene Technology Commercialisation Taken Two Decades to Materialise?

The transition phase between proven laboratory capabilities and economically viable production methods has created what industry experts term the "valley of death" for promising technologies. This critical gap has claimed numerous advanced materials over the past two decades, where technical feasibility fails to translate into commercial success.

For graphene technology commercialisation, this valley proved particularly treacherous due to the material's exceptional performance characteristics actually exceeding practical engineering requirements for most applications. When a material demonstrates electrical conductivity superior to copper, thermal conductivity exceeding traditional heat sinks by factor of ten, and mechanical strength surpassing steel, the challenge becomes justifying premium pricing for applications that function adequately with conventional materials.

The fundamental disconnect emerged between what graphene could theoretically achieve and what industrial customers actually needed. Early commercialisation attempts focused on leveraging maximum performance capabilities rather than identifying applications where graphene's unique properties solved specific, costly problems that existing materials could not address.

The "Valley of Death" Challenge in Advanced Materials

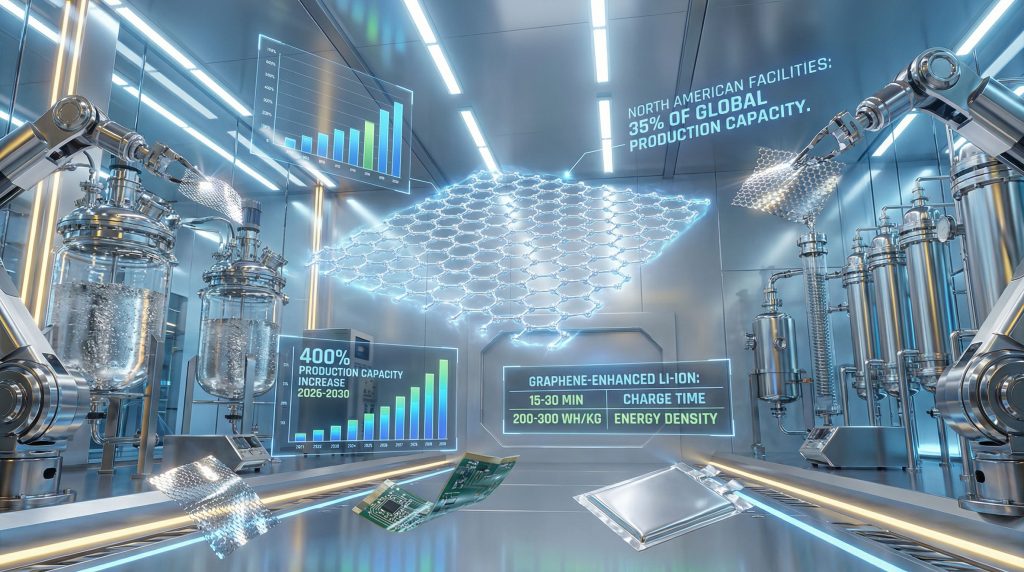

Manufacturing scale economics created insurmountable barriers during the early commercialisation phase. Production methodologies available during the 2010s generated costs exceeding $200-300 per kilogram with inconsistent purity grades ranging from 60-95% single-layer coverage.

Chemical reduction approaches offered improved scalability but introduced quality control challenges that prevented reliable performance across different production batches. Industrial customers require consistent material properties for qualification processes, equipment design, and long-term supply agreements.

Variability in electrical conductivity, thermal management capabilities, or mechanical reinforcement properties between batches made graphene unsuitable for critical applications despite laboratory demonstrations of exceptional performance. The cost-performance equation proved particularly challenging in sectors like coatings, where traditional epoxy formulations provide adequate corrosion protection at established price points.

Regulatory Approval Timelines for Novel Material Applications

Advanced materials face extended regulatory qualification periods, particularly for applications involving human contact, food packaging, medical devices, or critical infrastructure. Graphene's classification as a nanomaterial triggered additional safety assessment requirements that extended commercialisation timelines beyond typical industrial adoption cycles.

Environmental impact assessments for nanomaterial release during manufacturing, application, and end-of-life disposal required comprehensive studies spanning multiple years. These regulatory hurdles created significant capital requirements for companies pursuing battery-grade production trends, as extensive testing and documentation preceded any revenue generation opportunities.

The lack of established international standards for graphene quality specifications further complicated regulatory approval processes. Without standardized testing methodologies for purity, layer consistency, or defect density, regulatory agencies required custom qualification protocols for each application category, multiplying approval timelines and costs.

When big ASX news breaks, our subscribers know first

What Industrial Applications Are Driving Current Graphene Adoption?

Market forces have shifted dramatically as specific industrial sectors encounter performance limitations that conventional materials cannot address. The convergence of artificial intelligence infrastructure demands, electric vehicle acceleration requirements, and next-generation electronics miniaturisation has created application niches where graphene's premium properties justify economic investment.

Energy Storage Revolution: Beyond Traditional Battery Chemistry

Battery technology represents the most commercially advanced application area for graphene integration, driven by electric vehicle charging speed requirements and grid-scale energy storage demands. Traditional lithium-ion systems face fundamental constraints in charge rate capabilities that graphene-enhanced formulations can address through improved electrical conductivity and thermal management.

| Technology Type | Charge Time | Energy Density | Cost Premium | Commercial Status |

|---|---|---|---|---|

| Lithium-Ion Standard | 60-120 min | 150-250 Wh/kg | Baseline | Mass Production |

| Graphene-Enhanced Li-Ion | 15-30 min | 200-300 Wh/kg | 2-3x | Early Commercial |

| Graphene Aluminium-Ion | 6-10 min | 180-220 Wh/kg | 1.5-2x | Pilot Scale |

Recent developments in aluminium-ion battery chemistry demonstrate graphene's role in enabling entirely new electrochemical systems. These configurations achieve six-minute charging cycles with energy density approaching premium lithium technologies, representing breakthrough performance for applications requiring rapid energy replenishment cycles.

The thermal management advantages prove particularly critical for fast-charging applications, where traditional battery systems experience performance degradation or safety risks under high-current conditions. Graphene's thermal conductivity enables heat dissipation that maintains battery performance during rapid charging cycles, addressing infrastructure limitations that currently constrain electric vehicle adoption rates.

Thermal Management Solutions for Data Centre Infrastructure

Data centre cooling requirements have intensified dramatically with artificial intelligence computational loads and high-density processing configurations. Traditional cooling systems face efficiency limitations and energy consumption challenges that graphene-based thermal management solutions can address through superior heat transfer capabilities.

Graphene's thermal conductivity of approximately 5,000 W/mK at room temperature exceeds copper (385 W/mK) and aluminium (205 W/mK) by significant margins, enabling more efficient heat sink designs and reduced cooling energy requirements. This performance differential translates into meaningful operational cost savings for data centre operators managing thousands of processing units.

Furthermore, heat dissipation improvements enable higher computational density configurations, allowing data centres to achieve greater processing capacity within existing facility footprints. This capability becomes particularly valuable in urban areas where real estate costs make facility expansion economically challenging.

Advanced Composites Replacing Traditional Carbon Materials

Aerospace and automotive applications drive demand for lightweight, high-strength materials that exceed traditional carbon fibre capabilities. Graphene-enhanced composite materials offer improved strength-to-weight ratios while maintaining manufacturing compatibility with existing production processes.

The integration challenges that previously limited composite adoption have been addressed through improved dispersion techniques and manufacturing process modifications. Companies can now incorporate graphene additives into established composite production workflows without requiring complete manufacturing system redesigns.

These applications benefit from graphene's multifunctional properties, where single material additions provide mechanical reinforcement, electrical conductivity for electromagnetic shielding, and thermal management capabilities. This consolidation reduces system complexity compared to traditional approaches requiring separate materials for each performance requirement.

Which Manufacturing Breakthroughs Have Enabled Industrial Scale Production?

The transformation from laboratory curiosity to industrial commodity required fundamental advances in production methodologies, quality control systems, and cost reduction strategies. These breakthroughs occurred through systematic engineering improvements rather than single technological leaps.

Synthetic Production Methods Solving Purity Consistency Issues

Chemical synthesis approaches have replaced mechanical exfoliation and chemical reduction methods for commercial-scale production, addressing the purity and consistency challenges that limited earlier commercialisation efforts. Synthetic detonation graphene (SDG) and controlled chemical vapour deposition techniques generate consistent 95%+ monolayer purity grades suitable for demanding applications.

These synthetic methods provide batch-to-batch reproducibility essential for industrial qualification processes. Manufacturing customers require material specifications with narrow tolerance ranges for electrical conductivity, thermal properties, and mechanical characteristics.

The transition to synthetic methodologies also enables customisation of graphene properties for specific applications. Layer thickness, defect density, and surface functionalisation can be controlled during production rather than requiring post-processing treatments that add cost and complexity.

Cost Reduction Strategies: From $200/kg to Sub-$50/kg Economics

Production scaling has achieved dramatic cost reductions essential for commercial viability across cost-sensitive applications. Manufacturing facilities now operate at 100+ tonne annual capacity levels, enabling economies of scale that reduce unit costs by 75-80% compared to early production methods.

Raw material optimisation represents a significant cost reduction factor, with synthetic production methods utilising readily available carbon feedstocks rather than requiring high-purity graphite starting materials. This supply chain simplification reduces input costs and eliminates dependency on specialised graphite suppliers.

Equipment utilisation improvements through continuous production processes, rather than batch-based methods, have increased manufacturing efficiency and reduced labour costs per unit output. These operational improvements enable competitive pricing for volume applications while maintaining acceptable profit margins for specialised manufacturers.

Quality Control Standards for Industrial-Grade Graphene

International standardisation efforts have established testing methodologies and specification frameworks that enable consistent quality assessment across different suppliers and production methods. These standards reduce customer qualification time and enable broader supply chain adoption.

Quality control systems now incorporate real-time monitoring of production parameters that affect final product specifications. Electrical conductivity, thermal properties, and mechanical characteristics can be measured during production rather than requiring extensive post-production testing that delays material delivery.

In addition, the development of industry-specific quality grades enables optimised material specifications for different application categories. Electronics applications require different purity levels and electrical characteristics compared to structural composites or thermal management systems, allowing manufacturers to optimise production for specific market segments.

How Are Global Supply Chains Adapting to Graphene Integration?

Supply chain evolution reflects the strategic positioning of different geographic regions to capture value across the graphene technology commercialisation spectrum. Regional specialisation has emerged based on manufacturing capabilities, regulatory frameworks, and market proximity factors.

North American Production Hubs vs. Asian Manufacturing Centres

North American facilities have established leadership in high-purity synthetic graphene production, leveraging advanced manufacturing capabilities and proximity to aerospace, automotive, and electronics customers requiring premium material grades. Canadian operations particularly excel in synthetic production methodologies that generate consistent quality specifications.

"North American facilities now represent 35% of global graphene production capacity, with Canadian operations leading in high-purity synthetic variants. Asian manufacturers maintain cost advantages in bulk applications, while European facilities focus on specialty grades for automotive and aerospace sectors."

Asian manufacturing centres concentrate on cost-optimised production for bulk applications, including coatings additives, construction materials, and basic electronic components. These facilities leverage established chemical manufacturing infrastructure and supply chain networks to achieve competitive pricing for volume applications.

European production focuses on specialty grades aligned with strict regulatory requirements for automotive and aerospace applications. These facilities develop customised material specifications that meet specific performance standards required for safety-critical applications in transportation and industrial sectors.

Raw Material Dependencies and Vertical Integration Strategies

Upstream graphite supply security has driven vertical integration strategies among graphene manufacturers seeking to control raw material quality and availability. High-grade graphite resources with Total Graphitic Carbon (TGC) content exceeding 7% provide optimal feedstock for synthetic graphene production processes.

Resource projects like the Mahenge Graphite Project in Tanzania, containing 213 million tonnes at 7.8% TGC, represent globally significant raw material reserves capable of supporting large-scale graphene production expansion. These resources provide strategic supply chain security for manufacturers planning substantial capacity increases.

Vertical integration reduces exposure to graphite price volatility and ensures consistent feedstock quality essential for maintaining graphene production specifications. Companies controlling both upstream resources and downstream processing can optimise material properties across the entire production chain.

Logistics Challenges for Nanomaterial Distribution Networks

Nanomaterial handling requirements create specialised logistics challenges that differ from traditional chemical distribution networks. Graphene products require controlled atmospheric conditions, specialised packaging, and careful handling procedures to maintain material properties during transportation and storage.

Distribution networks must accommodate relatively small shipment volumes compared to bulk chemicals while maintaining cost-effective logistics solutions. Graphene applications typically require kilogram to tonne quantities rather than the multi-thousand tonne shipments common in traditional chemical markets.

However, international shipping regulations for nanomaterials vary across jurisdictions, requiring specialised documentation and handling procedures that add complexity to global supply chain operations. These regulatory requirements influence regional production strategies and customer delivery timeframes.

What Investment Patterns Signal Market Maturation?

Capital allocation trends across the graphene technology sector indicate a fundamental shift from research and development funding toward commercial scaling and manufacturing capacity expansion. This transition reflects investor confidence in proven applications and established customer demand.

Venture Capital Shift from R&D to Scaling Manufacturing

Early-stage funding has evolved from supporting fundamental research toward financing manufacturing facility development and production capacity expansion. Investors now prioritise companies with demonstrated customer contracts and proven production capabilities rather than purely technological innovation.

Manufacturing scale-up requirements demand significantly higher capital investments compared to laboratory research, with production facilities requiring multi-million dollar equipment purchases and extended construction timelines. This capital intensity has attracted institutional investors and strategic corporate partners capable of supporting large-scale development projects.

The transition from pilot-scale production (measured in kilograms annually) to commercial-scale facilities (producing hundreds of tonnes annually) requires systematic engineering development and substantial financial commitments. Companies successfully making this transition demonstrate operational capabilities that differentiate them from research-focused organisations.

Corporate Partnership Models: Joint Ventures vs. Acquisition Strategies

Established industrial companies pursue graphene integration through strategic partnerships rather than internal development, reflecting the specialised knowledge and production capabilities required for successful commercialisation. Joint venture arrangements enable technology access while sharing development risks and capital requirements.

Major coatings manufacturers, electronics companies, and automotive suppliers establish collaborative relationships with graphene specialists to develop application-specific formulations and production processes. These partnerships combine market knowledge and customer relationships with specialised graphene technology capabilities.

Acquisition strategies target companies with proven commercial production capabilities and established customer relationships rather than early-stage research organisations. Strategic buyers prioritise operational capabilities, intellectual property portfolios, and market positioning over pure technological innovation.

Government Funding Evolution from Research Grants to Industrial Incentives

Public sector support has transitioned from fundamental research grants toward industrial development incentives that encourage manufacturing capacity expansion and commercial deployment. Government programmes now prioritise economic development and strategic supply chain security objectives, particularly regarding critical minerals energy transition requirements.

Manufacturing incentive programmes support facility development, equipment purchases, and workforce training initiatives that enable commercial-scale production. These programmes recognise graphene as a strategic technology sector requiring policy support for competitive positioning against international alternatives.

National security considerations drive government interest in domestic graphene production capabilities, particularly for aerospace, defence, and critical infrastructure applications. Strategic material considerations influence public sector funding priorities and regulatory framework development.

Which Market Segments Show Strongest Commercial Traction?

Commercial adoption patterns reveal specific application areas where graphene's performance advantages justify premium pricing and integration complexity. These leading segments demonstrate sustainable business models and scalable market opportunities.

Coatings Industry: Anti-Corrosion Performance Driving Adoption

Industrial coating applications represent the most mature commercial market for graphene technology, with proven performance improvements and established customer adoption patterns. Anti-corrosion performance enhancements deliver quantifiable value propositions that justify material cost premiums.

Industrial Coating Performance Metrics:

- Traditional epoxy coatings: 5-7 year lifecycle

- Graphene-enhanced formulations: 12-15 year performance

- Cost-benefit analysis: 60% reduction in maintenance cycles

Field testing with major industrial operators has validated performance claims under real-world operating conditions, including exposure to harsh chemical environments, temperature cycling, and mechanical stress. These validations provide the technical credibility necessary for broader market adoption across industrial maintenance applications.

Major industrial asset owners have incorporated graphene-enhanced coatings into maintenance programmes for critical infrastructure, including oil and gas facilities, mining operations, and marine applications. The extended lifecycle performance reduces total cost of ownership despite higher initial material costs, supporting broader industry innovation trends.

Electronics Manufacturing: Conductive Inks and Flexible Substrates

Electronics applications leverage graphene's electrical conductivity and mechanical flexibility for next-generation circuit designs that traditional materials cannot support. Conductive ink formulations enable printable electronics and flexible circuit applications without the rigidity constraints of copper or silicon-based systems.

Flexible substrate applications particularly benefit from graphene's mechanical properties, maintaining electrical conductivity under bending, stretching, and twisting conditions that would damage traditional circuit materials. These capabilities enable wearable electronics, curved display technologies, and conformal sensor systems.

Manufacturing process compatibility allows graphene integration into established electronics production workflows without requiring complete equipment replacement. This compatibility reduces adoption barriers and enables gradual scaling across different product categories and manufacturing facilities.

Construction Materials: Concrete Enhancement and Infrastructure Applications

Construction sector adoption focuses on concrete enhancement applications where graphene additions improve mechanical properties, durability, and service life. These improvements deliver value through reduced maintenance requirements and extended infrastructure lifecycles.

Graphene-enhanced concrete demonstrates improved tensile strength, crack resistance, and durability under freeze-thaw cycling compared to traditional formulations. These performance improvements prove particularly valuable for infrastructure applications requiring extended service life, including bridges, highways, and building foundations.

The construction industry's established supply chain networks facilitate graphene adoption through existing material distribution channels and application processes. This infrastructure compatibility enables scaling without requiring specialised installation equipment or training programmes, supporting overall sustainability transformation initiatives across the sector.

The next major ASX story will hit our subscribers first

What Technical Barriers Remain for Widespread Adoption?

Despite significant commercialisation progress, technical challenges continue to limit graphene adoption across certain application categories and use environments. Addressing these barriers requires continued engineering development and industry collaboration.

Dispersion Challenges in Liquid-Based Applications

Achieving uniform graphene distribution within liquid matrices remains technically challenging for applications including paints, inks, and polymer systems. Graphene's tendency to agglomerate reduces effective surface area and diminishes performance benefits compared to theoretical capabilities.

Surface functionalisation approaches help improve dispersion characteristics but add manufacturing complexity and cost. Finding optimal functionalisation strategies for specific application requirements requires extensive testing and development work for each product category.

Processing equipment modifications may be necessary to achieve adequate dispersion quality, requiring capital investment and production process changes that create adoption barriers for established manufacturers with existing equipment installations.

Long-Term Stability Testing for Critical Infrastructure Uses

Applications involving critical infrastructure require extensive long-term performance validation that extends beyond typical commercial testing timelines. Aerospace, automotive safety systems, and structural applications demand multi-year or multi-decade service life verification.

Accelerated aging tests provide some performance indication but cannot fully replicate all environmental exposure conditions encountered during extended service periods. This testing requirement extends product qualification timelines and increases development costs for critical applications.

Environmental exposure conditions including ultraviolet radiation, temperature cycling, chemical exposure, and mechanical stress can affect graphene properties over extended periods. Understanding these effects requires comprehensive testing programmes that delay commercial deployment for safety-critical applications.

Standardisation Requirements Across Industrial Applications

Industry-specific standards development remains incomplete for many potential graphene applications, creating qualification uncertainty for both manufacturers and customers. Standardised testing methodologies, performance specifications, and quality requirements facilitate broader market adoption.

International coordination on standards development helps ensure global compatibility and reduces duplicative testing requirements across different geographic markets. This coordination requires collaboration among industry associations, government agencies, and technical organisations.

Application-specific standards must account for the diverse property requirements across different use categories, from electronics to structural materials to biological applications. This diversity requires multiple standardisation efforts rather than single universal specifications.

How Do Regulatory Frameworks Impact Commercialisation Timelines?

Regulatory approval processes significantly influence graphene technology commercialisation schedules, particularly for applications involving human contact, environmental release, or safety-critical systems. Understanding these frameworks enables more accurate development timeline planning.

FDA Approval Pathways for Biomedical Applications

Biomedical applications face extensive regulatory review requirements through established FDA pathways for novel materials and medical devices. Graphene-based biosensors, drug delivery systems, and diagnostic devices require comprehensive safety and efficacy documentation before market approval.

Biocompatibility testing requirements for graphene materials involve extensive animal testing and clinical studies that extend development timelines by several years compared to industrial applications. These studies must demonstrate safety across different exposure routes and duration periods.

The FDA's existing regulatory framework for nanomaterials provides guidance for graphene applications but requires case-by-case evaluation for novel applications. This individual review process creates timeline uncertainty and regulatory costs that influence commercial development strategies.

Environmental Safety Assessments for Nanomaterial Release

Environmental impact assessments for graphene manufacturing and application processes require evaluation of potential nanomaterial release during production, use, and disposal phases. These assessments examine environmental fate, bioaccumulation potential, and ecological effects, similar to broader challenges in graphene commercialisation.

Manufacturing facilities must implement containment systems and monitoring programmes that prevent uncontrolled graphene release into environmental media. These requirements add capital and operational costs that influence production facility design and location decisions.

Life cycle assessment requirements examine environmental impacts across entire product lifecycles, from raw material extraction through end-of-life disposal. These comprehensive evaluations support regulatory decision-making but require extensive data collection and analysis.

International Standards Development for Graphene Quality Specifications

International standards organisations are developing quality specifications and testing methodologies that will facilitate global trade and reduce technical barriers to adoption. These efforts require coordination among multiple national standards bodies and industry organisations.

Quality specifications must address the diverse property requirements across different application categories while maintaining practical testing methodologies that manufacturers can implement cost-effectively. Balancing comprehensiveness with practicality requires extensive industry consultation.

Harmonised international standards reduce testing duplication and enable global supply chain development, but achieving consensus among different national approaches and industry requirements remains challenging and time-consuming.

What Economic Models Support Sustainable Graphene Businesses?

Successful commercialisation requires business models that balance premium technology value with market acceptance and competitive pricing pressures. Different approaches suit various market segments and customer requirements.

Premium Pricing Strategies vs. Volume-Based Market Penetration

Premium pricing approaches target applications where graphene's performance advantages justify significant cost premiums, typically in specialised or high-performance applications. This strategy requires demonstrable value propositions that quantify customer benefits.

Volume-based penetration strategies focus on cost-competitive applications where graphene provides incremental performance improvements at modest price premiums. These approaches require large-scale production capabilities and optimised cost structures.

Market segmentation enables hybrid approaches where companies offer different product grades and pricing strategies for various application categories. This portfolio approach maximises revenue potential across diverse customer requirements and price sensitivity levels.

Licensing vs. Manufacturing Business Models

Licensing strategies enable technology commercialisation without requiring large capital investments in manufacturing infrastructure. This approach suits companies with strong intellectual property portfolios but limited manufacturing capabilities or market reach.

Manufacturing-focused business models provide greater control over product quality, customer relationships, and profit margins but require substantial capital investment and operational expertise. These approaches suit companies with established manufacturing capabilities and market access.

Hybrid models combining licensing and manufacturing enable companies to maximise technology value while limiting capital requirements. Strategic partnerships can provide manufacturing capabilities while maintaining technology ownership and licensing revenue potential.

Customer Education Investment Requirements

Market development requires substantial investment in customer education and application development support, particularly for industries with limited nanomaterial experience. Technical support capabilities often determine commercial success as much as product performance.

Application development programmes help customers integrate graphene into existing products and processes, reducing adoption barriers and accelerating market penetration. These programmes require technical expertise and significant time investment but create competitive differentiation.

Industry collaboration through trade associations, technical conferences, and educational initiatives helps build market awareness and acceptance. These collaborative efforts distribute education costs across multiple industry participants while accelerating overall market development.

Which Geographic Markets Lead Graphene Technology Adoption?

Regional adoption patterns reflect different market development strategies, regulatory environments, and industrial requirements. Understanding these geographic differences guides market entry and expansion planning.

Asia-Pacific Manufacturing Integration Rates

Asia-Pacific manufacturing centres demonstrate rapid graphene integration across electronics, automotive, and industrial applications. Established manufacturing infrastructure and supply chain networks facilitate technology adoption and scaling.

Electronics manufacturing in China, South Korea, and Japan drives significant graphene demand for conductive applications, flexible circuits, and thermal management systems. These markets benefit from integrated supply chains and established customer relationships.

Government technology development programmes in several Asia-Pacific countries support graphene research and commercialisation through funding incentives, infrastructure development, and regulatory framework advancement. These programmes accelerate market development and competitive positioning.

European Union Regulatory-Driven Market Development

European markets emphasise regulatory compliance and environmental performance, driving demand for graphene applications that meet strict safety and sustainability requirements. This regulatory focus creates opportunities for premium products with verified performance and safety characteristics.

Automotive sector requirements for lightweight, high-performance materials support graphene adoption in composite applications and electrical systems. European automotive manufacturers maintain technology leadership through advanced materials integration and performance optimisation.

Chemical industry integration in Europe focuses on specialty applications where graphene enhances product performance for demanding applications. These markets value technical support and application development capabilities alongside material performance.

North American Innovation Ecosystem Advantages

North American markets benefit from strong research and development capabilities, venture capital availability, and close collaboration between industry and academic institutions. This innovation ecosystem supports technology development and commercial scaling.

Aerospace and defence applications in North America drive demand for high-performance graphene materials meeting strict qualification requirements. These applications justify premium pricing while supporting technology advancement for broader commercial applications.

Industrial infrastructure requirements in North America, including data centres and energy systems, create substantial market opportunities for thermal management and electrical applications. These markets value performance improvements and operational efficiency gains, particularly as mineral production policy evolves to support domestic supply chains.

What Does the 2026-2030 Commercialisation Timeline Indicate?

Industry expansion plans and capacity development projects indicate accelerating commercialisation across multiple application areas and geographic markets. These developments suggest transition from niche applications toward mainstream industrial adoption.

Production Capacity Expansion Plans Across Key Players

Manufacturing capacity expansion projects demonstrate industry confidence in sustained demand growth and market development. Multiple companies plan significant production scaling that will increase global supply availability and reduce unit costs.

"Graphene production capacity is projected to increase 400% between 2026-2030, with synthetic production methods accounting for 65% of new capacity additions. Key expansion projects include North American facilities targeting automotive applications and Asian plants focused on electronics manufacturing."

Regional specialisation in capacity expansion reflects different market opportunities and competitive advantages. North American facilities emphasise high-quality applications while Asian capacity focuses on volume applications with optimised cost structures.

Technology improvements in production methodologies continue to reduce manufacturing costs and improve product consistency, supporting broader market penetration across price-sensitive applications.

Market Size Projections: From Niche to Mainstream Applications

Market growth projections indicate expansion from current niche applications toward mainstream industrial adoption across multiple sectors. This transition reflects improved cost competitiveness and proven performance in commercial applications.

Electronics and automotive sectors drive the largest growth projections, supported by increasing performance requirements and established supply chain integration. These markets demonstrate sustainable business models and scalable adoption patterns.

Construction and coatings applications provide substantial volume potential as cost reduction enables broader market penetration. These sectors offer large addressable markets with quantifiable value propositions for graphene integration.

Technology Convergence Opportunities with AI and Quantum Computing

Emerging technology convergence creates new application opportunities where graphene's properties enable advanced computing and sensing systems. These applications may drive premium market segments with substantial growth potential.

Artificial intelligence infrastructure requirements for improved processing speed and energy efficiency align with graphene's electrical and thermal properties. Data centre applications represent substantial market opportunities as AI adoption accelerates, supported by developments in graphene scale-up research.

Quantum computing development requires advanced materials with specialised electrical and thermal characteristics that graphene can provide. These applications represent early-stage opportunities with significant long-term potential as quantum technologies mature.

How Should Investors Evaluate Graphene Technology Companies?

Investment evaluation requires understanding both technological capabilities and commercial execution risks unique to advanced materials companies. Traditional technology investment frameworks may not capture all relevant factors for materials-based businesses.

Revenue Model Sustainability Assessment Criteria

Revenue model evaluation should examine customer concentration, contract duration, and pricing power sustainability across different market conditions. Materials companies face different competitive dynamics compared to software or service businesses.

Manufacturing scalability represents a critical evaluation factor, as production capacity constraints can limit growth potential while excessive capacity creates cost burdens. Optimal capacity planning requires understanding market development timelines and demand forecasting accuracy.

Intellectual property strength and freedom to operate analysis helps evaluate competitive positioning and potential licensing revenue opportunities. Patent portfolios should cover both production methods and application-specific innovations.

Intellectual Property Portfolio Strength Indicators

Patent portfolio evaluation should examine both breadth of coverage and commercial relevance of protected technologies. Academic research patents may have limited commercial value compared to application-specific innovations.

Freedom to operate analysis identifies potential patent infringement risks that could limit market access or create licensing obligations. This analysis requires specialised legal expertise and ongoing monitoring as new patents are granted.

Trade secret protection for manufacturing processes and application formulations may provide competitive advantages not captured in patent portfolios. Evaluating these intangible assets requires understanding operational capabilities and market positioning.

Manufacturing Scale-Up Risk Evaluation Framework

Scale-up risk assessment should examine both technical and financial challenges associated with transitioning from pilot to commercial production. Materials companies face unique scaling challenges compared to other technology sectors.

Technical scaling risks include maintaining product quality consistency, achieving target production costs, and implementing quality control systems. These technical challenges can significantly delay commercial timelines and increase capital requirements.

Financial scaling requirements often exceed initial projections due to equipment costs, facility development, and working capital needs. Understanding these capital requirements helps evaluate funding adequacy and potential dilution risks.

What Strategic Partnerships Define Industry Leadership?

Strategic partnership development indicates commercial progress and market validation for graphene technology companies. Partnership quality and customer relationships often determine competitive positioning more than technological capabilities alone.

Tier-1 Customer Validation as Competitive Advantage

Tier-1 customer relationships provide market validation and reference capabilities that facilitate broader market penetration. These relationships often require extensive technical qualification processes that create competitive barriers for other suppliers.

Major industrial customers typically require suppliers to meet strict qualification standards, quality systems, and supply chain reliability requirements. Companies meeting these standards gain competitive advantages through established relationships and proven capabilities.

Customer co-development programmes enable application-specific product optimisation and joint technology advancement. These collaborative relationships create switching costs and competitive differentiation beyond basic product performance.

Research Institution Collaboration Models

Academic partnerships provide access to advanced research capabilities and emerging technology developments that may create future commercial opportunities. These relationships require ongoing investment but can provide significant technological advantages.

University collaboration enables recruitment of specialised technical talent and access to research facilities that would be expensive to develop internally. These partnerships also provide credibility and technical validation for commercial development efforts.

Government research collaborations may provide funding opportunities and access to specialised testing facilities while supporting strategic technology development objectives. These partnerships often require long-term commitments and specific deliverable requirements.

Supply Chain Integration Strategies

Vertical integration strategies provide control over critical supply chain elements while requiring substantial capital investment and operational expertise. Companies must evaluate optimal integration levels based on competitive requirements and available resources.

Horizontal partnerships with complementary technology companies enable integrated solution development without requiring internal capability development. These partnerships can accelerate market development while sharing risks and costs.

Customer integration programmes help ensure supply chain alignment and reduce adoption barriers while creating closer commercial relationships. These programmes often require significant technical support investment but can generate competitive advantages.

Conclusion: Graphene's Transition from Promise to Performance

The graphene technology commercialisation landscape demonstrates a fundamental shift from research curiosity toward established industrial applications with proven value propositions. This transition reflects systematic progress in manufacturing capabilities, application development, and market acceptance rather than breakthrough technological developments.

Key Success Metrics for Commercial Viability

Commercial success increasingly depends on operational excellence, customer relationships, and manufacturing scale rather than pure technological innovation. Companies achieving sustainable market positions demonstrate consistent product quality, reliable supply capabilities, and application-specific performance optimisation.

Manufacturing cost competitiveness has become essential for market penetration across price-sensitive applications, requiring production scale and operational efficiency improvements. Technology differentiation remains important but insufficient without competitive cost structures and market execution capabilities.

Customer validation through tier-1 relationships and proven applications provides sustainable competitive advantages compared to laboratory performance claims. Market development requires substantial investment in customer support, application development, and industry relationship building.

Investment Risk-Reward Profile Evolution

Investment characteristics have evolved from high-risk research ventures toward manufacturing and commercial scaling opportunities with more predictable development timelines and market dynamics. This evolution attracts different investor categories with varying risk tolerance and return expectations.

Capital requirements for manufacturing scaling exceed typical technology startup funding needs, requiring institutional investment or strategic partnership arrangements. This capital intensity influences competitive positioning and market development strategies.

Market development timelines remain extended compared to software or service businesses but have become more predictable through established application validation and customer adoption patterns. Understanding these timelines enables more accurate investment evaluation and planning.

Long-Term Market Transformation Implications

Graphene adoption across multiple industrial sectors suggests potential for significant market transformation over extended timelines rather than rapid disruption. This gradual adoption pattern suits the capital-intensive nature of industrial equipment and infrastructure replacement cycles.

Technology convergence opportunities with artificial intelligence, quantum computing, and advanced manufacturing systems may create substantial new market opportunities beyond current applications. These emerging applications require continued technology development and market education investment.

Global supply chain development and manufacturing capacity expansion indicate industry maturation and transition toward mainstream industrial adoption. This infrastructure development supports continued market growth and cost competitiveness improvements across diverse application categories.

This analysis is based on publicly available information and industry reports. Investment decisions should consider additional factors and professional financial advice. Market projections involve inherent uncertainties and may not reflect actual future performance.

Looking to Capitalise on Advanced Materials Innovation?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. With graphene technology companies increasingly relying on high-grade graphite resources and strategic supply chains, understanding major mineral discoveries can provide crucial insights into materials sector developments. Begin your 14-day free trial today to position yourself ahead of the market's next breakthrough opportunity.