July 18, 2026

The Anode Supply Chain's Structural Blind Spot

Battery conversations tend to revolve around cathode chemistry. Which lithium iron phosphate formulation charges faster? Which nickel-manganese-cobalt blend delivers superior energy density? Yet quietly occupying the largest single volumetric position inside every lithium-ion cell is a material that rarely commands the same attention: graphite anode material. Natural graphite anodes account for roughly 95% of global anode supply by volume, and the overwhelming majority of that supply originates from a single geography. For battery manufacturers in Europe, North America, and Japan, this concentration is no longer a theoretical concern. It is an active procurement problem.

Understanding why Talga Group's (ASX:TLG, OTCQX:TLGRF) first Talga Talnode-C shipments to Nyobolt in July 2025 carry strategic weight requires stepping back from the announcement itself and examining what Western anode production has historically lacked: a commercially operational, vertically integrated alternative produced entirely outside of Asia.

When big ASX news breaks, our subscribers know first

Why the Graphite Anode Market Is Structurally Concentrated

China controls an estimated 70 to 80% of global natural graphite mining output and an even larger share of the downstream processing capacity required to convert raw graphite into battery-grade anode material. This processing dominance is the harder problem to solve. Mining graphite is one challenge. Purifying it to the 99.95%+ carbon purity levels required for anode applications, then shaping and surface-coating individual graphite particles to precise geometric and chemical specifications, requires proprietary process technology that took Chinese producers decades to refine.

The consequence is that even projects with access to high-quality graphite deposits outside Asia have historically struggled to replicate the full processing chain domestically. Most Western anode aspirants remain dependent on Chinese intermediaries for at least some processing steps, which directly undermines their ability to offer customers material that qualifies as free from foreign entities of concern under US and European procurement standards.

Furthermore, graphite supply shortages have intensified scrutiny on Western producers to accelerate their development timelines and deliver commercially viable alternatives at scale.

Regulatory frameworks including the US Inflation Reduction Act's FEOC provisions and the EU Battery Regulation are reshaping how battery manufacturers think about supply chain provenance. Material that cannot be traced through a fully documented, non-FEOC supply chain is increasingly disqualifying in government-adjacent procurement contexts, particularly for defence, grid storage, and mobility applications.

The EU Critical Raw Materials Act formally designated graphite as a critical raw material, creating a policy architecture that incentivises domestic production capacity. However, policy classification alone does not create supply. What closes the gap is commercially operational production, which is precisely what makes Talga's operational trajectory significant. In addition, rising critical minerals demand tied to the global energy transition is placing further urgency on establishing reliable non-Asian supply chains.

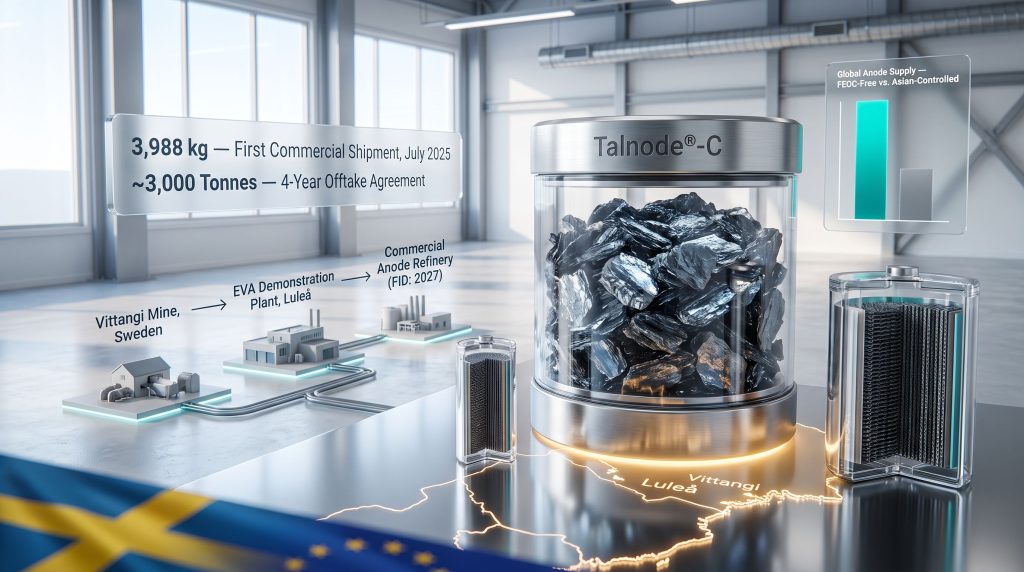

How Talga's Vittangi-to-Luleå Production Architecture Works

Talga's operational model is built around complete in-country vertical integration, distinguishing it from the partial-integration approaches that characterise most Western anode projects currently in development.

The production sequence works as follows:

- Mining stage: Natural graphite is extracted from the Vittangi deposit in Norrbotten County, northern Sweden. The deposit's geological characteristics are a material advantage. Vittangi hosts exceptionally high-grade flake graphite with a Total Graphitic Carbon content that positions it among the highest-grade natural graphite deposits globally, reducing the processing burden required to reach battery-grade purity.

- Purification and shaping: Graphite concentrate undergoes purification using Talga's proprietary processing technology developed in-house. Critically, this processing occurs within Sweden rather than being contracted to Asian processors, which is the step that most Western graphite companies cannot yet execute domestically.

- Surface coating: The shaped graphite particles are then coated to optimise electrochemical performance, completing the transformation into finished Talnode-C anode material ready for cell manufacturing qualification.

The entire chain, from bedrock to finished anode material, occurs within Sweden using proprietary technology. This is what makes Talga Talnode-C shipments meaningful as a supply chain benchmark rather than merely a commercial milestone for one company. Consequently, Europe's critical minerals supply chain now has a tangible domestic anchor from which to build broader anode supply security.

| Supply Model | Provenance Control | FEOC-Free Capability | Processing Location | Customer Qualification Risk |

|---|---|---|---|---|

| Vertically Integrated (Talga) | High | Yes | Fully in-country (Sweden) | Lower |

| Merchant Asian Processor | Low | No | China-dependent | High |

| Partial Western Integration | Medium | Conditional | Blended | Medium |

What Talnode-C Delivers Technically

Natural graphite anodes and synthetic graphite anodes are often discussed interchangeably, but their performance profiles diverge meaningfully in specific applications. Synthetic graphite, produced from petroleum coke at very high temperatures, offers consistent particle morphology but carries a significantly higher carbon footprint and cost trajectory. Natural graphite, when processed to battery grade, can achieve comparable or superior energy density at lower production energy input.

Hitachi Energy's life cycle assessment has further validated Talnode-C as the world's greenest graphite anode product, reinforcing the environmental credentials that are increasingly relevant to European procurement standards.

Where Talnode-C is specifically optimised is in high-power performance. The material's particle engineering targets ultra-fast charging and rapid discharge capability, which are the critical parameters in applications where charging speed or discharge rate, rather than simple energy capacity, determines product viability. These include:

- Industrial and humanoid robotics: Platforms requiring high cycle durability and burst discharge capability during peak load operations

- AI infrastructure backup systems: Data centre uninterruptible power systems where rapid response and energy density intersect

- Defence and commercial UAVs: Drone platforms where weight-to-power ratios and discharge rates are engineering constraints

- Grid-scale fast-response storage: Applications where response times rather than stored energy volume determine market value

Breaking Down the First Commercial Talga Talnode-C Shipments

The first commercial Talga Talnode-C shipments, comprising 3,988 kilograms of finished anode material, were dispatched from the EVA demonstration plant in Luleå, Sweden, in early July 2025. The recipient was Nyobolt, a battery technology company whose product architecture is specifically designed around ultra-fast charging systems, making the performance alignment between customer requirements and Talnode-C's technical profile strategically coherent rather than opportunistic.

The binding offtake agreement underpinning this shipment carries several characteristics worth examining carefully:

- Total committed volume: Approximately 3,000 tonnes of Talnode-C over the agreement term

- Contract duration: Four years, commencing 13 May 2025

- Pricing structure: Fixed commercial pricing for the full four-year term

- Supply source evolution: Initial volumes from the EVA demonstration plant; bulk of the contracted volume planned from a commercial-scale Anode Refinery

Fixed-price, multi-year offtake agreements serve a function that extends well beyond revenue predictability. For a development-stage project seeking project financing, a binding offtake from a creditworthy counterparty is one of the primary instruments that project lenders use to underwrite loan facilities. The Nyobolt agreement therefore functions simultaneously as a commercial contract and a project financing instrument.

The Two-Phase Supply Structure

An aspect of the Nyobolt agreement that deserves specific attention is the planned transition between supply sources across the contract term.

| Supply Phase | Source Facility | Indicative Volume | Timeline | FID Dependency |

|---|---|---|---|---|

| Phase 1 | EVA Demonstration Plant, Luleå | Initial shipments including 3,988 kg first delivery | From July 2025 | No |

| Phase 2 | Commercial-Scale Anode Refinery, Northern Sweden | Bulk of ~3,000t committed volume | From approximately 2027 | Yes |

Phase 2 supply is contingent on a Final Investment Decision for the commercial-scale Vittangi Anode Refinery. FID milestones of this type typically require a convergence of three conditions: sufficient offtake coverage to support debt service, confirmed financing commitments from lenders or strategic partners, and completed permitting. The Nyobolt agreement advances the first condition. The remaining conditions constitute the forward execution risk that investors should weigh carefully.

The High-Power Application Stack and Why It Matters

One of the less-discussed aspects of Talga's commercial strategy is its deliberate focus on high-power application markets rather than mainstream EV battery supply chains. This positioning reflects both a technical fit and a strategic calculation.

The mainstream EV anode market is heavily contested, with well-capitalised Asian producers offering established supply chains and competitive pricing. Competing directly on cost in that market, before Western processing capacity has reached scale, is structurally difficult. High-power specialty applications, by contrast, prioritise performance characteristics and supply chain provenance over price.

Defence-adjacent and government-linked procurement increasingly requires FEOC-free material regardless of cost premiums. Furthermore, the broader pressures created by China's export restrictions on critical materials have reinforced how urgently Western buyers need credible alternatives across the entire battery raw materials value chain.

Robotics and AI infrastructure customers face deployment timelines that make qualification delays more costly than material price differences. Nyobolt's own positioning as an ultra-fast charging battery system developer reflects exactly this demand profile. Its customers are not selecting battery technology on kilowatt-hour cost per unit. They are selecting on charge time, cycle performance, and, increasingly, supply chain integrity.

What the Commercial Launch Signals to the Market

Three structural shifts are embedded in the Talga Talnode-C shipments milestone that are worth framing distinctly:

- Proof of commercial-grade production outside Asia: The EVA demonstration plant in Luleå has now demonstrated the ability to produce and deliver battery-grade anode material meeting customer specifications at a commercial fixed price. This transitions Talga from a pre-revenue development company to an active materials supplier.

- A fixed-price revenue foundation for project financing: Four years of locked pricing creates a financial instrument that project lenders can model. This is qualitatively different from letters of intent or memoranda of understanding that have no binding pricing or volume commitment.

- Validation of FEOC-free anode material as a real procurement alternative: The fact that a sophisticated battery technology customer selected Talnode-C under a binding multi-year agreement establishes a proof point that FEOC-free natural graphite anode material is commercially viable at production scale.

Looking ahead, Talga has indicated it is actively pursuing additional offtake agreements across European, US, and Japanese markets, alongside engagement with strategic investors and financing partners for the Vittangi Anode Refinery. The pace at which further offtake coverage is secured — alongside progress in battery raw materials procurement across the Western world — will be a primary determinant of whether the 2027 construction timeline holds. Talga's official product page provides further detail on the full range of battery materials the company is developing beyond Talnode-C.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Talga Talnode-C and the Vittangi Anode Project

What exactly is Talnode-C?

Talnode-C is Talga Group's proprietary finished graphite anode material, produced from natural graphite mined at the Vittangi deposit in northern Sweden and processed using the company's own purification and surface-coating technology. It is engineered for high-power battery applications requiring fast charge and rapid discharge performance.

Why is Nyobolt a strategically significant first customer?

Nyobolt develops ultra-fast charging battery systems for demanding applications where standard battery chemistry cannot meet the required charge rates. Its technical requirements align directly with Talnode-C's high-power performance profile, making the qualification and binding offtake a meaningful endorsement of the material's commercial readiness.

How much Talnode-C has Talga shipped under the agreement?

The first commercial shipment totalled 3,988 kilograms, dispatched from the Luleå EVA demonstration plant in July 2025. The total committed volume under the four-year Nyobolt agreement is approximately 3,000 tonnes.

When will the commercial-scale Anode Refinery begin operating?

Construction commencement is targeted for 2027, conditional on a successful Final Investment Decision. FID is in turn conditional on finalising offtake coverage, project financing, and permitting milestones.

What makes Talnode-C genuinely FEOC-free?

The complete production chain, from graphite mining through purification, shaping, and surface coating, is conducted within Sweden using Talga's own process technology. There is no reliance on Chinese processing intermediaries at any stage of production, which is the defining characteristic of FEOC-free anode material under applicable US and European procurement frameworks.

This article is for informational purposes only and does not constitute financial or investment advice. Forward-looking statements regarding project timelines, financing, and commercial outcomes involve risks and uncertainties. Readers should conduct independent due diligence before making investment decisions.

Want to Track the Next Major ASX Mineral Discovery as It Happens?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across critical minerals, battery materials, and beyond, turning complex geological data into actionable investment insights for traders and long-term investors alike. Explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial market returns, then begin your 14-day free trial to position yourself ahead of the broader market.